Vanguard LifeStrategy

Discussion

Without wanting to prolong the argument, for someone like me who has 1 btl (and many of us out there like this since getting married etc) the ability to buy commercial property within a sipp is unrealistic. I know nothing about commercial property, or the costs, and any sellers would see me coming. I’d doubtless end up with an empty unit no one wants to rent, losing money (within or with It a sipp).

So I regard that aspect as not possible. Also with my 1 (mortgaged) btl I doubt if it’s worth selling and investing the released money in a fund within a sipp as I doubt it will perform as well in the long run as a property? (admittedly in NW london so constant upward pressure of population). Property in London has more or less been a one way bet up till now.

So I regard that aspect as not possible. Also with my 1 (mortgaged) btl I doubt if it’s worth selling and investing the released money in a fund within a sipp as I doubt it will perform as well in the long run as a property? (admittedly in NW london so constant upward pressure of population). Property in London has more or less been a one way bet up till now.

Groat said:

JulianPH said:

I don't think we need to have an online argument about this!!!

I remember leaving primary school in the 80's, so wasn't up to date with properties back then

My "pension" is completely maxed out now. You certainly have a point with regards to the limitations (thought these are due to the huge tax breaks on offer - not the products themselves).

Just give me a bell mate!

1) who's arguing? Don't worry, you'll know when it's arguing. When the family argues, out come the uzis....I remember leaving primary school in the 80's, so wasn't up to date with properties back then

My "pension" is completely maxed out now. You certainly have a point with regards to the limitations (thought these are due to the huge tax breaks on offer - not the products themselves).

Just give me a bell mate!

2) tax manipulating is considered most non-U these days.....unethical almost. How do you expect to have good public services/NHS/schools etc with all this tax-dodging going on? Disgraceful!

3)A bell! A bell! I know what you're after and I know a cold call when I hear one! Scary!

4) Very rarely drink beer. Mine's a wine. Currently (well a bit later) a Chateau Batailley Pauillac 2009. Preferably without food.

5) Due to a huge change in immediate financial circumstances which required a brief return to what I laughably refer to as "work", it is now likely, said circumstances having been turned around, that before the end of the year (possibly earlier) all "investing" aka wasting money on property having been banned by 'er indoors, a certain amount of groats may require safe management. The question is, with a close relative who is the ned board chairman of not one but two of the world's biggest investment companies and with whom I am on the best of terms, should I place this very un-hard earned pile with these multi-trillion dollar institutions, or with a Nottingham backstreet outfit run by a geezer I met on t'internet. No brainer really. So unless something seriously wayward happens (which, in fairness, is about once a week on Planet Groat) you (or, more likely, whichever accomplice actually mans the gaff) may expect a call. Though, I emphasise, not for a while. And, of course, not without dilemma and drama though hopefully avoiding trauma.

You and I both know if we were in the same neck of the woods we would happily meet us for a beer and put the world to rights.

Consider what I have said about the tax allowance you know as a pension. I take on board what you say about BTLs.

Now let's stop getting in the way of this thread!

So if you were 47 years old and had £35k to put away for 10 years+ without needing access to it, it would make reasonable sense to stick it in to a SIPP as the Government would increase it by 22% for a lower rate taxpayer and 40% for a higher rate tax payer? With the chance of higher compounding of dividends before having access to funds after 55.

Or am I getting the wrong end of the stick?

And what way does the 40% contribution from taxman work, would it be worth changing some salary sacrifice & company car to a higher CO² one to dip into the 40% tax rate for a year?

Or am I getting the wrong end of the stick?

And what way does the 40% contribution from taxman work, would it be worth changing some salary sacrifice & company car to a higher CO² one to dip into the 40% tax rate for a year?

This is an actual vanguard question, that I hold with HL. If I want to transfer my child’s Junior SIPP from 100% lifestrategy to 60% lifestrategy, what does it cost? I can’t see.

https://www.hl.co.uk/pensions/junior-sipp/junior-s...

Is it £25 to ‘transfer out’ to another holding (even if this is within HL?) is that the total cost, does anyone know?

https://www.hl.co.uk/pensions/junior-sipp/junior-s...

Is it £25 to ‘transfer out’ to another holding (even if this is within HL?) is that the total cost, does anyone know?

CoolHands said:

This is an actual vanguard question, that I hold with HL. If I want to transfer my child’s Junior SIPP from 100% lifestrategy to 60% lifestrategy, what does it cost? I can’t see.

https://www.hl.co.uk/pensions/junior-sipp/junior-s...

Is it £25 to ‘transfer out’ to another holding (even if this is within HL?) is that the total cost, does anyone know?

I’m not sure, but if you’re sticking with Vanguard, or making Vanguard-to-Vanguard transfers, it really doesn’t make sense to use HL as an intermediary - although I know it’s nice to have everything in one place.https://www.hl.co.uk/pensions/junior-sipp/junior-s...

Is it £25 to ‘transfer out’ to another holding (even if this is within HL?) is that the total cost, does anyone know?

Direct with Vanguard, you’ll pay around 0.44% annually (including the platform cost of using them directly), whereas with HL, you’re paying the Vanguard management fee plus HL’s platform fee of (I think) 0.45%.

Edited to add: found this on the Vanguard website:

Edited by Testaburger on Monday 22 July 04:25

Yeah appreciate that but at the moment they don’t offer a pension. They’re ’working on it’ and claim it will be ready soon.

https://www.vanguardinvestor.co.uk/need-help/answe...

The charge shown on hl for the LS fund is 0.22% ‘net ongoing charge’ + the hl charge if 0.45%. So if Vanguard launch with same costs as you quote it would save 0.23%

I imagine fund managers will be peed off when they do.

https://www.vanguardinvestor.co.uk/need-help/answe...

The charge shown on hl for the LS fund is 0.22% ‘net ongoing charge’ + the hl charge if 0.45%. So if Vanguard launch with same costs as you quote it would save 0.23%

I imagine fund managers will be peed off when they do.

Edited by CoolHands on Monday 22 July 07:58

Edited by CoolHands on Monday 22 July 07:59

CoolHands said:

Yeah appreciate that but at the moment they don’t offer a pension. They’re ’working on it’ and claim it will be ready soon.

https://www.vanguardinvestor.co.uk/need-help/answe...

The charge shown on hl for the LS fund is 0.22% ‘net ongoing charge’ + the hl charge if 0.45%. So if Vanguard launch with same costs as you quote it would save 0.23%

I imagine fund managers will be peed off when they do.

Apologies mate. Thought you said Junior ISA. https://www.vanguardinvestor.co.uk/need-help/answe...

The charge shown on hl for the LS fund is 0.22% ‘net ongoing charge’ + the hl charge if 0.45%. So if Vanguard launch with same costs as you quote it would save 0.23%

I imagine fund managers will be peed off when they do.

Edited by CoolHands on Monday 22 July 07:58

Edited by CoolHands on Monday 22 July 07:59

As you were!

CoolHands said:

This is an actual vanguard question, that I hold with HL. If I want to transfer my child’s Junior SIPP from 100% lifestrategy to 60% lifestrategy, what does it cost? I can’t see.

https://www.hl.co.uk/pensions/junior-sipp/junior-s...

Is it £25 to ‘transfer out’ to another holding (even if this is within HL?) is that the total cost, does anyone know?

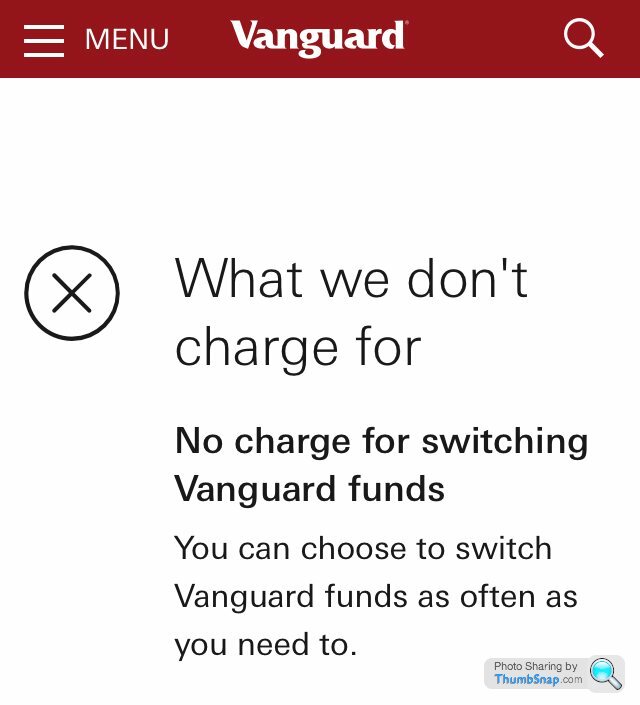

If you're just swtiching funds within HL it doesn't cost anything (see the Dealing Charges section of the page you linked to).https://www.hl.co.uk/pensions/junior-sipp/junior-s...

Is it £25 to ‘transfer out’ to another holding (even if this is within HL?) is that the total cost, does anyone know?

Sambucket said:

Mr Pointy said:

If you're just swtiching funds within HL it doesn't cost anything (see the Dealing Charges section of the page you linked to).

I do wonder if there is a hidden cost, either a spread, or something a bit steathier when switching similar funds within HL or VG?Sambucket said:

I do wonder if there is a hidden cost, either a spread, or something a bit steathier when switching similar funds within HL or VG?

From the HL website there's no spread on the Vanguard funds:https://www.hl.co.uk/funds/fund-discounts,-prices-...

Right another Vanguard LS question.

My dad died a few years ago leaving my mum with a whole bunch of funds in a S&S ISA.

On his death bed he suggested I move it all to Vanguard LS 40 for her to simplify the management.

Can anyone comment on the risk involved in moving all her eggs from one platform (but spread across many funds), to a single fund with a single platform?

Is there a risk that Vanguard does a Woodford?

Should I be looking to have a spread of LS-like funds on a couple of platforms instead?

My dad died a few years ago leaving my mum with a whole bunch of funds in a S&S ISA.

On his death bed he suggested I move it all to Vanguard LS 40 for her to simplify the management.

Can anyone comment on the risk involved in moving all her eggs from one platform (but spread across many funds), to a single fund with a single platform?

Is there a risk that Vanguard does a Woodford?

Should I be looking to have a spread of LS-like funds on a couple of platforms instead?

was8v said:

Right another Vanguard LS question.

My dad died a few years ago leaving my mum with a whole bunch of funds in a S&S ISA.

On his death bed he suggested I move it all to Vanguard LS 40 for her to simplify the management.

Can anyone comment on the risk involved in moving all her eggs from one platform (but spread across many funds), to a single fund with a single platform?

Is there a risk that Vanguard does a Woodford?

Should I be looking to have a spread of LS-like funds on a couple of platforms instead?

There’s zero chance of Lifestrategy doing a Woodford, for a few reasons. Chiefly, though, is that LS is diversified globally across several thousand companies and in fact, other funds. It’s then frequently balanced by their managers to maintain the sector/geographic weightings.. It may go down as well as up, but the idea behind it is that it will outperform global growth. Woodford has/had 105 (I think) holdings, many of them illiquid, and very risky. Think biotech startups. My dad died a few years ago leaving my mum with a whole bunch of funds in a S&S ISA.

On his death bed he suggested I move it all to Vanguard LS 40 for her to simplify the management.

Can anyone comment on the risk involved in moving all her eggs from one platform (but spread across many funds), to a single fund with a single platform?

Is there a risk that Vanguard does a Woodford?

Should I be looking to have a spread of LS-like funds on a couple of platforms instead?

It’s also very cheap to invest in, and I’ve found their customer services people excellent.

Also look up Intelligent Money on PH. They offer a couple of alternatives to LS and their head honcho (Julian) is on here, and is always more than willing to give you helpful advice and pointers.

Testaburger said:

There’s zero chance of Lifestrategy doing a Woodford, for a few reasons. Chiefly, though, is that LS is diversified globally across several thousand companies and in fact, other funds. It’s then frequently balanced by their managers to maintain the sector/geographic weightings.. It may go down as well as up, but the idea behind it is that it will outperform global growth. Woodford has/had 105 (I think) holdings, many of them illiquid, and very risky. Think biotech startups.

It’s also very cheap to invest in, and I’ve found their customer services people excellent.

Also look up Intelligent Money on PH. They offer a couple of alternatives to LS and their head honcho (Julian) is on here, and is always more than willing to give you helpful advice and pointers.

OK thanks for this. I suppose if Vanguard themselves went bust, your investments are held in underlying companies so could be reclaimed?! But the world would have to come to an end for that to happen?It’s also very cheap to invest in, and I’ve found their customer services people excellent.

Also look up Intelligent Money on PH. They offer a couple of alternatives to LS and their head honcho (Julian) is on here, and is always more than willing to give you helpful advice and pointers.

Intelligent Money, I looked at the website - I don't truly understand how to compare them to Vanguard, can you help?

You’re most welcome. Oh your first point, yes - reclaiming them might be an administrative chore (I honestly don’t know), but yes, you own all the little slices of the underlying companies in the Lifestrategy portfolio. The odds of Vanguard going under, however, are similar to the odds of me swimming the Pacific.

There’s a big thread on IM hosted by the company owner, but I appreciate it’s now become very long. I could have a go at explaining it, but I’ve no doubt he’ll be along to explain it clearer than anyone else can.

The Cliff Notes version is that, again, their ‘flagship’ product a fund with an enormous number of constituent holdings that’s global and balanced. Where it differs from LS is that it on top of passively tracking markets (like LS), it also holds proportions of other stuff such as commercial property and gold. The management are able to vary the allocation between these, as market conditions change. In essence, you’ve got something a bit more nimble and adaptable than purely passively tracking the market.

It’s a little more expensive - because there’s more hands-on management, but you also get personal financial planning services, which makes it extremely good value.

Disclaimer - I’m not an affiliate or a customer of IM (I’m an overseas resident so it’s not open to me), but I knew of IM in the fund marketplace previously, and have been subsequently very impressed with what I’ve learned about their product, service offering & demeanour since they introduced it to PH a little while back.

It may be worth popping a note in the IM sticky thread and pointing him (JulianPH) to to this thread.

Julian!

Julian!

There’s a big thread on IM hosted by the company owner, but I appreciate it’s now become very long. I could have a go at explaining it, but I’ve no doubt he’ll be along to explain it clearer than anyone else can.

The Cliff Notes version is that, again, their ‘flagship’ product a fund with an enormous number of constituent holdings that’s global and balanced. Where it differs from LS is that it on top of passively tracking markets (like LS), it also holds proportions of other stuff such as commercial property and gold. The management are able to vary the allocation between these, as market conditions change. In essence, you’ve got something a bit more nimble and adaptable than purely passively tracking the market.

It’s a little more expensive - because there’s more hands-on management, but you also get personal financial planning services, which makes it extremely good value.

Disclaimer - I’m not an affiliate or a customer of IM (I’m an overseas resident so it’s not open to me), but I knew of IM in the fund marketplace previously, and have been subsequently very impressed with what I’ve learned about their product, service offering & demeanour since they introduced it to PH a little while back.

It may be worth popping a note in the IM sticky thread and pointing him (JulianPH) to to this thread.

Julian!Edited by Testaburger on Tuesday 23 July 05:53

OK thanks.

I'm assuming IM cautious is pitched to the same market as LS40. Hard to tell from their pie charts what the mix is, but it looks like its about 45% equities in IM cautious.

Here is IM historical performance from the website https://www.intelligentmoney.com/private-clients/o...

M Optimum Cautious 1y 4.3% 3y 18.4% 5y 36.1% 10y 144.6% annualised 9.36%

And LS40

LS40 1y 6.60 3y 19.66 5y 40.35 10y - since inception 75.00

If my working out that the mix of equities / other (and hence "risk") is similar then LS40 has done much better historically - obviously usual crystal ball caveats apply.

I'm a little naive so please do correct me if wrong. I'm finding there is a LOT of jargon, and different ways of presenting things that seem designed to make it more difficult than it could be for an educated person to make a decision.

I'm assuming IM cautious is pitched to the same market as LS40. Hard to tell from their pie charts what the mix is, but it looks like its about 45% equities in IM cautious.

Here is IM historical performance from the website https://www.intelligentmoney.com/private-clients/o...

M Optimum Cautious 1y 4.3% 3y 18.4% 5y 36.1% 10y 144.6% annualised 9.36%

And LS40

LS40 1y 6.60 3y 19.66 5y 40.35 10y - since inception 75.00

If my working out that the mix of equities / other (and hence "risk") is similar then LS40 has done much better historically - obviously usual crystal ball caveats apply.

I'm a little naive so please do correct me if wrong. I'm finding there is a LOT of jargon, and different ways of presenting things that seem designed to make it more difficult than it could be for an educated person to make a decision.

Edited by was8v on Tuesday 23 July 10:21

Testaburger said:

Julian!An excellent description and many thanks for the mention.

I would also like to confirm that we only know each other over the years on PH and whilst we plan to meet when you are next in the UK we have never met, spoken on the phone, emailed or even PMed each other and are in no way affiliated.

was8v said:

OK thanks.

I'm assuming IM cautious is pitched to the same market as LS40. Hard to tell from their pie charts what the mix is, but it looks like its about 45% equities in IM cautious.

Here is IM historical performance from the website https://www.intelligentmoney.com/private-clients/o...

M Optimum Cautious 1y 4.3% 3y 18.4% 5y 36.1% 10y 144.6% annualised 9.36%

And LS40

LS40 1y 6.60 3y 19.66 5y 40.35 10y - since inception 75.00

If my working out that the mix of equities / other (and hence "risk") is similar then LS40 has done much better historically - obviously usual crystal ball caveats apply.

I'm a little naive so please do correct me if wrong. I'm finding there is a LOT of jargon, and different ways of presenting things that seem designed to make it more difficult than it could be for an educated person to make a decision.

Hi, I am very concious on not wanting to break PH rules so will answer the points you raise and suggest we move to the IM thread or you PM me for anything further.I'm assuming IM cautious is pitched to the same market as LS40. Hard to tell from their pie charts what the mix is, but it looks like its about 45% equities in IM cautious.

Here is IM historical performance from the website https://www.intelligentmoney.com/private-clients/o...

M Optimum Cautious 1y 4.3% 3y 18.4% 5y 36.1% 10y 144.6% annualised 9.36%

And LS40

LS40 1y 6.60 3y 19.66 5y 40.35 10y - since inception 75.00

If my working out that the mix of equities / other (and hence "risk") is similar then LS40 has done much better historically - obviously usual crystal ball caveats apply.

I'm a little naive so please do correct me if wrong. I'm finding there is a LOT of jargon, and different ways of presenting things that seem designed to make it more difficult than it could be for an educated person to make a decision.

You are right the IM Optimum Cautious is similar in its equity exposure to LS40. Vanguard LS40 has done better over recent times, but that is to be fully expected in a rising bull market.

IM Optimum is designed to put capital preservation first and has active asset allocation management and provided you with your own named account manager to assist you with all financial matters. So a Vanguard comparison is not a like for like one. A 10 year average annualised return for a cautious portfolio (as you point out) of 9.36% is pretty excellent going given tha additional benefits of being an IM Private Client.

By way of an example of active asset allocation we recently made several changes to our portfolios as I was concerned that we were facing (on top of each other) a new Prime Minister, political uncertainty in general and more specifically with regard to Brexit, increasing tensions with Iran, the knock on effect of increased oil prices and reduced availability with the economic impact this may have on China (an other factors).

We are therefore able to reflect such concerns in our IM Optimum portfolios in a way that Vanguard simply can't.

If you wanted a real like for like comparison then consider the IM Index funds we are about to launch (the below is the actual performance that this would have delivered after all charges, with both IM and LS figures to 30/6/2019):

| 1 Year Return | 3 Year Return | 5 Year Return | |

| IM Index 40 | 8.73% | 28.32% | 63.36% |

| Vanguard LS 40 | 6.6% | 19.66% | 40.35% |

This is a better comparison with VL40 and as you can see has generated massive out performance (and still comes with your Private Client Manager).

You are certainly right about about there being a lot of jargon and the industry deliberately designing things to make them seem as difficult as possible for people to understand. That is something we try to slice through and if you have a look on the IM thread you will see we do just that.

I hope this addresses your points and just want to say again this was a genuine answer to your genuine questions and in no way designed to be advertise IM.

I am in a no win situation here as if I don't answer when asked to I will seem evasive and unhelpful, yet if I do I will be accused of self promotion.

I think in this case it is pretty obvious to anyone I am simply trying to make a helpful contribution by simply answering the questions and addressing the points raised above. For anything else please quote this on the IM sticky and we can take the discussion their.

Cheers

Gassing Station | Finance | Top of Page | What's New | My Stuff