What to do with c£1k/month

Discussion

KTF said:

some overpayments above a certain limit attract a penalty.

And so does holding cash attract a penalty. Whether in Marcus or in Premium bonds it's 99.9% likely that cash will be shrinking with inflation.It's a good idea to crunch the numbers for a clear picture of which is likely to be cheaper in the long run.

Dave. said:

zero pension, but she's an only child and her folks have enough to see her through.

Yeah, but you could be squeezing some useful tax efficiency out of that. i.e. Perhaps the folks suppressing 40% IHT at the same time SWMBO was pocketing tax relief from the government and working towards a nice tax free lump sum.chibbard said:

What doesn't compute with me is when people say they have a £1000 spare each month but an 100K mortgage. It's a no brainer, overpay the mortgage by £1000 because until this is paid, you don't have "spare" money. Sorry, just don't get it. I'll probably never understand other peoples logic.

Because if you invest it well you stand to beat the interest rate on the debt.With a mortgage of less than 2% I’m happy to invest rather than overpay. This could change if interest rate changes happen but it’s worked out well over the last few years...

Dave. said:

Can you repeat that for a dumbass please?

Well put. There are no stupid question in the world of finance.- Let's assume the "folks" may eventually be charged 40% IHT (Inheritance Tax) on some of their estate after death.

- They can make exempt gifts now to SWMBO of £3,000 a year completely outside the scope of IHT.

- They can also make larger gifts which will, so long as the folks survive for 7 years, fall outside the scope of IHT.

- ISA - up to £20,000 p.a. All income and growth tax free.

- SIPP - amount depends on earnings but is £3,600 p.a. even for a non-earner. All income and growth tax free. 25% tax free lump sum available at retirement.

I hope this outline answer is helpful. Inevitably there are nuances which vary with the circumstances of the people involved.

Rockin

GR_TVR said:

chibbard said:

What doesn't compute with me is when people say they have a £1000 spare each month but an 100K mortgage. It's a no brainer, overpay the mortgage by £1000 because until this is paid, you don't have "spare" money. Sorry, just don't get it. I'll probably never understand other peoples logic.

Because if you invest it well you stand to beat the interest rate on the debt.With a mortgage of less than 2% I’m happy to invest rather than overpay. This could change if interest rate changes happen but it’s worked out well over the last few years...

Ari said:

Ah, the mythical Pistonheads perpetual motion money tree. Yup, if you can ever find the forrest where these live then it makes sense to max out every avenue of credit and invest invest invest. Don't forget to PCP the cars too.

That's not really what he is suggesting though?He is suggesting investing the SPARE £1000 per month rather than overpaying the mortgage. The rate of return for investing it over the last several years would have easily outperformed a mortgage at less than 2% interest, plus you can access the money should you need it in an emergency (which wouldn't be so easy if you had ploughed it all into mortgage overpayments).

It's exactly what he's suggesting. Borrow here and invest it there, get a better investment return than the borrowing costs. The famous PH mythical money tree, it gets trotted out on every PCP thread where PBDs are financing expensive cars 'because I can get a better return investing the money than the cost of borrowing it'.

I've asked a couple of times where this tree is, answers have so far proved vague...

I've asked a couple of times where this tree is, answers have so far proved vague...

I think you should actually read what he said, because all he is talking about is using the spare money to invest instead of overpaying a mortgage:

chibbard said:

What doesn't compute with me is when people say they have a £1000 spare each month but an 100K mortgage. It's a no brainer, overpay the mortgage by £1000 because until this is paid, you don't have "spare" money. Sorry, just don't get it. I'll probably never understand other peoples logic.

the other bloke said

Because if you invest it well you stand to beat the interest rate on the debt.

With a mortgage of less than 2% I’m happy to invest rather than overpay. This could change if interest rate changes happen but it’s worked out well over the last few years...

And bearing in mind the OP has already said he overpays the mortgage by the most he can without getting a penalty, investing it makes even more sense

chibbard said:

What doesn't compute with me is when people say they have a £1000 spare each month but an 100K mortgage. It's a no brainer, overpay the mortgage by £1000 because until this is paid, you don't have "spare" money. Sorry, just don't get it. I'll probably never understand other peoples logic.

the other bloke said

Because if you invest it well you stand to beat the interest rate on the debt.

With a mortgage of less than 2% I’m happy to invest rather than overpay. This could change if interest rate changes happen but it’s worked out well over the last few years...

And bearing in mind the OP has already said he overpays the mortgage by the most he can without getting a penalty, investing it makes even more sense

anonymous said:

[redacted]

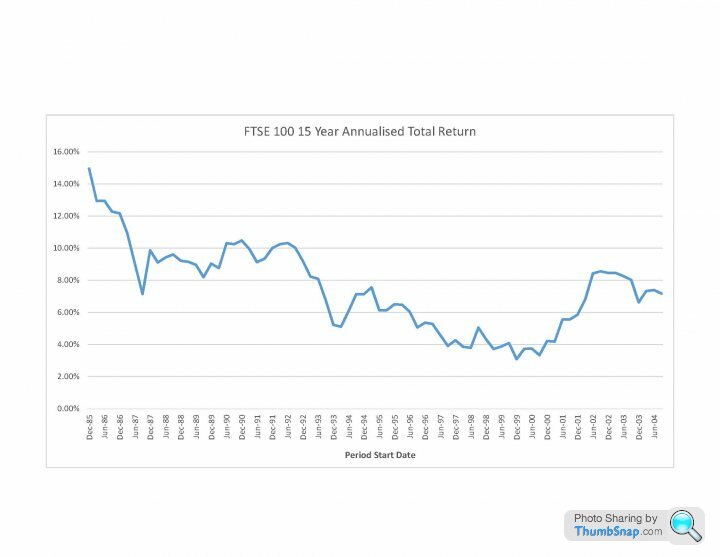

I just ran the numbers for each 15 year period starting on a FTSE 100 trading day between Dec-85 (i.e. when Bloomberg's FTSE 100 data starts) and Jun-04 (i.e. just ended). The annualised total return (i.e. including dividends) is almost always above 4%, but I imagine average mortgage rates during that time period would have been higher. Probably safe at low LTV (30-50%) but too high and it gets worrying.

anonymous said:

[redacted]

Classic PH... thanks for letting us know Gassing Station | Finance | Top of Page | What's New | My Stuff