What to do with c£1k/month

Discussion

anonymous said:

[redacted]

This is a very valid point. The same logic would dictate that you shouldn't start saving into a pension until you had cleared your mortgage off!The reality is all about balance.

Dave. - You said in your OP you were originally going to post this in the Intelligent Money thread, so we will come to you instead!

A mortgage is not simply debt, it is providing you and your family with a home. Obviously you want to have paid this off before you retire - as this considerably lowers your income requirements in retirement (and therefore the the strain on your pension/ISA contributions whilst you are working).

You are doing all the right things and have identified that cash is going to give you a terrible return (indeed you will lose money to inflation).

Putting this money in a S&S ISA (or a pension if you have any remaining allowance - particularly if the £1,000 a month is taxed at the higher rate) creates such balance over the long term.

15 years worth of ISA contributions at a 7% average annual return would net you an additional £312,863 for your retirement.

The same in a pension would be worth £391,079 (due to the addition on basic rate tax relief.

Obviously no one knows what future returns will be, but I went with 7% as it is the half way point between the 10% average annual return IM has delivered over the last 10 years and the much lower 4% return that has been used above.

If you would like a comparison between the Vanguard approach and the IM one please ask on the IM thread and I will be happy to help there (I wouldn't want to break forum rules here).

You equally can't go wrong with Vanguard.

Cheers!

anonymous said:

[redacted]

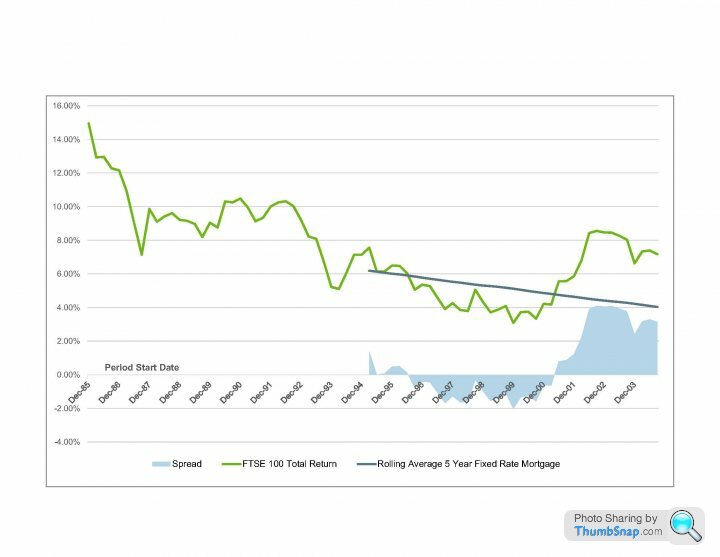

Right on rates but obviously you pay a spread on your mortgage.I added the mortgage rate data to my chart - Bloomberg only goes back to 1995 so we only have the period 1995 - 2004 to look at.

I use the 5 year fixed rate (just because that's what I've always gone for) but others are available. Data shows that about 50% of the time you would be worse off in the FTSE 100 (i.e. starting 1995 - 2000 due to the dotcom crash and 2007 crash), whereas starting in 2000-2004 you would be better off in the FTSE 100 (gains in the last 3-4 years have outweighed 2007).

Annual carry of 4% (i.e. 2001 and 2002 start years) would be huge over 15 years on the size of the average mortgage!

Obviously this doesn't take into account tax deltas. For higher rate taxpayers that should have full ISAs and be capped on pension contributions through tapering, this will eliminate much of the available gains.

Gassing Station | Finance | Top of Page | What's New | My Stuff