State Pension potential shortfall warning

Discussion

Phooey said:

I must be really thick because for the life of me I can't understand how to create a government gateway id / log-in account

I hate having to ring the accountants for (what should be) simple stuff like this. How the f k do you get into it??

k do you get into it??

https://www.gov.uk/personal-tax-accountI hate having to ring the accountants for (what should be) simple stuff like this. How the f

k do you get into it??Jasey_ said:

Fantastic - thanks mate! Not sure where I went wrong earlier but actually really quick and straight forward to access ( when you use the correct webpage

)

)

i4got said:

uknick said:

Does your state pension estimate/statement mention any amount for COPE?

If not, and they say you'll get the full £168 at today's prices, fair enough.

However, this means you've never been part of a occupational pension scheme for which you were opted out of SERPS and as a result paid reduced NI contributions from 1988 to 2016.

Nothing about COPE.If not, and they say you'll get the full £168 at today's prices, fair enough.

However, this means you've never been part of a occupational pension scheme for which you were opted out of SERPS and as a result paid reduced NI contributions from 1988 to 2016.

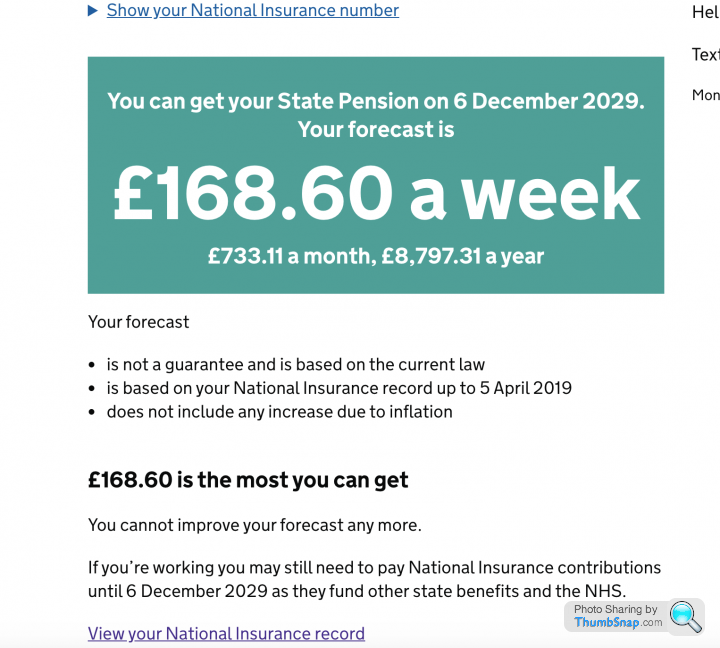

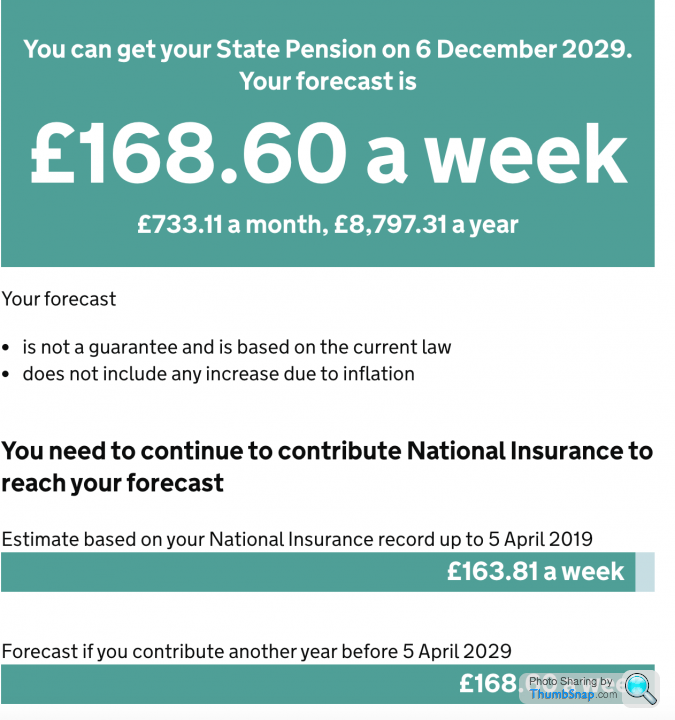

The screen shots in my prior message above showed that I had already qualified for full pension and no COPE amount was shown on the gov site.

The forecast has now come through and it is different to what was shown on the web site in two areas.

1) It says that I need to make one more years contribution to get the full pension.

2) It shows a COPE amount of £53.13 per week.

The online forecast has now also changed to reflect the information I received by post.

So its pretty safe to say that my original estimate was wrong and only by requesting the written forecast has it been corrected.

i4got said:

Well after all the talk on this thread I decided to ask for a written confirmation of my pension forecast using form BR19.

The screen shots in my prior message above showed that I had already qualified for full pension and no COPE amount was shown on the gov site.

The forecast has now come through and it is different to what was shown on the web site in two areas.

1) It says that I need to make one more years contribution to get the full pension.

2) It shows a COPE amount of £53.13 per week.

The online forecast has now also changed to reflect the information I received by post.

So its pretty safe to say that my original estimate was wrong and only by requesting the written forecast has it been corrected.

Thanks for the update. I have a feeling lots of people are going to be in your position, i.e. no COPE mentioned until they are about to get their pension and then they get a rude shock. The screen shots in my prior message above showed that I had already qualified for full pension and no COPE amount was shown on the gov site.

The forecast has now come through and it is different to what was shown on the web site in two areas.

1) It says that I need to make one more years contribution to get the full pension.

2) It shows a COPE amount of £53.13 per week.

The online forecast has now also changed to reflect the information I received by post.

So its pretty safe to say that my original estimate was wrong and only by requesting the written forecast has it been corrected.

uknick said:

Thanks for the update. I have a feeling lots of people are going to be in your position, i.e. no COPE mentioned until they are about to get their pension and then they get a rude shock.

Why would they get a rude shock?COPE is in addition to any state provision and other than the pre 2016 calculations doesn’t affect your state pension

craig1912 said:

Why would they get a rude shock?

COPE is in addition to any state provision and other than the pre 2016 calculations doesn’t affect your state pension

Yes, but it is included, not in addition to, the pension from the pension plan used for contracting out of SERPS purposes. So, overall, it appears to some people to be a reduction in overall expectation.COPE is in addition to any state provision and other than the pre 2016 calculations doesn’t affect your state pension

R.

craig1912 said:

uknick said:

Thanks for the update. I have a feeling lots of people are going to be in your position, i.e. no COPE mentioned until they are about to get their pension and then they get a rude shock.

Why would they get a rude shock?COPE is in addition to any state provision and other than the pre 2016 calculations doesn’t affect your state pension

I then asked for written quote and it came back showing a COPE amount and an addition years contribution required for full pension.

The implication (and it may be incorrect) is that until I asked for a written quote HMRC were not aware of any contracted out period, hence showing zero COPE amount.

The Leaper said:

Yes, but it is included, not in addition to, the pension from the pension plan used for contracting out of SERPS purposes. So, overall, it appears to some people to be a reduction in overall expectation.

R.

Yes but it doesn’t affect the state scheme and generally is a tiny part of the occupational scheme so makes a difference but, a relatively small difference and certainly not a “rude shock” difference.R.

Interestingly I have a COPE but no occupational scheme as I took a CETV and for some reason (I suspect an error or it’s just what happens when a CETV is taken) my COPE or GMP equivalent has gone.

Edited by craig1912 on Wednesday 5th February 17:59

craig1912 said:

Yes but it doesn’t affect the state scheme and generally is a tiny part of the occupational scheme so makes a difference but, a relatively small difference and certainly not a “rude shock” difference.

Interestingly I have a COPE but no occupational scheme as I took a CETV and for some reason (I suspect an error or it’s just what happens when a CETV is taken) my COPE or GMP equivalent has gone.

Noted. Looks to me that the transferring scheme retained the contracted out GMP and transferred a CETV of the balance of your accrued pension, hence that's why you have a COPE.Interestingly I have a COPE but no occupational scheme as I took a CETV and for some reason (I suspect an error or it’s just what happens when a CETV is taken) my COPE or GMP equivalent has gone.

Edited by craig1912 on Wednesday 5th February 17:59

R.

i4got said:

LeadFarmer said:

Theres nothing more that I can say. It's like puling teeth.

To anyone who is in two minds, ring them. Dont just ask them if the forecaster is correct, ask them about retiring early and not paying any further NI

To anyone who is in two minds, ring them. Dont just ask them if the forecaster is correct, ask them about retiring early and not paying any further NI

i4got said:

I 'retired' at 54 - living on savings etc until pensions etc kick in. I have more than 35 years contributions and haven't contributed in the 3 years since I 'retired'. On line is showing full £168 with no extra contributions required.

I rang HMRC and they said I didn't need to continue to pay,

My quote is from page 1 of this thread.I rang HMRC and they said I didn't need to continue to pay,

Here - https://www.gov.uk/self-employed-national-insuranc... it says

How much you pay

Class Rate for tax year 2019 to 2020

Class 2 £3 a week

Class 4 9% on profits between £8,632 and £50,000

2% on profits over £50,000

And:

Special rules for specific jobs

Some self-employed people do not pay National Insurance through Self Assessment, but may want to pay voluntary contributions. These are:

examiners, moderators, invigilators and people who set exam questions

people who run businesses involving land or property

ministers of religion who do not receive a salary or stipend

people who make investments for themselves or others - but not as a business and without getting a fee or commission

So I could pay £156 a year class 2 contributions instead of topping up missed years class 3 at nearly £800 a year?

I couldn't get the figures for my pension via the gateway - could log in, but not get to pension figures

Asked via 'phone and the figures arrived today.

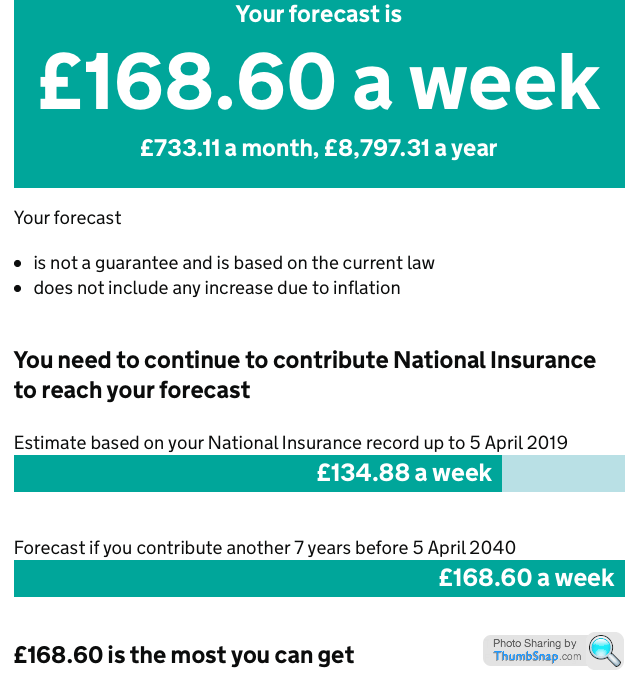

"you can get your pension on dd/mm/2025, your forecast is 168.60 a week. You forecast is not guaranteed etc.

Estimate based on your national insurance record up to 5 april 2019 158,72 a week, forecast if you contribute another 3 years before 5 april 2024 3168.60"

"when you reach 168.60 you may still need to pay N I contributions until dd/mm/2025 if you're working. They fund other state benefits and the NHS"

A bit of surprise, because I thought I'd have to work a few more years (I'll be 66 on the date)

A few years back I was told I'd get the full amount as I'd paid in for 35 full years - but this seems to contradict that (I guess the reason for the OP)

Ii work for a limited company (I am Director), and don't earn enough to pay NI - does anyone know the best/easiest/cheapest? way to contribute my other 3 years?

I'm a bit miffed that there hasn't been a national announcement that (presumably nearly all of us) have been subject to these new 'rules' - or maybe I've missed it?

Asked via 'phone and the figures arrived today.

"you can get your pension on dd/mm/2025, your forecast is 168.60 a week. You forecast is not guaranteed etc.

Estimate based on your national insurance record up to 5 april 2019 158,72 a week, forecast if you contribute another 3 years before 5 april 2024 3168.60"

"when you reach 168.60 you may still need to pay N I contributions until dd/mm/2025 if you're working. They fund other state benefits and the NHS"

A bit of surprise, because I thought I'd have to work a few more years (I'll be 66 on the date)

A few years back I was told I'd get the full amount as I'd paid in for 35 full years - but this seems to contradict that (I guess the reason for the OP)

Ii work for a limited company (I am Director), and don't earn enough to pay NI - does anyone know the best/easiest/cheapest? way to contribute my other 3 years?

I'm a bit miffed that there hasn't been a national announcement that (presumably nearly all of us) have been subject to these new 'rules' - or maybe I've missed it?

Fastpedeller said:

A few years back I was told I'd get the full amount as I'd paid in for 35 full years - but this seems to contradict that (I guess the reason for the OP)

Firstly, apologies for the selective quote, but pleased to seesomeone has had more or less the same experience I had. Which knocks the claims from certain quarters that if you are told however that you have 35 years then full amount SP follows.Fastpedeller said:

I couldn't get the figures for my pension via the gateway - could log in, but not get to pension figures

Asked via 'phone and the figures arrived today.

"you can get your pension on dd/mm/2025, your forecast is 168.60 a week. You forecast is not guaranteed etc.

Estimate based on your national insurance record up to 5 april 2019 158,72 a week, forecast if you contribute another 3 years before 5 april 2024 3168.60"

"when you reach 168.60 you may still need to pay N I contributions until dd/mm/2025 if you're working. They fund other state benefits and the NHS"

A bit of surprise, because I thought I'd have to work a few more years (I'll be 66 on the date)

A few years back I was told I'd get the full amount as I'd paid in for 35 full years - but this seems to contradict that (I guess the reason for the OP)

Ii work for a limited company (I am Director), and don't earn enough to pay NI - does anyone know the best/easiest/cheapest? way to contribute my other 3 years?

I'm a bit miffed that there hasn't been a national announcement that (presumably nearly all of us) have been subject to these new 'rules' - or maybe I've missed it?

I can't tell you all the options but if you pay voluntary class 3 its £780 per year.Asked via 'phone and the figures arrived today.

"you can get your pension on dd/mm/2025, your forecast is 168.60 a week. You forecast is not guaranteed etc.

Estimate based on your national insurance record up to 5 april 2019 158,72 a week, forecast if you contribute another 3 years before 5 april 2024 3168.60"

"when you reach 168.60 you may still need to pay N I contributions until dd/mm/2025 if you're working. They fund other state benefits and the NHS"

A bit of surprise, because I thought I'd have to work a few more years (I'll be 66 on the date)

A few years back I was told I'd get the full amount as I'd paid in for 35 full years - but this seems to contradict that (I guess the reason for the OP)

Ii work for a limited company (I am Director), and don't earn enough to pay NI - does anyone know the best/easiest/cheapest? way to contribute my other 3 years?

I'm a bit miffed that there hasn't been a national announcement that (presumably nearly all of us) have been subject to these new 'rules' - or maybe I've missed it?

If you have multiple incomplete years on your NI record then its possible you will be able to make them complete for significantly less than the £780.

Obviously best to start with the cheapest first.

Fastpedeller said:

I couldn't get the figures for my pension via the gateway - could log in, but not get to pension figures

Asked via 'phone and the figures arrived today.

"you can get your pension on dd/mm/2025, your forecast is 168.60 a week. You forecast is not guaranteed etc.

Estimate based on your national insurance record up to 5 april 2019 158,72 a week, forecast if you contribute another 3 years before 5 april 2024 3168.60"

"when you reach 168.60 you may still need to pay N I contributions until dd/mm/2025 if you're working. They fund other state benefits and the NHS"

A bit of surprise, because I thought I'd have to work a few more years (I'll be 66 on the date)

A few years back I was told I'd get the full amount as I'd paid in for 35 full years - but this seems to contradict that (I guess the reason for the OP)

Ii work for a limited company (I am Director), and don't earn enough to pay NI - does anyone know the best/easiest/cheapest? way to contribute my other 3 years?

I'm a bit miffed that there hasn't been a national announcement that (presumably nearly all of us) have been subject to these new 'rules' - or maybe I've missed it?

How much does the company pay you? For 2019/20, you only need to earn £6,136 to make the year a qualifying one for state pension but at that level you don't pay any NI. Effectively qualifying for free.Asked via 'phone and the figures arrived today.

"you can get your pension on dd/mm/2025, your forecast is 168.60 a week. You forecast is not guaranteed etc.

Estimate based on your national insurance record up to 5 april 2019 158,72 a week, forecast if you contribute another 3 years before 5 april 2024 3168.60"

"when you reach 168.60 you may still need to pay N I contributions until dd/mm/2025 if you're working. They fund other state benefits and the NHS"

A bit of surprise, because I thought I'd have to work a few more years (I'll be 66 on the date)

A few years back I was told I'd get the full amount as I'd paid in for 35 full years - but this seems to contradict that (I guess the reason for the OP)

Ii work for a limited company (I am Director), and don't earn enough to pay NI - does anyone know the best/easiest/cheapest? way to contribute my other 3 years?

I'm a bit miffed that there hasn't been a national announcement that (presumably nearly all of us) have been subject to these new 'rules' - or maybe I've missed it?

bladerrw said:

Fastpedeller said:

I couldn't get the figures for my pension via the gateway - could log in, but not get to pension figures

Asked via 'phone and the figures arrived today.

"you can get your pension on dd/mm/2025, your forecast is 168.60 a week. You forecast is not guaranteed etc.

Estimate based on your national insurance record up to 5 april 2019 158,72 a week, forecast if you contribute another 3 years before 5 april 2024 3168.60"

"when you reach 168.60 you may still need to pay N I contributions until dd/mm/2025 if you're working. They fund other state benefits and the NHS"

A bit of surprise, because I thought I'd have to work a few more years (I'll be 66 on the date)

A few years back I was told I'd get the full amount as I'd paid in for 35 full years - but this seems to contradict that (I guess the reason for the OP)

Ii work for a limited company (I am Director), and don't earn enough to pay NI - does anyone know the best/easiest/cheapest? way to contribute my other 3 years?

I'm a bit miffed that there hasn't been a national announcement that (presumably nearly all of us) have been subject to these new 'rules' - or maybe I've missed it?

How much does the company pay you? For 2019/20, you only need to earn £6,136 to make the year a qualifying one for state pension but at that level you don't pay any NI. Effectively qualifying for free.Asked via 'phone and the figures arrived today.

"you can get your pension on dd/mm/2025, your forecast is 168.60 a week. You forecast is not guaranteed etc.

Estimate based on your national insurance record up to 5 april 2019 158,72 a week, forecast if you contribute another 3 years before 5 april 2024 3168.60"

"when you reach 168.60 you may still need to pay N I contributions until dd/mm/2025 if you're working. They fund other state benefits and the NHS"

A bit of surprise, because I thought I'd have to work a few more years (I'll be 66 on the date)

A few years back I was told I'd get the full amount as I'd paid in for 35 full years - but this seems to contradict that (I guess the reason for the OP)

Ii work for a limited company (I am Director), and don't earn enough to pay NI - does anyone know the best/easiest/cheapest? way to contribute my other 3 years?

I'm a bit miffed that there hasn't been a national announcement that (presumably nearly all of us) have been subject to these new 'rules' - or maybe I've missed it?

I had a meeting with my IFA yesterday. He's a bit of a pensions guru and really seems to know about all the changes to legislation on personal and state pensions. I put to him the scenario about retiring early, having made 35+ years NI contributions, being told you're entitled to the full £168.60 at age 67 on Govt Gateway, but not actually getting it unless you continue to make NI payments between retiring and turning 67.

He knew nothing about it and, although he admitted that it was possible this had passed him by, he was pretty confident it was nonsense.

He knew nothing about it and, although he admitted that it was possible this had passed him by, he was pretty confident it was nonsense.

TwigtheWonderkid said:

I had a meeting with my IFA yesterday. He's a bit of a pensions guru and really seems to know about all the changes to legislation on personal and state pensions. I put to him the scenario about retiring early, having made 35+ years NI contributions, being told you're entitled to the full £168.60 at age 67 on Govt Gateway, but not actually getting it unless you continue to make NI payments between retiring and turning 67.

He knew nothing about it and, although he admitted that it was possible this had passed him by, he was pretty confident it was nonsense.

Thats not quite my scenario.He knew nothing about it and, although he admitted that it was possible this had passed him by, he was pretty confident it was nonsense.

In my experience if Govt Gateway tells you that you have ALREADY (ie as of todays date) earned a full £168.60 pension when you reach retirement AND the forecast is correct, then you do not need to make any more contributions.

My problem is that it was not correct. It showed no COPE amount even though I was contracted out for a while. This did not come to light until I sent in the form asking for a written projection.

The written projection correctly showed a COPE amount and as a result changed my forecast so that I needed one more years contribution to get the £168.60. The online forecast has now changed and matches what was sent by post.

The government are aware that up to 3% of online projections are incorrect but (at least in my case) asking for a written forecast seems to correct the issue.

https://www.moneysavingexpert.com/news/2019/06/war...

i4got said:

TwigtheWonderkid said:

I had a meeting with my IFA yesterday. He's a bit of a pensions guru and really seems to know about all the changes to legislation on personal and state pensions. I put to him the scenario about retiring early, having made 35+ years NI contributions, being told you're entitled to the full £168.60 at age 67 on Govt Gateway, but not actually getting it unless you continue to make NI payments between retiring and turning 67.

He knew nothing about it and, although he admitted that it was possible this had passed him by, he was pretty confident it was nonsense.

Thats not quite my scenario.He knew nothing about it and, although he admitted that it was possible this had passed him by, he was pretty confident it was nonsense.

In my experience if Govt Gateway tells you that you have ALREADY (ie as of todays date) earned a full £168.60 pension when you reach retirement AND the forecast is correct, then you do not need to make any more contributions.

My problem is that it was not correct. It showed no COPE amount even though I was contracted out for a while. This did not come to light until I sent in the form asking for a written projection.

The written projection correctly showed a COPE amount and as a result changed my forecast so that I needed one more years contribution to get the £168.60. The online forecast has now changed and matches what was sent by post.

The government are aware that up to 3% of online projections are incorrect but (at least in my case) asking for a written forecast seems to correct the issue.

https://www.moneysavingexpert.com/news/2019/06/war...

Gassing Station | Finance | Top of Page | What's New | My Stuff