House Price Crash Coming?

Discussion

moles said:

But will wfh be here longterm?, I don’t think it will several companies have come out and said they want people back at the office and what people don’t seem to be grasping with wfh is that if you can work from 200 miles away someone in Bangladesh can do your job as well for a third of your wage.

Totally agree - there's going to be a boom in hiring overseas workers. RaymondVanDerDon said:

moles said:

But will wfh be here longterm?, I don’t think it will several companies have come out and said they want people back at the office and what people don’t seem to be grasping with wfh is that if you can work from 200 miles away someone in Bangladesh can do your job as well for a third of your wage.

Totally agree - there's going to be a boom in hiring overseas workers. It's taught us there's no need for expensive offices in cities for 1000s of people to sit, we just need some collaboration space to use occasionally.

TheRainMaker said:

By all accounts, it’s a mini boom around here in Surrey.

Depends who you ask:https://www.zoopla.co.uk/house-prices/surrey/

RaymondVanDerDon said:

Totally agree - there's going to be a boom in hiring overseas workers.

Disagree, because companies who are seriously interested in doing this already do it. Our HR is based in Eastern Europe somewhere, software development is in a number of low cost off shore locations, etc. Outsourcing the “boring” non-core stuff like HR, accounts, billing, etc. to service companies is already possible. Companies who aren’t doing this either don’t see there’s an advantage of saving vs. service levels, want control over the people doing the work, or have other reasons not to do it.

wormus said:

You need to change the search field to "Last 3 months'. A detached property now up 4.17% whilst 'Last 6 months' only up 0.21% craigjm said:

Sounds like someone else is suggesting the move and you’re looking for some “evidence” that you shouldn’t because you don’t want to

Actually quite the opposite. Girlfriend is very happy with the house, I would like somewhere bigger so suggested we start looking. I was a bit shocked that houses that were ~£225k five years ago have gone up 55% in that timescale.Edited by craigjm on Tuesday 11th August 17:03

We'll see what happens. If I've called it wrong then we can stay put.

Julia121 said:

wormus said:

You need to change the search field to "Last 3 months'. A detached property now up 4.17% whilst 'Last 6 months' only up 0.21% Edited by anonymous-user on Tuesday 11th August 19:18

bogie said:

Adjusted for inflation house prices are just about back to where they were 10 years ago anyway

nationwide data below, blue line clearly shows the boom years

Once you overlay wage growth into a graph like this, you can see the problem.nationwide data below, blue line clearly shows the boom years

Sentiment works both ways in a market, but UK citizens aren't really familiar with a housing market downturn. The last one was just a blip, driven by poor banking practices.

If a sentiment of negativity takes hold in the UK, it could be catastrophic, and over the next 6 months, there are a few stars aligning together to drive that sentiment to a place we've never experienced before.

A big rush to complete sales before the stamp duty holiday ends early next year....followed by a natural slow down post rush....add the worst recession in our life time, add potential Brexit impact, add RPI inflation, and add record unemployment.....the sentiment has only ever been one direction in the UK but if that sentiment turns, things could get messy.

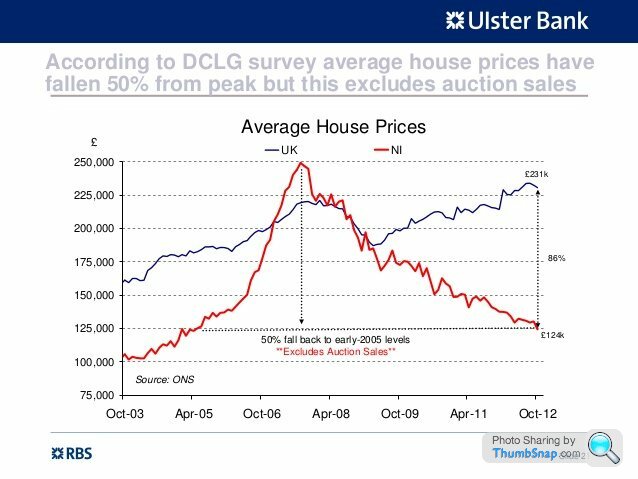

Over here in NI, house prices absolutely soared and then crashed. Current prices in 2020 are pretty realistic. The cost of bricks and mortor, the cost to build and about 20% on top. Ie, if it can be built for £150k, you'll pay about £180k as a rule of thumb.

So the capital value (eg, what an estate agent would value it at) and intrinsic value (perception of what its really worth) are fairly well matched in 2020. You are paying just a little bit more than the materials and the labour costs to build said asset. People can live with the prices right now.

But lets look at when the arse fell out of the NI property market. Graph below.

Car crash. It wasn't that people couldn't get mortgages or couldn't afford to buy - sentiment changed and a ton of people just handed their house back to the bank and said f

k this, I'll rent and start again now that prices are sensible. It was sentiment on the way up but when that sentiment reversed, it was a car crash.

k this, I'll rent and start again now that prices are sensible. It was sentiment on the way up but when that sentiment reversed, it was a car crash.In parts of the UK, capital values are far far too high, and if that sentiment of real worth changes, the intrinsic value changes, and as a result, the capital value moves on the exact same trajectory.

I bought in 2004, moved in 2008 (right in the middle of the crash) and could see as clear as day that the only thing that really controls house prices in a situation like that is sentiment, and sentiment only.

Forget about banks, forget about Estate agents, forget about experts.....they just scratched their heads like the rest of us. Its all about sentiment when you strip it back to its very core, and as I mentioned, most in the UK haven't lived through a switch in sentiment like that before. Its crazy when it happens - been there, got the T shirt

All of that is true and offshoring is a load of st all around. But when a bean counter is called in to cut costs they will try it yes it will fail but they will still try it.

Also will they start adjusting wages based on where you live?, I think companies will try it all on over the next few years in the quest to cut costs.

t all around. But when a bean counter is called in to cut costs they will try it yes it will fail but they will still try it. Also will they start adjusting wages based on where you live?, I think companies will try it all on over the next few years in the quest to cut costs.

anonymous said:

[redacted]

bogie said:

nationwide data below, blue line clearly shows the boom years

Whoever drew that red trend line should be taken out and shot. Look at the past 14 years on the blue line - there's a clear downward trend. But whoever imagined that red line onto the page shows an upward trend....

rockin said:

bogie said:

nationwide data below, blue line clearly shows the boom years

Whoever drew that red trend line should be taken out and shot. Look at the past 14 years on the blue line - there's a clear downward trend. But whoever imagined that red line onto the page shows an upward trend....

retail price inflation in red

versus

inflation adjusted house prices in blue

so retail inflation goes up a few percent each year as normal, and house prices (adjusted) vary ...if you sell in a boom where house price growth outstrips inflation, then you can make a lot of money ....for the remainder of the time its a lot of smoke n mirrors, you may think you have made some short term gains but taking into account inflation have made bugger all in real terms.

....unless you buy in a market dip (blue line below red) and sell in a market peak (blue line above red) Its easy to see in hindsight, but more difficult to know where the market is in real time. Residential property is not so liquid, you dont generally buy and sell property on a whim a like you do shares, so much of when you sell and buy can be down to luck....of course its all relative so long as you stay in the same area under the same rules. The only time you feel more "well off" is when you leave the expensive are and go somewhere cheaper/more average, and cash in from the boom area you lived in.....

but dont forget, no-one ever lost money on property, it always goes up ....mmmm...perhaps not if you are the person sat in negative equity after buying in a boom and paying mortgage interest whilst you wait for the market to come back up......

I have seen prices go up as much as 20-25% in the last few weeks in the area I am looking at (small village by the sea in the SW).

A flat came on the market recently that was £199k and sold in 24 hrs. In the same complex exact same flats were selling for £150-160k in winter.

The jump in prices does not match the saving in SDLT. People are rushing to buy, they are saving £10k (for example) in stamp but paying £50k more for the house. Something has to give.

Personally I think come October we are going to see chains failing all over the shop when people start to get made redundant. I also expect a lot of cash buyers are dragging out their purchases and will wait till the vendors are desperate and then lower their price at the last moment.

Its going to get nasty out there in the latter end of the year.

A flat came on the market recently that was £199k and sold in 24 hrs. In the same complex exact same flats were selling for £150-160k in winter.

The jump in prices does not match the saving in SDLT. People are rushing to buy, they are saving £10k (for example) in stamp but paying £50k more for the house. Something has to give.

Personally I think come October we are going to see chains failing all over the shop when people start to get made redundant. I also expect a lot of cash buyers are dragging out their purchases and will wait till the vendors are desperate and then lower their price at the last moment.

Its going to get nasty out there in the latter end of the year.

Welshbeef said:

You only lose money on property if you have to sell at a point in time where the price isn’t ideal.

Else you hold on wait - time is on your hands and history shows us they recover so you can say move from a negative equity position to be able to take some equity out.

And generally only if you are selling a property which was an investment and not your main home. The vast majority of people move from their one and only property to a new one and only property and can recover some of a dip in that the “cost to change” remains fairly constant Else you hold on wait - time is on your hands and history shows us they recover so you can say move from a negative equity position to be able to take some equity out.

Gassing Station | Finance | Top of Page | What's New | My Stuff