Your questions answered Vol 2 - IM Private Clients

Discussion

Mr Whippy said:

Exactly if you’ve been averaging in for say 5 years then you’ll be doing ok.

If you bought in a big chunk during 2021, then oops.

Though I’m sure right up until a few months ago people were saying lump sums should be invested right away and it’s always better than averaging in.

That's because on average it has been. At the moment? Who knows.If you bought in a big chunk during 2021, then oops.

Though I’m sure right up until a few months ago people were saying lump sums should be invested right away and it’s always better than averaging in.

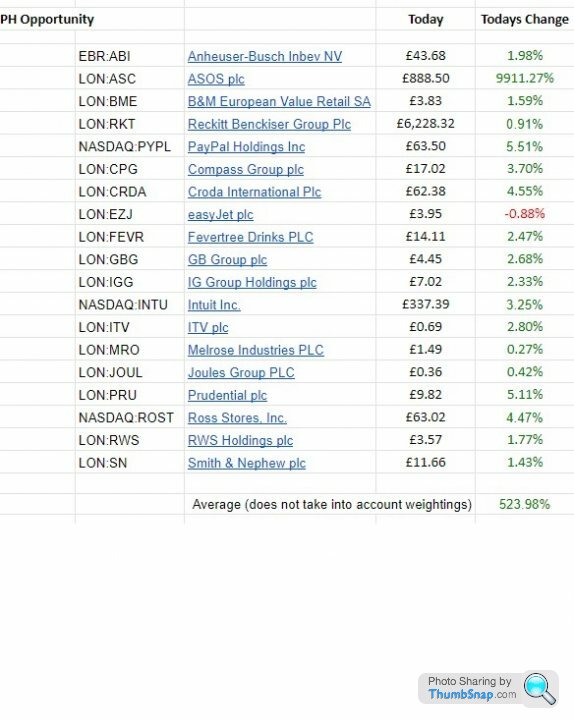

Well, some good news, ASOS has finally performed............................

Bad news, it's just a google finance error, apparently each share is now worth £888.50 each

PS. Could we have the decimal point moved two places to the right on our portfolio's as well please?

Bad news, it's just a google finance error, apparently each share is now worth £888.50 each

PS. Could we have the decimal point moved two places to the right on our portfolio's as well please?

Edited by Ron-ski on Friday 24th June 18:29

Edited by Ron-ski on Friday 24th June 18:29

Hi all,

A lot has been going on behind the scenes recently. We are very close to launching IM Lifestyle-just putting some finishing touches on the documentation which is all compliance based. The model and asset allocation is complete as of today! Next week is looking good for a launch.

The markets have had a solid week largely due to unexpected high demand for housing(and other economic data not as bad as first thought) and perceptions that inflation is starting to ease. I know, it's speculation really but that's forecasting for you and I think we will all agree that a gain is welcome.

Polestar (PHT) is now trading under its owns Ticker. Our position is sitting about flat(break even) after a pop of about 15% at the open and a slow retrace.

Earnings season is approaching again. Next week we have Nike reporting Tuesday then a week or so for United Health and Domino Pizza July 15th, Microsoft 21st ....

Have a good weekend, all

A lot has been going on behind the scenes recently. We are very close to launching IM Lifestyle-just putting some finishing touches on the documentation which is all compliance based. The model and asset allocation is complete as of today! Next week is looking good for a launch.

The markets have had a solid week largely due to unexpected high demand for housing(and other economic data not as bad as first thought) and perceptions that inflation is starting to ease. I know, it's speculation really but that's forecasting for you and I think we will all agree that a gain is welcome.

Polestar (PHT) is now trading under its owns Ticker. Our position is sitting about flat(break even) after a pop of about 15% at the open and a slow retrace.

Earnings season is approaching again. Next week we have Nike reporting Tuesday then a week or so for United Health and Domino Pizza July 15th, Microsoft 21st ....

Have a good weekend, all

Ron-ski said:

Well, some good news, ASOS has finally performed............................

Bad news, it's just a google finance error, apparently each share is now worth £888.50 each

PS. Could we have the decimal point moved two places to the right on our portfolio's as well please?

It's been corrected now Ron-ski Bad news, it's just a google finance error, apparently each share is now worth £888.50 each

PS. Could we have the decimal point moved two places to the right on our portfolio's as well please?

Currently showing as £88,850

Piece of cake this investing, just need hold on the down and cash in on the up

AdamIM said:

A lot has been going on behind the scenes recently. We are very close to launching IM Lifestyle-just putting some finishing touches on the documentation which is all compliance based. The model and asset allocation is complete as of today! Next week is looking good for a launch.

Hi Adam. As I understand it, 'IML' invests in a variable mix of other IM products according to individual requirements. In other words, I imagine someone much smarter than me will shuffle stuff about as they deem necessary. Do their options include cash, as a (relative) haven if other vehicles something looks likely to tank? Stable door/horse at present of course, but I feel it's an option that should be in the toybox for eventualities.People trot out 'time in the market', but if the market is going down it's not a great time to be in it! Lift going down? Step onto a floor.

Mr Pointy said:

Mr Whippy said:

Exactly if you’ve been averaging in for say 5 years then you’ll be doing ok.

If you bought in a big chunk during 2021, then oops.

Though I’m sure right up until a few months ago people were saying lump sums should be invested right away and it’s always better than averaging in.

That's because on average it has been. At the moment? Who knows.If you bought in a big chunk during 2021, then oops.

Though I’m sure right up until a few months ago people were saying lump sums should be invested right away and it’s always better than averaging in.

On average you’ll buy in a bull market.

Then roughly half the bear market you could buy at the top.

Averages are little consolation in this situation… a little bit of consideration of the wider economic situation could be of value in deciding whether to lump sum or average in.

Simpo Two said:

AdamIM said:

A lot has been going on behind the scenes recently. We are very close to launching IM Lifestyle-just putting some finishing touches on the documentation which is all compliance based. The model and asset allocation is complete as of today! Next week is looking good for a launch.

Hi Adam. As I understand it, 'IML' invests in a variable mix of other IM products according to individual requirements. In other words, I imagine someone much smarter than me will shuffle stuff about as they deem necessary. Do their options include cash, as a (relative) haven if other vehicles something looks likely to tank? Stable door/horse at present of course, but I feel it's an option that should be in the toybox for eventualities.People trot out 'time in the market', but if the market is going down it's not a great time to be in it! Lift going down? Step onto a floor.

As much as I’m holding a high proportion of cash in my IM savings, I feel that when I do invest into a fund it shouldn’t probably be using too much cash, as by definition I invest in a fund to be invested…

This recession looming while interest rates rise off the bottom is a bit of an anomaly as normally you’d have rates being cut and bond prices rising.

You could be safe(r) in bonds.

It’s an interesting one though. Should IML use cash? Or should that always be down to individuals to choose?

Mr Whippy said:

It’s an interesting one though. Should IML use cash? Or should that always be down to individuals to choose?

Moving into or out of cash is the same as moving into or out of any other vehicle. Therefore I see no reason why this shouldn't be within the remit of the fund manager. He/she is better placed to make that judgment than the investor - otherwise what are they doing? To have their hands tied by not being able to exploit cash (the short term performance of which is more predictable than equities) seems odd to me. Why exclude an option if, at a particular time, it happens to be the best option? It can be done - for as we know, PHR sold to cash when it was deemed most appropriate. It didn't buy back in, but that's a logical next step for a fully functioning actively managed portfolio IMHO. Sometimes cash is best, so use it as part of the arsenal to reduce losses when markets are falling.Simpo Two said:

Mr Whippy said:

It’s an interesting one though. Should IML use cash? Or should that always be down to individuals to choose?

Moving into or out of cash is the same as moving into or out of any other vehicle. Therefore I see no reason why this shouldn't be within the remit of the fund manager. He/she is better placed to make that judgment than the investor - otherwise what are they doing? To have their hands tied by not being able to exploit cash (the short term performance of which is more predictable than equities) seems odd to me. Why exclude an option if, at a particular time, it happens to be the best option? It can be done - for as we know, PHR sold to cash when it was deemed most appropriate. It didn't buy back in, but that's a logical next step for a fully functioning actively managed portfolio IMHO. Sometimes cash is best, so use it as part of the arsenal to reduce losses when markets are falling.Holding cash is prudent however that decision and percentage lies with the individual, not the Asset Manager. IML will hold near-cash assets in certain Target Dated Portfolio's (TDPs) in the form of Money market (commercial Paper) which have a very short duration (60-90 days) and as such are not impacted by yield changes to the degree multi year bonds are. It should be pointed out that this is the mandate (to achieve an objective)of that particular portfolio and its Strategic Asset Allocation (SAA) prescribes a percentage holding in these sorts of securities, as opposed to the Fund Manager transitioning to cash as part of a tactical overlay.

I hope that helps.

Julian and Nik will an update on IML next week.

Edited by AdamIM on Saturday 25th June 13:45

AdamIM said:

Simpo Two said:

Mr Whippy said:

It’s an interesting one though. Should IML use cash? Or should that always be down to individuals to choose?

Moving into or out of cash is the same as moving into or out of any other vehicle. Therefore I see no reason why this shouldn't be within the remit of the fund manager. He/she is better placed to make that judgment than the investor - otherwise what are they doing? To have their hands tied by not being able to exploit cash (the short term performance of which is more predictable than equities) seems odd to me. Why exclude an option if, at a particular time, it happens to be the best option? It can be done - for as we know, PHR sold to cash when it was deemed most appropriate. It didn't buy back in, but that's a logical next step for a fully functioning actively managed portfolio IMHO. Sometimes cash is best, so use it as part of the arsenal to reduce losses when markets are falling.Holding cash is prudent however that decision and percentage lies with the individual, not the Asset Manager. IML will hold near-cash assets in certain Target Dated Portfolio's (TDPs) in the form of Money market (commercial Paper) which have a very short duration (60-90 days) and as such are not impacted by yield changes to the degree multi year bonds are. It should be pointed out that this is the mandate (to achieve an objective)of that particular portfolio and its Strategic Asset Allocation (SAA) prescribes a percentage holding in these sorts of securities, as opposed to the Fund Manager transitioning to cash as part of a tactical overlay.

I hope that helps.

Julian and Nik will an update on IML next week.

Edited by AdamIM on Saturday 25th June 13:45

pingu393 said:

AdamIM said:

Simpo Two said:

Mr Whippy said:

It’s an interesting one though. Should IML use cash? Or should that always be down to individuals to choose?

Moving into or out of cash is the same as moving into or out of any other vehicle. Therefore I see no reason why this shouldn't be within the remit of the fund manager. He/she is better placed to make that judgment than the investor - otherwise what are they doing? To have their hands tied by not being able to exploit cash (the short term performance of which is more predictable than equities) seems odd to me. Why exclude an option if, at a particular time, it happens to be the best option? It can be done - for as we know, PHR sold to cash when it was deemed most appropriate. It didn't buy back in, but that's a logical next step for a fully functioning actively managed portfolio IMHO. Sometimes cash is best, so use it as part of the arsenal to reduce losses when markets are falling.Holding cash is prudent however that decision and percentage lies with the individual, not the Asset Manager. IML will hold near-cash assets in certain Target Dated Portfolio's (TDPs) in the form of Money market (commercial Paper) which have a very short duration (60-90 days) and as such are not impacted by yield changes to the degree multi year bonds are. It should be pointed out that this is the mandate (to achieve an objective)of that particular portfolio and its Strategic Asset Allocation (SAA) prescribes a percentage holding in these sorts of securities, as opposed to the Fund Manager transitioning to cash as part of a tactical overlay.

I hope that helps.

Julian and Nik will an update on IML next week.

Edited by AdamIM on Saturday 25th June 13:45

Hindsight is a wonderful thing. I think if individuals want to hold cash there is a mechanism to do so.

The portfolio's have objectives and a mandate. On the question of legalities. The FCA require all asset managers to operate in line with investors’ expectations as set by marketing and disclosure material, and investment mandates(see IM website fact sheets etc!). This is TR16-Thematic review (regulations we are bound by). This compliance is there to protect you.

pingu393 said:

Is it a legality thing that says that asset managers are not allowed to "invest" in cash? If so, I understand. If not, I find it strange that a manager wouldn't use the most obvious life raft when everything else is sinking.

Imagine the turmoil if all asset managers decided to invest their clients in cash in times when markets are moving downwards. Think that would / could be catastrophic, individual choice is there if there is a feeling the correct thing is to pull out of the market.

The way I see it is money is invested in funds and the investor accepts this way of managing or not.

Edited by tighnamara on Saturday 25th June 22:39

tighnamara said:

pingu393 said:

Is it a legality thing that says that asset managers are not allowed to "invest" in cash? If so, I understand. If not, I find it strange that a manager wouldn't use the most obvious life raft when everything else is sinking.

Imagine the turmoil if all asset managers decided to invest their clients in cash in times when markets are moving downwards. Think that would / could be catastrophic, individual choice is there if there is a feeling the correct thing is to pull out of the market.

The way I see it is money is invested in funds and the investor accepts this way of managing or not.

Edited by tighnamara on Saturday 25th June 22:39

A few hundred thousand quid going to cash, compared to many tens of billions going to cash.

First, I'd like to point out that this is not a dig at Adam, because he is doing a great job analysing stuff, but just genuine questions raised by his points. For some people investments are not a game and losses cannot be replaced by salary. Furthermore the majority of my stuff is outside IM, so it's really a general grumble because three years of growth has gone 'phut' and Adam just happens to be in the way

Why should the percentage of cash held be left to the (amateur) investor and not to the (professional) Asset Manager? Cash is an asset.

What percentage of TDPs do the portfolios have and how have they performed over the last few months?

Thanks to Julian, Intelligent Money is an innovator. We invest with IM because it is different/better/more flexible/responsive than other providers. Improvise, invent and create, don't just do what everybody else does. Sometimes vision and a desire to do something new/better/different from the pack means it can outperform the pack.

Most investors lack the time or knowledge to run their investments beyond an overview, so they rely on people more knowledgeable than themselves to make decisions. And sometimes when the road is very bumpy those people need to be more fleet-footed than usual. I like IM and its people, and it's doing no worse than anyone else. I just think that with its small size and according nimble-footedness, it has the potential to beat the pack once again. Don't defend the past because that is gone, adapt for the future

AdamIM said:

PHR was a one off opportunistic portfolio with predetermined goals (target prices and anticipated short/medium time period) and when those targets were reached the securities were cashed-in. All other IM products revolve around core investment principles, one being buy and hold.

Yes. But it showed the principle can work, one just needs to add a 're-buy' point as well and you have a self-sustaining fund with an extra asset which if used wisely will allow it to perform betterAdamIM said:

Holding cash is prudent however that decision and percentage lies with the individual, not the Asset Manager. IML will hold near-cash assets in certain Target Dated Portfolio's (TDPs) in the form of Money market (commercial Paper) which have a very short duration (60-90 days) and as such are not impacted by yield changes to the degree multi year bonds are. It should be pointed out that this is the mandate (to achieve an objective)of that particular portfolio and its Strategic Asset Allocation (SAA) prescribes a percentage holding in these sorts of securities, as opposed to the Fund Manager transitioning to cash as part of a tactical overlay.

This begs two questions:Why should the percentage of cash held be left to the (amateur) investor and not to the (professional) Asset Manager? Cash is an asset.

What percentage of TDPs do the portfolios have and how have they performed over the last few months?

AdamIM said:

Holding cash as a strategy will materially constrain the long term returns of a portfolio.

Traditionally yes, but here, ignoring cash has wiped out three years of growth.AdamIM said:

Second it would be counter intuitive to the objectives of the portfolio.

Things change, therefore objectives can change to reflect them. The world is very different from what it was a few months ago, and is not going to return for the foreseeable future. AdamIM said:

Third, when exactly would one redeploy this cash....when we knew the volatility was over?

Yes, nobody knows the peak or the trough until its over, but I maintain that if one buys back at a lower price than they sold, or vice versa, then they are better off than simply having sat it out.AdamIM said:

No one know's however history has proven that buying good companies and holding long term, works well. A real world example, if we held cash up until 8 days ago we would have missed out on 7% in PHT.

We can all find a bit of the graph that suits our case AdamIM said:

The portfolio's have objectives and a mandate. On the question of legalities. The FCA require all asset managers to operate in line with investors’ expectations as set by marketing and disclosure material, and investment mandates(see IM website fact sheets etc!). This is TR16-Thematic review (regulations we are bound by). This compliance is there to protect you.

Indeed. A portfolio or fund should not invest in things outside what was agreed at the outset. But you can equally well have a portfolio that says 'The manager may take/preserve gains by moving to cash'. There, that was easy Thanks to Julian, Intelligent Money is an innovator. We invest with IM because it is different/better/more flexible/responsive than other providers. Improvise, invent and create, don't just do what everybody else does. Sometimes vision and a desire to do something new/better/different from the pack means it can outperform the pack.

Most investors lack the time or knowledge to run their investments beyond an overview, so they rely on people more knowledgeable than themselves to make decisions. And sometimes when the road is very bumpy those people need to be more fleet-footed than usual. I like IM and its people, and it's doing no worse than anyone else. I just think that with its small size and according nimble-footedness, it has the potential to beat the pack once again. Don't defend the past because that is gone, adapt for the future

anonymous said:

[redacted]

Yes indeed.Edited by Simpo Two on Sunday 26th June 11:39

I very much agree with Daimler's comment about IM's openness, and because of their openness I know that they don't charge for cash holdings in a portfolio.

This must be a conflict of interest, as nobody in their right mind would suggest that you move out of a position that is paying them 0.8% into a position that is paying zero.

I wouldn't be surprised if fund managers are taught that once cash is in the market, it must stay in the market. If cash is available as part of the market, the volatility of the market would be seriously affected.

As I wrote earlier, I think that an individual moving a few hundred thousand dollars into cash would have no effect, but if tens of billion of dollars suddenly left the market and went to cash, the markets would feel the effect.

This must be a conflict of interest, as nobody in their right mind would suggest that you move out of a position that is paying them 0.8% into a position that is paying zero.

I wouldn't be surprised if fund managers are taught that once cash is in the market, it must stay in the market. If cash is available as part of the market, the volatility of the market would be seriously affected.

As I wrote earlier, I think that an individual moving a few hundred thousand dollars into cash would have no effect, but if tens of billion of dollars suddenly left the market and went to cash, the markets would feel the effect.

There's a lot of crystal ball gazing going on lately in the thread (hindsight involved, with a lot of shouldawouldacoulda) the market could all change on a moments notice, hopefully quickly returning to an upwards direction especially when/if Putin is put to rest, says me who is still sitting things out, saying to myself shouldacouldawoulda, now we just need another 4 or 5 weeks of returns equal to last weeks and we'll all be back to where we were at end of 2021 :-)

dingg said:

There's a lot of crystal ball gazing going on lately in the thread (hindsight involved, with a lot of shouldawouldacoulda) the market could all change on a moments notice, hopefully quickly returning to an upwards direction especially when/if Putin is put to rest, says me who is still sitting things out, saying to myself shouldacouldawoulda, now we just need another 4 or 5 weeks of returns equal to last weeks and we'll all be back to where we were at end of 2021 :-)

If something happens in Ukraine, you will only be a few days behind the market at the most.It's the stuff that a layman may think of as insider trading (I know that it's not) that we will miss out on.

There's lots of things going on in the big, bad world making people nervous. Nervous people don't invest.

Simpo Two said:

First, I'd like to point out that this is not a dig at Adam, because he is doing a great job analysing stuff, but just genuine questions raised by his points. For some people investments are not a game and losses cannot be replaced by salary. Furthermore the majority of my stuff is outside IM, so it's really a general grumble because three years of growth has gone 'phut' and Adam just happens to be in the way

Why should the percentage of cash held be left to the (amateur) investor and not to the (professional) Asset Manager? Cash is an asset.

What percentage of TDPs do the portfolios have and how have they performed over the last few months?

Thanks to Julian, Intelligent Money is an innovator. We invest with IM because it is different/better/more flexible/responsive than other providers. Improvise, invent and create, don't just do what everybody else does. Sometimes vision and a desire to do something new/better/different from the pack means it can outperform the pack.

Most investors lack the time or knowledge to run their investments beyond an overview, so they rely on people more knowledgeable than themselves to make decisions. And sometimes when the road is very bumpy those people need to be more fleet-footed than usual. I like IM and its people, and it's doing no worse than anyone else. I just think that with its small size and according nimble-footedness, it has the potential to beat the pack once again. Don't defend the past because that is gone, adapt for the future

Your views seem to be borne out of hindsight - had investments been cashed out then put back in the market at the dips then the losses could have been cut.AdamIM said:

PHR was a one off opportunistic portfolio with predetermined goals (target prices and anticipated short/medium time period) and when those targets were reached the securities were cashed-in. All other IM products revolve around core investment principles, one being buy and hold.

Yes. But it showed the principle can work, one just needs to add a 're-buy' point as well and you have a self-sustaining fund with an extra asset which if used wisely will allow it to perform betterAdamIM said:

Holding cash is prudent however that decision and percentage lies with the individual, not the Asset Manager. IML will hold near-cash assets in certain Target Dated Portfolio's (TDPs) in the form of Money market (commercial Paper) which have a very short duration (60-90 days) and as such are not impacted by yield changes to the degree multi year bonds are. It should be pointed out that this is the mandate (to achieve an objective)of that particular portfolio and its Strategic Asset Allocation (SAA) prescribes a percentage holding in these sorts of securities, as opposed to the Fund Manager transitioning to cash as part of a tactical overlay.

This begs two questions:Why should the percentage of cash held be left to the (amateur) investor and not to the (professional) Asset Manager? Cash is an asset.

What percentage of TDPs do the portfolios have and how have they performed over the last few months?

AdamIM said:

Holding cash as a strategy will materially constrain the long term returns of a portfolio.

Traditionally yes, but here, ignoring cash has wiped out three years of growth.AdamIM said:

Second it would be counter intuitive to the objectives of the portfolio.

Things change, therefore objectives can change to reflect them. The world is very different from what it was a few months ago, and is not going to return for the foreseeable future. AdamIM said:

Third, when exactly would one redeploy this cash....when we knew the volatility was over?

Yes, nobody knows the peak or the trough until its over, but I maintain that if one buys back at a lower price than they sold, or vice versa, then they are better off than simply having sat it out.AdamIM said:

No one know's however history has proven that buying good companies and holding long term, works well. A real world example, if we held cash up until 8 days ago we would have missed out on 7% in PHT.

We can all find a bit of the graph that suits our case AdamIM said:

The portfolio's have objectives and a mandate. On the question of legalities. The FCA require all asset managers to operate in line with investors’ expectations as set by marketing and disclosure material, and investment mandates(see IM website fact sheets etc!). This is TR16-Thematic review (regulations we are bound by). This compliance is there to protect you.

Indeed. A portfolio or fund should not invest in things outside what was agreed at the outset. But you can equally well have a portfolio that says 'The manager may take/preserve gains by moving to cash'. There, that was easy Thanks to Julian, Intelligent Money is an innovator. We invest with IM because it is different/better/more flexible/responsive than other providers. Improvise, invent and create, don't just do what everybody else does. Sometimes vision and a desire to do something new/better/different from the pack means it can outperform the pack.

Most investors lack the time or knowledge to run their investments beyond an overview, so they rely on people more knowledgeable than themselves to make decisions. And sometimes when the road is very bumpy those people need to be more fleet-footed than usual. I like IM and its people, and it's doing no worse than anyone else. I just think that with its small size and according nimble-footedness, it has the potential to beat the pack once again. Don't defend the past because that is gone, adapt for the future

anonymous said:

[redacted]

Yes indeed.Edited by Simpo Two on Sunday 26th June 11:39

Had the market climbed back and you weren't sitting on paper losses, you would be praising the invesment managers saying "what a gutsy move, if it was me managing my own money I would have gambled/speculated that the prices was going to go down and would have cashed out. I'm glad I left it to the fund managers to make that decision"

The market is fickled, emotional, irrational and unpredictable. The only thing we can expect from investment managers is to do their homework and find the companies which provide the best chance of gains in the long term based on those companies' business sense and financial stability/strategy i.e. which companies have a good business case which is likely to produce stable, if not spectacular, growths.

Those companies will find their prices going up and down like a yo-yo based on the market being fickled, emotional, irrational and unpredictable. But in the long term, you hope to be able to say the annualised growth in the last ten years was better than putting my money in a bank or in bonds and it beat inflation.

Gassing Station | Finance | Top of Page | What's New | My Stuff