Your questions answered Vol 2 - IM Private Clients

Discussion

I mentioned a few weeks ago that Vertex Pharma (PHT) was granted Breakthrough Therapy Designation for VX-548 due to its promising test results. A very rare accelerated testing protocol awarded to drugs with exceptional promise.

The company announced today that it is entering Phase 3(final) testing in Q4

VX -548 inhibits the NaV1.8 electrical pain signals within the nervous system but most critically it is NON Opioid based. A real break through and something the market desperately needs.

The TAM (total addressable market) is $4B annually.

VX-548 is just one of several very promising new drugs, in-trial presently.

The company announced today that it is entering Phase 3(final) testing in Q4

VX -548 inhibits the NaV1.8 electrical pain signals within the nervous system but most critically it is NON Opioid based. A real break through and something the market desperately needs.

The TAM (total addressable market) is $4B annually.

VX-548 is just one of several very promising new drugs, in-trial presently.

Edited by AdamIM on Friday 22 July 16:29

Microsoft reported Fiscal Q4/2022 earnings last night.

Top line growth +18% for the 12 months ending 30/6/22 and +12% for the 3 month quarter which was impacted by 5% FX headwinds (equates to $600M). Net income in the quarter was negatively impacted by a $126M charge relating to exit costs (Russia) and other income was (47M) cf +1.18B in the year ago quarter due to mark to market on their equity investments which is no surprise. These are non cash.

The only weakness during the quarter being Linkedin which grew double 26%, still suffered $100M lost advertising revenue. The china lockdown impacted PC sales which in turn impacted 365 and related software uptake ($300M)

As you can see from their results, they are rock solid and growing double digits on top and bottom lines.

Guidance is reaffirmed and strong for Fiscal 23 double digit growth!

The positives:

1. The CFO noted that there is NO IMPACT on large corporate Azure deals. And the number of 100M-1B new business is growing. Azure generated +40% revenue gains YoY(46% constant currency). The business invested an incremental $2.1B into cloud infrastructure with a view to accelerate this business and take market share during this period of uncertainty which MSFT see as an opportunity.

2. The CEO said that software is deflationary 'do more with less(spend)'. In uncertain times corporates will invest heavily in efficiency tools.

Top line growth +18% for the 12 months ending 30/6/22 and +12% for the 3 month quarter which was impacted by 5% FX headwinds (equates to $600M). Net income in the quarter was negatively impacted by a $126M charge relating to exit costs (Russia) and other income was (47M) cf +1.18B in the year ago quarter due to mark to market on their equity investments which is no surprise. These are non cash.

The only weakness during the quarter being Linkedin which grew double 26%, still suffered $100M lost advertising revenue. The china lockdown impacted PC sales which in turn impacted 365 and related software uptake ($300M)

As you can see from their results, they are rock solid and growing double digits on top and bottom lines.

Guidance is reaffirmed and strong for Fiscal 23 double digit growth!

The positives:

1. The CFO noted that there is NO IMPACT on large corporate Azure deals. And the number of 100M-1B new business is growing. Azure generated +40% revenue gains YoY(46% constant currency). The business invested an incremental $2.1B into cloud infrastructure with a view to accelerate this business and take market share during this period of uncertainty which MSFT see as an opportunity.

2. The CEO said that software is deflationary 'do more with less(spend)'. In uncertain times corporates will invest heavily in efficiency tools.

Alphabet (GOOG) reported Q2/2022 results last night. A very robust result; Revenue growth +13% albeit earnings down $2.5B which was due to FX 5% ($2B) and an unrealised loss of $497M compared to a gain of $2B(2021) relating to mark to market on their significant Bond portfolio (100b+).

We have to remember GOOG's biggest hurdle is their 2021 comparatives which saw revenue and earnings grow +70% in 2021 so to lap these figures is impressive.

The business added 30,000 additional staff during the period Q2/21 to Q2/22, an increase of 21%. This also impacted operating expenses but a clear sign the company is investing for the future.

Highlights are:

Heavy investment in AI, Search and Cloud. In particular transformational big bets on AI in the form of new ways to search, such as Google Lens which enables visual searches and multi search which combines words and images.

Using Augmented reality and 3D images for Google Shops to allow customers to 'try before they buy'

Hardware releases includingPixel Buds and Pixel watch together with A/R glasses and a range of updated phones.

Way robo-taxi began charging riders in San Fransisco and is one step closer to full commercialisation with 100% autonomous services.

Their Wing division surpassed 250,000 drone deliveries and unveiled a range of drone prototypes to handle a range of different sized packages. the company is excited about the future prospects in this field.

We have to remember GOOG's biggest hurdle is their 2021 comparatives which saw revenue and earnings grow +70% in 2021 so to lap these figures is impressive.

The business added 30,000 additional staff during the period Q2/21 to Q2/22, an increase of 21%. This also impacted operating expenses but a clear sign the company is investing for the future.

Highlights are:

Heavy investment in AI, Search and Cloud. In particular transformational big bets on AI in the form of new ways to search, such as Google Lens which enables visual searches and multi search which combines words and images.

Using Augmented reality and 3D images for Google Shops to allow customers to 'try before they buy'

Hardware releases includingPixel Buds and Pixel watch together with A/R glasses and a range of updated phones.

Way robo-taxi began charging riders in San Fransisco and is one step closer to full commercialisation with 100% autonomous services.

Their Wing division surpassed 250,000 drone deliveries and unveiled a range of drone prototypes to handle a range of different sized packages. the company is excited about the future prospects in this field.

share prices all round are up nicely.

Both companies did very well, in particular Google which on the face of it isn't its usual 20% revenue growth but one must remember they they drove 80% growth during Covid. Call it a two-year-stack. So to lap this extraordinary result is some feat.

These results from MSFT/GOOG resonate with investors -their models and growth stories are intact

In my opinion GOOG is the cheapest gilt edged security out there, trading at a multiple of around 16 when it deserves to be closer to 30

Both companies did very well, in particular Google which on the face of it isn't its usual 20% revenue growth but one must remember they they drove 80% growth during Covid. Call it a two-year-stack. So to lap this extraordinary result is some feat.

These results from MSFT/GOOG resonate with investors -their models and growth stories are intact

In my opinion GOOG is the cheapest gilt edged security out there, trading at a multiple of around 16 when it deserves to be closer to 30

Finally had a look at my investments last night, not dared look since the start of February.

Vanguard is down, but still above my initial investment, so surprised and happy with that.

My IM is split into 3 parts , and the index 100 and 80 are looking ok, but PH opportunity is well down, and needs a kick up the arse. In hindsight I should have left it in the two index groups.

Overall considering the losses I was expecting, it's not looking too bad, and hoping will recover back to making some money at some point.

Vanguard is down, but still above my initial investment, so surprised and happy with that.

My IM is split into 3 parts , and the index 100 and 80 are looking ok, but PH opportunity is well down, and needs a kick up the arse. In hindsight I should have left it in the two index groups.

Overall considering the losses I was expecting, it's not looking too bad, and hoping will recover back to making some money at some point.

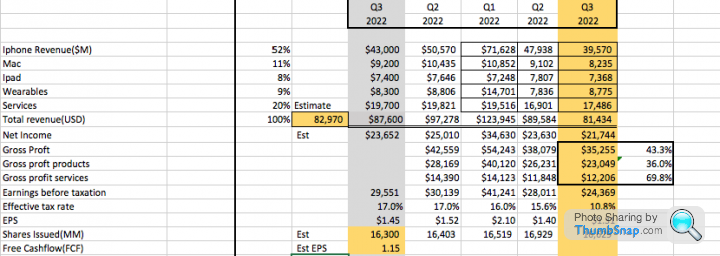

Apple report tonight-analyst expectations are low with estimates pegged at $82.9B and $1.15 eps. For what it's worth I don't think wall Street analysts have it remotely close.

Recently Apple lowered their iPhone trade in prices which indicates to me that their sales are robust. There will be lower China sales due to lock down and some logistical issues but not as bad as analysts are predicting (imo). Revenues will be impacted by FX in the range 3 to 3.5% but only on around 50% of their sales as the lions share is North America. And some of their debt is Euro denominated so they probably made a gain on revaluation there. I think they will do much better than $1.15 eps. maybe into the 1.40's is my call. We will soon see

Recently Apple lowered their iPhone trade in prices which indicates to me that their sales are robust. There will be lower China sales due to lock down and some logistical issues but not as bad as analysts are predicting (imo). Revenues will be impacted by FX in the range 3 to 3.5% but only on around 50% of their sales as the lions share is North America. And some of their debt is Euro denominated so they probably made a gain on revaluation there. I think they will do much better than $1.15 eps. maybe into the 1.40's is my call. We will soon see

Edited by AdamIM on Thursday 28th July 16:17

AdamIM said:

Apple report tonight-analyst expectations are low with estimates pegged at $82.9B and $1.15 eps. For what it's worth I don't think wall Street analysts have it remotely close.

Recently Apple lowered their iPhone trade in prices which indicates to me that their sales are robust. There will be lower China sales due to lock down and some logistical issues but not as bad as analysts are predicting (imo). Revenues will be impacted by FX in the range 3 to 3.5% but only on around 50% of their sales as the lions share is North America. And some of their debt is Euro denominated so they probably made a gain on revaluation there. I think they will do much better than $1.15 eps. maybe into the 1.40's is my call. We will soon see

so is that a bet your house on or a sell as its going to plummet? Recently Apple lowered their iPhone trade in prices which indicates to me that their sales are robust. There will be lower China sales due to lock down and some logistical issues but not as bad as analysts are predicting (imo). Revenues will be impacted by FX in the range 3 to 3.5% but only on around 50% of their sales as the lions share is North America. And some of their debt is Euro denominated so they probably made a gain on revaluation there. I think they will do much better than $1.15 eps. maybe into the 1.40's is my call. We will soon see

superlightr said:

AdamIM said:

Apple report tonight-analyst expectations are low with estimates pegged at $82.9B and $1.15 eps. For what it's worth I don't think wall Street analysts have it remotely close.

Recently Apple lowered their iPhone trade in prices which indicates to me that their sales are robust. There will be lower China sales due to lock down and some logistical issues but not as bad as analysts are predicting (imo). Revenues will be impacted by FX in the range 3 to 3.5% but only on around 50% of their sales as the lions share is North America. And some of their debt is Euro denominated so they probably made a gain on revaluation there. I think they will do much better than $1.15 eps. maybe into the 1.40's is my call. We will soon see

so is that a bet your house on or a sell as its going to plummet? Recently Apple lowered their iPhone trade in prices which indicates to me that their sales are robust. There will be lower China sales due to lock down and some logistical issues but not as bad as analysts are predicting (imo). Revenues will be impacted by FX in the range 3 to 3.5% but only on around 50% of their sales as the lions share is North America. And some of their debt is Euro denominated so they probably made a gain on revaluation there. I think they will do much better than $1.15 eps. maybe into the 1.40's is my call. We will soon see

A business like Apple doesn't tend to move the needle materially over earnings like many others due to its colossal size. I just find it interesting that historically, analysts get it most wrong with this company.

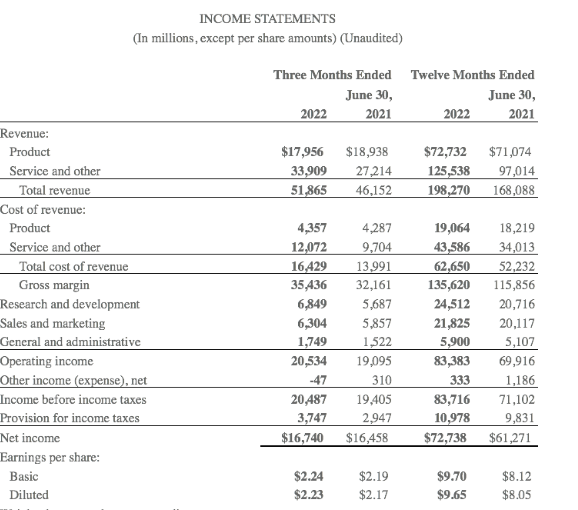

A business like Apple doesn't tend to move the needle materially over earnings like many others due to its colossal size. I just find it interesting that historically, analysts get it most wrong with this company.Apple came in with $83B and $1.30. Listening to the conference call Live last night, hosted by Tim Cook and Luca Maestri (CFO) there were 4 key areas which constrained the quarter.

1. China Lockdown severely impacted supply of all hardware, particularly iPhone and Mac

2. China Lockdown severely dampened demand for iPhone

3. FX headwinds of 600bps (huge)

4. Russia exit which not only reflects lost revenue but added exit costs.

On a positive note, given the about the business did extremely well, actually growing top and bottom lines. A record Q3

The company expects September(Q4 fiscal) to show accelerating revenues as according to Cook, there is no let up in demand and their supply channels are in better shape than in the previous quarter. During Q3 they generated a record $19.6B in services revenue and this was at a 71.5% Gross Margin. $14B Gross Profit just from services(this can only grow long term) due to their 1B iPhone installed based and 1.3B iOS device installed base.

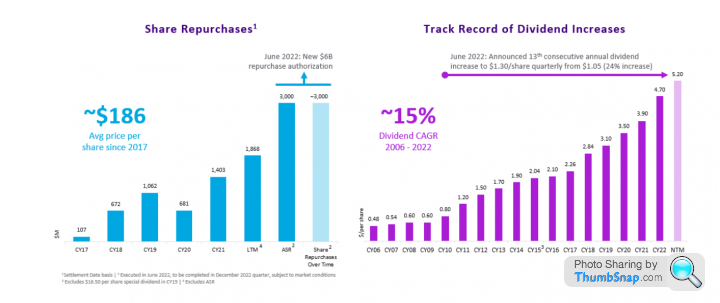

Apple returned $26B to stock holders via buy backs and dividends during the quarter.

The company hinted at new product releases in the Augmented Reality space-it is no secret that a new headset is due out in the next 6 months. The company also hired ex lamborghini head of chassis development to work on their autonomous vehicle which is expected in 2024.

Amazon reported a loss of $2B however this includes a non cash write down of $3.9B relating to their Rivian stake. AWS grew 33% YoY. Amazon guided for growth exceeding expectations. The company said it is navigating inflationary pressures well and has a good handle on its inventory volumes. Its advertising business grew 18% to $8.7B which is interesting in that it(and Google) are showing strength in this sector cf SNAP and Meta who are contracting. It show's albeit anecdotally that need driven search is intact vs data harvesting for other reasons is on the decline.

1. China Lockdown severely impacted supply of all hardware, particularly iPhone and Mac

2. China Lockdown severely dampened demand for iPhone

3. FX headwinds of 600bps (huge)

4. Russia exit which not only reflects lost revenue but added exit costs.

On a positive note, given the about the business did extremely well, actually growing top and bottom lines. A record Q3

The company expects September(Q4 fiscal) to show accelerating revenues as according to Cook, there is no let up in demand and their supply channels are in better shape than in the previous quarter. During Q3 they generated a record $19.6B in services revenue and this was at a 71.5% Gross Margin. $14B Gross Profit just from services(this can only grow long term) due to their 1B iPhone installed based and 1.3B iOS device installed base.

Apple returned $26B to stock holders via buy backs and dividends during the quarter.

The company hinted at new product releases in the Augmented Reality space-it is no secret that a new headset is due out in the next 6 months. The company also hired ex lamborghini head of chassis development to work on their autonomous vehicle which is expected in 2024.

Amazon reported a loss of $2B however this includes a non cash write down of $3.9B relating to their Rivian stake. AWS grew 33% YoY. Amazon guided for growth exceeding expectations. The company said it is navigating inflationary pressures well and has a good handle on its inventory volumes. Its advertising business grew 18% to $8.7B which is interesting in that it(and Google) are showing strength in this sector cf SNAP and Meta who are contracting. It show's albeit anecdotally that need driven search is intact vs data harvesting for other reasons is on the decline.

KLA Corporation deliver the goods, again. Beating on top and bottom lines. +29% Revenue growth and same EPS growth. KLAC trades at a low PE of 17 with a deep double digit growth rate. the company has visibility far into the future given contractual obligations with leading semi foundries. The company is guiding out to 2026 with Growth in Revenue and EPS of at least 100% over this period.

As you can see the company is an avid buyer of its own stock and has a long history of dividend growth.

Comments

Despite the macro and supply chain headwinds, KLA see the secular trends driving semiconductor growth and investments in Wafers as both durable and compelling over the long run.

Broad-based customer demand and simultaneous investments supporting growing semiconductor content across technology nodes remain intact.

These are long-term secular growth drivers for the industry, as technology investment and the resumption of scaling reflects the value that semiconductors and the industry have in lowering cost to end customers and enabling a broader adoption for semiconductor-based technology across multiple end-markets. Essentially-semiconductors are everywhere and growing

The company's track record of execution and the power of its product portfolio- management continue to deliver sustainable outperformance throughout changing economic periods. As one looks at the leading indicators for its business, including their backlog and sales channel visibility, they continue to excel. KLAC is by far the market leader in its field with a very bright future.

As you can see the company is an avid buyer of its own stock and has a long history of dividend growth.

Comments

Despite the macro and supply chain headwinds, KLA see the secular trends driving semiconductor growth and investments in Wafers as both durable and compelling over the long run.

Broad-based customer demand and simultaneous investments supporting growing semiconductor content across technology nodes remain intact.

These are long-term secular growth drivers for the industry, as technology investment and the resumption of scaling reflects the value that semiconductors and the industry have in lowering cost to end customers and enabling a broader adoption for semiconductor-based technology across multiple end-markets. Essentially-semiconductors are everywhere and growing

The company's track record of execution and the power of its product portfolio- management continue to deliver sustainable outperformance throughout changing economic periods. As one looks at the leading indicators for its business, including their backlog and sales channel visibility, they continue to excel. KLAC is by far the market leader in its field with a very bright future.

Colgate-PHE came in with a decent report card for the quarter as it navigates higher input costs via price rises, affirming its defensive nature and guides higher.

Colgate-Palmolive Non-GAAP EPS of $0.72 beats by $0.01, revenue of $4.48B beats by $130M

Colgate-Palmolive (CL): Q2 Non-GAAP EPS of $0.72 beats by $0.01.

Revenue of $4.48B (+5.2% Y/Y) beats by $130M.

The company raised its sales growth guidance for full year 2022 to 5% to 7%.

Colgate-Palmolive Non-GAAP EPS of $0.72 beats by $0.01, revenue of $4.48B beats by $130M

Colgate-Palmolive (CL): Q2 Non-GAAP EPS of $0.72 beats by $0.01.

Revenue of $4.48B (+5.2% Y/Y) beats by $130M.

The company raised its sales growth guidance for full year 2022 to 5% to 7%.

Gassing Station | Finance | Top of Page | What's New | My Stuff