When/Will house prices cool down?

Discussion

Jiebo said:

mike74 said:

There wasn't a crash in 2008, just a minor blip followed by a stagnant, sluggish market for a few years before the QE/ZIRP washed through the system and took effect.

Many areas outside of London crashed by 25%. Back then I had just graduated, and the houses around where my parents lived dropped by 30% in some cases and didn’t recover for a few years. Here's PensionCraft's report on 2022: https://youtu.be/iWjeLF7RT8o?t=564

What I haven't seen anywhere is separation of freeholds v leaseholds (particularly apartments) in modelling. I think freeholds and leaseholds will go in very different directions next year, unless legislation is brought in to protect leaseholders from the various ongoing scandals.

A surprising number of houses are now leasehold as well, and come with management fees.

What I haven't seen anywhere is separation of freeholds v leaseholds (particularly apartments) in modelling. I think freeholds and leaseholds will go in very different directions next year, unless legislation is brought in to protect leaseholders from the various ongoing scandals.

A surprising number of houses are now leasehold as well, and come with management fees.

Edited by Grrbang on Sunday 14th November 20:10

Grrbang said:

Here's PensionCraft's report on 2022: https://youtu.be/iWjeLF7RT8o?t=564

What I haven't seen anywhere is separation of freeholds v leaseholds (particularly apartments) in modelling. I think freeholds and leaseholds will go in very different directions next year, unless legislation is brought in to protect leaseholders from the various ongoing scandals.

A surprising number of houses are now leasehold as well, and come with management fees.

Leasehold reform should be a priority, particularly as younger people will be completely priced out of freeholds in cities such as London within the next 10 years. What I haven't seen anywhere is separation of freeholds v leaseholds (particularly apartments) in modelling. I think freeholds and leaseholds will go in very different directions next year, unless legislation is brought in to protect leaseholders from the various ongoing scandals.

A surprising number of houses are now leasehold as well, and come with management fees.

Edited by Grrbang on Sunday 14th November 20:10

There seems to be a lot of lethargy, which I suspect isn’t helped by the ultimate beneficial owners of the freeholds and management companies, who also happen to be in powerful positions in government and the legal system. There is a chap in the House of Lords who owns hundreds of freeholds and management companies, which although isn’t illegal, but does create bias and hinders progress for the ‘commoners’.

Leasehold is going to be interesting, I bought my place as leasehold and it was approx 15k cheaper than the neighbors who is freehold, lease is not onerous £12 per year ground rent for the next 940 years, no service charge and no increase in ground rent.

The whole leasehold issue is dependent on the details, if you look past the headline of lease you can get some very good deals

The whole leasehold issue is dependent on the details, if you look past the headline of lease you can get some very good deals

okgo said:

Joey Deacon said:

Agreed, nice houses in nice areas near to decent schools are cast iron investments.

To a level. Yes. Now I am not saying they won't go higher or won't drop.

It was more the fact I am sure back in 2008 when someone purchased something for close to 700k thought well this is a secure investment, brilliant area, excellent schools - it can only go up, yet its taken this long just to get back to the same levels.

Obviously something silly like 50% drop isn't going to happen but 10-20%, is that possible? I don't know. Can people absorb that sort of reduction? I assume that would be pretty much someones deposit erroded away.

Who knows

The market will dip and raise correspondingly to greater economic and social cycles, however the overall trend as with all inflation linked and finite commodity goods is up.

The issue you have is firstly trying to judge what point of the cycle we are in (impossible) and the second is what point of the cycle we are in when you find yourself at the point in life where you want or need to make changes to your housing (also impossible to completely control).

Summary- you can buy smart in up and coming areas, or put energy and time and money into renovations and 'see' something someone else may not, so obtain relative value, but trying to beat averages or bend your life timings to suit property cycles for your primary property is a waste of energy and time imho. Find somewhere you love, buy it, get on with life.

Non primary property decisions are a little different imho.

The issue you have is firstly trying to judge what point of the cycle we are in (impossible) and the second is what point of the cycle we are in when you find yourself at the point in life where you want or need to make changes to your housing (also impossible to completely control).

Summary- you can buy smart in up and coming areas, or put energy and time and money into renovations and 'see' something someone else may not, so obtain relative value, but trying to beat averages or bend your life timings to suit property cycles for your primary property is a waste of energy and time imho. Find somewhere you love, buy it, get on with life.

Non primary property decisions are a little different imho.

Chamon_Lee said:

I think its always easy to say that but in reality who knows. There is a particular area I am looking at which has some of the best schools around and having extensively looked through the data of houses sold, some are only JUST getting to the price they paid for them back in 2008.

Now I am not saying they won't go higher or won't drop.

It was more the fact I am sure back in 2008 when someone purchased something for close to 700k thought well this is a secure investment, brilliant area, excellent schools - it can only go up, yet its taken this long just to get back to the same levels.

Obviously something silly like 50% drop isn't going to happen but 10-20%, is that possible? I don't know. Can people absorb that sort of reduction? I assume that would be pretty much someones deposit erroded away.

Who knows

Another potential issue is that nearly 70% of Outstanding schools have been downgraded, according to recent stats. Ofsted's priorities have changed but public awareness hasn't.Now I am not saying they won't go higher or won't drop.

It was more the fact I am sure back in 2008 when someone purchased something for close to 700k thought well this is a secure investment, brilliant area, excellent schools - it can only go up, yet its taken this long just to get back to the same levels.

Obviously something silly like 50% drop isn't going to happen but 10-20%, is that possible? I don't know. Can people absorb that sort of reduction? I assume that would be pretty much someones deposit erroded away.

Who knows

Grrbang said:

Another potential issue is that nearly 70% of Outstanding schools have been downgraded, according to recent stats. Ofsted's priorities have changed but public awareness hasn't.

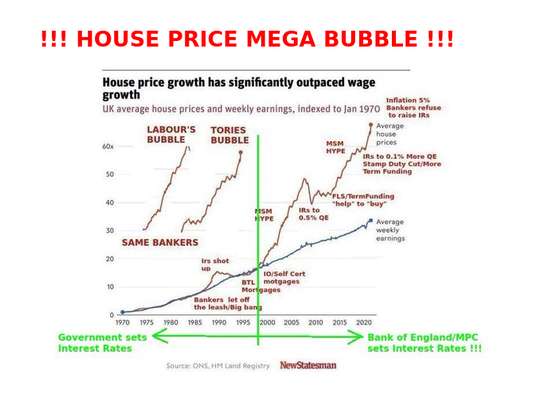

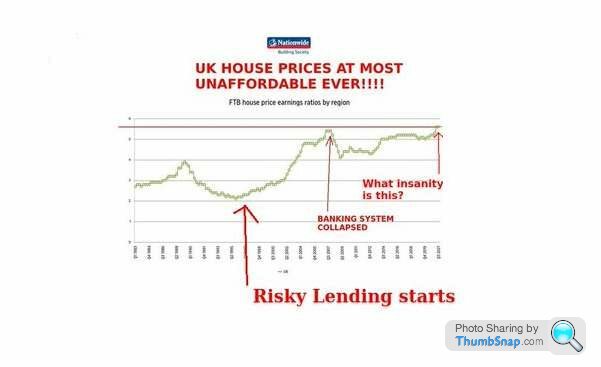

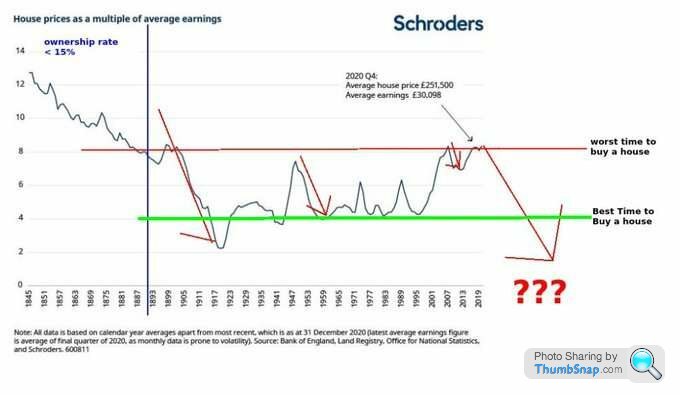

Any links to that? Ofsted barely manage two inspections a decade, so I'd be interested to know how they've got through so many schools and downgraded them?I notice my good name is being used in vein here so here are some charts for the good folk of piston heads to mull over.

And yes, since 2000 there has never been a worse time to buy a house, esp if you are a FTB. If/when prices revert to the average a lot of people are going to lose a lot of "wealth", wealth that maybe they have been relying on for retirement or such like. If you never realize your gains it's not actually wealth !!!

People don't seem to have twigged that the housing market has been an investment scam since 1998, whenTony Bliar introduced the 1998 banking act and let the BoE take over "the economy". Everyone should be angry as hell that so much of their own taxes/wealth/futures have been throw at the bankers and their scam. Even post banking system collapse people seem to happy with their magical wealth they are willing to look through systematic corruption, theft and fraud.

Sure, the bankers/politicians can and have delayed the inevitable correction in house prices but either nominally or in real terms prices will revert. It would be naive to think otherwise, the housing market is little more than a pyramid/ponzi scam, a sure metric of this is if people can afford to buy their own house, millions can't and certainly not on the wages they would have done in the past.

The currently levels of insanity are there for anyone to cares to look:

Here's house prices relative to wages, give IRs are 0.1% this means the prices are extreme !!!

The following two graphs show house prices relative to wage multiples with these levels at an all time high, now above the insane levels that collapsed the banking system and remember, tax payers are on the hook for the bankers losses now, so they dont care who they lend to ( sub-prime debt ) !!!

The only thing I find odd is the house prices relative to inflation chart ( posted on a previous page ), which shows that house prices haven't kept up with inflation ( certainly not outside London for sure ) and they could now actually be rising from the bottom of the cycle which is odd given the insane prices, this does mean that most savings account have out performed house prices since 2007, hard to believe for millions who think they are accumulating wealth but there you have it, the numbers dont lie, only banker, politicians and newspaper editors do.

If you could transport back to 1999 the best investment options you could have take were:

1999: Buy house In London

2006: Sell house/Buy Gold

2010: Sell gold, buy shares

2014: Sell shares, buy bitcoin.

2021: Sell bit coin buy private island, 10 dancing girls and a several private jets.

But hey, buy a house in a massively over priced market, you can't lose on bricks on mortar...they billionaire owned press tell you.

Going forward, there are sadly few good options for people to maintain their money/wealth/savings. The Bank Of England refuse to act in the best interest of the British people ( raise IRS) and the ex-banker son in law of a foreign billionaire Rishi Sunake seems prepared to make people's savings/wages worthless through inflation to force them to spend into the establishments economy/housing market. ( You will own nothing and be happy, he's even said he wants to stop people hoarding money, coming from a multi-millionaire banker with 10 houses, that is something !!! ).

If the BoE don't change course now then now is actually a great time to lever up and buy a house with all that money you made from investing from 2000 to now and let the inflation clear the debt.

However, of course, there is always the chance ( a good chance ) that the BoE/The £ will face a crisis and they will have to do the right thing and raise IRs, at which point the nominal house price collapse is nailed on, imagine 5% IRs now ?

It's impossible to know what these charlatans will do next but the BoE ignoring the inflation this month and refusing to raise IRs was telling, I expect more of the same, so if come Feb it'll be clear that path the bankers are taking. Mr Bailey and at least 1 more member of the BoE's MPC wants -ve IRs ( insanity to a new level ) and 1 other member is an ex-Goldman Sachs banker like Sunak ( coincidence ? ) and his mate who is now in charge of the BBC ( more coincidence ? ).

You make your own choices in life, but one thing for sure it....as of today, there has still never been a worse time to buy a house.

Come Feb next year it might be the only sane thing you could possible do.

I just wanted to post this because I see one of the trolls from HPC has been having a dig. He wont have told you that the original CoN left to live in France, disgusted at the actions of the Tories/Bankers and spurred on by death threats from internet trolls. I run the housepricemania twitter feed for him and post on his account. Trolly Mc Troll Face wont have told you that CoN number 2, ME, has accumulated nearly £3M in actual tangible fluid wealth since 2000 by not buying a house, the interest from just a fraction of that covers my rent ( buy is dead money, who knew ).

If you want some decent information on the economy/investing and what is really happen, you could do no better than follow this thread/forum, it's a more sensible version of the HPC forum:

https://www.dosbods.co.uk/topic/18761-credit-defla...

Anyway, good luck, 2022 is going to be an "interesting" year.

And yes, since 2000 there has never been a worse time to buy a house, esp if you are a FTB. If/when prices revert to the average a lot of people are going to lose a lot of "wealth", wealth that maybe they have been relying on for retirement or such like. If you never realize your gains it's not actually wealth !!!

People don't seem to have twigged that the housing market has been an investment scam since 1998, whenTony Bliar introduced the 1998 banking act and let the BoE take over "the economy". Everyone should be angry as hell that so much of their own taxes/wealth/futures have been throw at the bankers and their scam. Even post banking system collapse people seem to happy with their magical wealth they are willing to look through systematic corruption, theft and fraud.

Sure, the bankers/politicians can and have delayed the inevitable correction in house prices but either nominally or in real terms prices will revert. It would be naive to think otherwise, the housing market is little more than a pyramid/ponzi scam, a sure metric of this is if people can afford to buy their own house, millions can't and certainly not on the wages they would have done in the past.

The currently levels of insanity are there for anyone to cares to look:

Here's house prices relative to wages, give IRs are 0.1% this means the prices are extreme !!!

The following two graphs show house prices relative to wage multiples with these levels at an all time high, now above the insane levels that collapsed the banking system and remember, tax payers are on the hook for the bankers losses now, so they dont care who they lend to ( sub-prime debt ) !!!

The only thing I find odd is the house prices relative to inflation chart ( posted on a previous page ), which shows that house prices haven't kept up with inflation ( certainly not outside London for sure ) and they could now actually be rising from the bottom of the cycle which is odd given the insane prices, this does mean that most savings account have out performed house prices since 2007, hard to believe for millions who think they are accumulating wealth but there you have it, the numbers dont lie, only banker, politicians and newspaper editors do.

If you could transport back to 1999 the best investment options you could have take were:

1999: Buy house In London

2006: Sell house/Buy Gold

2010: Sell gold, buy shares

2014: Sell shares, buy bitcoin.

2021: Sell bit coin buy private island, 10 dancing girls and a several private jets.

But hey, buy a house in a massively over priced market, you can't lose on bricks on mortar...they billionaire owned press tell you.

Going forward, there are sadly few good options for people to maintain their money/wealth/savings. The Bank Of England refuse to act in the best interest of the British people ( raise IRS) and the ex-banker son in law of a foreign billionaire Rishi Sunake seems prepared to make people's savings/wages worthless through inflation to force them to spend into the establishments economy/housing market. ( You will own nothing and be happy, he's even said he wants to stop people hoarding money, coming from a multi-millionaire banker with 10 houses, that is something !!! ).

If the BoE don't change course now then now is actually a great time to lever up and buy a house with all that money you made from investing from 2000 to now and let the inflation clear the debt.

However, of course, there is always the chance ( a good chance ) that the BoE/The £ will face a crisis and they will have to do the right thing and raise IRs, at which point the nominal house price collapse is nailed on, imagine 5% IRs now ?

It's impossible to know what these charlatans will do next but the BoE ignoring the inflation this month and refusing to raise IRs was telling, I expect more of the same, so if come Feb it'll be clear that path the bankers are taking. Mr Bailey and at least 1 more member of the BoE's MPC wants -ve IRs ( insanity to a new level ) and 1 other member is an ex-Goldman Sachs banker like Sunak ( coincidence ? ) and his mate who is now in charge of the BBC ( more coincidence ? ).

You make your own choices in life, but one thing for sure it....as of today, there has still never been a worse time to buy a house.

Come Feb next year it might be the only sane thing you could possible do.

I just wanted to post this because I see one of the trolls from HPC has been having a dig. He wont have told you that the original CoN left to live in France, disgusted at the actions of the Tories/Bankers and spurred on by death threats from internet trolls. I run the housepricemania twitter feed for him and post on his account. Trolly Mc Troll Face wont have told you that CoN number 2, ME, has accumulated nearly £3M in actual tangible fluid wealth since 2000 by not buying a house, the interest from just a fraction of that covers my rent ( buy is dead money, who knew ).

If you want some decent information on the economy/investing and what is really happen, you could do no better than follow this thread/forum, it's a more sensible version of the HPC forum:

https://www.dosbods.co.uk/topic/18761-credit-defla...

Anyway, good luck, 2022 is going to be an "interesting" year.

Good morning thecountofnowhere, nice to see you. As somebody who has dipped in and out of HousePriceCrash for over 15 years are you still not prepared to admit you were all wrong?

Also at what point do you think the majority of posters on your forum would be prepared to buy a house, and why were they not prepared to buy a house when prices were actually at that level?

Serious question, I am not trolling I just find the whole mentality interesting, it is almost as if most posters are terrified of buying a house no matter what the price incase prices fall.

Also at what point do you think the majority of posters on your forum would be prepared to buy a house, and why were they not prepared to buy a house when prices were actually at that level?

Serious question, I am not trolling I just find the whole mentality interesting, it is almost as if most posters are terrified of buying a house no matter what the price incase prices fall.

thecountofnowhere said:

If you could transport back to 1999 the best investment options you could have take were:

1999: Buy house In London

2006: Sell house/Buy Gold

2010: Sell gold, buy shares

2014: Sell shares, buy bitcoin.

2021: Sell bit coin buy private island, 10 dancing girls and a several private jets.

This is a bit of a pointless argument as with hindsight everybody would have just bought bitcoin in 2008 and been multi billionaires today.1999: Buy house In London

2006: Sell house/Buy Gold

2010: Sell gold, buy shares

2014: Sell shares, buy bitcoin.

2021: Sell bit coin buy private island, 10 dancing girls and a several private jets.

Is the logic dont buy now, leverage the cash by doing XYZ to be ahead?

If so, a roadmap of predictions would be good to benchmark off... as with bookies, everyone is a winner when aftertiming

You have £250k cash now, and say need to spend £2k on rent as you need a roof over your head. Say household of two, £40k pa each.

What is your plan that will emerge better than buying somewhere with reasonable mortgage, and over what timeframes?

If so, a roadmap of predictions would be good to benchmark off... as with bookies, everyone is a winner when aftertiming

You have £250k cash now, and say need to spend £2k on rent as you need a roof over your head. Say household of two, £40k pa each.

What is your plan that will emerge better than buying somewhere with reasonable mortgage, and over what timeframes?

thecountofnowhere said:

I notice my good name is being used in vein here so here are some charts for the good folk of piston heads to mull over.

You’re not seriously expecting people to believe that those charts, complete with the annotations, actually came from the likes of Nationwide or Schroders?

thecountofnowhere said:

I run the housepricemania twitter feed for him and post on his account. Trolly Mc Troll Face wont have told you that CoN number 2, ME, has accumulated nearly £3M in actual tangible fluid wealth since 2000 by not buying a house, the interest from just a fraction of that covers my rent ( buy is dead money, who knew ).

Even if true, the irony there is immense. £3M invested in property, even at a 5% yield, would see you clearing rather more than you’ll be earning in interest… and would have benefitted from significant asset price inflation over the past 20 years. gibbon said:

Summary- you can buy smart in up and coming areas, or put energy and time and money into renovations and 'see' something someone else may not, so obtain relative value, but trying to beat averages or bend your life timings to suit property cycles for your primary property is a waste of energy and time imho. Find somewhere you love, buy it, get on with life.

Great post. Exactly the way I see it and it continues to work well for me.mwstewart said:

Did I really just read that the average savings account outperformed house prices since 2007?

I thought you must be mistaken, but rereading the post that appears to be exactly what he is saying. Here are the average interest rates on savings accounts since 20072020 0.64

2019 1.39

2018 1.18

2017 1.00

2016 1.23

2015 1.40

2014 1.48

2013 1.77

2012 2.80

2011 2.75

2010 2.80

2009 2.21

2008 5.09

2007 5.55

This is the first house near me I found on Rightmove that has sold recently and also in 2007

27, Cheyne Hill, Surbiton, Greater London KT5 8BL

3 bed, semi-detached

£677,000 24 Jun 2021 Freehold

£385,000 5 Apr 2007 Freehold

£280,000 28 Sep 2004 Freehold

The house has increased in value by 75% since 2007. First there is no way a savings account has increased by this much, and secondly if you don't own a property then you have to rent unless you like living on the streets. Assuming 14 years of rental at an average of £1500 a month (that house would rent for way more than that now days) that works out at £252K in rent over the last 14 years.

But yes, having your money in the bank and renting is clearly a better move than buying.

Plus I have rented in the past and it is horrible. Firstly you are paying the landlords mortgage and retirement, you have to wait for the landlord to fix things (and they hate spending money) and you have no stability as you never know if the landlord will want to sell.

But obviously everyone on HousePriceCrash loves the freedom of renting and has £3 million in Bitcoin.

troika said:

I get the HPC argument. The problem is the game is rigged. It seems to me that the top govt priority is to stop house prices falling. Everything else can go to rat s t, as long as house prices increase. It makes people feel wealthy and wins elections.

t, as long as house prices increase. It makes people feel wealthy and wins elections.

agree - I sat listening to Goldman Investment MD a few years ago and he said exactly the same. "Wealth" is generated through house price inflation. Govt can not afford for prices to correct/decline as it will sink the economy. t, as long as house prices increase. It makes people feel wealthy and wins elections. Gassing Station | Finance | Top of Page | What's New | My Stuff