When/Will house prices cool down?

Discussion

coetzeeh said:

agree - I sat listening to Goldman Investment MD a few years ago and he said exactly the same. "Wealth" is generated through house price inflation. Govt can not afford for prices to correct/decline as it will sink the economy.

Absolutely, yet the HousePriceCrashers are convinced there is going to be a massive correction and people will be begging them to buy their houses. The reality is it is better to realise it is a rigged game, buy a house, forget about house prices and get on with life.funinhounslow said:

and they don’t mention the service charge which I’m guessing is significant. Pool, gym and 24 hour “concierge” can’t be cheap surely…?

I think the BPS redevelopment is more about everything else around, it really is a new town location, loads of great places to shop work eat, things to do with gyms and cinemas etcI’m so glad they’ve restored the power station, it’s easily my favourite building in The world.

18million though, that is madness

Joey Deacon said:

coetzeeh said:

agree - I sat listening to Goldman Investment MD a few years ago and he said exactly the same. "Wealth" is generated through house price inflation. Govt can not afford for prices to correct/decline as it will sink the economy.

Absolutely, yet the HousePriceCrashers are convinced there is going to be a massive correction and people will be begging them to buy their houses. The reality is it is better to realise it is a rigged game, buy a house, forget about house prices and get on with life.Joey Deacon said:

Absolutely, yet the HousePriceCrashers are convinced there is going to be a massive correction and people will be begging them to buy their houses. The reality is it is better to realise it is a rigged game, buy a house, forget about house prices and get on with life.

The HPC brigade also seem to think that everyone who buys, borrows to their absolute maximum. What if you bought a house you can comfortably afford on your salary and ALSO be in a position to invest your disposable income on the same Bitcoin investments that these genius renters are doing? pb8g09 said:

The HPC brigade also seem to think that everyone who buys, borrows to their absolute maximum. What if you bought a house you can comfortably afford on your salary and ALSO be in a position to invest your disposable income on the same Bitcoin investments that these genius renters are doing?

Exactly, I could have borrowed £100000 more than I did, but I had no need to. I moved to a different area, same distance to work, just not as "nice". Sold my wholly owned house in the more expensive area and have paid off the mortgage on the new place after a year. I now have twice the size of house I did a year ago and arguably I can borrow even more now should I wish to move.By "nice" I mean better schools more shops in the area. Where I live now is much nicer for me, small village with countryside and forest park on the doorstep. Arguably I may find it harder to sell in the future.

Edited by 46and2 on Friday 19th November 11:58

vulture1 said:

Government want people moving house lots. As that generates new curtains, new kitchen, new sofa etc

Not sure I agree.Nonsense on TV & gossip magazines generates the constant need and desire to redecorate. My childminder went through 3 full lounge overhauls with curtains, wallpaper, suites, tables etc in the 12 years I was going there. My parents redecorated theirs once in 35 years.

In our newbuild estate’s Facebook group, it appears 3-5 years is still the turnover point for kitchens and lounges.

thecountofnowhere said:

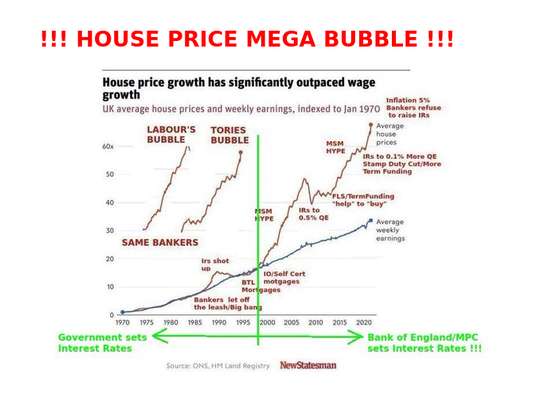

Very sobering .....says it all !

The fall in interest rates makes prices, of course, rise and the power of gearing of course, amplifies those gains yet further and sucks yet more into the market

Of course in a falling market, gearing amplifies those losses so you can lose all your equity and more !

Everything is hindsight.........

You can go back through the years and see that pretty much everything that could be done was done to avoid a harsh shock to the housing (all?) market(s), but it wasn't certain these would always be implemented? Did people see the descent of interest rates to pretty much zero?

It's hard now to imagine them doing anything to purposely harm the prices (eg recent stamp duty break), but over the last 20 years and now where prices are, you have first time buyers needing relatively huge deposits with student loans, high fuel/energy costs and interest rates flat at best (have to rise at some point?). Can they budget for rate rises, I suspect not much, but then as you say renting it painful and stops/elongates the deposit saving phase?

You also have early year owners with "Help to buy" which to me is the housing equivalent of a DFS Sofa where you can get in now and forget about some of the money you've borrowed for a few years, only it's not going away forever and at best will eat into any salary progression over the years.

Rock and a hard place!

So being a "the fundamentals don't make sense I'm not comfortable with things" person certainly hasn't paid off, but then declines are always sharper and shorter lived than the inclines. So you are always right more often to be on the upside and you can't argue with history but I can sympathise with the sentiment especially as the longer you've left it to take the plunge the more and more your gut tells you it's even worse!

You can go back through the years and see that pretty much everything that could be done was done to avoid a harsh shock to the housing (all?) market(s), but it wasn't certain these would always be implemented? Did people see the descent of interest rates to pretty much zero?

It's hard now to imagine them doing anything to purposely harm the prices (eg recent stamp duty break), but over the last 20 years and now where prices are, you have first time buyers needing relatively huge deposits with student loans, high fuel/energy costs and interest rates flat at best (have to rise at some point?). Can they budget for rate rises, I suspect not much, but then as you say renting it painful and stops/elongates the deposit saving phase?

You also have early year owners with "Help to buy" which to me is the housing equivalent of a DFS Sofa where you can get in now and forget about some of the money you've borrowed for a few years, only it's not going away forever and at best will eat into any salary progression over the years.

Rock and a hard place!

So being a "the fundamentals don't make sense I'm not comfortable with things" person certainly hasn't paid off, but then declines are always sharper and shorter lived than the inclines. So you are always right more often to be on the upside and you can't argue with history but I can sympathise with the sentiment especially as the longer you've left it to take the plunge the more and more your gut tells you it's even worse!

Scootersp said:

Everything is hindsight.........

You can go back through the years and see that pretty much everything that could be done was done to avoid a harsh shock to the housing (all?) market(s), but it wasn't certain these would always be implemented? Did people see the descent of interest rates to pretty much zero?

It's hard now to imagine them doing anything to purposely harm the prices (eg recent stamp duty break), but over the last 20 years and now where prices are, you have first time buyers needing relatively huge deposits with student loans, high fuel/energy costs and interest rates flat at best (have to rise at some point?). Can they budget for rate rises, I suspect not much, but then as you say renting it painful and stops/elongates the deposit saving phase?

You also have early year owners with "Help to buy" which to me is the housing equivalent of a DFS Sofa where you can get in now and forget about some of the money you've borrowed for a few years, only it's not going away forever and at best will eat into any salary progression over the years.

Rock and a hard place!

So being a "the fundamentals don't make sense I'm not comfortable with things" person certainly hasn't paid off, but then declines are always sharper and shorter lived than the inclines. So you are always right more often to be on the upside and you can't argue with history but I can sympathise with the sentiment especially as the longer you've left it to take the plunge the more and more your gut tells you it's even worse!

I take a very simpleton brutal attitude. As in 2008 any crash that comes will be triggered by banks restricting credit for whatever reason of which there could be many. All prices are pretty much dictated by bank evaluations of ability to pay rather than real value and no bank will be in a hurry to destroy its own balance sheet. If/when the next crash comes it’ll happen fast rather than a slow decline, but who knows when?You can go back through the years and see that pretty much everything that could be done was done to avoid a harsh shock to the housing (all?) market(s), but it wasn't certain these would always be implemented? Did people see the descent of interest rates to pretty much zero?

It's hard now to imagine them doing anything to purposely harm the prices (eg recent stamp duty break), but over the last 20 years and now where prices are, you have first time buyers needing relatively huge deposits with student loans, high fuel/energy costs and interest rates flat at best (have to rise at some point?). Can they budget for rate rises, I suspect not much, but then as you say renting it painful and stops/elongates the deposit saving phase?

You also have early year owners with "Help to buy" which to me is the housing equivalent of a DFS Sofa where you can get in now and forget about some of the money you've borrowed for a few years, only it's not going away forever and at best will eat into any salary progression over the years.

Rock and a hard place!

So being a "the fundamentals don't make sense I'm not comfortable with things" person certainly hasn't paid off, but then declines are always sharper and shorter lived than the inclines. So you are always right more often to be on the upside and you can't argue with history but I can sympathise with the sentiment especially as the longer you've left it to take the plunge the more and more your gut tells you it's even worse!

troika said:

I get the HPC argument. The problem is the game is rigged. It seems to me that the top govt priority is to stop house prices falling. Everything else can go to rat s t, as long as house prices increase. It makes people feel wealthy and wins elections.

t, as long as house prices increase. It makes people feel wealthy and wins elections.

If the game is rigged why do the HPC crowd keep predicting a crash? If you know it's rigged then surely you would pile in?t, as long as house prices increase. It makes people feel wealthy and wins elections. If not then it's like knowing a roulette table is rigger to favour black, but you keep betting on red.

okgo said:

fido said:

Then reduce SDLT - first time i'm looking at >50k just to move down the road - that will pay for a new extension.

Not even an issue for 99% of people buying houses for a couple of hundred grand though. roger.mellie said:

I take a very simpleton brutal attitude.

Simple solutions for complex problems mode:Some fag packet math on the subject and I think the government should make hay while the sun shines.

Remove GCT exemption for primary residence, allowable annual increase of inflation+(say)3%, allowance for money spent on significant refurbishments, landscaping and extensions. Anything over inflation+3% gets taxed at 50%.

Some worked examples suggest the only ones who will be “hurt” are in pockets of fairly ridiculous growth in London and some other patches of the south east. If you bought at £160k in 96 and are cashing out for multiple millions now, you’ve still done bloody well even with 50% tax levied on some of it.

Takes heat out the market and reduces the potential for such sales to banjo the markets in rural areas with ridiculously inflated equity looking for an out.

I’ve mentioned it before on here, clearly will never happen as it would be political suicide. Whilst these are all paper gains which have never been realised, people would still be apoplectic at “losing” some of the imaginary money they have been talking about for years at dinner parties.

emicen said:

Simple solutions for complex problems mode:

Some fag packet math on the subject and I think the government should make hay while the sun shines.

Remove GCT exemption for primary residence, allowable annual increase of inflation+(say)3%, allowance for money spent on significant refurbishments, landscaping and extensions. Anything over inflation+3% gets taxed at 50%.

Some worked examples suggest the only ones who will be “hurt” are in pockets of fairly ridiculous growth in London and some other patches of the south east. If you bought at £160k in 96 and are cashing out for multiple millions now, you’ve still done bloody well even with 50% tax levied on some of it.

Takes heat out the market and reduces the potential for such sales to banjo the markets in rural areas with ridiculously inflated equity looking for an out.

I’ve mentioned it before on here, clearly will never happen as it would be political suicide. Whilst these are all paper gains which have never been realised, people would still be apoplectic at “losing” some of the imaginary money they have been talking about for years at dinner parties.

Oh if I ruled the world etc gains on primary residence would be fully taxable. So you’ll not find much argument from me on that. But as a realist I don’t expect it to happen either. What’s the worst that could happen?, people, pensions, whatever having to invest in enterprises rather than bricks and mortar? Doesn’t sound that bad.Some fag packet math on the subject and I think the government should make hay while the sun shines.

Remove GCT exemption for primary residence, allowable annual increase of inflation+(say)3%, allowance for money spent on significant refurbishments, landscaping and extensions. Anything over inflation+3% gets taxed at 50%.

Some worked examples suggest the only ones who will be “hurt” are in pockets of fairly ridiculous growth in London and some other patches of the south east. If you bought at £160k in 96 and are cashing out for multiple millions now, you’ve still done bloody well even with 50% tax levied on some of it.

Takes heat out the market and reduces the potential for such sales to banjo the markets in rural areas with ridiculously inflated equity looking for an out.

I’ve mentioned it before on here, clearly will never happen as it would be political suicide. Whilst these are all paper gains which have never been realised, people would still be apoplectic at “losing” some of the imaginary money they have been talking about for years at dinner parties.

But entirely agreed on the simplistic solutions for complicated problems headliner point.

macstorm73 said:

Leasehold is going to be interesting, I bought my place as leasehold and it was approx 15k cheaper than the neighbors who is freehold, lease is not onerous £12 per year ground rent for the next 940 years, no service charge and no increase in ground rent.

The whole leasehold issue is dependent on the details, if you look past the headline of lease you can get some very good deals

I could not agree more - it is in the detail The whole leasehold issue is dependent on the details, if you look past the headline of lease you can get some very good deals

There is a great deal of hysteria over leasehold with lessees unable to sell their flats because the ground rent is more than 0.1% of the value of the flat or it is reviewed to the RPI every 5 years - utterly ridiculous - so long as the financial burden of the ground rent imposed on the property is reflected in the price paid it does not matter what the rent is - no problem if the ground rent is £5,000 per annum PROVIDED the price of the property is lowered by around £135k

Cladding - the campaigners would have you believe it is a kin to having petrol tanks strapped to the side of the building - again if the fire protection measures are tested and working correctly in a civilized block and the block is say 5 stories high - is there any real chance of being burnt alive - I dont think so

The campaign groups thanks to the power of the internet have succeeded in making leasehold a problem proposition

So as noted by macstorm73 this may be the time to consider buying leasehold - subject to examining the detail and taking a pragmatic view

okgo said:

fido said:

Then reduce SDLT - first time i'm looking at >50k just to move down the road - that will pay for a new extension.

Not even an issue for 99% of people buying houses for a couple of hundred grand though. But even if we're looking at the relatively few people who transact around London (say out to Zone 6) then a typical house will be over 500k and the buyer will be hit by a salary-like figure to move. When I bought my first place in Zone 4 - it was just a few £k!

Gassing Station | Finance | Top of Page | What's New | My Stuff