Enjoying Retirement

Discussion

PistonHead007 said:

If you've got any COPE and you still hit 35yrs of qualifying NIC then you're better off than someone who only hit the maximum flat rate (currently 35yrs for £179.60pw) because you get the full flat rate state pension and the COPE boost to whichever private pension you contracted out into.

If you've been contracted out you will need more than 35yrs to reach 35 qualifying years because of the NIC that was sent to your private pensions.

When it changed in 2016 anyone who had already accrued a combined basic + additional state pension at least as much as the flat rate wouldn't see any increase from further NIC. However, if you had built up more than the flat rate by 2016 the extra is protected and not lost. That's how you can end up with a full flat rate state pension with 32yrs NIC, it was made up when it was basic + additional and those contributions combined were worth more than one year of NIC now.

I understand. However my final salary pensions never mentioned at the time as wonderful as 3% employee contribution for a 1/60th final salary’s were that I’d take a slightly lower state pension. If you've been contracted out you will need more than 35yrs to reach 35 qualifying years because of the NIC that was sent to your private pensions.

When it changed in 2016 anyone who had already accrued a combined basic + additional state pension at least as much as the flat rate wouldn't see any increase from further NIC. However, if you had built up more than the flat rate by 2016 the extra is protected and not lost. That's how you can end up with a full flat rate state pension with 32yrs NIC, it was made up when it was basic + additional and those contributions combined were worth more than one year of NIC now.

As flagged only £15ish per week so not the end of the world but could have funded council tax and energy costs ho hum.

I don't think you do understand.

The £15 COPE isn't lost, that's broadly how much more you're getting in your private pensions as a result of being contracted out.

Go and get your state pension forecast from the gov.uk website and post the results. The forecast is what you could reach given the time left to SPA and what you already have. Below it'll confirm how many more years NIC are needed (if any) to reach your forecast amount.

The £15 COPE isn't lost, that's broadly how much more you're getting in your private pensions as a result of being contracted out.

Go and get your state pension forecast from the gov.uk website and post the results. The forecast is what you could reach given the time left to SPA and what you already have. Below it'll confirm how many more years NIC are needed (if any) to reach your forecast amount.

PistonHead007 said:

I don't think you do understand.

The £15 COPE isn't lost, that's broadly how much more you're getting in your private pensions as a result of being contracted out.

Go and get your state pension forecast from the gov.uk website and post the results. The forecast is what you could reach given the time left to SPA and what you already have. Below it'll confirm how many more years NIC are needed (if any) to reach your forecast amount.

No I get thatThe £15 COPE isn't lost, that's broadly how much more you're getting in your private pensions as a result of being contracted out.

Go and get your state pension forecast from the gov.uk website and post the results. The forecast is what you could reach given the time left to SPA and what you already have. Below it'll confirm how many more years NIC are needed (if any) to reach your forecast amount.

What I mean is my final salary pension didn’t flag it contained £15pw from state pension and be ready for state pension to be £15pw lower.

I wasn’t aware of it / not informed so assumed full state pension plus final salary as stated plus defined contribution (which has a bit more guess work to it’s effective annual rate)

Welshbeef said:

No I get that

What I mean is my final salary pension didn’t flag it contained £15pw from state pension and be ready for state pension to be £15pw lower.

I wasn’t aware of it / not informed so assumed full state pension plus final salary as stated plus defined contribution (which has a bit more guess work to it’s effective annual rate)

What does it matter where your £15pw comes from, you've got the benefit of those NIC payments. To be honest, if it is GMP in a final salary pension it's likely to have fixed rate revaluation that can be as punchy as 8.5%pa so in practice a lot more than £15pw.What I mean is my final salary pension didn’t flag it contained £15pw from state pension and be ready for state pension to be £15pw lower.

I wasn’t aware of it / not informed so assumed full state pension plus final salary as stated plus defined contribution (which has a bit more guess work to it’s effective annual rate)

If you post what I said I bet you'll get the full flat rate pension anyway, despite being contracted out. Ergo, you're better off.

craig1912 said:

It isn’t as simple as that. I have 42 years full years but still need another two. Having retired I’m not going to get those through paying NI but it maybe worth me paying a lump sum to get them which would give me an extra £6 pw. My max is £170.60.

I underpaid because I didn't realise that under my pension scheme contributions I paid a lower slighly lower NI so have about 36yrs fully paid at present.I'm not inclined to pay a 'lump sum' to give me an extra few pounds a week as it becomes a trade off with how long you live after 67 to get back the lump sum you paid upfront. That's too much the long game and as I've said before in my mind planning to have plenty of money left when I'm late 70s/80s means a miscalculation and lost opportunities on my part.

mikeiow said:

Eh?

It told you you would get £179.60, and (the important bit lower down) that £179.60 is the most you can get.

What tenner?!

IIRC, you use an IFA, or have I got this wrong? Do you have money conversations with him to clarify this stuff….

Oops sorry I had a few other numbers rattling around in my head ! Sorry my bad It told you you would get £179.60, and (the important bit lower down) that £179.60 is the most you can get.

What tenner?!

IIRC, you use an IFA, or have I got this wrong? Do you have money conversations with him to clarify this stuff….

Let’s get the thread back on track……

Having quick call with WM tonight just to discuss a few things re ISA’s etc which look like have recovered now after the recent slump !

Edited by GT3Manthey on Thursday 31st March 07:05

anonymous said:

[redacted]

Good advice!

Well, our lengthy (by our standards!) ski trip is heading to an early close....heavier snow forecast overnight and tomorrow might wipe out our last day, but we have enjoyed some amazing weather for the first 10½ days, so all good - this thread's about "enjoying retirement", right?

Cheers all!

What many people seem to miss is that COPE is just a kind of comment. You don't subtract that from your state pension. You can still hit the max of 179 with enough years of qualifying NI regardless of what your COPE number is.

All it's really saying is that the government contributed something to your private pension for you, so you're winning both ways.

All it's really saying is that the government contributed something to your private pension for you, so you're winning both ways.

Michael_B said:

COPE (Contracted Out Pension Equivalent) is "here's what the Govt would have paid had you not contracted out." It precisely says on the HMRC website that this amount will be paid by other institutions (to whom you contracted out) and not by HMRC.

In my case I was contracted out while working the UK in the 1990s, and upon leaving the UK in 2000 a statement from the Royal Sun Alliance showed a transfer value of about £10k for the policy that received these sums. Turns out it was a with profits vehicle and did reasonably well. I recently cashed it out for £63k gross from its current owner Phoenix Life, just after my 55th birthday.

Although emergency tax meant I only received £45k of it, I'll get £13k back from HMRC after April as I had no other UK income in that tax year, and am still a UK citizen. And the Swiss taxman confirmed that he doesn't care one jot, as the money has already been treated for tax in a jurisdiction with whom Bern has a DTA. Furthermore, these amounts *may* then have been paid as additional contributions to my current occupational DC pension, with a further 35% credit against this year's Swiss taxable income.

Hurrah for contracting out

Absolutely. I was contracted out from 1987 to 2012, into an Aviva private pension. My COPE is, from memory, about £9/week, so about £468/year I'm "missing out" on. When I retired last year, my IFA amalgamated all my private pensions into a SIPP, and my Aviva contracted out pot was £120K. So ignoring the growth on that amount now it's in my SIPP, given that I was 58 when I retired, I'll need to live to 314 before contracting out becomes an expensive mistake. I look after myself and I am fit and in good health, but even so, I think that's unlikely. In my case I was contracted out while working the UK in the 1990s, and upon leaving the UK in 2000 a statement from the Royal Sun Alliance showed a transfer value of about £10k for the policy that received these sums. Turns out it was a with profits vehicle and did reasonably well. I recently cashed it out for £63k gross from its current owner Phoenix Life, just after my 55th birthday.

Although emergency tax meant I only received £45k of it, I'll get £13k back from HMRC after April as I had no other UK income in that tax year, and am still a UK citizen. And the Swiss taxman confirmed that he doesn't care one jot, as the money has already been treated for tax in a jurisdiction with whom Bern has a DTA. Furthermore, these amounts *may* then have been paid as additional contributions to my current occupational DC pension, with a further 35% credit against this year's Swiss taxable income.

Hurrah for contracting out

Edited by Michael_B on Wednesday 30th March 21:40

GT3Manthey said:

Oops sorry I had a few other numbers rattling around in my head ! Sorry my bad

Let’s get the thread back on track……

Having quick call with WM tonight just to discuss a few things re ISA’s etc which look like have recovered now after the recent slump !

Also been dipping into this one regularly and thoroughly enjoying it. So much food for thought. Just turned 59 with 43 years work under my belt and head’s all over the place about when to finish. Two teenage children, eldest shortly off to uni in London, so probably not any time soon unfortunately! Let’s get the thread back on track……

Having quick call with WM tonight just to discuss a few things re ISA’s etc which look like have recovered now after the recent slump !

Edited by GT3Manthey on Thursday 31st March 07:05

Got various DB and DC pensions with varying retirement ages. A retained DB one with NRA 62 is showing a less than 4% penalty if I take it now. Apart from being whipped for higher rate tax for as long as I’m still working, what’s not to like there? It’s not as if it has a fixed term, as long as I’m still chugging along, so is surely just free extra money. Or am I missing something patently obvious…

radovich said:

Also been dipping into this one regularly and thoroughly enjoying it. So much food for thought. Just turned 59 with 43 years work under my belt and head’s all over the place about when to finish. Two teenage children, eldest shortly off to uni in London, so probably not any time soon unfortunately!

Got various DB and DC pensions with varying retirement ages. A retained DB one with NRA 62 is showing a less than 4% penalty if I take it now. Apart from being whipped for higher rate tax for as long as I’m still working, what’s not to like there? It’s not as if it has a fixed term, as long as I’m still chugging along, so is surely just free extra money. Or am I missing something patently obvious…

My plan for uni fees is to pay the accommodation fees but use the student loan facility and come back to that once my youngest finishes . Got various DB and DC pensions with varying retirement ages. A retained DB one with NRA 62 is showing a less than 4% penalty if I take it now. Apart from being whipped for higher rate tax for as long as I’m still working, what’s not to like there? It’s not as if it has a fixed term, as long as I’m still chugging along, so is surely just free extra money. Or am I missing something patently obvious…

We might be in a position to pay it off for her or , like most students, she’ll have to take that on herself but I’m sure we can help .

If you can muster a way to make the numbers work for retiring I’d say go for it .

Also look at what you’ll likely need once you pass 70 as most will front load their pensions so spending should reduce .

Good luck in your decision making .

This thread is great for picking up on bits you havnt thought of

radovich said:

Also been dipping into this one regularly and thoroughly enjoying it. So much food for thought. Just turned 59 with 43 years work under my belt and head’s all over the place about when to finish. Two teenage children, eldest shortly off to uni in London, so probably not any time soon unfortunately!

Got various DB and DC pensions with varying retirement ages. A retained DB one with NRA 62 is showing a less than 4% penalty if I take it now. Apart from being whipped for higher rate tax for as long as I’m still working, what’s not to like there? It’s not as if it has a fixed term, as long as I’m still chugging along, so is surely just free extra money. Or am I missing something patently obvious…

Will you be a higher rate taxpayer when you finally jack things in?Got various DB and DC pensions with varying retirement ages. A retained DB one with NRA 62 is showing a less than 4% penalty if I take it now. Apart from being whipped for higher rate tax for as long as I’m still working, what’s not to like there? It’s not as if it has a fixed term, as long as I’m still chugging along, so is surely just free extra money. Or am I missing something patently obvious…

My goal would be to avoid paying unnecessary taxes....as well as enjoying as long a retirement as possible!

Younger children makes it trickier, I am sure - I stopped last year as our last was finishing his masters degree. Both now gainfully employed & needing less help, & more guidance ("fill your LISA up before 5th April" !!)

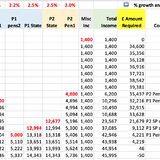

My 'planning' spreaddie is a more complex version of the sanitised version below, and is aiming to help figure out how the finances change over coming years. Aiming to be useful when you have various pots coming in at various points. Message me if you think it might help....but don't if you are scared of spreadsheets!

(of course, jacking in the day job is not as important as knowing how you will fill your time to enjoy your retirement....which is more the point of this thread, I feel!)

mikeiow said:

radovich said:

Also been dipping into this one regularly and thoroughly enjoying it. So much food for thought. Just turned 59 with 43 years work under my belt and head’s all over the place about when to finish. Two teenage children, eldest shortly off to uni in London, so probably not any time soon unfortunately!

Got various DB and DC pensions with varying retirement ages. A retained DB one with NRA 62 is showing a less than 4% penalty if I take it now. Apart from being whipped for higher rate tax for as long as I’m still working, what’s not to like there? It’s not as if it has a fixed term, as long as I’m still chugging along, so is surely just free extra money. Or am I missing something patently obvious…

Will you be a higher rate taxpayer when you finally jack things in?Got various DB and DC pensions with varying retirement ages. A retained DB one with NRA 62 is showing a less than 4% penalty if I take it now. Apart from being whipped for higher rate tax for as long as I’m still working, what’s not to like there? It’s not as if it has a fixed term, as long as I’m still chugging along, so is surely just free extra money. Or am I missing something patently obvious…

My goal would be to avoid paying unnecessary taxes....as well as enjoying as long a retirement as possible!

Younger children makes it trickier, I am sure - I stopped last year as our last was finishing his masters degree. Both now gainfully employed & needing less help, & more guidance ("fill your LISA up before 5th April" !!)

My 'planning' spreaddie is a more complex version of the sanitised version below, and is aiming to help figure out how the finances change over coming years. Aiming to be useful when you have various pots coming in at various points. Message me if you think it might help....but don't if you are scared of spreadsheets!

(of course, jacking in the day job is not as important as knowing how you will fill your time to enjoy your retirement....which is more the point of this thread, I feel!)

I retired almost a year ago, aged 54.

Expect to start drawing down my DC pension from next tax year, initially at the most tax efficient level simply to avoid losing my tax allowance.

nickfrog said:

GT3Manthey said:

We might be in a position to pay it off for her or , like most students, she’ll have to take that on herself but I’m sure we can help .

We paid it off because of the very high interest rate but we are charging her back at typical mortgage rate. Win win. Also, no one wants to think about it, but people sometimes die in their 20s or 30s. Paying off a student loan for a child who dies in an accident aged 25 is obviously a terrible idea in hindsight.

tertius said:

Ha, that's pretty well identical to my spreadsheet. Though I keep wrestling with the tax year vs age year vs calendar year as different things kick in at different dates.

My retirement projection spreadsheet version is based on my age year; this is made easier by my 1st July birthday being exactly half-way through the calendar year, plus Mrs B's birthday being very early January. In this way I just allocate 50% of her future new revenues in the initial year (Swiss/UK state or private pensions), as we will only receive it for the six months Jan-June, rather than the full year July-June. And the tax year in Switzerland is the Jan-Dec calendar, like it is in most civilised countries

As the CFO of a 40 person private limited company for the past 20 years, I should be capable of managing any combination of years/dates.

But I'm still glad we both chose the right dates/months to be born

TwigtheWonderkid said:

nickfrog said:

GT3Manthey said:

We might be in a position to pay it off for her or , like most students, she’ll have to take that on herself but I’m sure we can help .

We paid it off because of the very high interest rate but we are charging her back at typical mortgage rate. Win win. Also, no one wants to think about it, but people sometimes die in their 20s or 30s. Paying off a student loan for a child who dies in an accident aged 25 is obviously a terrible idea in hindsight.

The other risk is that she marries someone super wealthy and doesn't work ever again. She is not the type to lose her independence.

Gassing Station | Finance | Top of Page | What's New | My Stuff