Enjoying Retirement

Discussion

A couple needs £30,600 after tax for a moderate retirement and £49,700 after tax for a comfortable retirement according to this analysis:

https://www.retirementlivingstandards.org.uk/

Interestingly OP, your original post used the word ‘comfortable’ but it seems we all have different ideas about comfort. It is obviously subjective but the analysis makes some attempt at a definition.

https://www.retirementlivingstandards.org.uk/

Interestingly OP, your original post used the word ‘comfortable’ but it seems we all have different ideas about comfort. It is obviously subjective but the analysis makes some attempt at a definition.

Edited by anonymous-user on Friday 21st January 07:23

quote=Welshbeef]

When NLW jumps by the % it does and Employers NI up and their utility costs ramping up consumer has to pay.

[/quote]

I agree completely, but it creates a disconcerting situation if you’re trying to work out the size of pot you need and impact on drawdown rates.

To illustrate the effect of annual increases:

1% = 69.7 years to double

3% = 23.4

5% = 14.2

9% = 8.0 (included due to BT increase)

Obviously it’s the gap between savings performance and costs that’s important and the above assumes constant rates. But the really significant issue for people approaching/in retirement is that the current interest rate environment means you can’t go to cash without falling behind, yet there’s a greater risk exposure remaining in the markets, and even relatively benign sounding increases can have a big effect over the typical retirement period, even more so if you’re trying to retire early, where you could easily see drawdown needs significantly increasing in order to maintain the same standard of living.

There are going to be some difficult choices ahead for government/bank of England if the rates don’t begin to fall back to expected levels: https://www.bankofengland.co.uk/knowledgebank/will... especially since above average inflation increases to goods and services also serve to create further upward pressure on inflation numbers themselves and things such wages/benefits.

When NLW jumps by the % it does and Employers NI up and their utility costs ramping up consumer has to pay.

[/quote]

I agree completely, but it creates a disconcerting situation if you’re trying to work out the size of pot you need and impact on drawdown rates.

To illustrate the effect of annual increases:

1% = 69.7 years to double

3% = 23.4

5% = 14.2

9% = 8.0 (included due to BT increase)

Obviously it’s the gap between savings performance and costs that’s important and the above assumes constant rates. But the really significant issue for people approaching/in retirement is that the current interest rate environment means you can’t go to cash without falling behind, yet there’s a greater risk exposure remaining in the markets, and even relatively benign sounding increases can have a big effect over the typical retirement period, even more so if you’re trying to retire early, where you could easily see drawdown needs significantly increasing in order to maintain the same standard of living.

There are going to be some difficult choices ahead for government/bank of England if the rates don’t begin to fall back to expected levels: https://www.bankofengland.co.uk/knowledgebank/will... especially since above average inflation increases to goods and services also serve to create further upward pressure on inflation numbers themselves and things such wages/benefits.

We are both on FS pensions. These were both heavily invested into and are public sector. As such we receive a (what we consider to be) a hearty amount into the bank each month.

What I can’t work out (as we were public sector this was always done for us) is how much people are putting into a pension a month to expect £6-8k a month!?

Retiring early was fabulous tho and we are comfortable........

What I can’t work out (as we were public sector this was always done for us) is how much people are putting into a pension a month to expect £6-8k a month!?

Retiring early was fabulous tho and we are comfortable........

Rob_125 said:

Yeah, I'm putting £400/month aside into a Vanguard S&S ISA, and £150/month into a company shares scheme. Hopefully these may allow for early retirement if/when the criteria changes. But will have to keep an eye on the lifetime allowance, surely this will have to be increased over time?

You've done the hard work already! Even if you don't contribute a penny more, you should be getting close to lifetime allowance. Rockets7 said:

What I can’t work out (as we were public sector this was always done for us) is how much people are putting into a pension a month to expect £6-8k...

Nowadays you can only put 40k into your pension each year. People spending £8k per month in retirement are not funding it all from their pension pot.I'm mid 50s and a spreadsheet saddo, having been financially modelling our retirement for years - sensitivity analysis for rates of inflation and investment returns, the full shebang.

Oldest is in uni and youngest is 16 with my wife and I hoping to stop working in 6 years time. We'll have no mortgage or debts by then, and intend to run 2 modest cars. She has her gym membership and I fancy joining the local golf club. We live in Scotland.

We reckon £41k (post tax in today's money) will give us a decent lifestyle by our standards - and this amount includes car depreciation, house repairs & maintenance, every expense we can think of, and includes £15k/year on holidays/weekenders and social spend.

Council tax and utilities are a concern - currently £6k/year for us - and rising - so I can see the appeal of retiring to a warmer climate but can't see us moving away from the kids when they may be starting families of their own. Then again, they may have emigrated to god knows where by then.

Oldest is in uni and youngest is 16 with my wife and I hoping to stop working in 6 years time. We'll have no mortgage or debts by then, and intend to run 2 modest cars. She has her gym membership and I fancy joining the local golf club. We live in Scotland.

We reckon £41k (post tax in today's money) will give us a decent lifestyle by our standards - and this amount includes car depreciation, house repairs & maintenance, every expense we can think of, and includes £15k/year on holidays/weekenders and social spend.

Council tax and utilities are a concern - currently £6k/year for us - and rising - so I can see the appeal of retiring to a warmer climate but can't see us moving away from the kids when they may be starting families of their own. Then again, they may have emigrated to god knows where by then.

Bonkers PH responses on here, national average wage is 26k and it’s being suggested to enjoy retirement you need at least 2-3x that.

‘To comfortably run 4 cars, I’m budgeting 15k per annum for holidays etc, to pay leases on cars’

You shouldn’t need 50-75k net with the mortgage paid off, after income tax, without costs of working, with no dependents etc?

Planning to retire next year at 50, house and several cars paid, no debt, net income of 20-25k from a couple of holiday rental properties, try to keep pension untouched as long as possible.

Hang On said:

A couple needs £30,600 after tax for a moderate retirement and £49,700 after tax for a comfortable retirement according to this analysis:

https://www.retirementlivingstandards.org.uk/

Interestingly OP, your original post used the word ‘comfortable’ but it seems we all have different ideas about comfort. It is obviously subjective but the analysis makes some attempt at a definition.

Tks for this. https://www.retirementlivingstandards.org.uk/

Interestingly OP, your original post used the word ‘comfortable’ but it seems we all have different ideas about comfort. It is obviously subjective but the analysis makes some attempt at a definition.

Edited by Hang On on Friday 21st January 07:23

Yes agreed we’ve all become accustomed to a standard of living and have expenses with kids etc.

Chatting with the wife last night, defiantly packing work in next year and will be looking to sell up and move out whilst also selling our holiday flat.

Will soon have to start thinking about the CGT liabilities

bennno said:

Bonkers PH responses on here, national average wage is 26k and it’s being suggested to enjoy retirement you need at least 2-3x that.

‘To comfortably run 4 cars, I’m budgeting 15k per annum for holidays etc, to pay leases on cars’

You shouldn’t need 50-75k net with the mortgage paid off, after income tax, without costs of working, with no dependents etc?

Planning to retire next year at 50, house and several cars paid, no debt, net income of 20-25k from a couple of holiday rental properties, try to keep pension untouched as long as possible.

You have said what I was thinking. ‘To comfortably run 4 cars, I’m budgeting 15k per annum for holidays etc, to pay leases on cars’

You shouldn’t need 50-75k net with the mortgage paid off, after income tax, without costs of working, with no dependents etc?

Planning to retire next year at 50, house and several cars paid, no debt, net income of 20-25k from a couple of holiday rental properties, try to keep pension untouched as long as possible.

Having said that, I completed that "how much do you need to live" speadsheet that another poster linked to earlier. I think we live relatively frugally, or certainly living costs (our social lives are expensive but non-essential so could be culled significantly if our income fell). However, even taking into account modest household expenditure, subscriptions, gym memberships etc the sum required PCM was far higher than the estimated figure I had in the back of my head.

bennno said:

Bonkers PH responses on here, national average wage is 26k and it’s being suggested to enjoy retirement you need at least 2-3x that.

This is a forum of car enthusiasts, presumably many of whom earn more than the national median and have certain expectations around their standard of living.The question isn't 'what does the average person need?', it's 'what do you need?', and it's enlightening to compare notes with people with roughly comparable expectations.

Oh and most of the £££ discussions have focused on a retired couple, so the comparable figure above should be £52k gross.

bennno said:

Bonkers PH responses on here, national average wage is 26k and it’s being suggested to enjoy retirement you need at least 2-3x that.

‘To comfortably run 4 cars, I’m budgeting 15k per annum for holidays etc, to pay leases on cars’

You shouldn’t need 50-75k net with the mortgage paid off, after income tax, without costs of working, with no dependents etc?

Planning to retire next year at 50, house and several cars paid, no debt, net income of 20-25k from a couple of holiday rental properties, try to keep pension untouched as long as possible.

Is the last paragraph a quote from the thread or what you are going to do?‘To comfortably run 4 cars, I’m budgeting 15k per annum for holidays etc, to pay leases on cars’

You shouldn’t need 50-75k net with the mortgage paid off, after income tax, without costs of working, with no dependents etc?

Planning to retire next year at 50, house and several cars paid, no debt, net income of 20-25k from a couple of holiday rental properties, try to keep pension untouched as long as possible.

Rockets7 said:

What I can’t work out (as we were public sector this was always done for us) is how much people are putting into a pension a month to expect £6-8k a month!?

£1M pot gets you c.£40k draw down or c.£30k annuity.To get a £1M pot over say 35 years you are looking at "contributions" of c.£1k/mo assuming 4% returns.

I guess you could just about hit £6k a month as a couple if you went the draw down route and if you both had a £1M pot. Before tax.

So if you both paid £1k a month you might get there.

anonymous said:

[redacted]

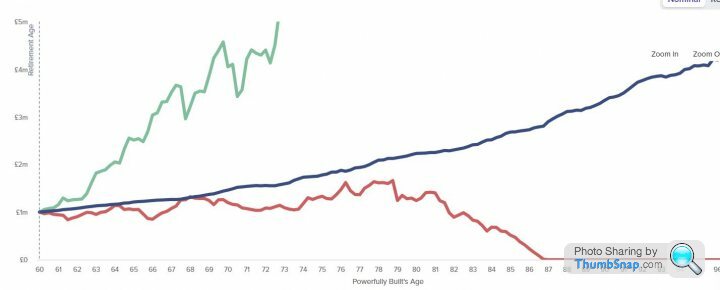

I think if you if you have an average run of luck with inflation/markets in retirement the pot is not that likely to shrink (in nominal terms). (The thinking being that if it is shrinking in "normal" markets, there may not be enough to sustain you if we have a blow-up).

Blue is "average", red is worst (and green is "time to buy 10 motorbikes

") for an example "Mr Powerfully Built".

") for an example "Mr Powerfully Built".

gotoPzero said:

£1M pot gets you c.£40k draw down or c.£30k annuity.

To get a £1M pot over say 35 years you are looking at "contributions" of c.£1k/mo assuming 4% returns.

I guess you could just about hit £6k a month as a couple if you went the draw down route and if you both had a £1M pot. Before tax.

So if you both paid £1k a month you might get there.

Id say that is very, cautious. My SIPP has averaged double that (roughly) and that performance also ties in with the long term market returns. To get a £1M pot over say 35 years you are looking at "contributions" of c.£1k/mo assuming 4% returns.

I guess you could just about hit £6k a month as a couple if you went the draw down route and if you both had a £1M pot. Before tax.

So if you both paid £1k a month you might get there.

Also, the 4% drawdown is arguably conservative too. You could drawdown more if the market is performing even averagely and still not be touching the pot. It may be better to plan to drawdown more in early retirement, and ease back as you get older?

Hang On said:

Rockets7 said:

What I can’t work out (as we were public sector this was always done for us) is how much people are putting into a pension a month to expect £6-8k...

Nowadays you can only put 40k into your pension each year. People spending £8k per month in retirement are not funding it all from their pension pot."For every £2 your adjusted income goes over £240,000, your annual allowance for the current tax year reduces by £1. The minimum reduced annual allowance you can have in the current tax year is £4,000"

https://www.gov.uk/guidance/pension-schemes-work-o...

(Edit: One for the First World Problems thread...)

Edited by Hereward on Friday 21st January 10:24

anonymous said:

[redacted]

Indeed. My father is 86 and a spritely 86 at that. However, aside from a healthy spend at Toolstation, he enjoys pottering in his man cave fiddling with woodwork and various DIY projects. Odd round of golf is probably his biggest other indulgence. As well as his pension he has also realised some capital in downsizing house, his Mercedes went for a Berlingo with buggy ramp, the motorhome was sold etc.I think many posters here are talking about retirement ages of 55 - 65 though, when in the modern world is still relatively young and healthy for the fortunate ones. Beyond 75 or so, I do think your spending falls away naturally. That said, with the inflation rampant and basics like energy and council tax rising rapidly, its still a concern to fix your income for the remainder of your life and quit working.

ray von said:

bennno said:

Bonkers PH responses on here, national average wage is 26k and it’s being suggested to enjoy retirement you need at least 2-3x that.

‘To comfortably run 4 cars, I’m budgeting 15k per annum for holidays etc, to pay leases on cars’

You shouldn’t need 50-75k net with the mortgage paid off, after income tax, without costs of working, with no dependents etc?

Planning to retire next year at 50, house and several cars paid, no debt, net income of 20-25k from a couple of holiday rental properties, try to keep pension untouched as long as possible.

Is the last paragraph a quote from the thread or what you are going to do?‘To comfortably run 4 cars, I’m budgeting 15k per annum for holidays etc, to pay leases on cars’

You shouldn’t need 50-75k net with the mortgage paid off, after income tax, without costs of working, with no dependents etc?

Planning to retire next year at 50, house and several cars paid, no debt, net income of 20-25k from a couple of holiday rental properties, try to keep pension untouched as long as possible.

Gassing Station | Finance | Top of Page | What's New | My Stuff