Enjoying Retirement

Discussion

Shnozz said:

Remember that PH isn't representative of society as a whole. There are many out there living off state pension alone and certainly over here in Spain, many pensioners living extremely well off that pension alone. Add in a private pension and you can live like a King (of a less wealthy nation).

Cheaper to live in Spain than in the UK do you think ?Shnozz said:

Oh without a doubt. However, I do see a few living in the UK off a state pension that do ok - albeit have to count every penny. The point I was making is that you can elect to live somewhere else, whether cheaper parts of the UK or elsewhere, where your money goes further.

The plan is to live further away & not be travelling to London. I’ve done the journey to the office for nigh on 40 years now and can’t tell you how sick of it I have become.

I suppose most ask themselves if they can afford to retire and sit crunching numbers for a good while. It’s the major factor in pulling the pin I guess.

We’ve asked ourselves what we want in retirement. We’re not bothered about travelling enormously , more interested in seeing more of the UK .

Time together & spent with family is very much the key for us and local leisure activities such as golf, gym and walking .

When I ask my friends if 5k a month is enough they almost get angry with me !

Only real ongoing kids payment will be with daughter at uni but I’ve thought about using the entire loan facility for this both fees and accommodation.

My want to retire is so great I’m sure we can make adjustments to make it work

plenty said:

I went self-employed a couple of years ago and never looked back. I work from wherever I want, plan my days so that my meetings are later in the day - I'm not an early bird and now I can pretty much get up whenever I want (I typically don't start working in earnest until 10 am).

No corporate or office politics, no manager or people to manage. I work with people I like on work I enjoy doing that I'm good at. I'm making pretty close to what I made in my corporate days.

I appreciate I'm pretty damn fortunate and not every line of work can offer the same opportunity.

I can’t work remotely in the business I’m in or work varying hours sadly but I’d love to change to something that enable this. No corporate or office politics, no manager or people to manage. I work with people I like on work I enjoy doing that I'm good at. I'm making pretty close to what I made in my corporate days.

I appreciate I'm pretty damn fortunate and not every line of work can offer the same opportunity.

May I ask what you do work wise ?

plenty said:

£5k/month is pretty close to our current outgoings, excluding provisions for children. We're mortgage-free, but council tax and energy alone in our current pad comes to £800/month. £4k per month would be more than adequate to sustain our standard of living once we move to a smaller place.

In terms of luxuries, the Mrs has a very busy social life involving lots of restaurant dates and we like to travel (4-5 short hauls and 1-2 long-hauls per year, but always via discount airlines and inexpensive accommodation). We have three cars (including two toys) but don't spend much on fuel as we don't need to commute by car, and my toys are fairly cheap to run. I'm quite frugal by nature but if I want something I buy it without needing to worry too much. We don't drink or go to pubs much.

Great post . In terms of luxuries, the Mrs has a very busy social life involving lots of restaurant dates and we like to travel (4-5 short hauls and 1-2 long-hauls per year, but always via discount airlines and inexpensive accommodation). We have three cars (including two toys) but don't spend much on fuel as we don't need to commute by car, and my toys are fairly cheap to run. I'm quite frugal by nature but if I want something I buy it without needing to worry too much. We don't drink or go to pubs much.

What monthly extra provisions so you allow for your children ?

My wife is quite a socialiser too!

We don’t often eat out but tend to drink to together indoors together .

I’ve spent many years out with clients and really hate that now

Edited by GT3Manthey on Thursday 20th January 12:20

Darlo74 said:

Interesting topic, I'm 8 years away from wanting the option to retire full-time... although I expect I'll not step away fully and find something to keep me occupied part-time and to provide additional income (even though I hope that's not needed). I'll be 55 in 8 years.

My plan is to have a minimum of £3k per month to cover essentials and anywhere between £1k - £2k per month on-top for holidays, cars, travel, unexpected expenses, kids, etc. This is to cover a joint income for me and my wife. Both kids will be out of full time education by then.

£3k will come from my SIPP and my wife's SIPP with on-tops from my ISAs, PBs and GIAs.

Once I reach 68 the state pension will be a nice on-top and provides a contingency if my savings have deteriorated more than expected!

My plan too and same numbers which is encouraging My plan is to have a minimum of £3k per month to cover essentials and anywhere between £1k - £2k per month on-top for holidays, cars, travel, unexpected expenses, kids, etc. This is to cover a joint income for me and my wife. Both kids will be out of full time education by then.

£3k will come from my SIPP and my wife's SIPP with on-tops from my ISAs, PBs and GIAs.

Once I reach 68 the state pension will be a nice on-top and provides a contingency if my savings have deteriorated more than expected!

Just been reminded of why I stated this thread.

Currently jammed into a train heading home from Liverpool St station on a reduced service .

Standing room only , 40% no masks, fat bloke opposite has nearly fallen over me 3 times & some 19yr old female chav wearing a green tracksuit insistent of talking into her mobile using an earpiece so we can all hear the conversation throwing out a load of F bombs.

Anyone got a gun ? !!!!!

Currently jammed into a train heading home from Liverpool St station on a reduced service .

Standing room only , 40% no masks, fat bloke opposite has nearly fallen over me 3 times & some 19yr old female chav wearing a green tracksuit insistent of talking into her mobile using an earpiece so we can all hear the conversation throwing out a load of F bombs.

Anyone got a gun ? !!!!!

Hang On said:

A couple needs £30,600 after tax for a moderate retirement and £49,700 after tax for a comfortable retirement according to this analysis:

https://www.retirementlivingstandards.org.uk/

Interestingly OP, your original post used the word ‘comfortable’ but it seems we all have different ideas about comfort. It is obviously subjective but the analysis makes some attempt at a definition.

Tks for this. https://www.retirementlivingstandards.org.uk/

Interestingly OP, your original post used the word ‘comfortable’ but it seems we all have different ideas about comfort. It is obviously subjective but the analysis makes some attempt at a definition.

Edited by Hang On on Friday 21st January 07:23

Yes agreed we’ve all become accustomed to a standard of living and have expenses with kids etc.

Chatting with the wife last night, defiantly packing work in next year and will be looking to sell up and move out whilst also selling our holiday flat.

Will soon have to start thinking about the CGT liabilities

Desiderata said:

This, my Mum is 85 and has an income of around £1200 per month. She still runs her car and manages to enjoy a couple of foreign holidays each year and give generously at Christmas and birthdays. She's probably only spending around £200 per month on day to day living.

My mother is 84 this year . She gets her final salary pension and her state pension.

In total she gets £2800 per month & hasn’t a clue what to do with it .

She won’t be spending, all in, half of that

eyebeebe said:

I've been reading this thread with interest and even typed out a post detailing our expected retirement spend, but deleted it, as it seemed a bit crass and braggy. I may change my mind and post it though

At 34 I probably had £70k in my pension pot and my OH similar. Both earning good money, no debts, but expensive rental and no real savings. We were pretty much living month to month. Also in Switzerland need a 20% deposit for a mortgage on already high house prices. At 36 our pay caught up with our lifestyle and at 38 we were able to buy a property, but that involved me liquidating my pension fund to put towards the deposit. I'd done some vague financial forecasting when we bought that we should be able to retire when I hit 55 and be comfortable. When COVID hit we realised how little we enjoy commuting and how it is a waste of a couple of hours a day. We also voiced concerns to each other that there are very few people in our offices over the age of 50. I did some more serious forecasting and we are now targeting retiring not long after my 50th birthday. It will be a very comfortable retirement.

and at 38 we were able to buy a property, but that involved me liquidating my pension fund to put towards the deposit. I'd done some vague financial forecasting when we bought that we should be able to retire when I hit 55 and be comfortable. When COVID hit we realised how little we enjoy commuting and how it is a waste of a couple of hours a day. We also voiced concerns to each other that there are very few people in our offices over the age of 50. I did some more serious forecasting and we are now targeting retiring not long after my 50th birthday. It will be a very comfortable retirement.

I've read in other posts of yours that you and your wife both earn well and I assume that at 34 you still have some decent earnings growth left in you. You've already got a house ticked off. So long as your lifestyle doesn't creep, you've got plenty of headroom to get your investments/pensions in order. Granted we have strong pension contributions from our employer (13% now rising to 19% at 45) and live in a very benign tax environment (total tax and social security deductions less than 20% of gross, no capital gains tax), but we will go from pretty much a standing start to a fantastic position in not much over 10 years. You've got 5 years on me, although having kid(s) probably offsets that advantage.

FWIW to achieve this we are looking at total investments and (employer and employee) pension contributions to gross income ratio and a investments to net income ratio of around 50%.

Well played sir . At 34 I probably had £70k in my pension pot and my OH similar. Both earning good money, no debts, but expensive rental and no real savings. We were pretty much living month to month. Also in Switzerland need a 20% deposit for a mortgage on already high house prices. At 36 our pay caught up with our lifestyle

and at 38 we were able to buy a property, but that involved me liquidating my pension fund to put towards the deposit. I'd done some vague financial forecasting when we bought that we should be able to retire when I hit 55 and be comfortable. When COVID hit we realised how little we enjoy commuting and how it is a waste of a couple of hours a day. We also voiced concerns to each other that there are very few people in our offices over the age of 50. I did some more serious forecasting and we are now targeting retiring not long after my 50th birthday. It will be a very comfortable retirement.I've read in other posts of yours that you and your wife both earn well and I assume that at 34 you still have some decent earnings growth left in you. You've already got a house ticked off. So long as your lifestyle doesn't creep, you've got plenty of headroom to get your investments/pensions in order. Granted we have strong pension contributions from our employer (13% now rising to 19% at 45) and live in a very benign tax environment (total tax and social security deductions less than 20% of gross, no capital gains tax), but we will go from pretty much a standing start to a fantastic position in not much over 10 years. You've got 5 years on me, although having kid(s) probably offsets that advantage.

FWIW to achieve this we are looking at total investments and (employer and employee) pension contributions to gross income ratio and a investments to net income ratio of around 50%.

Any kids to pay for too ?

MrVert said:

It's quite scary to realise how much you need to carry on your lifestyle when you stop working.

I started buying property about 10 years ago to supplement my pension schemes, which in my opinion would not give me what I needed to live the life I wanted The thought was to give me an additional investment stream with the capital being mostly safe and also something I could pass on to the next generation when I pop off, something which for some reason seems to be important to me.

In 2016 I and a couple of friends did a 'Bust Rallies' trip through Europe and the conversation turned to how much you'd need in retirement if we stopped now. All in our mid to late 40's at the time, all had one or two kids in their mid teens etc etc. I was in the position of owning my own business with no mortgage, the others had decent Director level jobs but with mortgages.

The initial thought was you'd need £2.5 - £3k per month once the mortgage and kids had departed off to Uni..

However once I started to work it all out, I realised if you wanted to live well, without significant change to your cushy lifestyle this would be nowhere near enough...

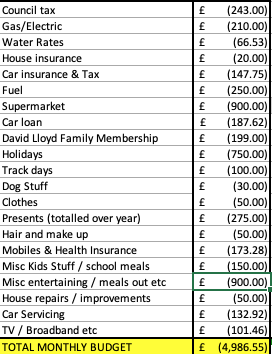

This is where I arrived at for monthly expenditure, obviously constantly under review...

Whichever way I worked it, without cutting out significant sums for travel / lifestyle stuff, it was basically £5k per month for a good life.

So we purchased quite a few more properties to supplement our future income, which in late 2017 enabled me to offload the company and stop full time work. Just over 4 years on, the expenditure has panned out almost to the penny compared to the forecast and I'm happy with my projections.

It's so important to realise what income level you will need when you retire and to be completely honest with your projections. I could not contemplate stopping work until I was 100% happy with my decision.

Obviously from the figures there's quite a bit there for the niceties in life, going out / holidays / gym / track days etc etc, but in my early fifties I'm certainly not ready to give these up yet.

Like anything in life, as long as you have a factor of safety there with the figures, you can ride out any blips that come up from time to time and adjust where you spend your money.

Pension is available from the middle of next year, so this will hopefully be used for more travel and more track based fun, joining golf club etc.

For me, it's worked out but only as I had funds available to purchase the properties. If I relied on my pensions, even with increased contributions, I didn't put enough in early on for it to ever be realistic to retire on it.

Looking at returns today and what a lot of people will have in their pension fund when they stop work in another 10-15 years, I really do fear for how they will manage. A lot of people are going to have to seriously reduce their expenditure even after working for longer than they would have liked.

Many tks for sharing this, its exactly the reason i started the thread to get an accurate and working example. Top man I started buying property about 10 years ago to supplement my pension schemes, which in my opinion would not give me what I needed to live the life I wanted The thought was to give me an additional investment stream with the capital being mostly safe and also something I could pass on to the next generation when I pop off, something which for some reason seems to be important to me.

In 2016 I and a couple of friends did a 'Bust Rallies' trip through Europe and the conversation turned to how much you'd need in retirement if we stopped now. All in our mid to late 40's at the time, all had one or two kids in their mid teens etc etc. I was in the position of owning my own business with no mortgage, the others had decent Director level jobs but with mortgages.

The initial thought was you'd need £2.5 - £3k per month once the mortgage and kids had departed off to Uni..

However once I started to work it all out, I realised if you wanted to live well, without significant change to your cushy lifestyle this would be nowhere near enough...

This is where I arrived at for monthly expenditure, obviously constantly under review...

Whichever way I worked it, without cutting out significant sums for travel / lifestyle stuff, it was basically £5k per month for a good life.

So we purchased quite a few more properties to supplement our future income, which in late 2017 enabled me to offload the company and stop full time work. Just over 4 years on, the expenditure has panned out almost to the penny compared to the forecast and I'm happy with my projections.

It's so important to realise what income level you will need when you retire and to be completely honest with your projections. I could not contemplate stopping work until I was 100% happy with my decision.

Obviously from the figures there's quite a bit there for the niceties in life, going out / holidays / gym / track days etc etc, but in my early fifties I'm certainly not ready to give these up yet.

Like anything in life, as long as you have a factor of safety there with the figures, you can ride out any blips that come up from time to time and adjust where you spend your money.

Pension is available from the middle of next year, so this will hopefully be used for more travel and more track based fun, joining golf club etc.

For me, it's worked out but only as I had funds available to purchase the properties. If I relied on my pensions, even with increased contributions, I didn't put enough in early on for it to ever be realistic to retire on it.

Looking at returns today and what a lot of people will have in their pension fund when they stop work in another 10-15 years, I really do fear for how they will manage. A lot of people are going to have to seriously reduce their expenditure even after working for longer than they would have liked.

Edited by MrVert on Sunday 23 January 10:04

TwigtheWonderkid said:

Not a rude question at all, but I'm not going to answer. I'm British, so discussing specific amounts makes me uncomfortable. But nothing like the millions many on here seem to think is the minimum requirement.

More than fair . May I just ask what your monthly spend is ?

I found the above post with a monthly breakdown very useful

TwigtheWonderkid said:

My standing orders are about £900, but that includes some stuff I want rather than need, like Sky Sports package. I could get it down to around £700 if I wanted. That would include council tax, gas and electric, home insurance, gym membership. Car insurance I pay in full. Our total spend is probably around £3000 or just under, all in. But I could knock a grand off that if I decided to be really frugal. We eat out about 6 - 8 times a month, and have a night away somewhere nice also about once a month.

Useful and a realistic number i feel.....Tks for sharing My plan has never been to take the 25% tax free lump sum , rather use it as part of my monthly draw .

One question though - if I don’t take the lump sum can I continue to draw down on a monthly basis tax free up to the amount that would have been tax free at the point of accessing my pot ?

Probably a very stupid question and as I’m typing this I’m thinking there must be a very straight forward answer but I’ve done it now !

One question though - if I don’t take the lump sum can I continue to draw down on a monthly basis tax free up to the amount that would have been tax free at the point of accessing my pot ?

Probably a very stupid question and as I’m typing this I’m thinking there must be a very straight forward answer but I’ve done it now !

Carbon Sasquatch said:

Assuming you're talking DC pot - You effectively crystallise an amount - and 25% is tax free. At the point of crystallisation, the % of LTA used is calculated & kept as a running total.

So you can crystallise it all up front, or in much smaller chunks.

Theoretically you can take more than the initial tax free amount - assuming the pot keeps growing - but eventually you may go over LTA.

No my pension pot is self funded. So you can crystallise it all up front, or in much smaller chunks.

Theoretically you can take more than the initial tax free amount - assuming the pot keeps growing - but eventually you may go over LTA.

The plan is to combine pension, ISA’s & cash to make up the monthly draw

mikeiow said:

?

If a pension pot is 'self funded', then it is a DC pot. Who is it invested with?

The other sources you talk off - ISAs & cash - are entirely separate pots.

How you draw down is up to you.

You can take some from your pension pot, and whatever you like from your ISAs and cash. Those two things are not linked, other than they form your income stream!

As Carbon said, you can chose to take tax free lump sums from the DC pot - the rest would be 'crystallised' and marked as a 'drawdown pot' by the Administrator (mine is Aviva). If you later draw from that drawdown pot, it is all part of your taxable income.

Also as Carbon said, you could instead take smaller amounts, 25% of which is tax free, leaving the rest of your pot 'uncrystallised'.

Maybe you would benefit from a chat with PensionWise to explain things?

Sorry misread the post whilst typing from a mobile phone , trying to work and take a call ! Too old to multi task . If a pension pot is 'self funded', then it is a DC pot. Who is it invested with?

The other sources you talk off - ISAs & cash - are entirely separate pots.

How you draw down is up to you.

You can take some from your pension pot, and whatever you like from your ISAs and cash. Those two things are not linked, other than they form your income stream!

As Carbon said, you can chose to take tax free lump sums from the DC pot - the rest would be 'crystallised' and marked as a 'drawdown pot' by the Administrator (mine is Aviva). If you later draw from that drawdown pot, it is all part of your taxable income.

Also as Carbon said, you could instead take smaller amounts, 25% of which is tax free, leaving the rest of your pot 'uncrystallised'.

Maybe you would benefit from a chat with PensionWise to explain things?

I have a wealth manager just hadn’t thought to ask about the differences of taking lump sum tax free or taking the tax free lump sum as a drawdown .

Sorry if not clear

gotoPzero said:

I think this is the bit a lot of people worry about - IMHO without much need.

Yes sure everyone has an uncle bob who is still running marathons at 95 but honestly the reality is for most people once you hit 80 you are going to slow down by a significant margin.

Having observed my grandparents get old and now my parents in their late 70s I would actually say people start to slow down at 70. Then by 75 they are going away less, going out less and generally their spending is significantly less.

Thats one of thing things that has driven me to want to retire as early as possible. I think you have that window till maybe 65 where you can be fairly confident you are going to be active but after that I think every day is a blessing!

Yes sure everyone has an uncle bob who is still running marathons at 95 but honestly the reality is for most people once you hit 80 you are going to slow down by a significant margin.

Having observed my grandparents get old and now my parents in their late 70s I would actually say people start to slow down at 70. Then by 75 they are going away less, going out less and generally their spending is significantly less.

Thats one of thing things that has driven me to want to retire as early as possible. I think you have that window till maybe 65 where you can be fairly confident you are going to be active but after that I think every day is a blessing!

This ^^^^^^

My family history of heart attacks makes for some stark reading plus my mother who has now made 83 can’t spend anymore than £1200 a month yet her pensions give her £2800

timberman said:

similar story with my parents,

retired at 65, and apart from some savings only had a state pension to live on with my mum only getting a basic pension due to her having worked part time,

now in their 80's with my dad fast approaching 90, they've gone from running the savings down to now seeing the bank balance grow again due to no longer spending any money other than the basics.

I think the bit we forget ( and I’m very much guilty of this) is that at 80, if I make it that far , I’ll not be playing golf, the wife won’t be going to the gym , wont be going out to dinner twice a week , takeaways we won’t want , holidays we be a faff so spending will be right down . retired at 65, and apart from some savings only had a state pension to live on with my mum only getting a basic pension due to her having worked part time,

now in their 80's with my dad fast approaching 90, they've gone from running the savings down to now seeing the bank balance grow again due to no longer spending any money other than the basics.

Also at some stage we’ll be selling the family home & downsizing to a flat .

ARHarh said:

My plan is to use up most if not all of the pot by the time I am 80, then live off state pension and the small DB pensions we have. As far as I can see most people give up the expensive around 80 years old. Most give up driving, most stop holidays and buying new stuff rarely happens. The only issue will be care, if needed to house can cover that.

I’m totally onboard with this idea too Gassing Station | Finance | Top of Page | What's New | My Stuff