Retirement calculator

Discussion

beanoir78 said:

The big unknown for me with any of these calculators, or even not using them is how much I would like or need as a pension.

The reality is not nearly as much as you think.You wont be commuting. Surprising what this saves, don't have to insure a car for commuting, less wear and tear, buy a lot less fuel. Or no season ticket.

you most likely wont be buying coffees and lunch everyday. For some this could be as much as the state pension.

Chances are your house will be paid for, could save thousands.

Saga do some good deals on insurance.

These are just a few things that you won't be spending so much on.

Best bet is to create a spread sheet with all your expenses listed, then get it to add up the expenses you will still need and the ones you won't need and you should after a few years get a decent answer.

ARHarh said:

Best bet is to create a spread sheet with all your expenses listed, then get it to add up the expenses you will still need and the ones you won't need and you should after a few years get a decent answer.

Agreed, understanding what you are spending now is key - many people spend far more than they realise and the supposed gap/surplus between income and expenditure doesn't exist. Once you have realistic current expenditure you can then estimate future expenditure on a row-by-row basis

b hstewie said:

hstewie said:

hstewie said: This seems decent too https://www.timelineapp.co

It's a useful tool (my screenshots from yesterday are from Timeline), but unless and until you have been through the pain of the expenditure exercise and built the financial plan (e.g. Voyant) I don't think you'd get the most value from it.Derek Chevalier said:

It's a useful tool (my screenshots from yesterday are from Timeline), but unless and until you have been through the pain of the expenditure exercise and built the financial plan (e.g. Voyant) I don't think you'd get the most value from it.

I signed up for free (it doesn't seem to care whether you're an IFA) and it seems to work.Took a bit of working out quite what they class as cash savings and the returns they use on investments don't seem visible (or I haven't spotted them yet) and there doesn't seem an obvious way to split pension contributions between my own and my employers but can't complain for free

Fully take the point about planning but sometimes there isn't a plan beyond knowing (roughly) what you hope to keep contributing and (roughly) what you think your spending might look and (roughly) when you might think f

k it I've had enough of work.bhstewie said:

hstewie said: and the returns they use on investments don't seem visible

I might have a slightly different version, but if you go to plan settings->portfolio->edit portfolio you can see the source data

bhstewie said:

hstewie said: and there doesn't seem an obvious way to split pension contributions between my own and my employers but can't complain for free

Timeline may disagree but this is where a tool such as Voyant comes into its own (I recall you can get Voyant cheaply via the Pete Matthews course).Derek Chevalier said:

Timeline may disagree but this is where a tool such as Voyant comes into its own (I recall you can get Voyant cheaply via the Pete Matthews course).

What sort of stuff does Voyant do then?I might work off basic "I spend £xx per year" just off the back of a napkin but when you say "built the financial plan" what sort of additional details do you typically think about?

For example I wouldn't have a clue if I intended to spend a £30K lump sum on a new car in 15 years time or anything that detailed.

bhstewie said:

hstewie said:Derek Chevalier said:

Timeline may disagree but this is where a tool such as Voyant comes into its own (I recall you can get Voyant cheaply via the Pete Matthews course).

What sort of stuff does Voyant do then?I might work off basic "I spend £xx per year" just off the back of a napkin but when you say "built the financial plan" what sort of additional details do you typically think about?

For example I wouldn't have a clue if I intended to spend a £30K lump sum on a new car in 15 years time or anything that detailed.

Pete also has a lot of publicly available videos including an overview of Voyant, so might be easier just to watch that - https://www.youtube.com/watch?v=fembQpmbFFo

Welshbeef said:

Is anyone instructing their pension funds to move to cash - given equities dropping -especially in the USA and the worrying tip of the iceberg falls

Given you've missed calling the top by 6 months, how do you rate your chances of calling the bottom ?There's plenty on other threads about timing the market. As uncomfortable as it feels right now, I expect that most people are in for the long term.

bhstewie said:

hstewie said: Fully take the point about planning but sometimes there isn't a plan beyond knowing (roughly) what you hope to keep contributing and (roughly) what you think your spending might look and (roughly) when you might think fk it I've had enough of work.

k it I've had enough of work.bhstewie said:

hstewie said:Derek Chevalier said:

Timeline may disagree but this is where a tool such as Voyant comes into its own (I recall you can get Voyant cheaply via the Pete Matthews course).

What sort of stuff does Voyant do then?I might work off basic "I spend £xx per year" just off the back of a napkin but when you say "built the financial plan" what sort of additional details do you typically think about?

For example I wouldn't have a clue if I intended to spend a £30K lump sum on a new car in 15 years time or anything that detailed.

Someone in their 30s with relatively simple needs probably isn't going to need the complexity of Voyant - a basic plan (in a spreadsheet) might be all that is needed.

However, someone in their mid-50s in the run-up to retirement with more complex needs is when a tool such as Voyant (other tools are available (e.g. https://cashcalc.co.uk/ but Voyant is still the daddy IMO) makes a lot more sense, and is far more cost-effective (and less error-prone) from an adviser point of view than attempting this in a spreadsheet (happy to discuss spreadsheets

).Voyant helps answer things like

1. Can I afford to retire? Voyant can answer this at a reasonable level and Timeline is used to stress test on a case-by-case basis. The expenditure data is imported from a spreadsheet to build the first draft of the financial plan.

2. What is the impact of/what-if scenarios

Finishing work now, a year early/later/working part-time

Gifting to children now.

Spending more in early retirement

One half of the couple gets run over

This is all doable in a spreadsheet but you can do this in near-real-time in Voyant live with the client (and the what-if scenarios get updated automatically when the master plan does).

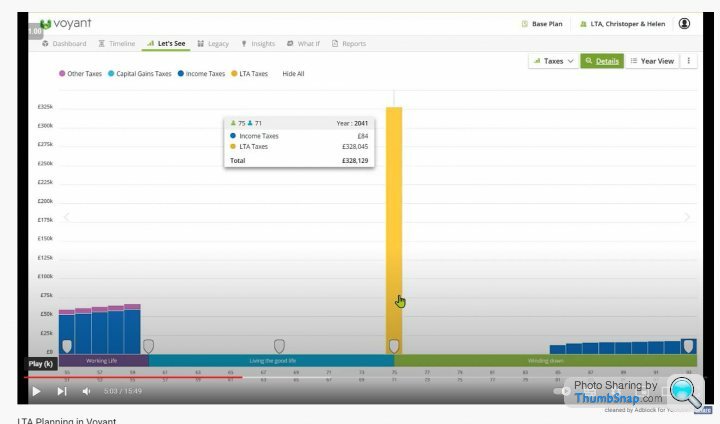

3. Optimising a withdrawal strategy and optimising lifetime taxation (LTA, IHT, income tax etc).

This is where Voyant is excellent, and I think where it would be much more tricky/time-consuming to attempt in a spreadsheet

An example below of LTA modelling

https://www.youtube.com/watch?v=Si0aDjCHpMU

Derek Chevalier said:

I think it really depends where you are on your journey and how complex your financial situation is.

Someone in their 30s with relatively simple needs probably isn't going to need the complexity of Voyant - a basic plan (in a spreadsheet) might be all that is needed.

However, someone in their mid-50s in the run-up to retirement with more complex needs is when a tool such as Voyant (other tools are available (e.g. https://cashcalc.co.uk/ but Voyant is still the daddy IMO) makes a lot more sense, and is far more cost-effective (and less error-prone) from an adviser point of view than attempting this in a spreadsheet (happy to discuss spreadsheets).

Voyant helps answer things like

1. Can I afford to retire? Voyant can answer this at a reasonable level and Timeline is used to stress test on a case-by-case basis. The expenditure data is imported from a spreadsheet to build the first draft of the financial plan.

2. What is the impact of/what-if scenarios

Finishing work now, a year early/later/working part-time

Gifting to children now.

Spending more in early retirement

One half of the couple gets run over

This is all doable in a spreadsheet but you can do this in near-real-time in Voyant live with the client (and the what-if scenarios get updated automatically when the master plan does).

3. Optimising a withdrawal strategy and optimising lifetime taxation (LTA, IHT, income tax etc).

This is where Voyant is excellent, and I think where it would be much more tricky/time-consuming to attempt in a spreadsheet

An example below of LTA modelling

https://www.youtube.com/watch?v=Si0aDjCHpMU

Thanks DerekSomeone in their 30s with relatively simple needs probably isn't going to need the complexity of Voyant - a basic plan (in a spreadsheet) might be all that is needed.

However, someone in their mid-50s in the run-up to retirement with more complex needs is when a tool such as Voyant (other tools are available (e.g. https://cashcalc.co.uk/ but Voyant is still the daddy IMO) makes a lot more sense, and is far more cost-effective (and less error-prone) from an adviser point of view than attempting this in a spreadsheet (happy to discuss spreadsheets

).Voyant helps answer things like

1. Can I afford to retire? Voyant can answer this at a reasonable level and Timeline is used to stress test on a case-by-case basis. The expenditure data is imported from a spreadsheet to build the first draft of the financial plan.

2. What is the impact of/what-if scenarios

Finishing work now, a year early/later/working part-time

Gifting to children now.

Spending more in early retirement

One half of the couple gets run over

This is all doable in a spreadsheet but you can do this in near-real-time in Voyant live with the client (and the what-if scenarios get updated automatically when the master plan does).

3. Optimising a withdrawal strategy and optimising lifetime taxation (LTA, IHT, income tax etc).

This is where Voyant is excellent, and I think where it would be much more tricky/time-consuming to attempt in a spreadsheet

An example below of LTA modelling

https://www.youtube.com/watch?v=Si0aDjCHpMU

That's really useful information. I have just started using Timeline as a private investor.

If you do not mind I have a question, can Voyant allow for two SIPP's, one crystallised to my personal protection allowance and the other uncrystallised for tax planning?

Thanks in advance

Monty

This is one of the bits I haven't quite figured out with Timeline.

Does anyone know what "category" does a company DC pension that's still being paid into as I'm working come under in the "Investment Accounts" section of plan settings?

Uncrystallised Funds?

Flexi-Access Drawdown?

I was expecting to see a category literally called SIPP or DC Pension or something that is smart enough to know when access can start etc.

Does anyone know what "category" does a company DC pension that's still being paid into as I'm working come under in the "Investment Accounts" section of plan settings?

Uncrystallised Funds?

Flexi-Access Drawdown?

I was expecting to see a category literally called SIPP or DC Pension or something that is smart enough to know when access can start etc.

Claret m said:

Derek Chevalier said:

I think it really depends where you are on your journey and how complex your financial situation is.

Someone in their 30s with relatively simple needs probably isn't going to need the complexity of Voyant - a basic plan (in a spreadsheet) might be all that is needed.

However, someone in their mid-50s in the run-up to retirement with more complex needs is when a tool such as Voyant (other tools are available (e.g. https://cashcalc.co.uk/ but Voyant is still the daddy IMO) makes a lot more sense, and is far more cost-effective (and less error-prone) from an adviser point of view than attempting this in a spreadsheet (happy to discuss spreadsheets).

Voyant helps answer things like

1. Can I afford to retire? Voyant can answer this at a reasonable level and Timeline is used to stress test on a case-by-case basis. The expenditure data is imported from a spreadsheet to build the first draft of the financial plan.

2. What is the impact of/what-if scenarios

Finishing work now, a year early/later/working part-time

Gifting to children now.

Spending more in early retirement

One half of the couple gets run over

This is all doable in a spreadsheet but you can do this in near-real-time in Voyant live with the client (and the what-if scenarios get updated automatically when the master plan does).

3. Optimising a withdrawal strategy and optimising lifetime taxation (LTA, IHT, income tax etc).

This is where Voyant is excellent, and I think where it would be much more tricky/time-consuming to attempt in a spreadsheet

An example below of LTA modelling

https://www.youtube.com/watch?v=Si0aDjCHpMU

Thanks DerekSomeone in their 30s with relatively simple needs probably isn't going to need the complexity of Voyant - a basic plan (in a spreadsheet) might be all that is needed.

However, someone in their mid-50s in the run-up to retirement with more complex needs is when a tool such as Voyant (other tools are available (e.g. https://cashcalc.co.uk/ but Voyant is still the daddy IMO) makes a lot more sense, and is far more cost-effective (and less error-prone) from an adviser point of view than attempting this in a spreadsheet (happy to discuss spreadsheets

).Voyant helps answer things like

1. Can I afford to retire? Voyant can answer this at a reasonable level and Timeline is used to stress test on a case-by-case basis. The expenditure data is imported from a spreadsheet to build the first draft of the financial plan.

2. What is the impact of/what-if scenarios

Finishing work now, a year early/later/working part-time

Gifting to children now.

Spending more in early retirement

One half of the couple gets run over

This is all doable in a spreadsheet but you can do this in near-real-time in Voyant live with the client (and the what-if scenarios get updated automatically when the master plan does).

3. Optimising a withdrawal strategy and optimising lifetime taxation (LTA, IHT, income tax etc).

This is where Voyant is excellent, and I think where it would be much more tricky/time-consuming to attempt in a spreadsheet

An example below of LTA modelling

https://www.youtube.com/watch?v=Si0aDjCHpMU

That's really useful information. I have just started using Timeline as a private investor.

If you do not mind I have a question, can Voyant allow for two SIPP's, one crystallised to my personal protection allowance and the other uncrystallised for tax planning?

Thanks in advance

Monty

By this I assume the 12,570 personal allowance

Yes, for each pension you can set the withdrawal limit (scheduled only) and then use the planned withdrawals functionality

https://support.planwithvoyant.com/hc/en-us/articl...

Note that's with Voyant Adviser (soon to de decommissioned), Go might be slightly different

https://www.ftadviser.com/your-industry/2022/05/25...

bhstewie said:

hstewie said: This is one of the bits I haven't quite figured out with Timeline.

Does anyone know what "category" does a company DC pension that's still being paid into as I'm working come under in the "Investment Accounts" section of plan settings?

Uncrystallised Funds?

Flexi-Access Drawdown?

I was expecting to see a category literally called SIPP or DC Pension or something that is smart enough to know when access can start etc.

Do you have access to the help functionality? "Case Study 2 – "John the Aircraft Pilot" might be worth a look.Does anyone know what "category" does a company DC pension that's still being paid into as I'm working come under in the "Investment Accounts" section of plan settings?

Uncrystallised Funds?

Flexi-Access Drawdown?

I was expecting to see a category literally called SIPP or DC Pension or something that is smart enough to know when access can start etc.

(I do my tax planning in Voyant so effectively "disable" the tax logic in Timeline).

Claret m said:

Hi Derek

Thanks for the reply. Sorry should have put individual protection 14 (£1,500,000).

ATB

Yes, you can set protectionThanks for the reply. Sorry should have put individual protection 14 (£1,500,000).

ATB

https://support.planwithvoyant.com/hc/en-us/articl...

and crystallise as required.

But, if you intend to start getting into this, it might be worth investing a month in Andy Hart's training course.

https://www.voyantmastery.com/

Derek Chevalier said:

Do you have access to the help functionality? "Case Study 2 – "John the Aircraft Pilot" might be worth a look.

(I do my tax planning in Voyant so effectively "disable" the tax logic in Timeline).

Boy do I hate John (I do my tax planning in Voyant so effectively "disable" the tax logic in Timeline).

Yes that helps thank you and it seems it's "Uncrystallised" that I want.

Guess I expected it to be a little more explicitly defined that "This is a DC pension and I can access it at age X" or "This is a SIPP and I can access it at age Y" and so on.

Beggars can't be choosers though and either way the core theme is I'm fine.

For anyone playing around with Timeline be careful with how it appears to handle pensions.

I'm seeing some weird stuff in the "Cashflow" section where it seems to be showing me withdrawing money from my pension whilst I'm still in my 40's which is clearly not possible.

It doesn't seem to matter whether I set that pot to Uncrystallised or Flex-Access Drawdown.

Maybe I'm missing something.

I'm seeing some weird stuff in the "Cashflow" section where it seems to be showing me withdrawing money from my pension whilst I'm still in my 40's which is clearly not possible.

It doesn't seem to matter whether I set that pot to Uncrystallised or Flex-Access Drawdown.

Maybe I'm missing something.

Gassing Station | Finance | Top of Page | What's New | My Stuff