Re-mortgage now or wait?

Discussion

mrpbailey said:

My BTL fixed rate is coming to an end at the end of June.

LTV ~ 51%. Currently with NatWest, interest only 2.88%.

For renewal they are offering:

-2 year fix @ 5.51% 0 fee (5.05% with 995 fee but annual cost works out higher)

-5 year fix @ 4.99% 0 fee (4.79 with fee but again works out higher annual cost)

So basically my monthly payments will be not far off doubling (which obviously has a big effect on the profit margin).

Best 2 year fix I am coming across elsewhere is HSBC at 5.19 with no fee. Roughly £19/month cheaper than NatWest.

Best 5 year fix I can find is again with HSBC AT 4.74%, 0 fee.

Am I likely to find anything better via a broker?

I’m hesitant to fix for 5 years as I may opt to sell up before then, but not sure 2 years is enough to see a significant reduction in interest rates.

I’m in a similar position, my current BTL rate ends next April so have been looking ahead at what rates are so I’m ready to press go when the time is right.LTV ~ 51%. Currently with NatWest, interest only 2.88%.

For renewal they are offering:

-2 year fix @ 5.51% 0 fee (5.05% with 995 fee but annual cost works out higher)

-5 year fix @ 4.99% 0 fee (4.79 with fee but again works out higher annual cost)

So basically my monthly payments will be not far off doubling (which obviously has a big effect on the profit margin).

Best 2 year fix I am coming across elsewhere is HSBC at 5.19 with no fee. Roughly £19/month cheaper than NatWest.

Best 5 year fix I can find is again with HSBC AT 4.74%, 0 fee.

Am I likely to find anything better via a broker?

I’m hesitant to fix for 5 years as I may opt to sell up before then, but not sure 2 years is enough to see a significant reduction in interest rates.

I think you, I, and many other BTL landlords are contemplating selling up or doing so already.

With HSBC their tracker rates don’t have any early redemption charges, so I’d be tempted to go for their 2 year tracker with no fee currently at 5.34% (for under 60% LTV). I know we’re potentially due another rate rise or two but the increases seem to be slowing, maybe we’re somewhere near the top? Who knows…

mrpbailey said:

My BTL fixed rate is coming to an end at the end of June.

LTV ~ 51%. Currently with NatWest, interest only 2.88%.

For renewal they are offering:

-2 year fix @ 5.51% 0 fee (5.05% with 995 fee but annual cost works out higher)

-5 year fix @ 4.99% 0 fee (4.79 with fee but again works out higher annual cost)

So basically my monthly payments will be not far off doubling (which obviously has a big effect on the profit margin).

Best 2 year fix I am coming across elsewhere is HSBC at 5.19 with no fee. Roughly £19/month cheaper than NatWest.

Best 5 year fix I can find is again with HSBC AT 4.74%, 0 fee.

Am I likely to find anything better via a broker?

I’m hesitant to fix for 5 years as I may opt to sell up before then, but not sure 2 years is enough to see a significant reduction in interest rates.

Take a look @ platform : https://www.platform.co.uk/mortgages/existing-mort...LTV ~ 51%. Currently with NatWest, interest only 2.88%.

For renewal they are offering:

-2 year fix @ 5.51% 0 fee (5.05% with 995 fee but annual cost works out higher)

-5 year fix @ 4.99% 0 fee (4.79 with fee but again works out higher annual cost)

So basically my monthly payments will be not far off doubling (which obviously has a big effect on the profit margin).

Best 2 year fix I am coming across elsewhere is HSBC at 5.19 with no fee. Roughly £19/month cheaper than NatWest.

Best 5 year fix I can find is again with HSBC AT 4.74%, 0 fee.

Am I likely to find anything better via a broker?

I’m hesitant to fix for 5 years as I may opt to sell up before then, but not sure 2 years is enough to see a significant reduction in interest rates.

2 year fixed 31/08/2025 £0 5.35% 5.00% (BBR*+4.50%)

5 year fixed 31/08/2028 £0 4.89% 5.00% (BBR*+4.50%)

remedy said:

I'm interested to hear that rates are down somewhat. 3.79% Halifax on 5 year fix...

Thankfully I've got till the end of July on my 2.09...

Barclays 3.84% 5 year fixed with £999 fee or 3.95% with no fee. 2 years deals are higher, seem like banks are feeling braver about whats going to happen in the next 5 years. More than double what we have currently fixed till 2028, but still way lower than the 5-6% 'normal' pre 2008 crash. Thankfully I've got till the end of July on my 2.09...

gangzoom said:

Barclays 3.84% 5 year fixed with £999 fee or 3.95% with no fee. 2 years deals are higher, seem like banks are feeling braver about whats going to happen in the next 5 years. More than double what we have currently fixed till 2028, but still way lower than the 5-6% 'normal' pre 2008 crash.

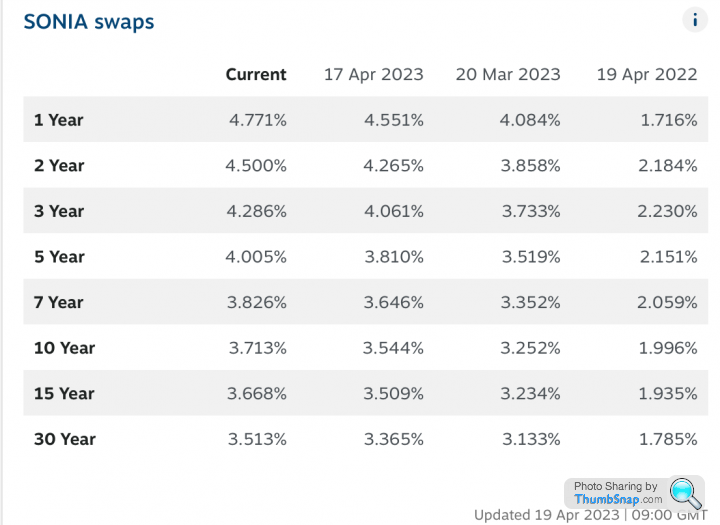

Banks dont really care as long as the LTVs are ok, your mortgage is sitting on their books for a matter of days before its packaged up. Sonia swaps are ticking upwards over last month.

Current 14 Apr 2023 17 Mar 2023 19 Apr 2022

1 Year 4.598% 4.551% 4.131% 1.716%

2 Year 4.314% 4.274% 3.944% 2.184%

3 Year 4.107% 4.069% 3.807% 2.230%

5 Year 3.853% 3.811% 3.554% 2.151%

7 Year 3.687% 3.639% 3.369% 2.059%

10 Year 3.582% 3.527% 3.246% 1.996%

gangzoom said:

remedy said:

I'm interested to hear that rates are down somewhat. 3.79% Halifax on 5 year fix...

Thankfully I've got till the end of July on my 2.09...

Barclays 3.84% 5 year fixed with £999 fee or 3.95% with no fee. 2 years deals are higher, seem like banks are feeling braver about whats going to happen in the next 5 years. More than double what we have currently fixed till 2028, but still way lower than the 5-6% 'normal' pre 2008 crash. Thankfully I've got till the end of July on my 2.09...

Any idea how Barclays ERC is i couldn’t see it at a glance.

I was intending to reach out to Sarnie again as I didn’t follow up last time panic set in and decided to see out the fix at 2.19% (ish).

G-wiz said:

Deesee said:

What does that all mean? Interest rates are set to continue to rise in the short/ mid term?The risk during this upward cycle is that we are more of a consumer society than ever before and trying to get people to actually not go shopping is close to impossible.

But personally, I don't think the BoE now controls that they way they once did. I think it's the FCA that controls how much people can buy when they go shopping.

All this excess shopping is done via credit. Just changing the cost of that credit a little bit doesn't really do anything. Much of the shopping is either done on 'zero deals' where the debt cost is hidden in the price of the goods so raising rates specifically raises inflation today not cut it!! or consumers are paying double digit funding costs on bad credit so an extra half a percent does nothing.

The only power the BoE really has is to try and keep the GBP stable against the USD.

Conversely, all the domestic power to curb spending lies in Westminster at the FCA.

Want to drop inflation on goods and services as well as reducing the amount being spent on them? Just increase the regulation on 'zero finance' and 'pay later' consumer finance.

Want to curb the inflationary pressure from credit card debt, just wind up the regulation on those lenders to make them reduce limits.

Want to curb the amount of spending on cars, just apply regulatory restrictions to car debt.

The FCA can micromanage every bit of consumer spending within the U.K. The BofE has nothing but a big hammer that no one would let it wield if possible.

In short, the FCA can look at each item in the CPI basket and restrict lending to it almost instantly and bring the CPI number down. Food is more difficult but most people self regulated by changing what they buy and those who can't will generally be on benefits so they can be managed directly.

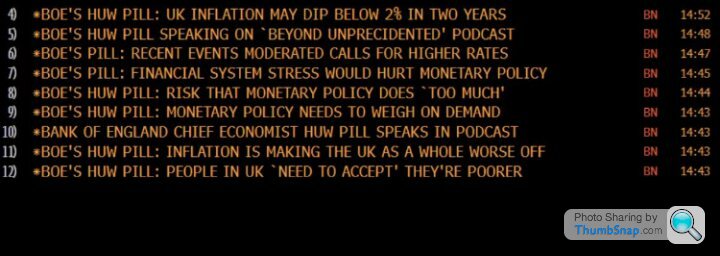

Going back to what Pill was alluding to, rates always overshoot. Always. What he is saying is that we all want 5% to be the overshoot but that gets less and less likely the more and more pay rises there are to keep people over spending.

Mind you, I wouldn't have phrased his last sound bite the way he did. I wouldn't have said that people need to get used to being less wealthy but instead said that people need to wake up to the reality that they were never as wealthy as they thought and how all that cheap borrowing made them think they were.

DonkeyApple said:

Mind you, I wouldn't have phrased his last sound bite the way he did. I wouldn't have said that people need to get used to being less wealthy but instead said that people need to wake up to the reality that they were never as wealthy as they thought and how all that cheap borrowing made them think they were.

Politically though, that would have been, ah, unpalatable.

Agree on FCA vs BoE...sadly our current government is unlikely to do anything useful...

Gassing Station | Finance | Top of Page | What's New | My Stuff