Re-mortgage now or wait?

Discussion

I always took the long term fix rather than variable over several terms. Being that I started fixing in 2004, I was nearly always on the wrong side and could have paid less. But, the amounts were never much and if someone asked me for £30/40 a month you can guarantee that as long as your personal circumstances don’t change then you will have that certainly you will be able to afford the roof over your head, it would seem like a good deal

ThingsBehindTheSun said:

If, as it looking likely Ukraine are going to lose the war with Russia this year, what effect do we think this will have on the market?

Or is everyone going to be so scared of being nuked to death that they won't care?

Not sure Ukraine losing is more likely to set off a nuke war? I generally think that the expected likely outcomes are priced in to deals. It’s the unexpected that causes things to then Or is everyone going to be so scared of being nuked to death that they won't care?

Stella Tortoise said:

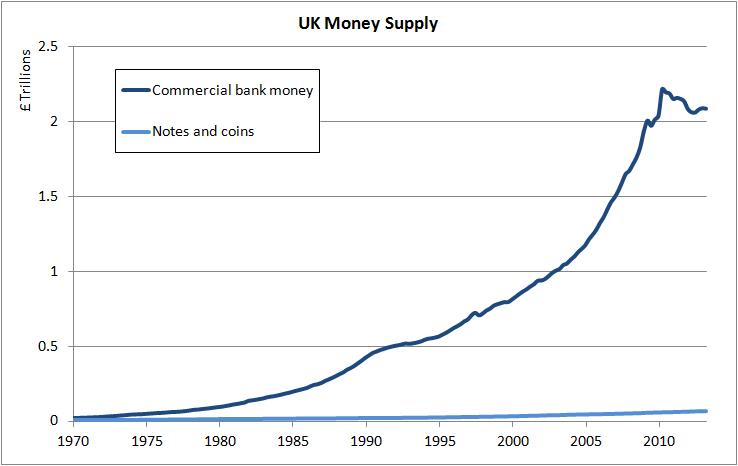

On the BOE website you can download a spreadsheet showing every rate change since around 1975.

It puts today’s rates into perspective.

Indeed, but it's worth crossing those dates with say M2 money supply at the time to get a better feel:It puts today’s rates into perspective.

Rates have been much higher historically but on next to no money compared to today.

And that chart only goes up to 2011. It's £3bn today!!!

Stella Tortoise said:

On the BOE website you can download a spreadsheet showing every rate change since around 1975.

It puts today’s rates into perspective.

Without considering house prices/ required levels of borrowing to afford a house these days - the perspective is skewed.It puts today’s rates into perspective.

At that the time of the disastrous Sept 22 mini budget it was reported that 6% at todays prices was the equivalent of 15% back in the day.

Zj2002 said:

Stella Tortoise said:

On the BOE website you can download a spreadsheet showing every rate change since around 1975.

It puts today’s rates into perspective.

Without considering house prices/ required levels of borrowing to afford a house these days - the perspective is skewed.It puts today’s rates into perspective.

At that the time of the disastrous Sept 22 mini budget it was reported that 6% at todays prices was the equivalent of 15% back in the day.

I was interested in how the BOE have used rates to tackle inflation.

Edited by Stella Tortoise on Wednesday 1st May 08:10

DonkeyApple said:

10 year rates kept disappearing over the previous decade. And when they were on the table they often didn't look hugely competitive.

There were moments when they were in the market and great value but I'm not sure there's any mileage in self flagellation as the odds of facing a renewal window when that was the case might have been long.

Harry Hindsight, the greatest and wealthiest chap any of us will ever know but the bloke's actually a complete tool as he's rarely around when you need him.

I was a first time buyer in 2017, very green, very conservative. Mortgage advisor recommended a 5yr fix with CBS at 2.34% (85%LTV) There were moments when they were in the market and great value but I'm not sure there's any mileage in self flagellation as the odds of facing a renewal window when that was the case might have been long.

Harry Hindsight, the greatest and wealthiest chap any of us will ever know but the bloke's actually a complete tool as he's rarely around when you need him.

At renewal time in 2022, and I've just missed out on all those lovely 1 and 2% rates. Checking the market and there's not much on offer below 3.5% (Aug 22) so I call my existing lender and have a chat.

They offer a 15 year term with a 10 year fix at 3.7% (60%LTV) which I balked at initially, but the advisor explained that this also came with unlimited overpayments, and no ERC, so if rates were to drop again, I could swap with no penalties.

Looking back now, I think that was the right decision and I'm glad I took it. I upped my monthly payment slightly, and am paying regularly into a 4.1% savings account with a view to clearing it completely before the end of the fix.

Edited by RoadToad84 on Wednesday 1st May 09:13

Well today is completion day on my remortgage journey. Managed to secure the Co-Op 3.89% 5yr Fix that was briefly offered back in January.

Coupled with a paydown of 10% of the capital my monthly payments are only increasing by £95 (on a new balance of 225k)

So having gone from 1.94% to 3.89% and given the way rates are moving at the moment I'm happy with the outcome.

Coupled with a paydown of 10% of the capital my monthly payments are only increasing by £95 (on a new balance of 225k)

So having gone from 1.94% to 3.89% and given the way rates are moving at the moment I'm happy with the outcome.

Edited by K is King on Wednesday 1st May 12:20

usn90 said:

I’ve locked in a 5.51% (+0.26% ) 2 year tracker with Santander, could have gone for a 4.4% 5 year fixed but wanted a tracker for unlimited overpayments.

Have until October for any improvements in deals to come up.

Bold. Have until October for any improvements in deals to come up.

This is kind of what I’d probably opt for though, but the issue I have in my head was how far some of the fixed deals being offered were below base when things looked a bit more rosey. I don’t quite understand the mechanics of how they price but I remember 3.89% being around recently, takes a fairly punchy cut for you to get to that - and if you do, will the fixed rates be considerably lower still?

usn90 said:

I’ve locked in a 5.51% (+0.26% ) 2 year tracker with Santander, could have gone for a 4.4% 5 year fixed but wanted a tracker for unlimited overpayments.

Have until October for any improvements in deals to come up.

First Direct have a 4.44% 5yr fixed that allows unlimited overpayments. Have until October for any improvements in deals to come up.

Sarnie said:

It's been pretty much rate rises non stop for about 2 months, including this week, which you would assume which include today's hold...........so even if we see some rate cuts, it will take a while just to get back to where they were around February.

Why is that? As far as I can tell we're in the same position as February now, i.e., inflation looks actually under control now, rate cut imminent, why are we not seeing lenders throw out the sub 4 rates again?okgo said:

Why is that? As far as I can tell we're in the same position as February now, i.e., inflation looks actually under control now, rate cut imminent, why are we not seeing lenders throw out the sub 4 rates again?

Mortgage rates are about 0.6% higher than they were in February. I did a number at 3.89% back then, one today at the same LTV was 4.52%........okgo said:

Why is that? As far as I can tell we're in the same position as February now, i.e., inflation looks actually under control now, rate cut imminent, why are we not seeing lenders throw out the sub 4 rates again?

we have a war in europe, a war in the middle east, an election in the autumn, a US election, and the Fed saying rate cuts will be slow. all that risk needs to be baked in, and i wouldnt count on a rate cut in the UK soon -

ARHarh said:

Inflation may be lower than it was, but it is still far from under control. It is still running at nearly 2x what everyone wants. Can't see any significant cuts yet.

The bloke who in part makes the decisions literally said this morning that he saw cuts coming, no? Word is that April inflation data will be positive..Anyway, I see your point Chris but all that stuff was there in Feb too. Perhaps banks got burned before and are reluctant to jump the gun with their mortgage offers this time.

Gassing Station | Finance | Top of Page | What's New | My Stuff