Re-mortgage now or wait?

Discussion

DonkeyApple said:

I guess the calculation works where 4-5 year's rent while trying to build a deposit is a greater cost. It'll be a good product for the right person. The key will be to use the 5 years to bang in enough so as to be able to get a normal mortgage as soon as possible.

At the end of the 5 year term you will have about 5% equity and can start to move onto other products, assuming no price changes (which I think will only help the people on this product). I think if you are wanting to buy in London then it's a similar cost to something that isn't a house share and gives you more stability. It's not for everyone but it's a good product for the right person.Stella Tortoise said:

Mr Penguin said:

At the end of the 5 year term you will have about 5% equity

Not a given unfortunately.Stella Tortoise said:

Not a given unfortunately.

There is risk that prices fall, but that is always true. You are more likely to benefit from prices going up IMO, in which case you could be well on the way to 10%. In any case, you need to think about your appetite for risk and what you think is likely to happen over the next few years as with any other decision. It's still a good product for the person who thinks it's right for them.Caddyshack said:

Yes, if they are lucky with the timing they may inflate the value with some price rises and get a better LTV that way too....it's a gamble.

I can see this being attractive to young professionals on the way up with income etc.

Add in being able to haggle and sweat a seller out, which is not an innate skill when we are young but hardly difficult to self teach and buying something which is sound but needs some TLC which you can take care of yourself, again a skill which is very easy to self learn and it's not impossible to end up in something which has a 5-10% uplift pretty much done in yr1. All you need to then do is not go shopping like a ponce from the 'everything new' brigade and with a spot of career enhancement over the period all is good. I can see this being attractive to young professionals on the way up with income etc.

Mr Penguin said:

Stella Tortoise said:

Not a given unfortunately.

There is risk that prices fall, but that is always true. You are more likely to benefit from prices going up IMO, in which case you could be well on the way to 10%. In any case, you need to think about your appetite for risk and what you think is likely to happen over the next few years as with any other decision. It's still a good product for the person who thinks it's right for them.

Builders will do anything to maintain the book value. Free carpets, a car etc.

Paying 3% on £500k for two years is super cheap funding compared to what they will currently be paying on the debt against the stuck properties that are bleeding them.

As you say, the key is whether the nominal value is correct and how much of your 25% remains in two years time when you step up onto a normal rate.

But they're clearly getting desperate so if it's what you want, where you want there's probably more to be given. Screw them down further on the price, they're bound to have put some fluff into their asking. Screw them down on the service charge, that's a hidden area they might be willing to concede massively on as what they take off yours will be paid by the other leaseholders. You might be able to pull a real blinder on that front. Why not ask for a nice family holiday as well and a few £K of John Lewis vouchers all to help you to help them out of their little predicament. They'll just pay it out of the staff bonus pool. No harm in asking for a contract that'll pay you a cash lump sum immediately should the CMA find Berkeley guilting of price fixing. Their guilt, would after all impact the value of your home so you'd expect compensation.

This is a company that wouldn't hesitate to f k you into next week so if they have a bit of a problem shifting some unwanted stock that's burning them a funding hole then anyone who has an interest in living there should not hesitate to absolutely screw the crap out of them. You just don't know what they're will to bribe you with to get you take over their debt issue until you ask and then ask for more and keep asking until they tell you to fk off, upon which you then ask for more. It's Canary Wharf, be brash, be brazen, be arrogant, be repellent even. They're a house builder with a load of debt bleeding them and a bunch of stock they can't shift. You are their saviour, you're willing to do them a massive favour but they're going to need to bend over.

k you into next week so if they have a bit of a problem shifting some unwanted stock that's burning them a funding hole then anyone who has an interest in living there should not hesitate to absolutely screw the crap out of them. You just don't know what they're will to bribe you with to get you take over their debt issue until you ask and then ask for more and keep asking until they tell you to fk off, upon which you then ask for more. It's Canary Wharf, be brash, be brazen, be arrogant, be repellent even. They're a house builder with a load of debt bleeding them and a bunch of stock they can't shift. You are their saviour, you're willing to do them a massive favour but they're going to need to bend over.

Paying 3% on £500k for two years is super cheap funding compared to what they will currently be paying on the debt against the stuck properties that are bleeding them.

As you say, the key is whether the nominal value is correct and how much of your 25% remains in two years time when you step up onto a normal rate.

But they're clearly getting desperate so if it's what you want, where you want there's probably more to be given. Screw them down further on the price, they're bound to have put some fluff into their asking. Screw them down on the service charge, that's a hidden area they might be willing to concede massively on as what they take off yours will be paid by the other leaseholders. You might be able to pull a real blinder on that front. Why not ask for a nice family holiday as well and a few £K of John Lewis vouchers all to help you to help them out of their little predicament. They'll just pay it out of the staff bonus pool. No harm in asking for a contract that'll pay you a cash lump sum immediately should the CMA find Berkeley guilting of price fixing. Their guilt, would after all impact the value of your home so you'd expect compensation.

This is a company that wouldn't hesitate to f

k you into next week so if they have a bit of a problem shifting some unwanted stock that's burning them a funding hole then anyone who has an interest in living there should not hesitate to absolutely screw the crap out of them. You just don't know what they're will to bribe you with to get you take over their debt issue until you ask and then ask for more and keep asking until they tell you to fk off, upon which you then ask for more. It's Canary Wharf, be brash, be brazen, be arrogant, be repellent even. They're a house builder with a load of debt bleeding them and a bunch of stock they can't shift. You are their saviour, you're willing to do them a massive favour but they're going to need to bend over. ooid said:

Their current ratio is pretty decent though? (Over 3.0). I assumed many housebuilders in UK were quite well positioned with their debt levels since 08.

Most look to be but they've also got to be able to refinance and if they aren't moving units then lenders are going to crucify them on rates or even reduce their lines. Plus, they've got shareholders to reward and they want units sold, cash in and the least amount being paid to lenders. And obviously, they have their peers to compete against. Subsidising a mortgage by 3% for a couple of years to get a unit shifted seems like a clever move but it also reveals which units are stuck and not moving so if you were looking to buy a pad in Canary Wharf you'd be a bit mad to not be smelling blood and keen to see how far you can push them. They're not a charity so screw them for every penny on the table. There's no downside to offering to help them out with their problem and being CW they'll recognise the price of help.

But then I've always looked at those 'last few units' adverts as declarations that no one who did buy on the development wanted those units which is why they haven't sold and the builder is very keen to get shot and clear the books on the development. And developers can be very keen to give you lots of things that don't directly cost them money and still allow them to book the big number without revealing the real price. It's a soft market so make them pay, you make your money on a property when you buy it rather than when you sell it.

That 700k 1 bed unit also has -estimated- 4.7k service charge (annual) - Meaning, it will go through the roof in a few years. My colleague last year sold his less than 10 years old flat there, the service charge was nearly 9k annual!

Loads of supply available in the area at the moment, I mentioned previously and most of it quite good quality. I think the area is changing slightly from business to residential, though loads of public amenities should be created. Without decent schools and hospitals, the area will never attract young families with relatively good earning power and lifestyle.

- Meaning, it will go through the roof in a few years. My colleague last year sold his less than 10 years old flat there, the service charge was nearly 9k annual!Loads of supply available in the area at the moment, I mentioned previously and most of it quite good quality. I think the area is changing slightly from business to residential, though loads of public amenities should be created. Without decent schools and hospitals, the area will never attract young families with relatively good earning power and lifestyle.

ooid said:

That 700k 1 bed unit also has -estimated- 4.7k service charge (annual) - Meaning, it will go through the roof in a few years. My colleague last year sold his less than 10 years old flat there, the service charge was nearly 9k annual!

Loads of supply available in the area at the moment, I mentioned previously and most of it quite good quality. I think the area is changing slightly from business to residential, though loads of public amenities should be created. Without decent schools and hospitals, the area will never attract young families with relatively good earning power and lifestyle.

It's not any easy place to live for the prices being asked. If the convenience of the 10 minute commute to the office where you spend 20 hours a day waiting for the boss to go home before you can leave isn't there then there isn't much of a draw to live in the area? It's an area that remains mostly social housing and hard work to get out of should the tube not be working. Very little private schooling and the social juxtaposition of the state system isn't palatable. - Meaning, it will go through the roof in a few years. My colleague last year sold his less than 10 years old flat there, the service charge was nearly 9k annual!Loads of supply available in the area at the moment, I mentioned previously and most of it quite good quality. I think the area is changing slightly from business to residential, though loads of public amenities should be created. Without decent schools and hospitals, the area will never attract young families with relatively good earning power and lifestyle.

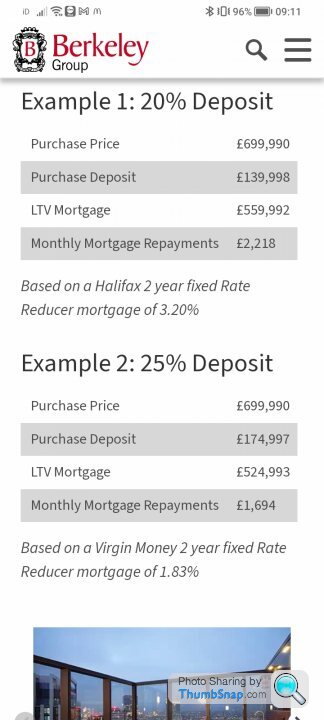

Re the 700k flat, the builder is offering to subsidise 3% of a £500k loan for the first two years. So not even a 5% discount on the asking in reality but the key is that it'll be a strong lure for folks who never think or plan more than a year or so in advance and it allows them to not show the discount on the book value, plus 3% will be less than they're currently paying to have it empty and no sc being paid.

I suspect you could screw them into a good deal so long as it allows them to not reveal the giveaway in the book value. There will be lots of things of value they can throw in that don't cost them much but represent cash in the bank for you.

There are loads of 1 bed or studio flats in E14 at the moment, sub 300k. Mostly 5-15 years old stock, not too aged and require less service charge with lower amenities.

Developers went extremely myopic in the area last 10 years, produced only one type of property there and tectonic-shift in the office market totally left them with a massive over*supply. In a way, I kinda like the area now whenever I visit its more lively than before, more locals and active. It is lacking infrastructural amenities though for longer term community aspect. Proper top*down strategic touch necessary but current or future governments will not have any intellectual capacity or skills for that.

Developers went extremely myopic in the area last 10 years, produced only one type of property there and tectonic-shift in the office market totally left them with a massive over*supply. In a way, I kinda like the area now whenever I visit its more lively than before, more locals and active. It is lacking infrastructural amenities though for longer term community aspect. Proper top*down strategic touch necessary but current or future governments will not have any intellectual capacity or skills for that.

My current rate of 2.84% ends at the end of September, so I have just under six months to make a decision. I have a call with my mortgage broker tomorrow, but obviously he will want a fee. Last time on my other property the best he could do was beat the renewal quoted by Natwest by 0.05% and he agreed to waive his fee as it would have ended up costing more with the fee.

I am not prepared to pay an arrangement fee to lower the monthly cost, so the deals offered by Virgin on a BTL are :

2 Year = 5.65%

3 Year = 5.55%

5 Year = 5.03%

By comparison, I can get 5 Years at 4.73% if I pay a £1995.

I can arrange this over the internet with one button click. I will also add that I have always gone for two year deals and hate the hassle, gamble and potential fees that go with this.

One important fact is I am overpaying 10% each year. My gut feel is to wait a few months in the hope that rates might fall slightly before the election and then go for the 5 year fix with no fee for 5.03% and keep overpaying 10% a year.

The mortgage is just under £150K so we are not talking massive differences in the monthly payments.

I am not prepared to pay an arrangement fee to lower the monthly cost, so the deals offered by Virgin on a BTL are :

2 Year = 5.65%

3 Year = 5.55%

5 Year = 5.03%

By comparison, I can get 5 Years at 4.73% if I pay a £1995.

I can arrange this over the internet with one button click. I will also add that I have always gone for two year deals and hate the hassle, gamble and potential fees that go with this.

One important fact is I am overpaying 10% each year. My gut feel is to wait a few months in the hope that rates might fall slightly before the election and then go for the 5 year fix with no fee for 5.03% and keep overpaying 10% a year.

The mortgage is just under £150K so we are not talking massive differences in the monthly payments.

ooid said:

There are loads of 1 bed or studio flats in E14 at the moment, sub 300k. Mostly 5-15 years old stock, not too aged and require less service charge with lower amenities.

Developers went extremely myopic in the area last 10 years, produced only one type of property there and tectonic-shift in the office market totally left them with a massive over*supply. In a way, I kinda like the area now whenever I visit its more lively than before, more locals and active. It is lacking infrastructural amenities though for longer term community aspect. Proper top*down strategic touch necessary but current or future governments will not have any intellectual capacity or skills for that.

its because studio and 1 beds are / were dirt easy to sell in Asia to BTL investors. seriously easy Developers went extremely myopic in the area last 10 years, produced only one type of property there and tectonic-shift in the office market totally left them with a massive over*supply. In a way, I kinda like the area now whenever I visit its more lively than before, more locals and active. It is lacking infrastructural amenities though for longer term community aspect. Proper top*down strategic touch necessary but current or future governments will not have any intellectual capacity or skills for that.

ThingsBehindTheSun said:

My current rate of 2.84% ends at the end of September, so I have just under six months to make a decision. I have a call with my mortgage broker tomorrow, but obviously he will want a fee. Last time on my other property the best he could do was beat the renewal quoted by Natwest by 0.05% and he agreed to waive his fee as it would have ended up costing more with the fee.

I am not prepared to pay an arrangement fee to lower the monthly cost, so the deals offered by Virgin on a BTL are :

2 Year = 5.65%

3 Year = 5.55%

5 Year = 5.03%

By comparison, I can get 5 Years at 4.73% if I pay a £1995.

I can arrange this over the internet with one button click. I will also add that I have always gone for two year deals and hate the hassle, gamble and potential fees that go with this.

One important fact is I am overpaying 10% each year. My gut feel is to wait a few months in the hope that rates might fall slightly before the election and then go for the 5 year fix with no fee for 5.03% and keep overpaying 10% a year.

The mortgage is just under £150K so we are not talking massive differences in the monthly payments.

Find a broker that doesn't charge you every single time........I am not prepared to pay an arrangement fee to lower the monthly cost, so the deals offered by Virgin on a BTL are :

2 Year = 5.65%

3 Year = 5.55%

5 Year = 5.03%

By comparison, I can get 5 Years at 4.73% if I pay a £1995.

I can arrange this over the internet with one button click. I will also add that I have always gone for two year deals and hate the hassle, gamble and potential fees that go with this.

One important fact is I am overpaying 10% each year. My gut feel is to wait a few months in the hope that rates might fall slightly before the election and then go for the 5 year fix with no fee for 5.03% and keep overpaying 10% a year.

The mortgage is just under £150K so we are not talking massive differences in the monthly payments.

Gassing Station | Finance | Top of Page | What's New | My Stuff