BOE 3rd November Rate Announcement

Discussion

Panamax said:

BOE forced to increase rates purely to prevent collapse of the currency.

The effect of increased borrowing costs on top of energy price rises and food price inflation will trash the whole economy, plunging UK into a long recession from which there's no obvious route to recovery.

It does feel like we just have to tow the feds line? It's doesn't feel like we are in control of our destiny, global supply shocks, the global reverse currency rate setting and the markets reaction if we stray away from the same increases? What can we do proactively different, zero? Why do we need the Boe to make decisions we just do QE when the FED does it, tightens when it tightens, raises rates when it does, or face as Panamax says (even worse) currency devaluation? The effect of increased borrowing costs on top of energy price rises and food price inflation will trash the whole economy, plunging UK into a long recession from which there's no obvious route to recovery.

p1doc said:

my first house bought 2000 was 3 bedroom midterraced villa for £59,950 sold 5 years later for £120,000 bixarre how prices have just escalated since 2000

In some ways, it was that period that was the most surprising of all. The base rate was 5.5% coming into 2000 and was still 4.5% at the end of 2005, but prices still shot up, doubling in your example.It's more understandable after 2009, when base rates were reduced to 0.5%, borrowing multiples increased and all of the other stimuli were introduced.

kingston12 said:

I'm sure I saw something linked on a thread here showing that the affordability of 6% mortgages now is about the equivalent of paying 14% interest back in the 90s.

I'll see if I can find the link, but if not hopefully someone else will. It sounded fairly sensible, if very frightening at the same time.

I'll see if I can find the link, but if not hopefully someone else will. It sounded fairly sensible, if very frightening at the same time.

https://twitter.com/EdConwaySky/status/15849499336...

kingston12 said:

p1doc said:

my first house bought 2000 was 3 bedroom midterraced villa for £59,950 sold 5 years later for £120,000 bixarre how prices have just escalated since 2000

In some ways, it was that period that was the most surprising of all. The base rate was 5.5% coming into 2000 and was still 4.5% at the end of 2005, but prices still shot up, doubling in your example.It's more understandable after 2009, when base rates were reduced to 0.5%, borrowing multiples increased and all of the other stimuli were introduced.

Mind you that's balanced somewhat by the disappearance of such things as final salary pensions, meaning my generation will have to use its unearned property equity to provide as comfortable retirement income as those who came before. I appreciate it's even worse now for young people starting out, they have neither affordable property nor a golden pension market. Of course, a lot of the wealth will pass down from my generation to them via Bank of Mum and Dad, and inheritance. So there are some swings and roundabouts at play, but overall yes, I am concerned about youngsters, and of course add in student debt and things look really tough. I have 2 teenagers about to embark on higher education so all of this is in the forefront of my mind, and I also want to retire in 7 or 8 years.

It really is a buggers' muddle, and looking back, to the way the financial and property markets have been handled by the governments since about 1979 (blimey, that's a very precise "about"...hmmm wonder who won an election that year and stayed around for near 20 years), it's all got its root in extreme free market dogma, as opposed to taking a more Western European/Scandinavian social democratic governance model IMHO.

wildoliver said:

I have a real feeling that people are dumping money in to classic cars as a safe place to put it, last time that happened was back at the start of the 90s and the market went through the floor leaving people holding deeply ordinary cars they had bought at extraordinary prices.

Agreed! Some classics dropped to a 1/3 of their peak and it's easy to imagine it happening again. The only thing we learn from history is that no one ever learns anything from history!  ked the economy.

ked the economy.Ari said:

wildoliver said:

I have a real feeling that people are dumping money in to classic cars as a safe place to put it, last time that happened was back at the start of the 90s and the market went through the floor leaving people holding deeply ordinary cars they had bought at extraordinary prices.

Agreed! Some classics dropped to a 1/3 of their peak and it's easy to imagine it happening again. The only thing we learn from history is that no one ever learns anything from history! gazapc said:

Armitage.Shanks said:

Some of us remember mortgage rates of above 10% that figure is lost on the current millennials who have been used to very low interest rates for years.

Considering the ratios of earnings to average house prices, I wouldn't be surprised if the the current ~6% rates on offer are effectively more expensive than 10% rates 30-40 years ago.Anyone have stats on this?

House price rises have been ridiculous for the last two years, pity younger people wanting to get on the first rung of the ladder, maybe they will fall a bit now.

If that’s the correlation then yes it wasn’t fun !

Iirc our rate at its highest was 15.4% but thankfully it didn’t stay at that level for many months which considering we had zero savings at the time was just as well.

We moved in 1988 paying £125k and sold it in 1995 for £105k so definitely fell a few rungs on that ladder.

Iirc our rate at its highest was 15.4% but thankfully it didn’t stay at that level for many months which considering we had zero savings at the time was just as well.

We moved in 1988 paying £125k and sold it in 1995 for £105k so definitely fell a few rungs on that ladder.

Armitage.Shanks said:

The rate rise is long overdue and BoE should have done it 6+ months ago.

It needs to go higher yet to get inflation under control and reduce public spending. Savings rates also need to start looking attractive again.

Take a look around, all pubs, restaurants, hign end luxury goods etc. are at their highest still with no sign of spenders reining in finances.

Some of us remember mortgage rates of above 10% that figure is lost on the current millennials who have been used to very low interest rates for years.

If I had a £1 for everyone over the age of 50 that says "I remember when blah blah blah" I'd have paid off my mortgage by now. It's an entirely different economic landscape, please stop banging on about it.It needs to go higher yet to get inflation under control and reduce public spending. Savings rates also need to start looking attractive again.

Take a look around, all pubs, restaurants, hign end luxury goods etc. are at their highest still with no sign of spenders reining in finances.

Some of us remember mortgage rates of above 10% that figure is lost on the current millennials who have been used to very low interest rates for years.

Pheo said:

skinnyman said:

If I had a £1 for everyone over the age of 50 that says "I remember when blah blah blah" I'd have paid off my mortgage by now. It's an entirely different economic landscape, please stop banging on about it.

Does get a bit old doesn’t it.Edited by anonymous-user on Thursday 3rd November 20:43

mdavids said:

My rate is due to end next October, currently it's 1.9% and I'll have about £65k left. My provider's current rates are over 5.5% SVR and even more for a fix, I'm guessing they'll be about that or more this time next year.

Last week I got myself a £25k bank loan at 3.9% and have stuck this away for 6 months earning almost the same in interest as what it's costing me. I'm lucky enough ( tight enough) that I've managed to save enough to pay off the rest of the mortgage if I put this £25k in.

So if mortgage rates are below this next October I'll renew and just pay off the loan. If they're more I'll clear the mortgage and my only debt will be the remainder of the £25k.

I think I've done a good thing, worst case it's cost me a couple of hundred quid. But I have a bit of peace of mind now knowing I don't have to secure another mortgage unless I want to.

I’m doing exactly the same, decided to use savings and a 25k bank loan I got for 3.6% over 3yrs (£1.3k interest) instead of 5.89% and around £35k interest over the term. Last week I got myself a £25k bank loan at 3.9% and have stuck this away for 6 months earning almost the same in interest as what it's costing me. I'm lucky enough ( tight enough) that I've managed to save enough to pay off the rest of the mortgage if I put this £25k in.

So if mortgage rates are below this next October I'll renew and just pay off the loan. If they're more I'll clear the mortgage and my only debt will be the remainder of the £25k.

I think I've done a good thing, worst case it's cost me a couple of hundred quid. But I have a bit of peace of mind now knowing I don't have to secure another mortgage unless I want to.

I know people are against paying it off but I see it as perfect sense raiding the savings to get the house paid off.

skinnyman said:

Armitage.Shanks said:

The rate rise is long overdue and BoE should have done it 6+ months ago.

It needs to go higher yet to get inflation under control and reduce public spending. Savings rates also need to start looking attractive again.

Take a look around, all pubs, restaurants, hign end luxury goods etc. are at their highest still with no sign of spenders reining in finances.

Some of us remember mortgage rates of above 10% that figure is lost on the current millennials who have been used to very low interest rates for years.

If I had a £1 for everyone over the age of 50 that says "I remember when blah blah blah" I'd have paid off my mortgage by now. It's an entirely different economic landscape, please stop banging on about it.It needs to go higher yet to get inflation under control and reduce public spending. Savings rates also need to start looking attractive again.

Take a look around, all pubs, restaurants, hign end luxury goods etc. are at their highest still with no sign of spenders reining in finances.

Some of us remember mortgage rates of above 10% that figure is lost on the current millennials who have been used to very low interest rates for years.

My main point is that the current BoE interest rate is nowhere near where it needs to be to bring down inflation. We should then see a collapse in housing values which in some respect will assist those to get on the housing ladder despite higher rates which I suspect won't last long where like me once you're used to paying it you then carry on overpaying and reduce the mortgage term.

I said it months ago that this economy can't withstand 2.5% rates over the longer term let alone 5%, there is simply too much debt and to inflate it away in a reasonable amount of time will be very painful.

If they can't get away with 3 more 0.25% hikes and need to do more then we are all in serious trouble whether one has debt or not because it means structurally the system isn't functioning correctly anymore.

A lot of US economists are predicting US inflation below 2% by end of 2023, to go from 8% to 2% in a year means that a lot of demand and a lot of jobs are going out of the market.

The other reason rates can't go too much is because of Government debt, I know everyone says about long dated Gilts etc but as rates rise, it affects the value of the underlying and at 3% the value notionally drops by £184B, the BOE own it but it is guaranteed by the Treasury. If you are Japan it doesn't matter but since we as a country require external financing, this is a problem from a market point of view.

If they can't get away with 3 more 0.25% hikes and need to do more then we are all in serious trouble whether one has debt or not because it means structurally the system isn't functioning correctly anymore.

A lot of US economists are predicting US inflation below 2% by end of 2023, to go from 8% to 2% in a year means that a lot of demand and a lot of jobs are going out of the market.

The other reason rates can't go too much is because of Government debt, I know everyone says about long dated Gilts etc but as rates rise, it affects the value of the underlying and at 3% the value notionally drops by £184B, the BOE own it but it is guaranteed by the Treasury. If you are Japan it doesn't matter but since we as a country require external financing, this is a problem from a market point of view.

skinnyman said:

Armitage.Shanks said:

The rate rise is long overdue and BoE should have done it 6+ months ago.

It needs to go higher yet to get inflation under control and reduce public spending. Savings rates also need to start looking attractive again.

Take a look around, all pubs, restaurants, hign end luxury goods etc. are at their highest still with no sign of spenders reining in finances.

Some of us remember mortgage rates of above 10% that figure is lost on the current millennials who have been used to very low interest rates for years.

If I had a £1 for everyone over the age of 50 that says "I remember when blah blah blah" I'd have paid off my mortgage by now. It's an entirely different economic landscape, please stop banging on about it.It needs to go higher yet to get inflation under control and reduce public spending. Savings rates also need to start looking attractive again.

Take a look around, all pubs, restaurants, hign end luxury goods etc. are at their highest still with no sign of spenders reining in finances.

Some of us remember mortgage rates of above 10% that figure is lost on the current millennials who have been used to very low interest rates for years.

There is much more debt and asset prices are higher, which has been fuelled by years of low interest rates and looser borrowing, but the external factors still have a big influence, hence we are now seeing interest rates that are not really compatible with the current levels of assets prices and debt.

kingston12 said:

skinnyman said:

Armitage.Shanks said:

The rate rise is long overdue and BoE should have done it 6+ months ago.

It needs to go higher yet to get inflation under control and reduce public spending. Savings rates also need to start looking attractive again.

Take a look around, all pubs, restaurants, hign end luxury goods etc. are at their highest still with no sign of spenders reining in finances.

Some of us remember mortgage rates of above 10% that figure is lost on the current millennials who have been used to very low interest rates for years.

If I had a £1 for everyone over the age of 50 that says "I remember when blah blah blah" I'd have paid off my mortgage by now. It's an entirely different economic landscape, please stop banging on about it.It needs to go higher yet to get inflation under control and reduce public spending. Savings rates also need to start looking attractive again.

Take a look around, all pubs, restaurants, hign end luxury goods etc. are at their highest still with no sign of spenders reining in finances.

Some of us remember mortgage rates of above 10% that figure is lost on the current millennials who have been used to very low interest rates for years.

There is much more debt and asset prices are higher, which has been fuelled by years of low interest rates and looser borrowing, but the external factors still have a big influence, hence we are now seeing interest rates that are not really compatible with the current levels of assets prices and debt.

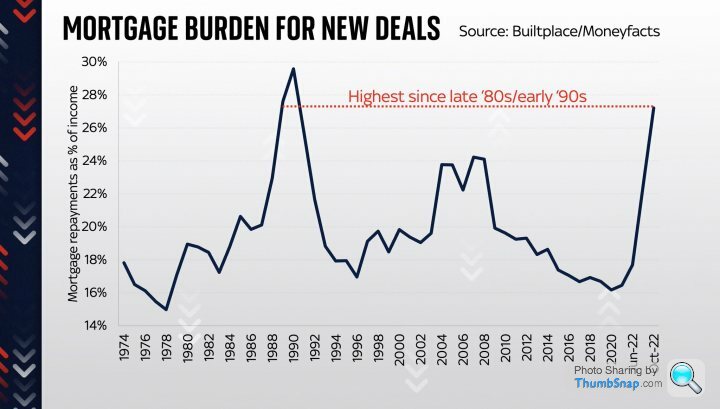

'Leeds Building Society said today’s average two-year fixed rate mortgage rate of 6.43 per cent may seem lower than the mortgage rates of 15 per cent in 1980, but surging house prices, driven by a lack of supply and historically low interest rates since the financial crisis of 2008, and the increase in household indebtedness, mean that the current mortgage rates are equivalent to a rate of 25.7 per cent in 1980.

In 1980, the average UK house price was around £21,000 and mortgage costs accounted for 11.3 per cent of disposable income. Today, those figures are around £292,000 and 45.1 per cent respectively.

In a statement, the mutual said: “Housing is now at its least affordable point since records began. The average home currently costs 9.1 times the average local wage compared to 3.5 in 1997 (Source ONS). This particularly impacts young people.'

Average mortgage costs 45.1% of household income ffs!

Gassing Station | Finance | Top of Page | What's New | My Stuff