Gloomy pension prospects on average salary?

Discussion

jgrewal said:

I am always weary of posting in threads such as this and I think I posted in haste earlier. I think the opening poster is just saying it doesn't feel like there is going to expected or suitable pot being projected with his current earnings and contributions.

Personally with our country totally messed up financially I have no trust in a state pension being around - I think we'll get to a point where it is means tested by 2040. You don't need to be giving 10k a year to a person who has 500k plus in their private pot!

Someone with a £500k private pot is depending on state pension to top up their income substantially and whatsmore has likely paid far more towards earning their entitlement in lifetime tax/NI contributions than most.Personally with our country totally messed up financially I have no trust in a state pension being around - I think we'll get to a point where it is means tested by 2040. You don't need to be giving 10k a year to a person who has 500k plus in their private pot!

Who in their right mind would also save past the threshold if they are going to lose a benefit worth £200k+

All this sort of tinkering does is create further distortions with unintended side effects, which the government have just been forced to try and alleviate by removing the LTA.

It would backfire spectacularly, IMO

jgrewal said:

I am always weary of posting in threads such as this and I think I posted in haste earlier. I think the opening poster is just saying it doesn't feel like there is going to expected or suitable pot being projected with his current earnings and contributions.

Personally with our country totally messed up financially I have no trust in a state pension being around - I think we'll get to a point where it is means tested by 2040. You don't need to be giving 10k a year to a person who has 500k plus in their private pot!

Although possible I think they will just keep pushing the age of the state pension up. Otherwise the majority of people would just stop saving into a private pension once they get to a level where their state pension is at risk. Plus the public sector would all start striking.Personally with our country totally messed up financially I have no trust in a state pension being around - I think we'll get to a point where it is means tested by 2040. You don't need to be giving 10k a year to a person who has 500k plus in their private pot!

OP should probably factor in state pension not kicking in until 70-72 as the more realistic threat.

By and large so far there has been great advice given on this thread, e.g. upping to a 15-20% personal contribution to avoid 40% income tax, never marrying unless to a minted bird (or other gender of choice!) on a gold plated senior government/doctor pension or with huge family wealth, not having kids etc. The OP should be well set now for an early retirement of sports cars and luxury holidays.

I think a few folk will be shocked at the fairly

basic life you’ll lead on half a million quid given anyone who’s 30 odd now will live most likely well into their 90’s.

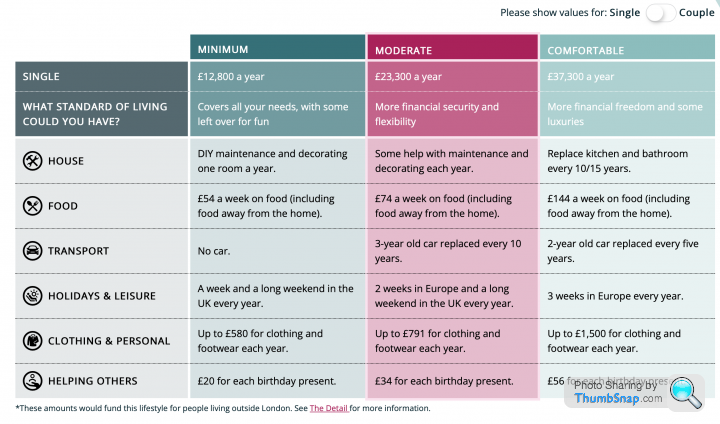

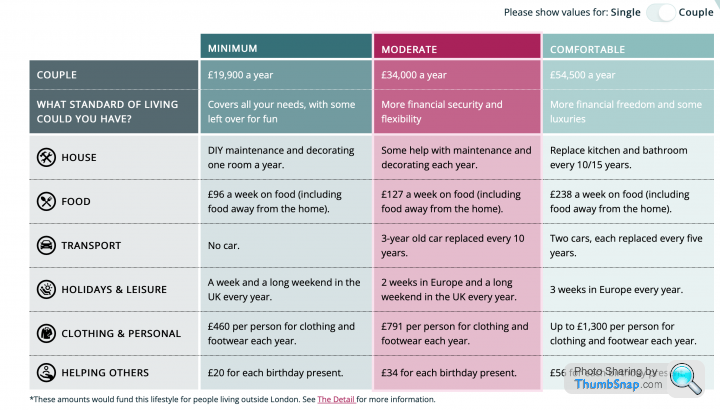

Even when you look at what it classed as ‘luxurious life’ by the IFS or whoever it was, it really isn’t anything more than normal comfortable living IMO.

£42k I think it was, for a couple!! Unsure whether they mixed up Great Britain and Romania but that’s in no way luxury to most people.

basic life you’ll lead on half a million quid given anyone who’s 30 odd now will live most likely well into their 90’s.

Even when you look at what it classed as ‘luxurious life’ by the IFS or whoever it was, it really isn’t anything more than normal comfortable living IMO.

£42k I think it was, for a couple!! Unsure whether they mixed up Great Britain and Romania but that’s in no way luxury to most people.

DoubleSix said:

There is average in the technical, national sense. And “average” in the sense of ones peer group and personal aspirations.

I don’t think the OP should be castigated for his perspective, rather, it says to me he realises he could be earning more and has a sense of self worth that is commendable.

To flip that, those who believe they are “achieving” by earning above the national average have set themselves a very low bar.

So 'average' in the real actual sense as everyone else understands it, and 'average' as in what the op thinks he's worth. Maybe he should 'work more hours' or 'get a better paid job'I don’t think the OP should be castigated for his perspective, rather, it says to me he realises he could be earning more and has a sense of self worth that is commendable.

To flip that, those who believe they are “achieving” by earning above the national average have set themselves a very low bar.

As for perspective, maybe he should spend a day volunteering at the CAB.

WelshRich said:

Many online tools assume that you’re going to use your fund to buy an annuity - Things may look a bit better if you take the forecast value when you hope to retire and plug it into a pension drawdown calculator instead…

P.S. I’m also a little wary of the tools sponsored by/hosted on pension company websites. They can be biased towards making your glass look half empty because they make more money if you pay more into your pension…

P.S. I’m also a little wary of the tools sponsored by/hosted on pension company websites. They can be biased towards making your glass look half empty because they make more money if you pay more into your pension…

deebs said:

The aviva calculator is a half decent one it'll let you set your target income, then show pot size and how long that'll last /what age you'll be when /if it runs out.

Echo these two posts., I put my figures in to some random calculators last night and it was incredible how poor it made me feel despite knowing I was way ahead of the pension pot curve and contribution levels for my age.Aviva is much more telling, and gives you better visibility. Something many calculators don't consider that your cost of living if retiring at 55 is going to be drastically different in your early 60s vs late 70s. Yes you still need to fund through to the live expectancy of 90 odd, but your cost of living is going to drastically ramp down with age, for most people.

ChrisNic said:

I hope OP doesn’t have any kids either.

The marginal rate for people earning £50-60k and not putting it into a pension (or other sal sacrifice) is terrifying. So many of my colleagues appear oblivious of this fact and are literally throwing money at HMRC.

I’m caught in an odd first world trap because of this and can no longer take any pay rises as cash.

There has to be some balance here surely? To get me down to none 40% tax I would need to chuck 25% of my salary into my pension, all the while mortgage rates are climbing (due to a bit of silly planning which I admit my mortgage payments have risen by 35%), my bills are more than ever (as in utilities, fuel, council tax and food) as well as regular living expenses, I am pushing 10% of my salary and my employer contributes 5%. I have had a pension most of my working life and my predicted pot at the end is around £200-300K (I also have a LISA that I put spare money into when I can) with a state pension (as long as it is still around) will give an ok income, certainly enough when you consider the mortgage should be done by then etc. Yes I am giving some money away to HRMC but I am also covering myself in the here and now. The marginal rate for people earning £50-60k and not putting it into a pension (or other sal sacrifice) is terrifying. So many of my colleagues appear oblivious of this fact and are literally throwing money at HMRC.

I’m caught in an odd first world trap because of this and can no longer take any pay rises as cash.

I dunno maybe my view is considered short sighted and I can be suitably ripped apart by those who know better but everyone outside of PH I talk to seems to think I have a reasonably good plan.

Boo-urns said:

The gloomy state of the stock market at the moment suggests that this is a good time to be investing heavily in your pension, does it not? It's what I'm doing at the moment. No doubt someone will be along in a moment to tell me I'm wrong!

I'm with you on this. I currently pay the maximum AVC I'm allowed on mine. Been here 4.5 years and it's currently only up about 8.5%, but given how low everything is at the moment I'm working on the theory that means I can buy more now and it'll go up later.A load of more recent staff are moaning a lot about the pension scheme though, as people who started a year or two ago have lost money so far.

okgo said:

I think a few folk will be shocked at the fairly

basic life you’ll lead on half a million quid given anyone who’s 30 odd now will live most likely well into their 90’s.

Even when you look at what it classed as ‘luxurious life’ by the IFS or whoever it was, it really isn’t anything more than normal comfortable living IMO.

£42k I think it was, for a couple!! Unsure whether they mixed up Great Britain and Romania but that’s in no way luxury to most people.

I think it depends on what you spend your money on obviously!basic life you’ll lead on half a million quid given anyone who’s 30 odd now will live most likely well into their 90’s.

Even when you look at what it classed as ‘luxurious life’ by the IFS or whoever it was, it really isn’t anything more than normal comfortable living IMO.

£42k I think it was, for a couple!! Unsure whether they mixed up Great Britain and Romania but that’s in no way luxury to most people.

We are retired and some months we spend not a lot if we are at home and don't go out much.

Everyone is different though.

We are frugal though, so shop at aldi, phone of giff gaff, no particularly expensive hobbies etc.

Our base budget is £1500 a month. There is usually some left over.

The issue is you can easily spend a lot of money if you dont think about it so you have to keep on top of your spending.

I think the main thing people dont realise is just how much they are taxed at work and the cost to go to work!

Someone on 40k a year thinks jeez I can only just survive on 40k so I need a pension income of more!

When in reality they are only getting 30k a year after tax. Lose another £5k on the cost to get to work and suddenly your 40k is actually 25.

Just my 2ps worth.

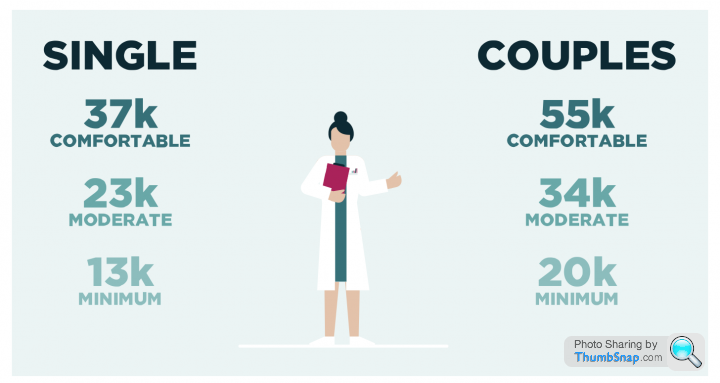

I find this website helps focus peoples minds on what "might" be needed in retirement in terms of actual income - examples for single and couples, both nationally and in London/SE areas

Once people have an idea of what income they need or desire, then it's easier to start thinking about how to save enough to reach that sort of target income

Seems to me that factoring some state pension towards those figures is useful, and then start working out what to save privately, either through a workplace pension, ISA or personal pension to attain the remainder is a useful approach.

https://www.retirementlivingstandards.org.uk

Once people have an idea of what income they need or desire, then it's easier to start thinking about how to save enough to reach that sort of target income

Seems to me that factoring some state pension towards those figures is useful, and then start working out what to save privately, either through a workplace pension, ISA or personal pension to attain the remainder is a useful approach.

https://www.retirementlivingstandards.org.uk

Edited by phpe on Friday 17th March 12:13

gotoPzero said:

I think it depends on what you spend your money on obviously!

We are retired and some months we spend not a lot if we are at home and don't go out much.

Everyone is different though.

We are frugal though, so shop at aldi, phone of giff gaff, no particularly expensive hobbies etc.

Our base budget is £1500 a month. There is usually some left over.

The issue is you can easily spend a lot of money if you dont think about it so you have to keep on top of your spending.

I think the main thing people dont realise is just how much they are taxed at work and the cost to go to work!

Someone on 40k a year thinks jeez I can only just survive on 40k so I need a pension income of more!

When in reality they are only getting 30k a year after tax. Lose another £5k on the cost to get to work and suddenly your 40k is actually 25.

Just my 2ps worth.

This is a decent point, you can structure retirement income using SIPPs and ISAs so you pay a very low tax rate (and no national insurance deductions) compared to when you were getting rinsed as an employee. Factor that in with a paid off mortgage and things suddenly don't look so bad.We are retired and some months we spend not a lot if we are at home and don't go out much.

Everyone is different though.

We are frugal though, so shop at aldi, phone of giff gaff, no particularly expensive hobbies etc.

Our base budget is £1500 a month. There is usually some left over.

The issue is you can easily spend a lot of money if you dont think about it so you have to keep on top of your spending.

I think the main thing people dont realise is just how much they are taxed at work and the cost to go to work!

Someone on 40k a year thinks jeez I can only just survive on 40k so I need a pension income of more!

When in reality they are only getting 30k a year after tax. Lose another £5k on the cost to get to work and suddenly your 40k is actually 25.

Just my 2ps worth.

You may even end up feeling better off than when you were working, with no mortgage or pension contributions coming out.

DoubleSix said:

There is average in the technical, national sense. And “average” in the sense of ones peer group and personal aspirations.

I don’t think the OP should be castigated for his perspective, rather, it says to me he realises he could be earning more and has a sense of self worth that is commendable.

To flip that, those who believe they are “achieving” by earning above the national average have set themselves a very low bar.

I actually agree 100% that it's good to be proactive and thinking about this stuff in your 30's I know I wish I had given it more thought.I don’t think the OP should be castigated for his perspective, rather, it says to me he realises he could be earning more and has a sense of self worth that is commendable.

To flip that, those who believe they are “achieving” by earning above the national average have set themselves a very low bar.

I shouldn't have been a dick about it.

Take the age at which you start contributing properly to a pension and halve it. This is the pension contribution percentage you should be making. That's supposedly the rule of thumb anyway.

Interesting that people are funneling large percentages into pensions to avoid paying any higher rate whatsoever. I considered doing that myself thinking it was probably quite an unusual thing to do but decided that it seemed a bit like cutting my nose off to spite my face. The game I'm playing is trying to keep my higher rate tax amount at a fraction of the base rate amount. Such games are only going to get more painful with inflation and Hunt having put tax bands in the deep freeze. As to people running in the red due to their pension contributions

P.S. For the interest of the OP, I am 33, I've been putting in since I was 22 ensuring that I got the free money. In the past few years I have increased my contributions and my employee and I are now contributing a combined 15%. The pot is probably £50k. I hope I'm beating the curve but my situation is pretty much par according to the pension company's retirement calculator

Interesting that people are funneling large percentages into pensions to avoid paying any higher rate whatsoever. I considered doing that myself thinking it was probably quite an unusual thing to do but decided that it seemed a bit like cutting my nose off to spite my face. The game I'm playing is trying to keep my higher rate tax amount at a fraction of the base rate amount. Such games are only going to get more painful with inflation and Hunt having put tax bands in the deep freeze. As to people running in the red due to their pension contributions

P.S. For the interest of the OP, I am 33, I've been putting in since I was 22 ensuring that I got the free money. In the past few years I have increased my contributions and my employee and I are now contributing a combined 15%. The pot is probably £50k. I hope I'm beating the curve but my situation is pretty much par according to the pension company's retirement calculator

Edited by HustleRussell on Friday 17th March 12:28

nickfrog said:

alock said:

Up your contributions so you stop paying 40% tax

This!!Super Sonic said:

DoubleSix said:

There is average in the technical, national sense. And “average” in the sense of ones peer group and personal aspirations.

I don’t think the OP should be castigated for his perspective, rather, it says to me he realises he could be earning more and has a sense of self worth that is commendable.

To flip that, those who believe they are “achieving” by earning above the national average have set themselves a very low bar.

So 'average' in the real actual sense as everyone else understands it, and 'average' as in what the op thinks he's worth. Maybe he should 'work more hours' or 'get a better paid job'I don’t think the OP should be castigated for his perspective, rather, it says to me he realises he could be earning more and has a sense of self worth that is commendable.

To flip that, those who believe they are “achieving” by earning above the national average have set themselves a very low bar.

As for perspective, maybe he should spend a day volunteering at the CAB.

Do you think anyone who owns property in London gives a fig about national house prices?? Statistics can be used to argue any position you like, or even fool yourself if you wish...

We are a diverse nation and personally, when my career was in its ascendency (20's, 30's) I don't ever recall looking at national averages as a gauge of my own success. Far more sensible to look at those that had similar opportunities to myself, lived/worked in similar geography and had equivalent support networks. Only then could I gauge if I was over or underachieving.

Boo-urns said:

TwigtheWonderkid said:

100%. If you're on £62500, of the £12500 over £50K, you're only receiving £7500. Pay the £12500 into your pension, and you get it all. That's a 66.6% increase on your on your investment straight away, forgetting about future growth. Not bad when you'd do well to get 4% in a savings account.

True, but at the same time it's important to consider how useful you'd find that money now. £7,500 is a lot of money, even if you'd be netting £12,500 into your pension instead.In most cases this is a shrewd move, but once it's in your pension pot, it's gone until you're 55 with no chance of getting it back without incurring heavy penalties.

57 minimum for OP, probably later by the time he gets there. But if he can live happily without it, it's a no brainer.

HustleRussell said:

As to people running in the red due to their pension contributions

Depends on their situation. I've got money in a GIA that I'd rather not have generating CGT and dividend tax liability. If I increase my salary sacrifice to the point I am selling down that GIA to eat, I get more money overall, pay less tax and reduce my future tax liability. What's not to like?I am actually in a very privileged position to now be earning within the 60% tax bracket from April. I will now be upping the contribution on my pension to bring my pay back below the 100k mark to avoid the additional tax trap (I have been informed this will be seen as a salary sacrifice so HRMC will see me below the self assessment threshold). However, I would not move it down any lower because I need to enjoy some of the fruits of my labour now. What is the point entirely saving a for future that I may not see aIl? It is a fine balance for sure and kudos to the those who are better at financial planning and harder nosed at tax avoidance.

Gassing Station | Finance | Top of Page | What's New | My Stuff