Rubbish investment period? October '21 present

Discussion

Similar tale of woe here.

Sold a BTL in June 21 and started dripping lumps into funds and shares then, by December 21 thought I had the Midas touch as was +9%.

I’d say overall I’m down 20%, particularly poor buys were Scottish Mortgage and various other Baillie Gifford funds, Smithson and IM Opportunities.

Vanguard portfolio is +4%.

Sold a BTL in June 21 and started dripping lumps into funds and shares then, by December 21 thought I had the Midas touch as was +9%.

I’d say overall I’m down 20%, particularly poor buys were Scottish Mortgage and various other Baillie Gifford funds, Smithson and IM Opportunities.

Vanguard portfolio is +4%.

I also started in 2021. I have mine spread over 4 pots and each one is currently slightly down. I'm not looking to do anything with the funds for another 10 - 15 years so not too worried. I've been up and down but still progressing with topping up each month. Just have to trust the process.

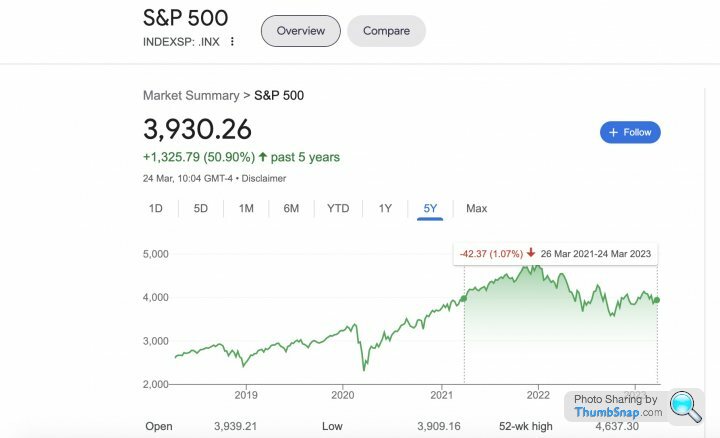

S&P500 Fun fact for the day -

Yesterday was the 3yr anniversary of the Covid crash market low. Today the S&P500 is up approx 75% since that market low. All of that gain was in the first year - so for 2yrs on a nett basis the 500 has gone nowhere. But, on a 5yr span the 500 is up +10% on an annualised basis... which tells us stocks and markets are for the long term. Not short-term frothy peaks.

Takeaway - If investing for the long term zoom out and ignore the short term noise.

Yesterday was the 3yr anniversary of the Covid crash market low. Today the S&P500 is up approx 75% since that market low. All of that gain was in the first year - so for 2yrs on a nett basis the 500 has gone nowhere. But, on a 5yr span the 500 is up +10% on an annualised basis... which tells us stocks and markets are for the long term. Not short-term frothy peaks.

Takeaway - If investing for the long term zoom out and ignore the short term noise.

SteveStrange said:

Agreed Phooey, but it's part of my daily ritual to check the balances/rises/falls/bigger falls at 6pm once the US stock markets have had a chance to do their worst, and it's a bit soul-destroying. I should ignore the charts for a year and then see where we are

I did exactly that. Lost 4%I ignored one pension pot for six years. Lost 3%

Flooble said:

SteveStrange said:

Agreed Phooey, but it's part of my daily ritual to check the balances/rises/falls/bigger falls at 6pm once the US stock markets have had a chance to do their worst, and it's a bit soul-destroying. I should ignore the charts for a year and then see where we are

I did exactly that. Lost 4%I ignored one pension pot for six years. Lost 3%

SteveStrange said:

Flooble said:

SteveStrange said:

Agreed Phooey, but it's part of my daily ritual to check the balances/rises/falls/bigger falls at 6pm once the US stock markets have had a chance to do their worst, and it's a bit soul-destroying. I should ignore the charts for a year and then see where we are

I did exactly that. Lost 4%I ignored one pension pot for six years. Lost 3%

Phooey said:

S&P500 Fun fact for the day -

Yesterday was the 3yr anniversary of the Covid crash market low. Today the S&P500 is up approx 75% since that market low. All of that gain was in the first year - so for 2yrs on a nett basis the 500 has gone nowhere. But, on a 5yr span the 500 is up +10% on an annualised basis... which tells us stocks and markets are for the long term. Not short-term frothy peaks.

Takeaway - If investing for the long term zoom out and ignore the short term noise.

S&P is up ~16% over the last two years. Yesterday was the 3yr anniversary of the Covid crash market low. Today the S&P500 is up approx 75% since that market low. All of that gain was in the first year - so for 2yrs on a nett basis the 500 has gone nowhere. But, on a 5yr span the 500 is up +10% on an annualised basis... which tells us stocks and markets are for the long term. Not short-term frothy peaks.

Takeaway - If investing for the long term zoom out and ignore the short term noise.

PM3 said:

Ah, but if one is ( me for example ) a British based retail investor ,,,,,,and correct for GBP/USD ....... the S&P in effect is up something like that ?

For example look at HSBC S&P 500 UCITS ETF (HSPX.L)

Yup, but that's not what DC said. I said on a "nett basis". Instead DC applied one of his normal condescending one-liner remarks, which was wrong, on a 'nett' basis.For example look at HSBC S&P 500 UCITS ETF (HSPX.L)

Phooey said:

PM3 said:

Ah, but if one is ( me for example ) a British based retail investor ,,,,,,and correct for GBP/USD ....... the S&P in effect is up something like that ?

For example look at HSBC S&P 500 UCITS ETF (HSPX.L)

Yup, but that's not what DC said. I said on a "nett basis". Instead DC applied one of his normal condescending one-liner remarks, which was wrong, on a 'nett' basis.For example look at HSBC S&P 500 UCITS ETF (HSPX.L)

I guess it depends whether you put a chunk of cash in in late 2021, or have been dripping it in monthly. If it’s monthly investments, you should have done OK due to the effect of dollar (or pound) cost averaging. If a lump sum, then bad luck on the timing. If an existing portfolio, you probably did well on it previously and if you wait it will almost certainly recover

Of course, it’s not just what the portfolio has lost, it’s also what it could have been expected to gain over the period of the slump

Of course, it’s not just what the portfolio has lost, it’s also what it could have been expected to gain over the period of the slump

PM3 said:

Phooey said:

Ah, but if one is ( me for example ) a British based retail investor ,,,,,,and correct for GBP/USD ....... the S&P in effect is up something like that ?For example look at HSBC S&P 500 UCITS ETF (HSPX.L)

1. In GBP

2. On a total return basis (i.e. dividends included)

Anything else tends to be confusing/misleading, IMO.

Just got some paperwork through for a Santander ISA I took out decades ago.

Looking good Nov 2021. Has lost 15 percent as of Nov 2022

As has been said earlier, ISAs and such are for long term but it's judging when long term has been enough.

Hindsight says, if only I cashed it back then, but even if I cash in today, it's still done ok, not brilliantly but ok.

I dare not look at what it's worth today.

Never had online access to it.

ETA just looked online.

Up 2% since that 15% drop, woo hoo.

Looking good Nov 2021. Has lost 15 percent as of Nov 2022

As has been said earlier, ISAs and such are for long term but it's judging when long term has been enough.

Hindsight says, if only I cashed it back then, but even if I cash in today, it's still done ok, not brilliantly but ok.

I dare not look at what it's worth today.

Never had online access to it.

ETA just looked online.

Up 2% since that 15% drop, woo hoo.

Edited by croyde on Saturday 25th March 09:05

I don’t know why people get surprised by these things, all you need is a few of the world indexes on your stock app that is on every smart phone and you’ll easily know roughly what is going on in the world.

I’ve mostly bought into index funds and also Fundsmith at what feels like ‘the lows’ by luck - it’s looking likely that this latest dip will possibly coincide quite nicely with the new ISA year. That said it gets harder to convince my wife we should be investing all our spare cash when the “it’ll come good” line hasn’t turned out to be true so far

Ultimately if you’re worried about any of this then don’t ever look at that you pension is invested in…

I’ve mostly bought into index funds and also Fundsmith at what feels like ‘the lows’ by luck - it’s looking likely that this latest dip will possibly coincide quite nicely with the new ISA year. That said it gets harder to convince my wife we should be investing all our spare cash when the “it’ll come good” line hasn’t turned out to be true so far

Ultimately if you’re worried about any of this then don’t ever look at that you pension is invested in…

My dad said to me in 2015 when I came back from an overseas assignment- "Take some of that money you've earned, buy Barclays and Lloyds shares... mark my words rodders, this time next year you'll be 20% up"

They have only twice been valued at a figure equal to that which I invested in the past 7.5 years, and even then only fleetingly.

Rightly or wrongly I have just rebalanced and bought more and similar, in a probably misguided effort to jailbreak that dead money and at least scrape even (let's not talk about inflation)

Also a lump sum and ongoing direct debits into a Vanguard 100% equity fund.

I suppose I'm betting on some upside.

They have only twice been valued at a figure equal to that which I invested in the past 7.5 years, and even then only fleetingly.

Rightly or wrongly I have just rebalanced and bought more and similar, in a probably misguided effort to jailbreak that dead money and at least scrape even (let's not talk about inflation)

Also a lump sum and ongoing direct debits into a Vanguard 100% equity fund.

I suppose I'm betting on some upside.

Gassing Station | Finance | Top of Page | What's New | My Stuff