Home Insurance contents question - Outbuilding defintion

Discussion

Equus said:

Ham_and_Jam said:

The first word is ‘Garages’.

Read on, MacDuff..."Garages, stables and other fixed animal housing, greenhouses, sheds, fixed outside stores and summer houses and other similar structures and their fixtures and fittings, detached from the private residence, all used for domestic purposes, and business purposes we have agreed, at the address shown in your policy schedule."

Watching with interest.

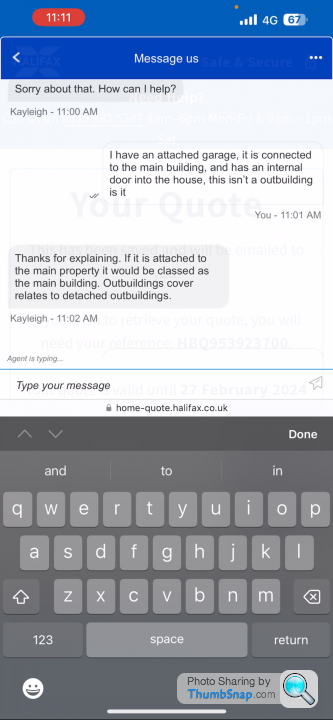

We have an attached garage, linked to the house by an original single story brick build corridor.

Every time car fumes get through to the kitchen, I am great full that the attached nature makes contents insurance much easier.

I have little to suggest, other than to show them their own documents and tell them to cough up!

Sheepshanks said:

nigelpugh7 said:

Sure here you go, as you can see it’s quite ambiguous relating to outbuildings.

I don't think it's ambiguous - it's just giving an example of an outbuilding. It doesn't mean (in any normal interpretation) that all garages are outbuildings.

It's absolutely clear that an integral garage, in everyday English, is not an outbuilding. In order to make an integral garage an outbuilding, they would have to say "we class all garages automatically as outbuildings".

TwigtheWonderkid said:

That's my take on it.

It's absolutely clear that an integral garage, in everyday English, is not an outbuilding. In order to make an integral garage an outbuilding, they would have to say "we class all garages automatically as outbuildings".

Or even: "we class garages as outbuildings". It's absolutely clear that an integral garage, in everyday English, is not an outbuilding. In order to make an integral garage an outbuilding, they would have to say "we class all garages automatically as outbuildings".

Sorry for not updating this thread, a lot has been going on relating to this claim.

We had an email, then a call from the gentleman at the ombudsman.

The upshot is the ombudsman agree that the terms in the policy were ambiguous and that the Halifax changed terms relating to a garage and outbuilding in the policy without expressly informing us as the policy holder that it would have a material change to any subsequent claim in the future.

The ombudsman have now instructed Halifax to revisit the claim and process the contents claim in full as our garage is an integral part of the house and any claims should be covered by the main contents policy and not have any individual limit, apart form single high value items not listed separately on the policy.

So I think we can say that this is a win in our case.

It also goes to prove that you really should stand by something if your belief is that the judgment is simply, not right and that you are prepared to stand firm and fight your case.

We had an email, then a call from the gentleman at the ombudsman.

The upshot is the ombudsman agree that the terms in the policy were ambiguous and that the Halifax changed terms relating to a garage and outbuilding in the policy without expressly informing us as the policy holder that it would have a material change to any subsequent claim in the future.

The ombudsman have now instructed Halifax to revisit the claim and process the contents claim in full as our garage is an integral part of the house and any claims should be covered by the main contents policy and not have any individual limit, apart form single high value items not listed separately on the policy.

So I think we can say that this is a win in our case.

It also goes to prove that you really should stand by something if your belief is that the judgment is simply, not right and that you are prepared to stand firm and fight your case.

nigelpugh7 said:

Sorry for not updating this thread, a lot has been going on relating to this claim.

We had an email, then a call from the gentleman at the ombudsman.

The upshot is the ombudsman agree that the terms in the policy were ambiguous and that the Halifax changed terms relating to a garage and outbuilding in the policy without expressly informing us as the policy holder that it would have a material change to any subsequent claim in the future.

The ombudsman have now instructed Halifax to revisit the claim and process the contents claim in full as our garage is an integral part of the house and any claims should be covered by the main contents policy and not have any individual limit, apart form single high value items not listed separately on the policy.

So I think we can say that this is a win in our case.

It also goes to prove that you really should stand by something if your belief is that the judgment is simply, not right and that you are prepared to stand firm and fight your case.

That's brilliant news and well done We had an email, then a call from the gentleman at the ombudsman.

The upshot is the ombudsman agree that the terms in the policy were ambiguous and that the Halifax changed terms relating to a garage and outbuilding in the policy without expressly informing us as the policy holder that it would have a material change to any subsequent claim in the future.

The ombudsman have now instructed Halifax to revisit the claim and process the contents claim in full as our garage is an integral part of the house and any claims should be covered by the main contents policy and not have any individual limit, apart form single high value items not listed separately on the policy.

So I think we can say that this is a win in our case.

It also goes to prove that you really should stand by something if your belief is that the judgment is simply, not right and that you are prepared to stand firm and fight your case.

I secretly thought you had little chance with this as I found it hard to believe that such a large organisation would make such a cock-up and would surely have the 'legals' pouring over any change in contracts prior to releasing them

KTMsm said:

Great - although I can't believe the insurer didn't cave before as it's pretty obvious that an outbuilding can't be integral !

That’s what they always do apparently, just respond with they have made a decision and that is final.I suppose a lot of people would have just said well that that then, and accepted the £5K settlement figure.

Good job we are not those type of people!

dickymint said:

That's brilliant news and well done

I secretly thought you had little chance with this as I found it hard to believe that such a large organisation would make such a cock-up and would surely have the 'legals' pouring over any change in contracts prior to releasing them

Which again is what we all assume when it comes to huge companies like this, but as we have witnessed here, it’s simply not always the case.I secretly thought you had little chance with this as I found it hard to believe that such a large organisation would make such a cock-up and would surely have the 'legals' pouring over any change in contracts prior to releasing them

When the claim is complete and settled in full I will share some of the ombudsman’s findings, as it makes for interesting reading.

nigelpugh7 said:

K87 said:

Good result.

Let’s wait to see what they actually decide they will pay out on before we crack open the champagne!usn90 said:

I’m slightly confused, what terms change was the OP not informed about?

I thought their whole argument was a classed as an outbuilding, integral or not.

The ombudsman picked up on the fact that the definition of both a garage and an outbuilding was specifically changed in several versions of our policy over several years.I thought their whole argument was a classed as an outbuilding, integral or not.

Gassing Station | Homes, Gardens and DIY | Top of Page | What's New | My Stuff