Home Insurance contents question - Outbuilding defintion

Discussion

Ham_and_Jam said:

The first word is ‘Garages’.

Read on, MacDuff..."Garages, stables and other fixed animal housing, greenhouses, sheds, fixed outside stores and summer houses and other similar structures and their fixtures and fittings, detached from the private residence, all used for domestic purposes, and business purposes we have agreed, at the address shown in your policy schedule."

Ham_and_Jam said:

Not sure if this is a relevant to your specific policy, but page 46 of their latest poilcy booket defines Outbuildings.

The first word is ‘Garages’.

https://www.halifax.co.uk/assets/pdf/insurance/pdf...

But it says that Outbuildings are 'detached' from the main property and the OP has said that his garages are not detached.The first word is ‘Garages’.

https://www.halifax.co.uk/assets/pdf/insurance/pdf...

I think you have misunderstood. Detached garages along with sheds etc are provided with the same cover as the main house (with integral garage)

If he had two garages one attached to the house the other elsewhere in the grounds they would have the same cover in terms of contents that were stored in them.

Personally I am surprised that insurers have provided this cover without a sublimit given that garages often have such poor locks and non standard construction.

If he had two garages one attached to the house the other elsewhere in the grounds they would have the same cover in terms of contents that were stored in them.

Personally I am surprised that insurers have provided this cover without a sublimit given that garages often have such poor locks and non standard construction.

CharlesElliott said:

But it says that Outbuildings are 'detached' from the main property and the OP has said that his garages are not detached.

It also says outbuildings are covered, so I think the OP is all good. Loss adjustors are often independent and work on behalf of, but not for, the insurance co, so it's possible he is mistaken, and it is up to Halifax to suggest what the solution is. Ham_and_Jam said:

Not sure if this is a relevant to your specific policy, but page 46 of their latest poilcy booket defines Outbuildings.

The first word is ‘Garages’.

https://www.halifax.co.uk/assets/pdf/insurance/pdf...

The 25th word is ‘detached’ The first word is ‘Garages’.

https://www.halifax.co.uk/assets/pdf/insurance/pdf...

ovlovlover said:

Apologies for butting in but out of interest does anyone have seperate outbuildings insurance or recommend a company who provide?

Always thought about this and the OPs bad luck reminded me.

NFU are hard to beat. Fantastic service and no quibble cover, but you do pay for it!Always thought about this and the OPs bad luck reminded me.

fourstardan said:

Is there over 5k of contents gone? Feels to be quite generous for a garage tbh.

I would tend to agree that £5K is quite generous if it was just used to store just a few items such a car cleaning items etc.However as they are two large garages we have used them as additional storage areas for a manner of items.

These include my Roll Top Cabinet full of Snap on and Wera tools.

5 of my 1/8 RC race cars, two of which are Serpent 977 and Team X-Ray both with Nova Rossi race engines, which are about £1500 minimum each to replace.

Then there were other larger items such as my Hyundai Electric Start petrol generator, another item that cost over £1000.

Then there are three mountain bicycles, two Cannondales and one Specialized full suspension, and my Scott Foil Carbon road bike with Shimano DI2 Ultegra group set, which on its own will cost about £10000 to replace, the mountain bikes perhaps about £5000 to replace.

The other large item that that was not on a separate insurance policy was my Montesa Cota 4RT 2021 Trial motorcycle which was completely destroyed.

That too would cost around £7000 to replace.

Just doing a quick spreadsheet to add those items up they come to around £30000.

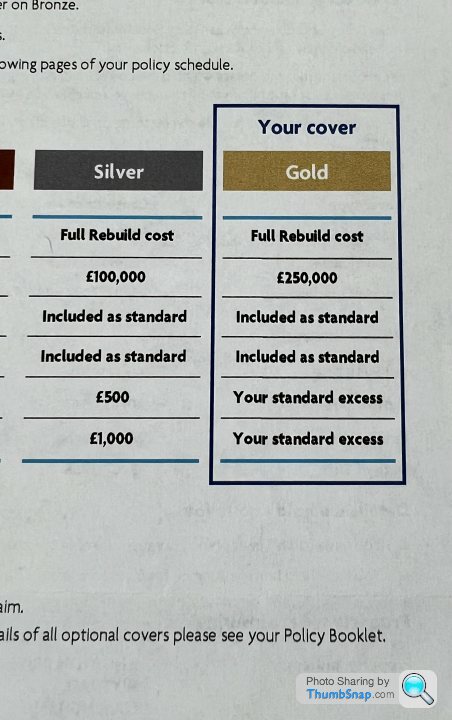

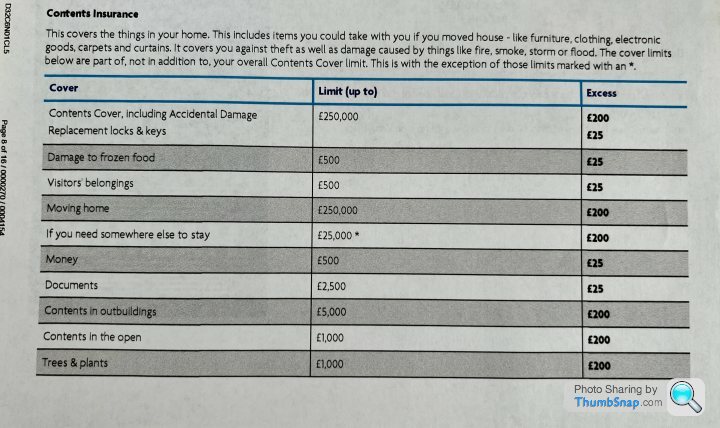

Some might say that’s a lot of moneys worth of items to have in a garage without a separate specific insurance policy to cover those specific items, but as we have Gold level cover that covers £250’000 worth of contents we felt that should be more than sufficient cover.

Here’s what’s left of my trials bike.

Ask them to define an outbuilding, you're not going to get a definite answer on here. It could easily be that an outbuilding is any room or building with its own entrance, in which case the garage would be an outbuilding, or that an outbuilding is any building separate to the house, in which case its probably not an outbuilding.

Fwiw a dictionary definition is "a smaller separate building such as a shed or barn that belongs to a main building, such as a house or farm." Suggesting you could argue the garage is not an outbuilding.

Fwiw a dictionary definition is "a smaller separate building such as a shed or barn that belongs to a main building, such as a house or farm." Suggesting you could argue the garage is not an outbuilding.

Note the bold, as its a policy definition, as below..

However..

You would have needed the bike & model cars with seperate individual listings/specified items, this is normally 2/3k (I cant find it on the PDF posted above), or separate cover.

Other items they should pay if they are outside of the what we don't cover section.

Also you might want to check if 250k contents cover is actually enough, its probably not, and if 'underinsured' they could ratchet down a claim.

Nb, edit, they also have a separate pedal bike section/cover. check your policy schedule for pedal cover.

Good luck.

Edited by Deesee on Thursday 31st August 09:18

Page 46 of the above policy states

Outbuildings

Garages, stables and other fixed animal housing, greenhouses, sheds, fixed outside stores and summer houses and other similar structures and their fixtures and fittings, detached from the private residence,

Many year ago I had 2 bikes stolen from an internal garage, insurance paid out no problem as it was part of the dwelling.

First question the police asked was is there a door from the garage into the house. Yes. This escalated it to a one hour response as it was classed as theft from the home rather than an outbuilding.

Outbuildings

Garages, stables and other fixed animal housing, greenhouses, sheds, fixed outside stores and summer houses and other similar structures and their fixtures and fittings, detached from the private residence,

Many year ago I had 2 bikes stolen from an internal garage, insurance paid out no problem as it was part of the dwelling.

First question the police asked was is there a door from the garage into the house. Yes. This escalated it to a one hour response as it was classed as theft from the home rather than an outbuilding.

Condi said:

Ask them to define an outbuilding, you're not going to get a definite answer on here. It could easily be that an outbuilding is any room or building with its own entrance, in which case the garage would be an outbuilding, or that an outbuilding is any building separate to the house, in which case its probably not an outbuilding.

Fwiw a dictionary definition is "a smaller separate building such as a shed or barn that belongs to a main building, such as a house or farm." Suggesting you could argue the garage is not an outbuilding.

Thanks bud, yes we have requested that as part of our formal complaint, still not had a reply on that one though. Fwiw a dictionary definition is "a smaller separate building such as a shed or barn that belongs to a main building, such as a house or farm." Suggesting you could argue the garage is not an outbuilding.

Deesee said:

Note the bold, as its a policy definition, as below..

However..

You would have needed the bike & model cars with seperate individual listings/specified items, this is normally 2/3k (I cant find it on the PDF posted above), or separate cover.

Other items they should pay if they are outside of the what we don't cover section.

Also you might want to check if 250k contents cover is actually enough, its probably not, and if 'underinsured' they could ratchet down a claim.

Nb, edit, they also have a separate pedal bike section/cover. check your policy schedule for pedal cover.

Good luck.

Edited by Deesee on Thursday 31st August 09:18

We have done exactly the same, but can’t help feeling that those to paragraphs effectively contradict themselves?

We know now about having to list items of value above £2000 as separate items to be covered, have to be honest never spotted that before and as a result we never added any items.

And of course the range of high value items I own that are in the garage would have probably have doubled or perhaps tripled the annual premium, but with hindsight it would of course been prudent to do so.

nigelpugh7 said:

Deesee said:

Note the bold, as its a policy definition, as below..

However..

You would have needed the bike & model cars with seperate individual listings/specified items, this is normally 2/3k (I cant find it on the PDF posted above), or separate cover.

Other items they should pay if they are outside of the what we don't cover section.

Also you might want to check if 250k contents cover is actually enough, its probably not, and if 'underinsured' they could ratchet down a claim.

Nb, edit, they also have a separate pedal bike section/cover. check your policy schedule for pedal cover.

Good luck.

Edited by Deesee on Thursday 31st August 09:18

We have done exactly the same, but can’t help feeling that those to paragraphs effectively contradict themselves?

We know now about having to list items of value above £2000 as separate items to be covered, have to be honest never spotted that before and as a result we never added any items.

And of course the range of high value items I own that are in the garage would have probably have doubled or perhaps tripled the annual premium, but with hindsight it would of course been prudent to do so.

Either way the tools and other goods (not including the excluded in picture 3, motor bike/pedal bikes etc) will be in excess of 5k, and they have incorrectly assessed your claim on their own definitions.

Deesee said:

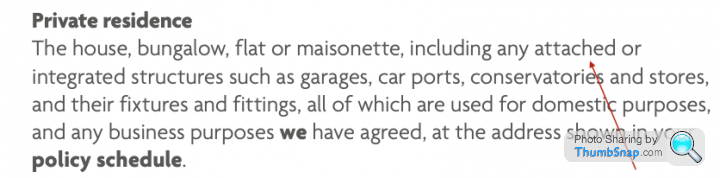

No problem, their definition takes you from outbuilding to private residence (second picture fits your description of the property), your tools will be covered, the motorised stuff won't, and you would have needed additional pedal bike cover (and this id say would have been needed to be specified as the values) this will be your schedule if you have opted for it.

Either way the tools and other goods (not including the excluded in picture 3, motor bike/pedal bikes etc) will be in excess of 5k, and they have incorrectly assessed your claim on their own definitions.

Yes the fact that they have incorrectly assessed the claim, or more importantly the loss adjuster who came to asses the damage did not adequately assess the extent of the damage.Either way the tools and other goods (not including the excluded in picture 3, motor bike/pedal bikes etc) will be in excess of 5k, and they have incorrectly assessed your claim on their own definitions.

Remember Halifax insure the contents, so items inside the house/dwelling as a whole.

The loss adjuster did not even look in the loft space, which is above the one garage, but this also extends to another loft above the utility, and the loft was also used to store a range of items some of them quite valuable.

The whole of the loft and utility area was hosed down by the fire brigade as they used heat sensing equipment to detect areas that still showed signs of heat.

In the Utility itself are electrical items such as Washing Machine, Tumble dryer and Microwave, all of which were contaminated with smoke damage and then water damage from the fire hoses.

The loss adjuster did not even look at or ask about those items, or look at any other parts of the house which has smoke damage.

We understand that most of the smoke damage will be covered by the buidings insurance, and indeed the other loss adjuster that came on behalf of RSA was very thorough, and went through the house room by toom, taking notes and pictures of every area that had visible smoke damage, and even areas that were not so visibly damaged.

As mentioned earlier it was apparent that the contents loss adjuster had predetermined that it was only the two garages that were affected, and had also pre decided that the only cover they were going to offer was the £5K just for the outbuildings.

This will be the main area we will contest to ensure that we are able to claim for exactly what was damaged in the fire as part of the contents cover for the shoot of the house.

Dog Star said:

K87 said:

I have just downloaded and read the current LV buildings and contents policy, this may be a different wording than 2014.

They cover contents at the home at the address in the schedule together with the contents in the outbuildings and garage.

They don't differentiate between an integral garage and free standing.

That’s very annoying! I cannot tell you how depressing it is when they pull the old “ah, unfortunately your cover….” I lost thousands of pounds worth of tools which took years to replace, bit by bit. They cover contents at the home at the address in the schedule together with the contents in the outbuildings and garage.

They don't differentiate between an integral garage and free standing.

I might investigate them upon renewal next year - I’ve never had cover in excess of the current 2.5k per outbuilding that current insurers Aviva offer. Mrs DS would be happy too - currently all my cordless Makita stuff (there’s a lot) and more expensive items are stacked in the dining room where they’re covered. Ironically my garage is now a lot more secure than the house - it’s like a fortress.

nigelpugh7 said:

Yes the fact that they have incorrectly assessed the claim, or more importantly the loss adjuster who came to asses the damage did not adequately assess the extent of the damage.

Remember Halifax insure the contents, so items inside the house/dwelling as a whole.

The loss adjuster did not even look in the loft space, which is above the one garage, but this also extends to another loft above the utility, and the loft was also used to store a range of items some of them quite valuable.

The whole of the loft and utility area was hosed down by the fire brigade as they used heat sensing equipment to detect areas that still showed signs of heat.

In the Utility itself are electrical items such as Washing Machine, Tumble dryer and Microwave, all of which were contaminated with smoke damage and then water damage from the fire hoses.

The loss adjuster did not even look at or ask about those items, or look at any other parts of the house which has smoke damage.

We understand that most of the smoke damage will be covered by the buidings insurance, and indeed the other loss adjuster that came on behalf of RSA was very thorough, and went through the house room by toom, taking notes and pictures of every area that had visible smoke damage, and even areas that were not so visibly damaged.

As mentioned earlier it was apparent that the contents loss adjuster had predetermined that it was only the two garages that were affected, and had also pre decided that the only cover they were going to offer was the £5K just for the outbuildings.

This will be the main area we will contest to ensure that we are able to claim for exactly what was damaged in the fire as part of the contents cover for the shoot of the house.

I with you 100% on this, they have used an incorrect way of assigning and assessing your claim.. thats totally not fair, has put you in a worse position as well as creating additional stress, its certainly not treating customers fairly.Remember Halifax insure the contents, so items inside the house/dwelling as a whole.

The loss adjuster did not even look in the loft space, which is above the one garage, but this also extends to another loft above the utility, and the loft was also used to store a range of items some of them quite valuable.

The whole of the loft and utility area was hosed down by the fire brigade as they used heat sensing equipment to detect areas that still showed signs of heat.

In the Utility itself are electrical items such as Washing Machine, Tumble dryer and Microwave, all of which were contaminated with smoke damage and then water damage from the fire hoses.

The loss adjuster did not even look at or ask about those items, or look at any other parts of the house which has smoke damage.

We understand that most of the smoke damage will be covered by the buidings insurance, and indeed the other loss adjuster that came on behalf of RSA was very thorough, and went through the house room by toom, taking notes and pictures of every area that had visible smoke damage, and even areas that were not so visibly damaged.

As mentioned earlier it was apparent that the contents loss adjuster had predetermined that it was only the two garages that were affected, and had also pre decided that the only cover they were going to offer was the £5K just for the outbuildings.

This will be the main area we will contest to ensure that we are able to claim for exactly what was damaged in the fire as part of the contents cover for the shoot of the house.

You'll need to itemise these goods/valuables, pictures, and perhaps receipts/bank transactions/ebay statements etc.

Thankfully it sound like everyone is safe, and well, stuff can be replaced.

Is it worth appointing a loss assessor? Even retrospectively to deal with the 'grey areas' that may appear between the buildings and contents, and help with the complaint with the contents?

Deesee said:

I with you 100% on this, they have used an incorrect way of assigning and assessing your claim.. thats totally not fair, has put you in a worse position as well as creating additional stress, its certainly not treating customers fairly.

You'll need to itemise these goods/valuables, pictures, and perhaps receipts/bank transactions/ebay statements etc.

Thankfully it sound like everyone is safe, and well, stuff can be replaced.

Is it worth appointing a loss assessor? Even retrospectively to deal with the 'grey areas' that may appear between the buildings and contents, and help with the complaint with the contents?

Yes the main point is as you say that the everyone is safe, it might have been a very much worse outcome if my daughter had not been still awake at 2AM in the morning and heard what she thought was somone trying to break into the garage, which we now know was actually all the aerosols I had in the garage for bike maintenance etc going pop.You'll need to itemise these goods/valuables, pictures, and perhaps receipts/bank transactions/ebay statements etc.

Thankfully it sound like everyone is safe, and well, stuff can be replaced.

Is it worth appointing a loss assessor? Even retrospectively to deal with the 'grey areas' that may appear between the buildings and contents, and help with the complaint with the contents?

We actually had a Loss Assessor attend just a few days ago, it was his advice that we reject the offer and contest what the loss adjuster was saying regarding the garage being classed as an outbuilding.

He also told us it was not worth his company taking on the case, as the total claim was likely to be less than £100K which seems to be the minimum amount they use as a starting point to justify them taking on such a claim.

I think he mentioned that they charge 30% of any claim as their fee, so it would need to be £100m claim to get a £30K fee.

I suppose the very word is the clue, an outbuilding is outwith the main house, I.e. Away from the house.

Lawinsider defines an outbuilding as a building away from the house, possibly a garage or a shed.

The Loss Adjuster is wrong. You should receive a formal offer letter, this should be repudiated.

Lawinsider defines an outbuilding as a building away from the house, possibly a garage or a shed.

The Loss Adjuster is wrong. You should receive a formal offer letter, this should be repudiated.

Edited by K87 on Thursday 31st August 14:19

K87 said:

I suppose the very word is the clue, an outbuilding is outwith the main house, I.e. Away from the house.

And as I pointed out above, the word 'building' implies a single structure, whether or not that structure incorporates multiple compartments, uses or occupations.

We have a different word for a seperate storage use attached to a building: it's called an 'outshut'.

Gassing Station | Homes, Gardens and DIY | Top of Page | What's New | My Stuff