Home Insurance contents question - Outbuilding defintion

Discussion

K87 said:

It will be interesting to see the outcome.

Especially if the contents of a garage are to be treated as house contents and therefore are they subject to the same terms and conditions, for example protected by locks to a certain standard and covered by the alarm system.

My garage just has tools and car detailing stuff, a bicycle, suitcases and ladders, £5000 would be enough but after the loss if I was asked to prove what I owned by receipts then I would be lost, perhaps some pics would be a good idea.

We had an independent specialist loss adjuster visit to assess the damage and estimate the claim.Especially if the contents of a garage are to be treated as house contents and therefore are they subject to the same terms and conditions, for example protected by locks to a certain standard and covered by the alarm system.

My garage just has tools and car detailing stuff, a bicycle, suitcases and ladders, £5000 would be enough but after the loss if I was asked to prove what I owned by receipts then I would be lost, perhaps some pics would be a good idea.

He took one look in both of the garages, and when he noticed my roll can with all the Snap on Tools and Wera tools he knew it was going to be a bigger claim than £5000.

He also told us that his company would not take it on as it had to be a claim of at least £50000 as they work on commission and their fees are 25%, so he said it would not be with them engaging.

He also believed there was no way an integral garage would be classed as an outbuilding, and as we had £250K of contents insurance we should be well covered.

He commented that most people have a lot of stuff that’s worth a lot of money in their garages, and when you do have to make a list of what was lost to the fire and start adding it all up to produce a shopping list of what you need to buy the final bill surprised most people.

Unlike the loss adjuster from Halifax, he also spent time looking at the other rooms in the house that suffered smoke damage, and told us the term we should use in relation to getting items like chairs and tables replaced by the contents insurance was “ Contaminated “ as once an item is smoke damaged it can never be properly cleaned and made as new again, so is therefore classed as contaminated and requires replacement.

nigelpugh7 said:

K87 said:

It will be interesting to see the outcome.

Especially if the contents of a garage are to be treated as house contents and therefore are they subject to the same terms and conditions, for example protected by locks to a certain standard and covered by the alarm system.

My garage just has tools and car detailing stuff, a bicycle, suitcases and ladders, £5000 would be enough but after the loss if I was asked to prove what I owned by receipts then I would be lost, perhaps some pics would be a good idea.

We had an independent specialist loss adjuster visit to assess the damage and estimate the claim.Especially if the contents of a garage are to be treated as house contents and therefore are they subject to the same terms and conditions, for example protected by locks to a certain standard and covered by the alarm system.

My garage just has tools and car detailing stuff, a bicycle, suitcases and ladders, £5000 would be enough but after the loss if I was asked to prove what I owned by receipts then I would be lost, perhaps some pics would be a good idea.

He took one look in both of the garages, and when he noticed my roll can with all the Snap on Tools and Wera tools he knew it was going to be a bigger claim than £5000.

He also told us that his company would not take it on as it had to be a claim of at least £50000 as they work on commission and their fees are 25%, so he said it would not be with them engaging.

He also believed there was no way an integral garage would be classed as an outbuilding, and as we had £250K of contents insurance we should be well covered.

He commented that most people have a lot of stuff that’s worth a lot of money in their garages, and when you do have to make a list of what was lost to the fire and start adding it all up to produce a shopping list of what you need to buy the final bill surprised most people.

Unlike the loss adjuster from Halifax, he also spent time looking at the other rooms in the house that suffered smoke damage, and told us the term we should use in relation to getting items like chairs and tables replaced by the contents insurance was “ Contaminated “ as once an item is smoke damaged it can never be properly cleaned and made as new again, so is therefore classed as contaminated and requires replacement.

Your experience has been a learning curve for many of us, if for no other reason than the price of tools and equipment is so much more than when it was bought X years ago.

Good luck with your insurer and the Ombudsman. I think it is disappointing that someone who manages the claims at Halifax doesn't take a look at your situation and either sort it out and pay up or say to you, this is the reason why we are going to pay you £5000 and not a penny more, the seed for all this delay must lie with that individual who came to see you initially.

Good luck with the Ombudsman, sadly I've not heard good things of them lately, it seems they are swamped.

If all else fails, I would talk to somebody like Roger Flaxman at Flaxman and Partners, rather than employing a Loss Assessor or solicitor. All of their people are very experienced insurance people and good at this sort of issue.

If all else fails, I would talk to somebody like Roger Flaxman at Flaxman and Partners, rather than employing a Loss Assessor or solicitor. All of their people are very experienced insurance people and good at this sort of issue.

K87 said:

My garage just has tools and car detailing stuff, a bicycle, suitcases and ladders, £5000 would be enough but after the loss if I was asked to prove what I owned by receipts then I would be lost, perhaps some pics would be a good idea.

I had a theft claim from a large shed / workshopThey asked for receipts but I buy most of my stuff secondhand from ebay, FB etc and a lot of it I'd had for many years

I explained that and they accepted it - possibly because I wasn't claiming for a Rolex etc and it was my only theft claim in 20+ years

I now take occasional photos of what's in my garages / outbuildings because it's impossible to remember everything you had, until you come to use it

When they give new for old cover (as someone who buys used) the price builds up very quickly, whilst it might have cost me £5k (2 gang mowers, 3 chainsaws, 2 sit on mowers etc) to replace it with new would be closer to £25k

What a nightmare OP. This was something I'd been "afraid" of with insurance and why I shopped round after very very carefully reading the terms and conditions when renewing. Just between the milling machine, lathe and power tools I've probably got 5k worth in the garage before you start on other stuff!

Real downside is regardless of how it ends up, the trails bike I can't see being covered. Just about every insurer seems to have an exclusion for "motor vehicles" and makes no differentiation between road going and not (for example ours states "contents are not: • motor vehicles (including motorbikes, quad bikes and motorised scooters), caravans, trailers, watercraft, aircraft and all their accessories;"

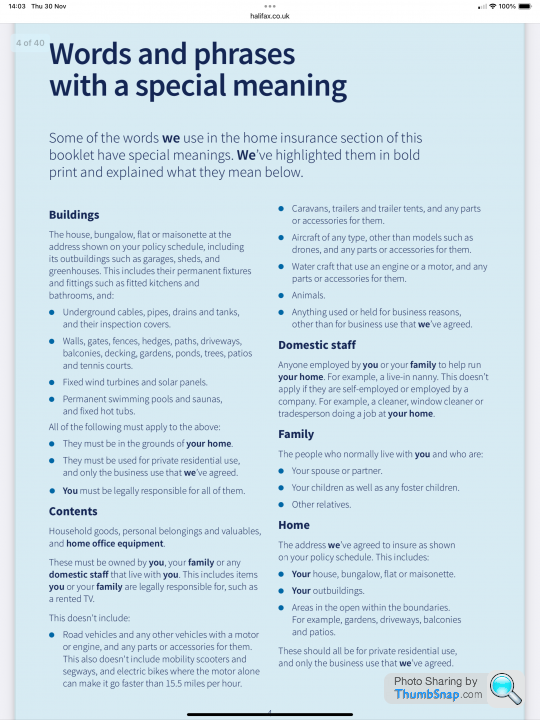

Then it defines the "home" as "the private property at the address shown on your personal details, together with its garages and outbuildings."

Of course that doesn't prevent the insurance company from being an arse and making up s t if it comes to a claim like they have in the OP's case!

t if it comes to a claim like they have in the OP's case!

Real downside is regardless of how it ends up, the trails bike I can't see being covered. Just about every insurer seems to have an exclusion for "motor vehicles" and makes no differentiation between road going and not (for example ours states "contents are not: • motor vehicles (including motorbikes, quad bikes and motorised scooters), caravans, trailers, watercraft, aircraft and all their accessories;"

Dog Star said:

Perhaps relevant to your claim, OP.

We had our detached, brick garage burgled in 2014. We had unlimited contents cover.

Insurance - who were about to pay out on the huge amount of stuff that was stolen - clocked this and my claim was knocked back to £2k, the max that could be paid for outbuilding contents.

I was told, at the time, that if my garage had been integral (as yours is) that the claim would have been settled in full. Integral = attached to main house. That was with LV=.

Interesting I presume they've changed since (as we're currently with LV=) because currently they make *no* mention of outbuildings being separate. Either as a specific separate Policy Limit or being considered different *anywhere* within the policy documentation. Its why we went with them as they define "Contents" as "contents are the following property belonging to you or your family or which you or your family are legally responsible for when inside your home:"We had our detached, brick garage burgled in 2014. We had unlimited contents cover.

Insurance - who were about to pay out on the huge amount of stuff that was stolen - clocked this and my claim was knocked back to £2k, the max that could be paid for outbuilding contents.

I was told, at the time, that if my garage had been integral (as yours is) that the claim would have been settled in full. Integral = attached to main house. That was with LV=.

Then it defines the "home" as "the private property at the address shown on your personal details, together with its garages and outbuildings."

Of course that doesn't prevent the insurance company from being an arse and making up s

t if it comes to a claim like they have in the OP's case!cayman-black said:

Not sure if the answer is in this thread but shouldn't the trial bike have its own insurance?

It was mentioned earlier, but trials bike insurance is very hard to get, lots of places say they offer it, but then insist that the bike is road registered and has an imobilser fitted which due to the nature of a trials bike is next to impossible!Then in addition most companies that do offer insurance it’s mostly for theft only, accidental damage, which includes fire damage is almost always not even offered on the policy.

Fastdruid said:

Interesting I presume they've changed since (as we're currently with LV=) because currently they make *no* mention of outbuildings being separate. Either as a specific separate Policy Limit or being considered different *anywhere* within the policy documentation. Its why we went with them as they define "Contents" as "contents are the following property belonging to you or your family or which you or your family are legally responsible for when inside your home:"

Then it defines the "home" as "the private property at the address shown on your personal details, together with its garages and outbuildings."

Of course that doesn't prevent the insurance company from being an arse and making up st if it comes to a claim like they have in the OP's case!

Thanks for that note bud, and yes we know that the trials bike won’t be covered under the home contents policy, I’ve sort of become resigned to the fact it wasn’t covered, and have manage to rebuild it back to full operating condition for not a lot of outlay on the few things that needed to be replaced to get it running again. Then it defines the "home" as "the private property at the address shown on your personal details, together with its garages and outbuildings."

Of course that doesn't prevent the insurance company from being an arse and making up s

t if it comes to a claim like they have in the OP's case!Of course not had the time at the weekends to ride it anyway as most time has been consumed doing other garage related stuff!

Still something to look forward to in the new year!

usn90 said:

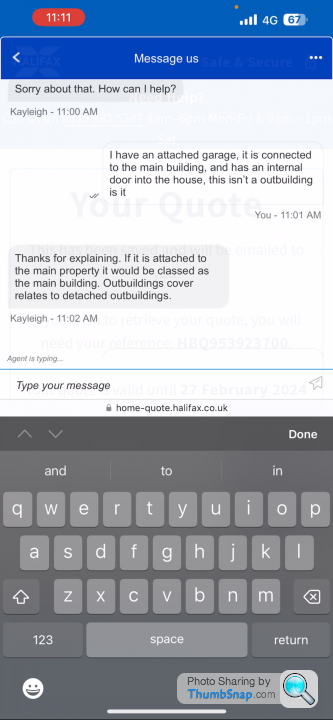

I’ve just been onto Halifax regarding my renewal, they confirmed an attached garage, is not classed as an outbuilding

That’s fantastic, and thanks for sharing.Now we need to try and get Halifax to agree to confirm the same regarding our own policy.

Need to try and figure out the best way to try and achieve that without them getting wind of it of course!

Fastdruid said:

What a nightmare OP. This was something I'd been "afraid" of with insurance and why I shopped round after very very carefully reading the terms and conditions when renewing. Just between the milling machine, lathe and power tools I've probably got 5k worth in the garage before you start on other stuff!

Things get iffy if the tools are considered "trade", rather than normal DIY stuff.Car parts too - they were excluded for the container insurance I took out to store my garage contents while our house was being extended.

Edited by Sheepshanks on Wednesday 29th November 15:33

Sheepshanks said:

Fastdruid said:

What a nightmare OP. This was something I'd been "afraid" of with insurance and why I shopped round after very very carefully reading the terms and conditions when renewing. Just between the milling machine, lathe and power tools I've probably got 5k worth in the garage before you start on other stuff!

Things get iffy if the tools are considered "trade", rather than normal DIY stuff.That's then when the insurance companies making stuff as they go along becomes a problem. Because I could totally see them arguing that it's "industrial machinery" or something stupid. Which it kind of is but not related to any business (which is the only type of reasonable exclusion in the policy) and equally its common for such stuff to be owned for hobbies after its long outlived its "industrial" life.

Same for some of the IT kit I have, ex-enterprise stuff, even second hand it's pricy but its not what most people would have round the house.

Sheepshanks said:

Car parts too - they were excluded for the container insurance I took out to store my garage contents while our house was being extended.

Yeah, Unfortunately there doesn't really seem to be many policies that will cover such without paying an absolute fortune (and they'll still probably try and get out of it if you ever claim). I have a load of spare bike parts that I've just had to accept it's not economic to insure. Again less from theft so much as fire.

K87 said:

Its a lesson for us all, we all would prefer to pay the lowest premium and not many of us actually read the proposed wording to see how it would work for our particular circumstances.

Not really - I think 90% of people could accurately describe what an "outbuilding" is, it's just his insurer is in the 10% that can't !I do hope the OP gets it sorted out, i feel that it's such a shame you have to go through all of this to get a resolve.

I have a few large outbuildings one of which is a full blown workshop, 2 ramps, welders, machine tools the whole 9 yards, it's been my life dream and it's my world. Once it was built i realised that our existing insurance would not cover it, i had seen the "outbuilding" clause.

I had a hard time trying to get cover as it more akin to a commercial set up than a domestic, in the end my brooker found a policy, but still i wanted it in writing that i was covered, the only thing they wanted from me was assurance i was not using it for business or in connection with my business.

Getting a policy is the easy bit, making sure that it will pay out in the event is the hard bit !

I have a few large outbuildings one of which is a full blown workshop, 2 ramps, welders, machine tools the whole 9 yards, it's been my life dream and it's my world. Once it was built i realised that our existing insurance would not cover it, i had seen the "outbuilding" clause.

I had a hard time trying to get cover as it more akin to a commercial set up than a domestic, in the end my brooker found a policy, but still i wanted it in writing that i was covered, the only thing they wanted from me was assurance i was not using it for business or in connection with my business.

Getting a policy is the easy bit, making sure that it will pay out in the event is the hard bit !

nigelpugh7 said:

In particular it is the part that refers to outbuildings and states that a garage is an outbuilding.There is no definition anywhere in the policy document or the schedule relating to an integral garage such as the ones we have at our home.

Gassing Station | Homes, Gardens and DIY | Top of Page | What's New | My Stuff