Retire early (living off savings)

Discussion

Hang On said:

You really need to get a statement for her and be sure. If she does have missing years you can buy some of them and the rate of return is very high. (Buy a year for circa £700 and get more than £200 per year for life). The reduced rates to buy her earlier years will expire next year so don't wait to decide what to do.

Great info many Tks dingg said:

Best check that as my wife hasn't worked much but qualifies for full pension due to credit of nic for when the kids were being brought up.

anyway in similar vein for this thread

my plan is to retire either this year or next - take my 25% from my pension pot and sell up in the uk move to somewhere where its possible to drawdown almost my whole pot over 10 years tax free, after gaining residence there , that should release circa 50k a year , with about 100-150k left in the pot when I return to uk , I shall re-invest 20k a year in the wife's isa (which is currently quite healthy) , out of the 50k I drawdown (she will keep uk residency to enable this to happen)

after the 10 years are up myself and wife both will be able to obtain our OAP in the uk ,having paid (or been exempted from) enough contributions already, I will be still able to drawdown a small pension from my remaining pension pot (hopefully) which should give us a decent amount free of tax , and a quite healthy sum tax free from the wife's isa pot , we also would need to use some of this pot to purchase another property back in the uk.

its a no brainer as far as I can see , as long as I can legitimately avoid the tax and get a more relaxed lifestyle earlier and a holiday home at the end of it thrown in for free as I see it - man maths wins here!

just need steadyish returns from the stock market and have a good buffer (which we have) if it all goes wrong for a year or two , so I'm happy with the risk/reward

so were off in september house hunting

ETA - the big risk here is the wife falling out with me and running off with the pot/poolman

Interesting thoughts.anyway in similar vein for this thread

my plan is to retire either this year or next - take my 25% from my pension pot and sell up in the uk move to somewhere where its possible to drawdown almost my whole pot over 10 years tax free, after gaining residence there , that should release circa 50k a year , with about 100-150k left in the pot when I return to uk , I shall re-invest 20k a year in the wife's isa (which is currently quite healthy) , out of the 50k I drawdown (she will keep uk residency to enable this to happen)

after the 10 years are up myself and wife both will be able to obtain our OAP in the uk ,having paid (or been exempted from) enough contributions already, I will be still able to drawdown a small pension from my remaining pension pot (hopefully) which should give us a decent amount free of tax , and a quite healthy sum tax free from the wife's isa pot , we also would need to use some of this pot to purchase another property back in the uk.

its a no brainer as far as I can see , as long as I can legitimately avoid the tax and get a more relaxed lifestyle earlier and a holiday home at the end of it thrown in for free as I see it - man maths wins here!

just need steadyish returns from the stock market and have a good buffer (which we have) if it all goes wrong for a year or two , so I'm happy with the risk/reward

so were off in september house hunting

Edited by dingg on Sunday 21st January 10:48

ETA - the big risk here is the wife falling out with me and running off with the pot/poolman

Edited by dingg on Sunday 21st January 11:21

Out of interest where would you be looking at getting residency ?

Would you give up U.K residency or can you keep both ?

Is it as easy as move abroad and drawdown your pension paying no tax on money that the U.K. has given tax breaks over the years ?

No concerns on house price changes over the 10 years you are out of the country ?

Unsure how this works so just curious, sounds ideal but just don’t see that it can be that easy.

Edited by tighnamara on Sunday 21st January 16:37

tighnamara said:

Interesting thoughts.

Out of interest where would you be looking at getting residency ? Portugal - nhr status

Would you give up U.K residency or can you keep both ? yes give up uk , can't be resident in 2 places at once

Is it as easy as move abroad and drawdown your pension paying no tax on money that the U.K. has given tax breaks over the years ? yes completely legal at the minute

No concerns on house price changes over the 10 years you are out of the country ? no I expect portugal to rise further than uk

Unsure how this works so just curious, sounds ideal but just don’t see that it can be that easy. some hoops to be jumped through but all legal and above board at the moment - gut feeling says the door will close at some stage so going for it before it does

Out of interest where would you be looking at getting residency ? Portugal - nhr status

Would you give up U.K residency or can you keep both ? yes give up uk , can't be resident in 2 places at once

Is it as easy as move abroad and drawdown your pension paying no tax on money that the U.K. has given tax breaks over the years ? yes completely legal at the minute

No concerns on house price changes over the 10 years you are out of the country ? no I expect portugal to rise further than uk

Unsure how this works so just curious, sounds ideal but just don’t see that it can be that easy. some hoops to be jumped through but all legal and above board at the moment - gut feeling says the door will close at some stage so going for it before it does

Edited by tighnamara on Sunday 21st January 16:37

tighnamara said:

Interesting thoughts.

Out of interest where would you be looking at getting residency ?

Would you give up U.K residency or can you keep both ?

Is it as easy as move abroad and drawdown your pension paying no tax on money that the U.K. has given tax breaks over the years ?

No concerns on house price changes over the 10 years you are out of the country ?

Unsure how this works so just curious, sounds ideal but just don’t see that it can be that easy.

For countries with which the UK has a tax treaty you will find in most a cases a parallel agreement to the effect that if the pension is taken as a draw-down that tax will be owed in the then current country of residence whereas if the pension is taken as a 100% lump sum it will be taxed in the country where the pension was origInally accumulated.Out of interest where would you be looking at getting residency ?

Would you give up U.K residency or can you keep both ?

Is it as easy as move abroad and drawdown your pension paying no tax on money that the U.K. has given tax breaks over the years ?

No concerns on house price changes over the 10 years you are out of the country ?

Unsure how this works so just curious, sounds ideal but just don’t see that it can be that easy.

Edited by tighnamara on Sunday 21st January 16:37

I've begun. Got off my @rse and started the process. Opted for a Vanguard product as it seems pretty flexible and was easy to understand. I can double dip a bit too, as the tax year flips in a couple of months, so I can spread the risk even further, satisfying my inner anti-risk self.

Smitters said:

I've begun. Got off my @rse and started the process. Opted for a Vanguard product as it seems pretty flexible and was easy to understand. I can double dip a bit too, as the tax year flips in a couple of months, so I can spread the risk even further, satisfying my inner anti-risk self.

You reduce risk by diversification...you don't spread it.Smitters said:

I've begun. Got off my @rse and started the process. Opted for a Vanguard product as it seems pretty flexible and was easy to understand. I can double dip a bit too, as the tax year flips in a couple of months, so I can spread the risk even further, satisfying my inner anti-risk self.

ISA with the LifeStrategy fund? I'm going to be doing this too - as I'm 55 this year I'll go either 20 or possibly 40 whereas I assume you will be looking at 80 or 100 at your age. xeny said:

garyhun said:

ISA with the LifeStrategy fund? I'm going to be doing this too - as I'm 55 this year I'll go either 20 or possibly 40 whereas I assume you will be looking at 80 or 100 at your age.

If you're 55, can you not do it via a SIPP and get some income tax back? Although I suppose I can do £3600 pa so yes.Edit to add: So that's £2880 I can pay into a SIPP (grossing up to £3600 with the tax relief) and the rest into ISA. Thanks for the reminder.

Edited by anonymous-user on Monday 22 January 14:34

garyhun said:

Smitters said:

I've begun. Got off my @rse and started the process. Opted for a Vanguard product as it seems pretty flexible and was easy to understand. I can double dip a bit too, as the tax year flips in a couple of months, so I can spread the risk even further, satisfying my inner anti-risk self.

ISA with the LifeStrategy fund? I'm going to be doing this too - as I'm 55 this year I'll go either 20 or possibly 40 whereas I assume you will be looking at 80 or 100 at your age. I'm now in the slightly more involved process of assessing the household spending, getting some big wins (utilities), finding some repeatable savings and working out how much more I can save each month. I'm not very good at saving without doing it on payday, so I'm planning to save via standing order as close to payday as possible into the various mechanisms and then see if my bank will do a variable payment the day before payday to reduce the account balance to a set level (say £100), so I also save at the back end. Anyone else do this?

garyhun said:

Jimboka said:

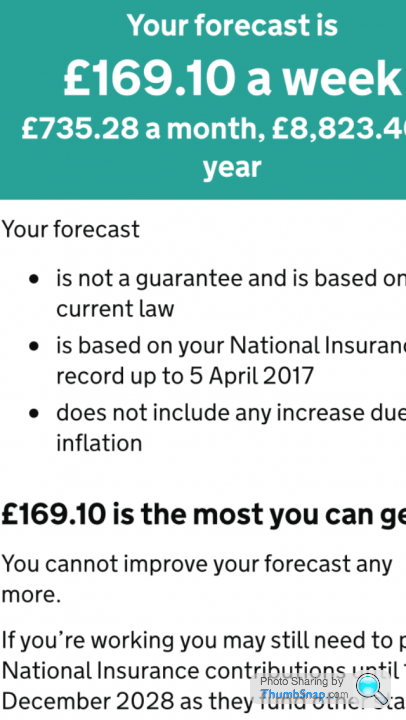

I wonder if someone can clarify something please on state pension summary?

Mine says

From 2028 my state pension forecast is £169.10 a week

£169.19 is the most I can get

40 years of full contributions

Then

You’ve been in a contracted-out pension scheme

COPE estimate £54.83 a week

Google says that state pension will be £169

Google also says £169-£54

Who is right please ?!

Be interested to know exactly what you googled!Mine says

From 2028 my state pension forecast is £169.10 a week

£169.19 is the most I can get

40 years of full contributions

Then

You’ve been in a contracted-out pension scheme

COPE estimate £54.83 a week

Google says that state pension will be £169

Google also says £169-£54

Who is right please ?!

The maximum state pension is currently £159.55 so not sure where £169 comes from.

The COPE estimate is basically saying ‘this is what you would have got if you had stayed contracted-in’ and assumes you probably should get at least this from the private pension you invested your contracted-out contributions in.

Smitters said:

I'm not very good at saving without doing it on payday, so I'm planning to save via standing order as close to payday as possible into the various mechanisms and then see if my bank will do a variable payment the day before payday to reduce the account balance to a set level (say £100), so I also save at the back end. Anyone else do this?

Never heard of this, but I would be interested to hear what they say when you ask.Robbo 27 said:

Cotty said:

Never heard of this, but I would be interested to hear what they say when you ask.

I have asked my bank, Yorkshire, if they would do this and the answer was no, also asked First Direct and they couldnt do it either.garyhun said:

I assume you have additional ‘non contracted out’ years as well which makes up the difference from £159.

Edited to replace ? with 9.

No. He must have accrued 'additional state pension' under the old system and as such his carry-in entitlement in April 2016 was higher than the amount under the new rule. One always starts with the higher of old system vs new system and so long as that remains greater that's what you get in retirement. I could be wrong but I don't think the starting amount is inflation adjusted in this case so should the new state pension finally exceed £169, he would get the new one instead.Edited to replace ? with 9.

Edited by garyhun on Friday 26th January 12:18

Hang On said:

garyhun said:

I assume you have additional ‘non contracted out’ years as well which makes up the difference from £159.

Edited to replace ? with 9.

No. He must have accrued 'additional state pension' under the old system and as such his carry-in entitlement in April 2016 was higher than the amount under the new rule. One always starts with the higher of old system vs new system and so long as that remains greater that's what you get in retirement. I could be wrong but I don't think the starting amount is inflation adjusted in this case so should the new state pension finally exceed £169, he would get the new one instead.Edited to replace ? with 9.

Edited by anonymous-user on Friday 26th January 12:18

Gassing Station | The Lounge | Top of Page | What's New | My Stuff