PCP deal calculation help

Discussion

daemon said:

Bloody hell. Thats a good price!

I might have missed out the inlays and red calipers but I doubt they will add much to cost. Didn't realise the S3 comes with option for LED headlights though! Tempted but should be happy with the Xenon Plus.

dealer quoted spec said:

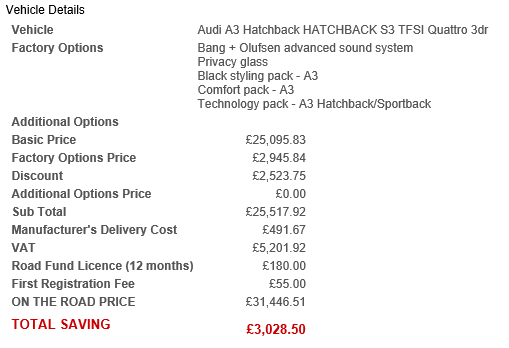

S3 3 door 6 speed manual in Panther black

Bang & Olufsen

Black styling package

Technology package with Audi connect

Comfort package

Privacy glass

Red brake calipers

Black inlays

Bang & Olufsen

Black styling package

Technology package with Audi connect

Comfort package

Privacy glass

Red brake calipers

Black inlays

Edited by crazy about cars on Tuesday 16th December 19:04

crazy about cars said:

At the moment I am comfortable putting in £5,000 deposit and £380/month for 3 years. I might but car outright but what I will do is negotiate to go onto another PCP deal.

The last quote at list price I believe the final cost of purchase at 7.2% apr was £42,000 which I'm definitely not comfortable with.

I reckon if discounted to £31,000 I should be able to hit the target above.

What's the total cost to buy at £31k?The last quote at list price I believe the final cost of purchase at 7.2% apr was £42,000 which I'm definitely not comfortable with.

I reckon if discounted to £31,000 I should be able to hit the target above.

Grandfondo said:

What's the total cost to buy at £31k?

With same parameters I presume it's around £37k however I don't intend to buy it outright and also don't intend to put the full 13k into the PCP as deposit

Anyhow doubt they'll consider a £4.5k discount (£36k -> £31.5k) no matter how desperate they are

Edited by crazy about cars on Tuesday 16th December 19:16

crows said:

Sorry, couldn't let this go. I'm a bit late to the party myself too but I think you need to check your understanding of PCP deals, as the website is doing it correctly. With a PCP you are financing the depreciation of the vehicle. So if the total price is 50K, you put in a 10K deposit and the GFV is 20K that leaves (50-10-20) = 20K to be financed over the term. You don't finance the GFV as well.

You have to pay interest on the GFV, that's the point.daemon said:

+1

Also, PCP is not the way to finance a car if your aim is to own it. Use a straight HP deal for that.

PCP deals work best with smallish deposit, sensible repayments then either rinse and repeat or go and do something else next time.

]

Most people who PCP (if they are not rich( choose PCP because they cannot afford the HP payments !Also, PCP is not the way to finance a car if your aim is to own it. Use a straight HP deal for that.

PCP deals work best with smallish deposit, sensible repayments then either rinse and repeat or go and do something else next time.

]

Mandat said:

But isn't it the same with all methods of car purchase?

Even is someone buys the same new car outright for cash they will lose the £13k due to depreciation over the 3 years, and they will be left in a similar position as the PCP owner.

Also, no one is left with "NOTHING!!!" as you put it, since at the very least they will be left with the benefit of having had use of the car for the previous 3 years.

no because on a PCP as quoted a lot here you pay interest on the balloon as you never pay that off interest on a 40k car can easy be 10k worth.Even is someone buys the same new car outright for cash they will lose the £13k due to depreciation over the 3 years, and they will be left in a similar position as the PCP owner.

Also, no one is left with "NOTHING!!!" as you put it, since at the very least they will be left with the benefit of having had use of the car for the previous 3 years.

as for the OP on his quote he stands to loose way more than 13k was it more like £22k and still have to hand the car back !

Edited by mrdemon on Wednesday 17th December 09:14

crazy about cars said:

With same parameters I presume it's around £37k however I don't intend to buy it outright and also don't intend to put the full 13k into the PCP as deposit

Anyhow doubt they'll consider a £4.5k discount (£36k -> £31.5k) no matter how desperate they are

12% is about the max you can get. But at this time of year, just say 12% discount or no sale.Anyhow doubt they'll consider a £4.5k discount (£36k -> £31.5k) no matter how desperate they are

they are always desperate end of Dec

mrdemon said:

daemon said:

+1

Also, PCP is not the way to finance a car if your aim is to own it. Use a straight HP deal for that.

PCP deals work best with smallish deposit, sensible repayments then either rinse and repeat or go and do something else next time.

]

Most people who PCP (if they are not rich( choose PCP because they cannot afford the HP payments !Also, PCP is not the way to finance a car if your aim is to own it. Use a straight HP deal for that.

PCP deals work best with smallish deposit, sensible repayments then either rinse and repeat or go and do something else next time.

]

People who chose HP chose to do so because they plan on keeping the car a set period of time and are happy to rinse and repeat OR chose another method of payment next time.

They'll happily run a new car for three years, then chop it in for another.

They tend to have no particular desire to have a whole pile of equity tied up in a car.

ALSO, there are many many preferential PCP deals whereby the manufacturer is injecting "finance contributions" that you are unlikely to otherwise be able to get as discount.

A decent PCP deal will allow people to stick in a smallish amount up front (like a lease), have palatable monthly payments (like a lease) but give them the added flexibility of having options come end of term - such as trade the car back in and release any equity and thus avoiding any "unreasonable" demands that a lease company may levy. Also, you have rights under the Consumer Credit Act with a PCP deal that limits your exposure which you dont have with a lease - the lease company can pretty much demand all the remaining payments under a lease deal for example - whereas with a PCP deal you could hand the car back after 50% of the total amount payable has been made with nothing more to pay. OR you could trade the car in if your circumstances change and its a different type of car you need.

Come the end of term you are free to look at another PCP deal, take on an HP agreement or buy a car with cash.

IF its used correctly, and IF people understand the rules, it can be a reasonably cost efficient and controlled way of running a new car for a set period of time.

And for the avoidance of doubt i have no particular preference for PCP deals. Leasing has its merits, straight HP has its merits, buying with cash has its merits - all dependant on the car, the deals available and your own personal preference.

Dr Jekyll said:

crows said:

Sorry, couldn't let this go. I'm a bit late to the party myself too but I think you need to check your understanding of PCP deals, as the website is doing it correctly. With a PCP you are financing the depreciation of the vehicle. So if the total price is 50K, you put in a 10K deposit and the GFV is 20K that leaves (50-10-20) = 20K to be financed over the term. You don't finance the GFV as well.

You have to pay interest on the GFV, that's the point.Not uncommon for people to make this mistake.

With the way prices are rising on cars people seem to forget how much it actually is to borrow cash, prices go up but people want to spend 200quid a month still.

36 grand over 5 years with no interest is 600quid a month, chuck some interest in and its a lot of money a month for no offence an averagely priced car these days.

36 grand over 5 years with no interest is 600quid a month, chuck some interest in and its a lot of money a month for no offence an averagely priced car these days.

mrdemon said:

no because on a PCP as quoted a lot here you pay interest on the balloon as you never pay that off interest on a 40k car can easy be 10k worth.

£10,000 of interest on a £40K car purchases? :rotfl:BMW Z4 28i example, 3 years, 10K miles PA, £3,000 down, list price £37,390 -

Deposit (£3,000) + payments (£425*36) + residual (£14,580).

Total amount payable to OWN a car with a list price of £37,390 = £32,880.

Total cost to DRIVE the car for three years and hand it back = £18,300, which come to roughly 50% of the cars value which is roughly equal to the depreciation it will suffer anyway.

http://www.bmw.co.uk/en_GB/topics/owners/offers/z4...

mrdemon said:

as for the OP on his quote he stands to loose way more than 13k was it more like £22k and still have to hand the car back !

Yes, thats a bad deal. Wrong finance tool on the wrong car. I'd be leasing that of a Golf R for a fraction of that.After_Shock said:

With the way prices are rising on cars people seem to forget how much it actually is to borrow cash, prices go up but people want to spend 200quid a month still.

36 grand over 5 years with no interest is 600quid a month, chuck some interest in and its a lot of money a month for no offence an averagely priced car these days.

Thats why i think we'll see an even bigger move to PCP deals and then on to leasing.36 grand over 5 years with no interest is 600quid a month, chuck some interest in and its a lot of money a month for no offence an averagely priced car these days.

£32,000 for a Golf R hot hatch?

£25,000 for a Golf diesel?

£35,000 for a 2.0 litre diesel 5 series?

£40,000 for a 2.0 litre z4??

All just plain daft.

If you want a new car the de facto choice has to be a PCP or lease deal these days. I cant think of ANY reason why you'd want to put your own hard earned into run of the mill new cars these days.

mrdemon said:

Most people who PCP (if they are not rich) choose PCP because they cannot afford the HP payments !

crazy_about_cars - I suggest you keep all of your cash "on the hip" for the next 20 years and then see what it buys you (other than an aching hip). This also gives you the added benefit of being able to sneer at others using finance to buy (sorry, rent) their car.On the assumption you "can't afford to own the car" and, as stated a number of times, you have no real intention of keeping the car at the end of the term - Grandfondo's and mrdemon's advice is that you should always go for HP or a Personal loan even if the %APR on the PCP is lower. This saves you having to admit (oh no! the shame!) that you're "trapped" in a PCP'd car that "you can't afford to own". Hint: regardless of how the loan is structured (e.g. GFV) - APR's raison d'être is to allow like-for-like comparison; the %APR on the OP's S1 PCP is lower than Grandfondo's ~3.9% personal loan example.

Given we're in the realms of making sweeping statements without facts (e.g. specific deal details) - here's mine: PCP on a used car isn't a good idea (JetskiJezz - what was the %APR on your Porsche?). A manufacturer has no reason to incentivise the rate - when did you last see (e.g.) BBC News reporting on European used car sales (i.e. never)? Whilst there may(?) be more profit, at an individual dealer level, in used cars - as a manufacturer I'm fairly certain the number of new car sales is one of the key points the market judges you on. Continually shifting new cars is what PCPs are designed for. Although new cars or not, some manufacturers seem to have no problem shifting them and hence have (as far as I can tell) no reason to offer decent rates of finance - Porsche (via VWFS, I assume) is one such example.

mrdemon's and Grandfondo's points are mostly valid, although like others who hold prejudiced views - it can be hard to accept that their views aren't always correct. They also offer an insight into the PH absolutism fallacy which befalls many threads such as these. In this particular case "PCP's are always bad", "never use PCP" - when what they actually mean is "in my experience, of which may be limited or vast - I'll not quantify, PCP's aren't a good idea". Other PH examples being - insurance ("fully comp insurance allows you to drive any other car with third-party cover") or leasing ("pence per mile overages charges are for unlimited miles"). The common theme being that they're all based on contracts and, although there may be similarity between contracts, it is entirely down to the terms of the contract you sign that determines the options (or, not) that are available to you (VT point/%APR/etc).

PS: should you raise any future threads on car finance I'll be sure to pop in to labour the point that you “can't afford to own the car”. God forbid you sign up for the car and post in the Audi forum about your new purchase - I'll make sure I post in there nit picking at your use of the word "purchase" (YOU'RE ONLY RENTING/etc).

PPS: “you can't afford to own the car”. I'm (sometimes) a cash buyer - look at meeeee!

I've followed this thread with interest, but only had the time to post now.

I, too, was in a similar position to the OP in 2011: with a reasonably large deposit, hadn't done PCP before and interested in an S3. I read all the internet threads about PCP, various funding models, pricing and specs; but still - in hindsight - made an expensive error.

In my case, I agreed a PCP deal on a 9-month old S3 in a spec that wasn't quite perfect - but I was happy enough and probably blinded by the car itself and the excuses I made for needing a new motor. The S3 I ended-up with was a great car and I enjoyed driving it for 18 months, although it was too bling for my tastes.

Circumstances changed, though. A new job and its prohibitive "grey fleet" terms made it seem more economic to run a company car, which I duly did. I ended the S3's PCP and, because of the large deposit, was able to do so without a financial headache at the time. However, I did crystalise a five-figure loss.

To be clear, I would have paid that amount of money (and more) if I'd kept it longer. But I walked away with nothing but an empty wallet.

The irony was that the previous car (absolutely mint 5-year old A3 2.0T quattro with a great spec) was perfect and owed me nothing. I had part-funded the S3 using short-term savings, which I lost most of. I also have some more substantial long-term savings in addition to my pension pot, which could have been used...but let's not go there!!

When we eventually downsized to one car again (on the back of fewer work miles), I did not repeat the PCP route again. Obviously there are some amazing lease deals from time-to-time, but they won't put you in a positive position come the end of the contract.

I'm now driving a 6-year old Golf R32; the lower ownership costs of which will re-gain my S3's lost depreciation...if I keep it for another year or two. That's with a no-expenses spared approach too (see my thread).

I realise I've not gone into much detail and that this is all personal, but the lessons I've learnt are:

1) New and new-ish cars can be very poor VFM;

2) There is a level of VFM with cars that I am comfortable with, regardless of income, which I exceeded with the S3;

3) I will take a much longer, harder look at my existing car and why I'd want a new one when considering a change;

4) PCP is not a funding model I'd look at in preference again;

5) Longer-term ownership of a depreciation-minimised car costs me the least.

I, too, was in a similar position to the OP in 2011: with a reasonably large deposit, hadn't done PCP before and interested in an S3. I read all the internet threads about PCP, various funding models, pricing and specs; but still - in hindsight - made an expensive error.

In my case, I agreed a PCP deal on a 9-month old S3 in a spec that wasn't quite perfect - but I was happy enough and probably blinded by the car itself and the excuses I made for needing a new motor. The S3 I ended-up with was a great car and I enjoyed driving it for 18 months, although it was too bling for my tastes.

Circumstances changed, though. A new job and its prohibitive "grey fleet" terms made it seem more economic to run a company car, which I duly did. I ended the S3's PCP and, because of the large deposit, was able to do so without a financial headache at the time. However, I did crystalise a five-figure loss.

To be clear, I would have paid that amount of money (and more) if I'd kept it longer. But I walked away with nothing but an empty wallet.

The irony was that the previous car (absolutely mint 5-year old A3 2.0T quattro with a great spec) was perfect and owed me nothing. I had part-funded the S3 using short-term savings, which I lost most of. I also have some more substantial long-term savings in addition to my pension pot, which could have been used...but let's not go there!!

When we eventually downsized to one car again (on the back of fewer work miles), I did not repeat the PCP route again. Obviously there are some amazing lease deals from time-to-time, but they won't put you in a positive position come the end of the contract.

I'm now driving a 6-year old Golf R32; the lower ownership costs of which will re-gain my S3's lost depreciation...if I keep it for another year or two. That's with a no-expenses spared approach too (see my thread).

I realise I've not gone into much detail and that this is all personal, but the lessons I've learnt are:

1) New and new-ish cars can be very poor VFM;

2) There is a level of VFM with cars that I am comfortable with, regardless of income, which I exceeded with the S3;

3) I will take a much longer, harder look at my existing car and why I'd want a new one when considering a change;

4) PCP is not a funding model I'd look at in preference again;

5) Longer-term ownership of a depreciation-minimised car costs me the least.

jw673 said:

crazy_about_cars - I suggest you keep all of your cash "on the hip" for the next 20 years and then see what it buys you (other than an aching hip). This also gives you the added benefit of being able to sneer at others using finance to buy (sorry, rent) their car.

On the assumption you "can't afford to own the car" and, as stated a number of times, you have no real intention of keeping the car at the end of the term - Grandfondo's and mrdemon's advice is that you should always go for HP or a Personal loan even if the %APR on the PCP is lower. This saves you having to admit (oh no! the shame!) that you're "trapped" in a PCP'd car that "you can't afford to own". Hint: regardless of how the loan is structured (e.g. GFV) - APR's raison d'être is to allow like-for-like comparison; the %APR on the OP's S1 PCP is lower than Grandfondo's ~3.9% personal loan example.

Given we're in the realms of making sweeping statements without facts (e.g. specific deal details) - here's mine: PCP on a used car isn't a good idea (JetskiJezz - what was the %APR on your Porsche?). A manufacturer has no reason to

incentivise the rate - when did you last see (e.g.) BBC News reporting on European used car sales (i.e. never)? Whilst

there may(?) be more profit, at an individual dealer level, in used cars - as a manufacturer I'm fairly certain the number of new car sales is one of the key points the market judges you on. Continually shifting new cars is what PCPs are designed for. Although new cars or not, some manufacturers seem to have no problem shifting them and hence have (as far as I can tell) no reason to offer decent rates of finance - Porsche (via VWFS, I assume) is one such example.

mrdemon's and Grandfondo's points are mostly valid, although like others who hold prejudiced views - it can be hard to accept that their views aren't always correct. They also offer an insight into the PH absolutism fallacy which befallsmany threads such as these. In this particular case "PCP's are always bad", "never use PCP" - when what they actually mean is "in my experience, of which may be limited or vast - I'll not quantify, PCP's aren't a good idea". Other PH examples being - insurance ("fully comp insurance allows you to drive any other car with third-party cover") or leasing ("pence per mile overages charges are for unlimited miles"). The common theme being that they're all based on contracts

and, although there may be similarity between contracts, it is entirely down to the terms of the contract you sign that determines the options (or, not) that are available to you (VT point/%APR/etc

PS: should you raise any future threads on car finance I'll be sure to pop in to labour the point that you “can't afford to own the car”. God forbid you sign up for the car and post in the Audi forum about your new purchase - I'll make sure I post in there nit picking at your use of the word "purchase" (YOU'RE ONLY RENTING/etc).

PPS: “you can't afford to own the car”. I'm (sometimes) a cash buyer - look at meeeee!

When did the OP mention 0% on an S1?On the assumption you "can't afford to own the car" and, as stated a number of times, you have no real intention of keeping the car at the end of the term - Grandfondo's and mrdemon's advice is that you should always go for HP or a Personal loan even if the %APR on the PCP is lower. This saves you having to admit (oh no! the shame!) that you're "trapped" in a PCP'd car that "you can't afford to own". Hint: regardless of how the loan is structured (e.g. GFV) - APR's raison d'être is to allow like-for-like comparison; the %APR on the OP's S1 PCP is lower than Grandfondo's ~3.9% personal loan example.

Given we're in the realms of making sweeping statements without facts (e.g. specific deal details) - here's mine: PCP on a used car isn't a good idea (JetskiJezz - what was the %APR on your Porsche?). A manufacturer has no reason to

incentivise the rate - when did you last see (e.g.) BBC News reporting on European used car sales (i.e. never)? Whilst

there may(?) be more profit, at an individual dealer level, in used cars - as a manufacturer I'm fairly certain the number of new car sales is one of the key points the market judges you on. Continually shifting new cars is what PCPs are designed for. Although new cars or not, some manufacturers seem to have no problem shifting them and hence have (as far as I can tell) no reason to offer decent rates of finance - Porsche (via VWFS, I assume) is one such example.

mrdemon's and Grandfondo's points are mostly valid, although like others who hold prejudiced views - it can be hard to accept that their views aren't always correct. They also offer an insight into the PH absolutism fallacy which befallsmany threads such as these. In this particular case "PCP's are always bad", "never use PCP" - when what they actually mean is "in my experience, of which may be limited or vast - I'll not quantify, PCP's aren't a good idea". Other PH examples being - insurance ("fully comp insurance allows you to drive any other car with third-party cover") or leasing ("pence per mile overages charges are for unlimited miles"). The common theme being that they're all based on contracts

and, although there may be similarity between contracts, it is entirely down to the terms of the contract you sign that determines the options (or, not) that are available to you (VT point/%APR/etc

PS: should you raise any future threads on car finance I'll be sure to pop in to labour the point that you “can't afford to own the car”. God forbid you sign up for the car and post in the Audi forum about your new purchase - I'll make sure I post in there nit picking at your use of the word "purchase" (YOU'RE ONLY RENTING/etc).

PPS: “you can't afford to own the car”. I'm (sometimes) a cash buyer - look at meeeee!

Why do people get so het up about a statement of fact that does not concern them? Unless it does of course!

In you posts you just about mention every time that you deserve a medal for paying cash for a car and how you still could but go on to argue vehemently for PCP?

PCP certainly works for cars that can't be shifted and the manufacturer knows the only way to get them moving is to throw bundles of cash at the deal like the BMW Z4!

Merry Xmas.

Edited by Grandfondo on Wednesday 17th December 13:07

Grandfondo said:

When did the OP mention 0% on an S1?

He didn't and neither did I:crazy about cars said:

initial quote is correct but it's actually for an S1 - that was the first car I looked at and got offered PCP

jw673 said:

From the OP: £35,999 - £13,000 PX - GFV £13,798.75, 49M@£227.33

=~1.29% Flat/~2.58% APR, ~£493 Per Month over the term (incl. PX). If ignoring PX - ~£227 = ~£39 Interest & ~£188 Depreciation, per month.

I'm not arguing for or against PCP - and the medal/look at me comments, in case it isn't clear in the tone, are sarcastic. I think some people see car finance threads purely as a thinly veiled excuse to post their cash car purchasing superiority/snobbery, as opposed to answering the question being posed by the OP.=~1.29% Flat/~2.58% APR, ~£493 Per Month over the term (incl. PX). If ignoring PX - ~£227 = ~£39 Interest & ~£188 Depreciation, per month.

Grandfondo said:

Why do people get so het up about a statement of fact that does not concern them? Unless it does of course!

Because its such a banal comment, and often you use it in an inflammatory context that it needs correcting.It would be like me saying "SOME men ride bicycles because they like to see mens bottoms in front of them in lycra". To which you might (?) reply "I ride bicycles to keep fit and because I enjoy it", to which i would then go "Why do people get so het up about a statement of fact that does not concern them? Unless it does of course!"

And of course, i would then repeat that at every possible opportunity on every possible thread and the more people retorted to it, the more i would declare "Oh oh you're protesting too much!"

And why does it seem to matter to you so much IF people use PCP deals? Do you not understand that people have a range of options open to them and are very capable of chosing what suits them best?

Why must you try to broad brush all PCP deals?

You seem to think it makes you look smart - it doesnt - its cringeworthy.

Grandfondo said:

In you posts you just about mention every time that you deserve a medal for paying cash for a car and how you still could but go on to argue vehemently for PCP?

Just because he can see how on occassions a PCP deal may work for someone, doesnt mean its the ONLY tool he might use.Hes not arguing vehemently, hes giving a viewpoint.

Grandfondo said:

PCP certainly works for cars that can't be shifted and the manufacturer knows the only way to get them moving is to throw bundles of cash at the deal like the BMW Z4!

Yes. Exactly. The Z4 is reaching end of life now so they are having to support it on the market.Interestingly Mercedes are doing similar with the SLK.

Thats the trick with PCP deals - find the deals where the manufacturer is incentivising them.

Edited by daemon on Wednesday 17th December 18:02

Edited by daemon on Wednesday 17th December 18:05

jw673 said:

I'm not arguing for or against PCP - and the medal/look at me comments, in case it isn't clear in the tone, are sarcastic. I think some people see car finance threads purely as a thinly veiled excuse to post their cash car purchasing superiority/snobbery, as opposed to answering the question being posed by the OP.

+1And of course, being Pistonheads, everyone is a powerfully built company director who buys everything with cash.

Edited by daemon on Wednesday 17th December 18:02

Gassing Station | General Gassing | Top of Page | What's New | My Stuff