Are the wheels about to fall of car finance?

Discussion

TA14 said:

Granfondo said:

And in the immortal words of DUNCAN Banantyne I'AM OOT

Since I now know that you're a stickler for detail it's Bannatyne: https://www.bannatyne.co.uk/about-duncan-bannatynedjc206 said:

Ares said:

Unless early settlement has punitive penalties! Settlement figures in year one often have full term interest within.

You're entitled to withdraw from any financial product within the first 14 days without penalty are you not?....Although, as the car was then used, it would be worth even less, so buy it back and double save?

To settle finance, they would throw in admin charges and/or other costs. I've heard of interest being 100% front loaded, so the first £X,000 you may is all interest, hence why settlement figures in the first few months are often the full cost of the car.

Wills2 said:

Ares said:

Granfondo said:

TA14 said:

Brave Fart said:

2) suppose that £65k Alfa was available for £60k if bought outright, £65k on PCP - then you'd be better off buying. Even with a (say) 1.5% p.a. opportunity cost. Although I accept that the Alfa's used value after 4 years may be uncertain and that in itself might be reason to PCP.

Alfa values are not too dissimilar to other makes. A car that can be readily bought for £60K will be a £22K ish car after four years. Even if Ares was offered the car for £50K cash that's £28K depreciation plus £2K RFL = £30K vs £29K on PCP. It's an odd market place and Ares has simply found a very good deal via PCP.That's way cheaper than either a CP M3 or C63 both of which have far more support on them (discounts) than the QF presently has.

Rates are still very good, via brokers. M3/C63 were about the same when I looked, maybe £50/mth more. Not sure now.

Sample of current rates:

Ares said:

djc206 said:

Ares said:

Unless early settlement has punitive penalties! Settlement figures in year one often have full term interest within.

You're entitled to withdraw from any financial product within the first 14 days without penalty are you not?Ares said:

Yes. BMW was PCP, Alfa leased but incl VAT.

Rates are still very good, via brokers. M3/C63 were about the same when I looked, maybe £50/mth more. Not sure now.

Sample of current rates:

A great deal for a great car, looks really well in the pictures on your thread. Rates are still very good, via brokers. M3/C63 were about the same when I looked, maybe £50/mth more. Not sure now.

Sample of current rates:

I can't see how you could fund it better than how you have.

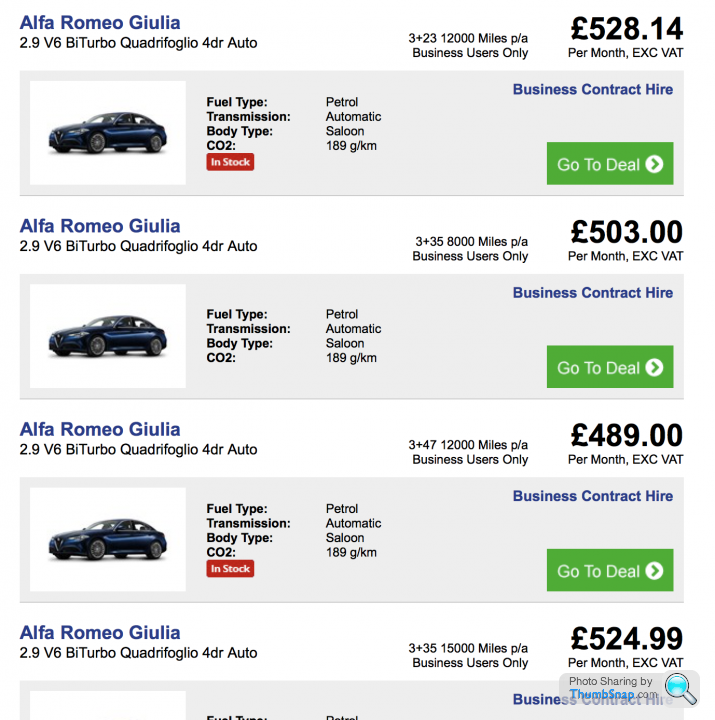

Can I ask the name of the provider on the image above, I'm quite interested at those rates.

PTF said:

Ares said:

I'm better off even without the return on capital. (But my investments are in a managed fund, primarily tracking the UK market, and are on very low risk profile). The points you make are relevant if factoring the opportunity cost as part of the saving.

The Alfa was available with £3250 off, given the spec I have. Half of which will be eaten up with the RFL. There is no way in hell a 4 year old, 60,000 mile Alfa will be worth £33k.

My 3yr 3mth old 640d (£74k list price, available at the time with £14500 discount) is currently worth £25-27k, even with the £5k Schnitzer performance kit and only 40,000 miles on the clock.

I reckon the Alfa will be close to, maybe under £20k at 4yrs/60,000miles. It will have lost over £40,000, c£840 per month. I'm paying c2/3rds of that?

Loving the man-maths.The Alfa was available with £3250 off, given the spec I have. Half of which will be eaten up with the RFL. There is no way in hell a 4 year old, 60,000 mile Alfa will be worth £33k.

My 3yr 3mth old 640d (£74k list price, available at the time with £14500 discount) is currently worth £25-27k, even with the £5k Schnitzer performance kit and only 40,000 miles on the clock.

I reckon the Alfa will be close to, maybe under £20k at 4yrs/60,000miles. It will have lost over £40,000, c£840 per month. I'm paying c2/3rds of that?

So comparing (a) pouring a large chunk of money away with (b) pouring an even larger chunk of money away, suddenly makes (a) seem like the sensible option.

Either way it's blowing somewhere approaching £1 per mile on a nice car. To argue that one is slightly better than the other is quite funny to observe as someone who really finds it hard to stomach even a £2k depreciation loss per year on a car.

All cars cost money. If depreciation is a dread worry, and you are happy to drive round in an old car (with the increased risks that brings), then thats great for you. But it doesn't make the maths wrong.

If you pay cash up front then get some cash back when you sell, the difference between the two is the cost - depreciation.

If you lease/PCP, you don't pay the full amount up front, but don't get anything (or much) back when you sell, but you pay a fixed monthly out going.

If depreciation over the term is greater than the total of the payments, you're better off with the fixed monthly cost. If you are sure the depreciation will be less than the total of the payments, then take the gamble and pay cash.

Simples, and the meerkats used to say

RSK21 said:

PTF said:

Loving the man-maths.

So comparing (a) pouring a large chunk of money away with (b) pouring an even larger chunk of money away, suddenly makes (a) seem like the sensible option.

Either way it's blowing somewhere approaching £1 per mile on a nice car. To argue that one is slightly better than the other is quite funny to observe as someone who really finds it hard to stomach even a £2k depreciation loss per year on a car.

Full circle as ever on these groundhog finance threads.So comparing (a) pouring a large chunk of money away with (b) pouring an even larger chunk of money away, suddenly makes (a) seem like the sensible option.

Either way it's blowing somewhere approaching £1 per mile on a nice car. To argue that one is slightly better than the other is quite funny to observe as someone who really finds it hard to stomach even a £2k depreciation loss per year on a car.

There's always a different/cheaper/better way to do things and If everybody thought the way you do there would be no new car market other than GT series Porsches and a few Ferraris.

Everybody's circumstances, financial position, needs, wants and desires are different.

I've little doubt Ares could buy the car outright if he wished to. His solution as outlined, for his circumstances is however a more cost effective one. Not aimed at you specifically but some people simply seem unable to grasp this thinking. Guess what ? He knows he's renting it, and that's all part of the plan.

PTF said:

TA14 said:

PTF said:

Either way it's blowing somewhere approaching £1 per mile on a nice car. To argue that one is slightly better than the other is quite funny to observe as someone who really finds it hard to stomach even a £2k depreciation loss per year on a car.

His maths isn't too bad though. 60,000 miles at £30,000 is 50p per mile.For a brand new, 500bhp Italian car, it is

Toltec said:

berlintaxi said:

PTF said:

Either way it's blowing somewhere approaching £1 per mile on a nice car. To argue that one is slightly better than the other is quite funny to observe as someone who really finds it hard to stomach even a £2k depreciation loss per year on a car.

But then it is all relative to what your disposable income is.berlintaxi said:

Ares said:

djc206 said:

Ares said:

Unless early settlement has punitive penalties! Settlement figures in year one often have full term interest within.

You're entitled to withdraw from any financial product within the first 14 days without penalty are you not?Ares said:

berlintaxi said:

Ares said:

djc206 said:

Ares said:

Unless early settlement has punitive penalties! Settlement figures in year one often have full term interest within.

You're entitled to withdraw from any financial product within the first 14 days without penalty are you not?Wills2 said:

Ares said:

Yes. BMW was PCP, Alfa leased but incl VAT.

Rates are still very good, via brokers. M3/C63 were about the same when I looked, maybe £50/mth more. Not sure now.

Sample of current rates:

A great deal for a great car, looks really well in the pictures on your thread. Rates are still very good, via brokers. M3/C63 were about the same when I looked, maybe £50/mth more. Not sure now.

Sample of current rates:

I can't see how you could fund it better than how you have.

Can I ask the name of the provider on the image above, I'm quite interested at those rates.

All from: http://www.contracthireandleasing.com

berlintaxi said:

daemon said:

berlintaxi said:

If you withdraw in the first 14 days the finance agreement is cancelled and you pay for the car as if you just paid cash in the first place, there is always the possibility of the garage asking for the inducement to finance the car back, but have never heard of it happening.

I think thats wrong? You need to settle the finance with the finance company, not cancel the finance. The garage / supplying dealer never see the financial inducement / incentive in the first place. They merely get paid the full transaction amount by the finance house. You then pay full transaction amount minus incentive to the finance house.Certainly with Mercedes they offered an inducement to take finance then just wanted the price of the car minus the inducement to withdraw from the agreement, no mention of having to repay the inducement to anybody.

Firstly, the finance incentive has nothing at all to do with the dealer. They never see it, they never get it as a separate payment. They simply get a full payment from the finance company. The finance company deduct their incentive from your amount owed.

If you CANCEL your agreement within 14 days, then the finance contract no longer exists and you owe the full balance of the cost of the car to the DEALER. You would then be obliged to pay the dealer for the car in full, either by cash or personal loan.

If you SETTLE your agreement with the finance company, then you are provided with a settlement figure by the finance company (often just including a few days interest, and excluding any requirement to pay back any finance incentive), you then pay the FINANCE COMPANY that amount, and the contract is then closed and complete.

So yes, theres a huge difference between a CANCEL and a SETTLEMENT of a finance agreement.

Very surprised that so many people on here allegedly do this as a matter of course, but dont know how its done......

Edited by daemon on Tuesday 8th August 16:23

Ares said:

djc206 said:

Ares said:

Unless early settlement has punitive penalties! Settlement figures in year one often have full term interest within.

You're entitled to withdraw from any financial product within the first 14 days without penalty are you not?....Although, as the car was then used, it would be worth even less, so buy it back and double save?

To settle finance, they would throw in admin charges and/or other costs. I've heard of interest being 100% front loaded, so the first £X,000 you may is all interest, hence why settlement figures in the first few months are often the full cost of the car.

If you SETTLE within the first month (or any time for that matter) they are legally obliged to only charge you a fair interest amount. They CANT charge you a years interest or the full interest. Typically that amounts to a few pounds / few hundred pounds at most.

And for the avoidance of doubt, you dont CANCEL the agreement - that would roll back the finance agreement and make the full amount payable to the dealer.

And i know thats how it works as (a) i used to work for Santander bank, (b) i used to sell cars for a living and (c) i've done it!!

Again, very surprised that some of the people who tell us they do this regularly havent by now jumped in to explain - gee, maybe that tells us something.....

berlintaxi said:

Ares said:

djc206 said:

Ares said:

Unless early settlement has punitive penalties! Settlement figures in year one often have full term interest within.

You're entitled to withdraw from any financial product within the first 14 days without penalty are you not?daemon said:

berlintaxi said:

Ares said:

djc206 said:

Ares said:

Unless early settlement has punitive penalties! Settlement figures in year one often have full term interest within.

You're entitled to withdraw from any financial product within the first 14 days without penalty are you not?Edited by berlintaxi on Tuesday 8th August 16:46

berlintaxi said:

daemon said:

berlintaxi said:

Ares said:

djc206 said:

Ares said:

Unless early settlement has punitive penalties! Settlement figures in year one often have full term interest within.

You're entitled to withdraw from any financial product within the first 14 days without penalty are you not?Edited by anonymous-user on Tuesday 8th August 16:46

Daemon is right that there is a difference between cancelling and settling finance.

In your case you settled the agreement. I agree with you this is a smart thing to do when incentives are available for taking finance which can't be secured for cash.

Had you cancelled the agreement within your 14 days then you would have had no obligation to MB Finance but you would have been liable for the full amount to the dealer instead. They *could* quite justifiably then claim that you weren't entitled to the incentives as they were dependent on you agreeing to the finance product, no matter how quickly you chose to settle it.

Gassing Station | General Gassing | Top of Page | What's New | My Stuff