Are the wheels about to fall of car finance?

Discussion

RSK21 said:

You've got bogged down in terminology.

Daemon is right that there is a difference between cancelling and settling finance.

In your case you settled the agreement. I agree with you this is a smart thing to do when incentives are available for taking finance which can't be secured for cash.

Had you cancelled the agreement within your 14 days then you would have had no obligation to MB Finance but you would have been liable for the full amount to the dealer instead. They *could* quite justifiably then claim that you weren't entitled to the incentives as they were dependent on you agreeing to the finance product, no matter how quickly you chose to settle it.

I don't think the ability to cancel exists, especially once you've got the car because you've taken it under the finance agreement. AFAIK the only options are to Withdraw or Settle. And you do those with the finance company.Daemon is right that there is a difference between cancelling and settling finance.

In your case you settled the agreement. I agree with you this is a smart thing to do when incentives are available for taking finance which can't be secured for cash.

Had you cancelled the agreement within your 14 days then you would have had no obligation to MB Finance but you would have been liable for the full amount to the dealer instead. They *could* quite justifiably then claim that you weren't entitled to the incentives as they were dependent on you agreeing to the finance product, no matter how quickly you chose to settle it.

I've no idea why they don't ask you to pay the contribution, but they don't. And I'm sure they would if they could, so there must be some legal reason why they don't make you pay.

berlintaxi said:

daemon said:

berlintaxi said:

Ares said:

djc206 said:

Ares said:

Unless early settlement has punitive penalties! Settlement figures in year one often have full term interest within.

You're entitled to withdraw from any financial product within the first 14 days without penalty are you not?Edited by berlintaxi on Tuesday 8th August 16:46

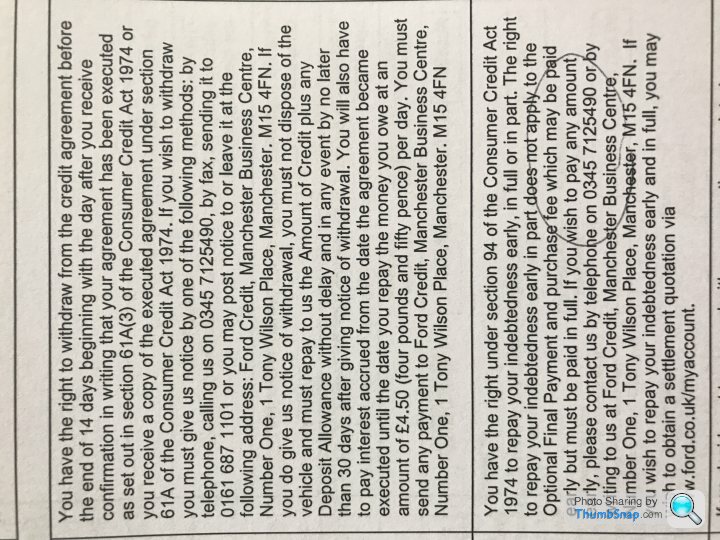

Here's my agreement:

Sheepshanks said:

RSK21 said:

You've got bogged down in terminology.

Daemon is right that there is a difference between cancelling and settling finance.

In your case you settled the agreement. I agree with you this is a smart thing to do when incentives are available for taking finance which can't be secured for cash.

Had you cancelled the agreement within your 14 days then you would have had no obligation to MB Finance but you would have been liable for the full amount to the dealer instead. They *could* quite justifiably then claim that you weren't entitled to the incentives as they were dependent on you agreeing to the finance product, no matter how quickly you chose to settle it.

I don't think the ability to cancel exists, especially once you've got the car because you've taken it under the finance agreement. AFAIK the only options are to Withdraw or Settle. And you do those with the finance company.Daemon is right that there is a difference between cancelling and settling finance.

In your case you settled the agreement. I agree with you this is a smart thing to do when incentives are available for taking finance which can't be secured for cash.

Had you cancelled the agreement within your 14 days then you would have had no obligation to MB Finance but you would have been liable for the full amount to the dealer instead. They *could* quite justifiably then claim that you weren't entitled to the incentives as they were dependent on you agreeing to the finance product, no matter how quickly you chose to settle it.

I've no idea why they don't ask you to pay the contribution, but they don't. And I'm sure they would if they could, so there must be some legal reason why they don't make you pay.

RSK21 said:

Daemon is right that there is a difference between cancelling and settling finance.

Yes, definitely. RSK21 said:

Had you cancelled the agreement within your 14 days then you would have had no obligation to MB Finance but you would have been liable for the full amount to the dealer instead.

No. When you buy a car with PCP there are two separate parts behind the scene. You buy the car from the dealer at the agreed figure, and you borrow the bulk of the cash to pay for it from the Finance co. As security for the loan the finance co takes ownership of the car.If you withdraw (= cancelling) from finance then you need to pay back the amount you borrowed to the finance company. The dealer simply doesn't come into it. You're not withdrawing from the purchase of the car - because you cannot do that. And you can't offer the car to the finance company, because they deal in cash, not cars... Here's the Audi UK Q&A on finance withdrawal.

AudiUK said:

If I withdraw from the finance, what happens to the vehicle?

The customer has to pay off the outstanding balance on the finance Agreement within 30 days of notification of withdrawing from the finance together with the daily interest charges. If the finance is not repaid, the creditor will take appropriate legal action to recover their monies and/or the vehicle.

The customer has to pay off the outstanding balance on the finance Agreement within 30 days of notification of withdrawing from the finance together with the daily interest charges. If the finance is not repaid, the creditor will take appropriate legal action to recover their monies and/or the vehicle.

silentbrown said:

RSK21 said:

Daemon is right that there is a difference between cancelling and settling finance.

Yes, definitely. RSK21 said:

Had you cancelled the agreement within your 14 days then you would have had no obligation to MB Finance but you would have been liable for the full amount to the dealer instead.

No. When you buy a car with PCP there are two separate parts behind the scene. You buy the car from the dealer at the agreed figure, and you borrow the bulk of the cash to pay for it from the Finance co. As security for the loan the finance co takes ownership of the car.If you withdraw (= cancelling) from finance then you need to pay back the amount you borrowed to the finance company. The dealer simply doesn't come into it. You're not withdrawing from the purchase of the car - because you cannot do that. And you can't offer the car to the finance company, because they deal in cash, not cars... Here's the Audi UK Q&A on finance withdrawal.

AudiUK said:

If I withdraw from the finance, what happens to the vehicle?

The customer has to pay off the outstanding balance on the finance Agreement within 30 days of notification of withdrawing from the finance together with the daily interest charges. If the finance is not repaid, the creditor will take appropriate legal action to recover their monies and/or the vehicle.

The customer has to pay off the outstanding balance on the finance Agreement within 30 days of notification of withdrawing from the finance together with the daily interest charges. If the finance is not repaid, the creditor will take appropriate legal action to recover their monies and/or the vehicle.

Fact remains that settling is different to cancelling and settling would seem to be a better option to take in order to mitigate the risk of being pursued for return of incentives.

ETA - Flip side of the above is I assume that the salesman gets a a small sign up bonus on PCPs which falls away upon cancellation but would be honoured on settlement. Ongoing payments to the dealership/salesman therefater one assumes vanish in both instances.

Edited by anonymous-user on Tuesday 8th August 17:32

RSK21 said:

berlintaxi said:

daemon said:

berlintaxi said:

Ares said:

djc206 said:

Ares said:

Unless early settlement has punitive penalties! Settlement figures in year one often have full term interest within.

You're entitled to withdraw from any financial product within the first 14 days without penalty are you not?Edited by berlintaxi on Tuesday 8th August 16:46

Daemon is right that there is a difference between cancelling and settling finance.

In your case you settled the agreement. I agree with you this is a smart thing to do when incentives are available for taking finance which can't be secured for cash.

Had you cancelled the agreement within your 14 days then you would have had no obligation to MB Finance but you would have been liable for the full amount to the dealer instead. They *could* quite justifiably then claim that you weren't entitled to the incentives as they were dependent on you agreeing to the finance product, no matter how quickly you chose to settle it.

Withdrawing from the finance agreement, then paying in cash for the car is very different from "settling the finance early."

daemon said:

you dont CANCEL the agreement - that would roll back the finance agreement and make the full amount payable to the dealer.

And i know thats how it works as (a) i used to work for Santander bank, (b) i used to sell cars for a living and (c) i've done it!!

When I cancelled my PCP deal with VW, the day after taking delivery, I definitely paid them (VW in Milton Keynes), not the dealer. I never spoke to dealer after driving the car away from their premises.And i know thats how it works as (a) i used to work for Santander bank, (b) i used to sell cars for a living and (c) i've done it!!

I kept the £2500 VW incentive for PCP and I kept the cheap service plan deal.

RSK21 said:

Sheepshanks said:

RSK21 said:

You've got bogged down in terminology.

Daemon is right that there is a difference between cancelling and settling finance.

In your case you settled the agreement. I agree with you this is a smart thing to do when incentives are available for taking finance which can't be secured for cash.

Had you cancelled the agreement within your 14 days then you would have had no obligation to MB Finance but you would have been liable for the full amount to the dealer instead. They *could* quite justifiably then claim that you weren't entitled to the incentives as they were dependent on you agreeing to the finance product, no matter how quickly you chose to settle it.

I don't think the ability to cancel exists, especially once you've got the car because you've taken it under the finance agreement. AFAIK the only options are to Withdraw or Settle. And you do those with the finance company.Daemon is right that there is a difference between cancelling and settling finance.

In your case you settled the agreement. I agree with you this is a smart thing to do when incentives are available for taking finance which can't be secured for cash.

Had you cancelled the agreement within your 14 days then you would have had no obligation to MB Finance but you would have been liable for the full amount to the dealer instead. They *could* quite justifiably then claim that you weren't entitled to the incentives as they were dependent on you agreeing to the finance product, no matter how quickly you chose to settle it.

I've no idea why they don't ask you to pay the contribution, but they don't. And I'm sure they would if they could, so there must be some legal reason why they don't make you pay.

Sheepshanks said:

I've no idea why they don't ask you to pay the contribution, but they don't. And I'm sure they would if they could, so there must be some legal reason why they don't make you pay.

I think as you say, legally they cant. Its like any of these furniture places offering 0% finance. We all know that it costs them money but by law they cant offer you a discount in lieu of the 0% finance.Likewise with this - i think its a finance "incentive" or "contribution". Whatever that means in financial legal terms, presumably they cant then take it off you again.

Brave Fart said:

daemon said:

you dont CANCEL the agreement - that would roll back the finance agreement and make the full amount payable to the dealer.

And i know thats how it works as (a) i used to work for Santander bank, (b) i used to sell cars for a living and (c) i've done it!!

When I cancelled my PCP deal with VW, the day after taking delivery, I definitely paid them (VW in Milton Keynes), not the dealer. I never spoke to dealer after driving the car away from their premises.And i know thats how it works as (a) i used to work for Santander bank, (b) i used to sell cars for a living and (c) i've done it!!

I kept the £2500 VW incentive for PCP and I kept the cheap service plan deal.

By virtue of the fact you paid VW Finance, Milton Keynes rather than the dealer shows it was a settlement not a cancellation.

Brave Fart said:

daemon said:

you dont CANCEL the agreement - that would roll back the finance agreement and make the full amount payable to the dealer.

And i know thats how it works as (a) i used to work for Santander bank, (b) i used to sell cars for a living and (c) i've done it!!

When I cancelled my PCP deal with VW, the day after taking delivery, I definitely paid them (VW in Milton Keynes), not the dealer. I never spoke to dealer after driving the car away from their premises.And i know thats how it works as (a) i used to work for Santander bank, (b) i used to sell cars for a living and (c) i've done it!!

I kept the £2500 VW incentive for PCP and I kept the cheap service plan deal.

silentbrown said:

RSK21 said:

Daemon is right that there is a difference between cancelling and settling finance.

Yes, definitely. RSK21 said:

Had you cancelled the agreement within your 14 days then you would have had no obligation to MB Finance but you would have been liable for the full amount to the dealer instead.

No. When you buy a car with PCP there are two separate parts behind the scene. You buy the car from the dealer at the agreed figure, and you borrow the bulk of the cash to pay for it from the Finance co. As security for the loan the finance co takes ownership of the car.If you withdraw (= cancelling) from finance then you need to pay back the amount you borrowed to the finance company. The dealer simply doesn't come into it. You're not withdrawing from the purchase of the car - because you cannot do that. And you can't offer the car to the finance company, because they deal in cash, not cars... Here's the Audi UK Q&A on finance withdrawal.

AudiUK said:

If I withdraw from the finance, what happens to the vehicle?

The customer has to pay off the outstanding balance on the finance Agreement within 30 days of notification of withdrawing from the finance together with the daily interest charges. If the finance is not repaid, the creditor will take appropriate legal action to recover their monies and/or the vehicle.

The customer has to pay off the outstanding balance on the finance Agreement within 30 days of notification of withdrawing from the finance together with the daily interest charges. If the finance is not repaid, the creditor will take appropriate legal action to recover their monies and/or the vehicle.

RSK21 said:

ETA - Flip side of the above is I assume that the salesman gets a a small sign up bonus on PCPs which falls away upon cancellation but would be honoured on settlement. Ongoing payments to the dealership/salesman therefater one assumes vanish in both instances.

I'm curious about this as I don't know the details. but Google threw this up. http://www.mallardvehiclefinance.co.uk/pdf/mallard...Mallard Finance said:

Confirmation of rates, terms & commission

• A visual health check and MOT if needed will have to be done before proceeding with PCP Plus.

• Representative 9.99% APR.

• Lending terms from twenty four to sixty months.

• Commission is 2.5% of the total advance up to a maximum commission payable of £750.00 per deal.

• Commission will be paid in respect of each deal introduced during the month after that deal is funded.

• Commission may be debited back only in the case of fraud or cancellation of finance prior to first payment.

No idea if that's representative, but it means £500 commission on a £20K loan, paid as soon as first finance payment is made. So cancelling within 14 days will lead to an unhappy salesman.• A visual health check and MOT if needed will have to be done before proceeding with PCP Plus.

• Representative 9.99% APR.

• Lending terms from twenty four to sixty months.

• Commission is 2.5% of the total advance up to a maximum commission payable of £750.00 per deal.

• Commission will be paid in respect of each deal introduced during the month after that deal is funded.

• Commission may be debited back only in the case of fraud or cancellation of finance prior to first payment.

djc206 said:

Brave Fart said:

daemon said:

you dont CANCEL the agreement - that would roll back the finance agreement and make the full amount payable to the dealer.

And i know thats how it works as (a) i used to work for Santander bank, (b) i used to sell cars for a living and (c) i've done it!!

When I cancelled my PCP deal with VW, the day after taking delivery, I definitely paid them (VW in Milton Keynes), not the dealer. I never spoke to dealer after driving the car away from their premises.And i know thats how it works as (a) i used to work for Santander bank, (b) i used to sell cars for a living and (c) i've done it!!

I kept the £2500 VW incentive for PCP and I kept the cheap service plan deal.

Theres an important difference between cancelling within the cooling off period and settling the finance via withdrawal from the agreement.

Its worth noting the difference, as it may be significant to someone planning on doing so, and who is reading this thread.

daemon said:

There is a difference between cancelling the contract within 14 days (the cooling off period) whereby you would still be obliged to pay for the goods to the seller, and withdrawing from the finance agreement (the terminology used by Audi there) which is effectively settling the account.

sigh... No again.https://www.audifinance.co.uk/en/private_customers...

RSK21 said:

ETA - Flip side of the above is I assume that the salesman gets a a small sign up bonus on PCPs which falls away upon cancellation but would be honoured on settlement. Ongoing payments to the dealership/salesman therefater one assumes vanish in both instances.

From "back in the day" when i was a car salesman, you got a small signing fee and the dealership got a backhander from the finance company after a certain amount of time.I think salesmen are bonused overally on cars sold, finance agreements sold, add ons sold, so it would all go towards their target.

RSK21 said:

I'm happy to be corrected but I thought that in a Withdrawal within the 14 day period the deal is effectively unwound, meaning the finance house effectively seeks repayment of the monies they have paid the dealer on the applicant's behalf and the dealer than has to cover this by seeking payment from the individual.

Not in my case. I paid VWFS.I Withdrew a week after collecting the car. Actually what happens is you do still pay interest but it's on a daily basis for the number of days you've had the car. They freeze it at the point you confirm you want to Withdraw and then you have 30 days to pay. So I paid a few £ interest but didn't repay the 3 grand deposit contribution.

If you Settled you'd typically pay 2 months interest - could be a few hundred pounds. Plus any doc etc fees - you don't pay those if you Withdraw.

As I said earlier, you can't cancel once you've got the car. What a can of worms that would be - people would have cars that they hadn't paid for and the dealer has to chase them for payment. Hmmm...what could possible go wrong?

Edited by Sheepshanks on Tuesday 8th August 17:59

daemon said:

Personally, i'm not arguing, i'm stating how it is

Theres an important difference between cancelling within the cooling off period and settling the finance via withdrawal from the agreement.

Its worth noting the difference, as it may be significant to someone planning on doing so, and who is reading this thread.

Indeed but the use of withdrawing, settling and cancelling is all getting rather confused. Theres an important difference between cancelling within the cooling off period and settling the finance via withdrawal from the agreement.

Its worth noting the difference, as it may be significant to someone planning on doing so, and who is reading this thread.

To my mind everyone here who has wanted out of a finance agreement has phoned up the finance house for a settlement figure and paid the balance. They have settled their finance, they haven't cancelled anything, they haven't withdrawn from anything they've just paid the debt off as you would any other credit account. Of course withdrawal is an option but I don't see anyone here's description of what they've done as a withdrawal.

djc206 said:

Indeed but the use of withdrawing, settling and cancelling is all getting rather confused.

To my mind everyone here who has wanted out of a finance agreement has phoned up the finance house for a settlement figure and paid the balance. They have settled their finance, they haven't cancelled anything, they haven't withdrawn from anything they've just paid the debt off as you would any other credit account. Of course withdrawal is an option but I don't see anyone here's description of what they've done as a withdrawal.

I Withdrew from my deal. It's very common. Key practical difference is there's no interest penalty.To my mind everyone here who has wanted out of a finance agreement has phoned up the finance house for a settlement figure and paid the balance. They have settled their finance, they haven't cancelled anything, they haven't withdrawn from anything they've just paid the debt off as you would any other credit account. Of course withdrawal is an option but I don't see anyone here's description of what they've done as a withdrawal.

Sheepshanks said:

I Withdrew from my deal. It's very common. Key practical difference is there's no interest penalty.

Not necessarily true. I have posted the section from my agreement (last page) there is a £4.50/day interest penalty on mine in the event of withdrawal. Mine also stipulates that any deposit contribution would need to be repaid in full so in my case I'd have to be mad to withdraw from the agreement when I could instead just phone up and 'settle' it in full (not that I have any intention).But I stand corrected regarding people on this thread having withdrawn

Edit: I see you clarified above in a different response. I would encourage people to look very carefully at their contracts before doing anything. Mine very clearly states that any contribution would need to be repaid on withdrawal. It makes no mention of any interest penalty but since the interest is calculated monthly and the settlement figure is usually valid until the next scheduled payment date I'm guessing that's the penalty you're referring to which on a £40k car at 5.9% would be ~£200.

Edited by djc206 on Tuesday 8th August 18:13

Gassing Station | General Gassing | Top of Page | What's New | My Stuff