How does NCD work

Discussion

Jaroon said:

b ks, the business model relies on low ball first offers, often accepted by oldies, the unaware and the can;t be arsed. Further more the business model also relies on not paying out when it can avoid it whether from a potentially fraudulent claim or an innocent clerical error. Yes millions pay peanuts on st boxes because they won't claim unless a third party is involved and even then will try to pay cash to stop the robbing bds hiking the premium. Grubby industry.

ks, the business model relies on low ball first offers, often accepted by oldies, the unaware and the can;t be arsed. Further more the business model also relies on not paying out when it can avoid it whether from a potentially fraudulent claim or an innocent clerical error. Yes millions pay peanuts on st boxes because they won't claim unless a third party is involved and even then will try to pay cash to stop the robbing bds hiking the premium. Grubby industry.

Wow, I must've been very lucky then, never to have had a single issue in the claims I've made across various types of insurance policies over the last 35 odd years.ks, the business model relies on low ball first offers, often accepted by oldies, the unaware and the can;t be arsed. Further more the business model also relies on not paying out when it can avoid it whether from a potentially fraudulent claim or an innocent clerical error. Yes millions pay peanuts on st boxes because they won't claim unless a third party is involved and even then will try to pay cash to stop the robbing bds hiking the premium. Grubby industry.And companies like Aviva (Norwich Union) and the other household names, to have been in business for 300 years despite having a business model you describe, to essentially cheat their customers. You'd have thought word would have got around after 3 centuries.

Still, you know best.

swisstoni said:

TwigtheWonderkid said:

No you haven't. You keep a copy of your 9 yrs ncb from 2015, and a copy of your 6 years ncb from 2016 and 2017, and if your new firm in 2017 has an 11 yr maximum, then you'll be eligible or it. Because you have proof of 9 yrs from 2 years ago, and 2 yrs claim free since then.

And that, folks, neatly sums up the ridiculousness of the situation. And the whole you can't have one no claims bonus on two cars, but if you crash one you lose both of your no claims.

TwigtheWonderkid said:

Jaroon said:

bks, the business model relies on low ball first offers, often accepted by oldies, the unaware and the can;t be arsed. Further more the business model also relies on not paying out when it can avoid it whether from a potentially fraudulent claim or an innocent clerical error. Yes millions pay peanuts on st boxes because they won't claim unless a third party is involved and even then will try to pay cash to stop the robbing bds hiking the premium. Grubby industry.

Wow, I must've been very lucky then, never to have had a single issue in the claims I've made across various types of insurance policies over the last 35 odd years.ks, the business model relies on low ball first offers, often accepted by oldies, the unaware and the can;t be arsed. Further more the business model also relies on not paying out when it can avoid it whether from a potentially fraudulent claim or an innocent clerical error. Yes millions pay peanuts on st boxes because they won't claim unless a third party is involved and even then will try to pay cash to stop the robbing bds hiking the premium. Grubby industry.And companies like Aviva (Norwich Union) and the other household names, to have been in business for 300 years despite having a business model you describe, to essentially cheat their customers. You'd have thought word would have got around after 3 centuries.

Still, you know best.

The jigsaw piece you seem to be missing here Twig is they stay in business because car insurance is compulsory. They make large profits because they charge much more than they payout and the greater they can make margin the happier they are, it's what they do. They want to give as little back as they can while taking as much as they can, justifiably or unscrupulously. The business model is exactly to cheat the customers when they can or offer the worse possible value if they can get away with it. Word has got round old love but we've no choice but to bend over and hope the lube is in reach. Grubby industry.

Jaroon said:

You have been lucky or you're lying. Never low balled on a car value, never asked sneaky off the cuff questions followed by "sorry that invalidates your claim" there are simply too many fiddles to list but glad you've never been victim of any.

The jigsaw piece you seem to be missing here Twig is they stay in business because car insurance is compulsory. They make large profits because they charge much more than they payout and the greater they can make margin the happier they are, it's what they do. They want to give as little back as they can while taking as much as they can, justifiably or unscrupulously. The business model is exactly to cheat the customers when they can or offer the worse possible value if they can get away with it. Word has got round old love but we've no choice but to bend over and hope the lube is in reach. Grubby industry.

A nice summation.The jigsaw piece you seem to be missing here Twig is they stay in business because car insurance is compulsory. They make large profits because they charge much more than they payout and the greater they can make margin the happier they are, it's what they do. They want to give as little back as they can while taking as much as they can, justifiably or unscrupulously. The business model is exactly to cheat the customers when they can or offer the worse possible value if they can get away with it. Word has got round old love but we've no choice but to bend over and hope the lube is in reach. Grubby industry.

Incidentally Twig's statement of "millions paying £250 fully comp" is a lie he's posted before. Figures below are from 2015, according to the ABI. Bear in mind the car insurance racket has put prices up by 20-30% in the last two years (rising tax - which they should cover themselves, and compensation payouts - which the industry would rather pay than fight in court because they can just pass the costs onto innocent drivers, ie you and me) so even the lowest figure will be at least £60 higher.

Age of Policyholder Average premium

18-20 £972

21-25 £649

26-30 £502

31-35 £426

36-40 £378

41-45 £343

46-50 £326

51-55 £306

56-60 £277

61-65 £252

66-70 £241

71-75 £255

76-80 £291

81-85 £352

86-90 £415

91+ £478

OK, so I'm old.

Anyway my first job in 1977 was with Cornhill Insurance (now part of Allianz).

Windscreen cover was FREE if you had Comprehensive cover, and had no excess whether repaired (which was quite a new concept then) or replaced - but we'd only pay for a toughened screen if that was what got broken, even though all the replacement firms seemed to only fit laminated screens!

Why does windscreen cover have an excess these days? Can anyone in the industry now explain that?

6 years NCD got you a 65% discount, one more year got you a protected NCD for FREE. 1 "fault" claim cost nothing, but you had the rest of that insurance year and the whole of the next one without protection. But if you got there claim free you got the protection back FOR FREE!

Nowadays the "protected" NCD is a load of B*llocks - they charge you to have it, but even if you pay for it and have a claim they allow you to keep your NCD but then load the premium! Trousers down and get ready.

Similar situation with "multi-car" insurance - back in that era we could put up to 4 cars on one policy! Not a new invention in any way, shape or form!

But it allegedly is a new invention - my A*se!

The personal insurance industry is a complete p*ss-take these days!

Anyway my first job in 1977 was with Cornhill Insurance (now part of Allianz).

Windscreen cover was FREE if you had Comprehensive cover, and had no excess whether repaired (which was quite a new concept then) or replaced - but we'd only pay for a toughened screen if that was what got broken, even though all the replacement firms seemed to only fit laminated screens!

Why does windscreen cover have an excess these days? Can anyone in the industry now explain that?

6 years NCD got you a 65% discount, one more year got you a protected NCD for FREE. 1 "fault" claim cost nothing, but you had the rest of that insurance year and the whole of the next one without protection. But if you got there claim free you got the protection back FOR FREE!

Nowadays the "protected" NCD is a load of B*llocks - they charge you to have it, but even if you pay for it and have a claim they allow you to keep your NCD but then load the premium! Trousers down and get ready.

Similar situation with "multi-car" insurance - back in that era we could put up to 4 cars on one policy! Not a new invention in any way, shape or form!

But it allegedly is a new invention - my A*se!

The personal insurance industry is a complete p*ss-take these days!

popeyewhite said:

A nice summation.

Incidentally Twig's statement of "millions paying £250 fully comp" is a lie he's posted before. Figures below are from 2015, according to the ABI. Bear in mind the car insurance racket has put prices up by 20-30% in the last two years (rising tax - which they should cover themselves, and compensation payouts - which the industry would rather pay than fight in court because they can just pass the costs onto innocent drivers, ie you and me) so even the lowest figure will be at least £60 higher.

Age of Policyholder Average premium

18-20 £972

21-25 £649

26-30 £502

31-35 £426

36-40 £378

41-45 £343

46-50 £326

51-55 £306

56-60 £277

61-65 £252

66-70 £241

71-75 £255

76-80 £291

81-85 £352

86-90 £415

91+ £478

It's not a lie, you're just not very good at maths. Let's look at 41-45, £343 av premium. There will plenty of people in there early 40s, successful, living in a city, with a Porsche or whatever, playing £800 or £1000. If one person in that age group is paying £843, then 5 people need to be paying £243 to get your average of £343. Apply that principle to the rest of the age bands. 61-65, av premium £252. If one person is paying £1152 for his Lamborghini, 300 people would need to be paying £249 to get your average. Incidentally Twig's statement of "millions paying £250 fully comp" is a lie he's posted before. Figures below are from 2015, according to the ABI. Bear in mind the car insurance racket has put prices up by 20-30% in the last two years (rising tax - which they should cover themselves, and compensation payouts - which the industry would rather pay than fight in court because they can just pass the costs onto innocent drivers, ie you and me) so even the lowest figure will be at least £60 higher.

Age of Policyholder Average premium

18-20 £972

21-25 £649

26-30 £502

31-35 £426

36-40 £378

41-45 £343

46-50 £326

51-55 £306

56-60 £277

61-65 £252

66-70 £241

71-75 £255

76-80 £291

81-85 £352

86-90 £415

91+ £478

Now of course there wouldn't be 300 people. Someone is paying 150, someone else is paying £175 etc. But with 35 million cars, it's obvious based on your own figures supplied that millions are paying sub £250.

Jaroon said:

The jigsaw piece you seem to be missing here Twig is they stay in business because car insurance is compulsory. They make large profits because they charge much more than they payout and the greater they can make margin the happier they are, it's what they do. They want to give as little back as they can while taking as much as they can, justifiably or unscrupulously. The business model is exactly to cheat the customers when they can or offer the worse possible value if they can get away with it. Word has got round old love but we've no choice but to bend over and hope the lube is in reach. Grubby industry.

So Aviva stay in business for 300 years because car insurance is compulsory, even though car insurance has only been compulsory for 87 years. Also, only 2 insurances are compulsory, car and employers' liability. How do Aviva sell any other insurances if their business model is one of cheating the customer. Do you think car insurance is what keeps Aviva afloat. Surely after all these years of cheating the customer, they wouldn't be able to sell any kind of insurance to anyone. Finally, the fact is car insurance is a loss maker for the vast majority of those writing it. 2 mins research on google will tell you this. So all your talk of large profits is utter b

ks. TwigtheWonderkid said:

It's not a lie, you're just not very good at maths. Let's look at 41-45, £343 av premium. There will plenty of people in there early 40s, successful, living in a city, with a Porsche or whatever, playing £800 or £1000. If one person in that age group is paying £843, then 5 people need to be paying £243 to get your average of £343. Apply that principle to the rest of the age bands. 61-65, av premium £252. If one person is paying £1152 for his Lamborghini, 300 people would need to be paying £249 to get your average.

Now of course there wouldn't be 300 people. Someone is paying 150, someone else is paying £175 etc. But with 35 million cars, it's obvious based on your own figures supplied that millions are paying sub £250.

Do stop wittering on. Now of course there wouldn't be 300 people. Someone is paying 150, someone else is paying £175 etc. But with 35 million cars, it's obvious based on your own figures supplied that millions are paying sub £250.

popeyewhite said:

TwigtheWonderkid said:

It's not a lie, you're just not very good at maths. Let's look at 41-45, £343 av premium. There will plenty of people in there early 40s, successful, living in a city, with a Porsche or whatever, playing £800 or £1000. If one person in that age group is paying £843, then 5 people need to be paying £243 to get your average of £343. Apply that principle to the rest of the age bands. 61-65, av premium £252. If one person is paying £1152 for his Lamborghini, 300 people would need to be paying £249 to get your average.

Now of course there wouldn't be 300 people. Someone is paying 150, someone else is paying £175 etc. But with 35 million cars, it's obvious based on your own figures supplied that millions are paying sub £250.

Do stop wittering on. Now of course there wouldn't be 300 people. Someone is paying 150, someone else is paying £175 etc. But with 35 million cars, it's obvious based on your own figures supplied that millions are paying sub £250.

desolate said:

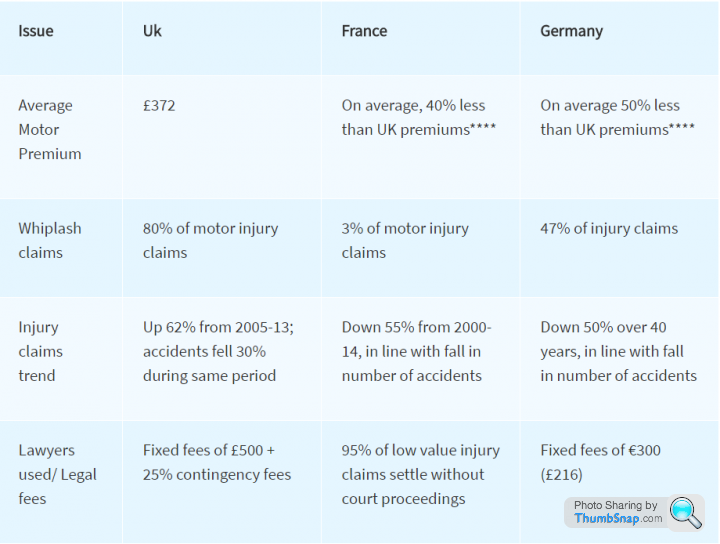

The UK insurance market is one of the most competitive in the world. Yet still we pay more than similar European countries. There are some legitimate reasons why this should be the case but the public need to look to themselves as well:

The beginning year '17 UK average premium was £484. https://www.theguardian.com/money/2017/jul/18/cost...

Confused states prices have shot up in the last quarter and are now nearer an average £847.

https://www.confused.com/car-insurance/price-index

popeyewhite said:

The beginning year '17 UK average premium was £484.

https://www.theguardian.com/money/2017/jul/18/cost...

Confused states prices have shot up in the last quarter and are now nearer an average £847.

https://www.confused.com/car-insurance/price-index

And what about the other factors outlined in the table?https://www.theguardian.com/money/2017/jul/18/cost...

Confused states prices have shot up in the last quarter and are now nearer an average £847.

https://www.confused.com/car-insurance/price-index

Are the relevant or not?

desolate said:

And what about the other factors outlined in the table?

Are the relevant or not?

I'm sure they are relevant. The plethora of whiplash claims needs to be nipped in the bud by legislation, or the insurance companies will just pass the cost on to the customer. There was me thinking the whole idea is you purchase insurance and sometimes you win by claiming and sometimes you lose. More often than not you lose, and the insurers make their lucre. But when insurance companies lose they still win by hiking premiums. Great business model. Injury claims - the same though I'll concede lawyer greed needs to be addressed. What's the rest of Europe like? Same again lawyer fees. It would be interesting to see if this high number of claims and hence excessive fees were reduced if the price would be reflected in reduced premiums. I'd bet my house it wouldn't.Are the relevant or not?

popeyewhite said:

I'm sure they are relevant. The plethora of whiplash claims needs to be nipped in the bud by legislation, or the insurance companies will just pass the cost on to the customer. There was me thinking the whole idea is you purchase insurance and sometimes you win by claiming and sometimes you lose. More often than not you lose, and the insurers make their lucre. But when insurance companies lose they still win by hiking premiums. Great business model. Injury claims - the same though I'll concede lawyer greed needs to be addressed. What's the rest of Europe like? Same again lawyer fees. It would be interesting to see if this high number of claims and hence excessive fees were reduced if the price would be reflected in reduced premiums. I'd bet my house it wouldn't.

The UK and Ireland have a more American style claim culture than anywhere else in Europe - new legislation is taking effect and reducing the volume of soft tissue claims but other factors have hat a detrimental effect (Ogden Rate, Tax and Vehicle repair costs)I have no doubt that is claims costs reduce then so will premiums as if the incumbents don't reduce premiums new capital will.

I'm dubious about the claims of cheaper insurance in Germany. I have quite a few friends in Germany and they all think insurance is a rip off, especially for drivers 40+. It is better for young drivers apparently. But I'm 55 and most of my German friends are in my age group and they can't believe how little I pay. Their insurance is 4 times the cost.

In France, ncb goes with the driver and not the car/policy. So have max ncb on 1 vehicle, and any other vehicles you get also have max ncb. They hate it. Because if you have a crash on your moped, you lose your bonus on all your cars. Unlike here where you only lose the bonus on the policy your claimed on. They all ask why they can't have a system like ours!

In France, ncb goes with the driver and not the car/policy. So have max ncb on 1 vehicle, and any other vehicles you get also have max ncb. They hate it. Because if you have a crash on your moped, you lose your bonus on all your cars. Unlike here where you only lose the bonus on the policy your claimed on. They all ask why they can't have a system like ours!

Gassing Station | General Gassing | Top of Page | What's New | My Stuff