Ask a car salesman anything...anything at all (Vol. 2).

Discussion

KTF said:

Trevor555 said:

You'll never know now that you've paid them.

Agreed. Can still cancel it on the credit card I paid it with I guess to find out. But if they didn't actually say you couldn't have your car back then the card company might not take that view.

It's worth a quick call to the FCA to see if the dealer can ask for this £250 back.

After all, you've cancelled the agreement within the cooling off period which you are entitled to do.

If the FCA say it's not on and they start a case the dealer has to pay for the investigation, and do a LOT of paperwork. And can be fined if theyve broken any rules.

KTF said:

They said it was a dealer contribution and they would have got it back from the finance company had I not cancelled if.

As I had cancelled it they were now £250 short on the car.

My car was in for warranty work at the time so they had the keys and car at that point as well.

When you cancelled the finance did you pay any interest - even a few pounds?As I had cancelled it they were now £250 short on the car.

My car was in for warranty work at the time so they had the keys and car at that point as well.

It seems a massive grey area to me - if you cancel (Withdraw) it’s like the finance never existed so it seems logical that any deposit contribution also now doesn’t exist.

Yet when I did it with a new VW, I was surprised to be charged about £25 interest - so it must be considered that there’s a loan in place. There was no suggestion of having to repay the £2750 deposit contribution.

KTF said:

They said it was a dealer contribution and they would have got it back from the finance company had I not cancelled if.

As I had cancelled it they were now £250 short on the car.

My car was in for warranty work at the time so they had the keys and car at that point as well.

What does your finance paperwork say ref deposit contributions?As I had cancelled it they were now £250 short on the car.

My car was in for warranty work at the time so they had the keys and car at that point as well.

As I've mentioned many times in various similar threads, Renault/Dacia finance paperwork states that if you withdraw, you are liable for any deposit contribution or incentive.

Sheepshanks said:

When you cancelled the finance did you pay any interest - even a few pounds?

It seems a massive grey area to me - if you cancel (Withdraw) it’s like the finance never existed so it seems logical that any deposit contribution also now doesn’t exist.

Yet when I did it with a new VW, I was surprised to be charged about £25 interest - so it must be considered that there’s a loan in place. There was no suggestion of having to repay the £2750 deposit contribution.

To cancel after the 4 days it took to get the details it was the loan plus £4ish interest, to settle it was the loan plus £40. It seems a massive grey area to me - if you cancel (Withdraw) it’s like the finance never existed so it seems logical that any deposit contribution also now doesn’t exist.

Yet when I did it with a new VW, I was surprised to be charged about £25 interest - so it must be considered that there’s a loan in place. There was no suggestion of having to repay the £2750 deposit contribution.

HTP99 said:

What does your finance paperwork say ref deposit contributions?

As I've mentioned many times in various similar threads, Renault/Dacia finance paperwork states that if you withdraw, you are liable for any deposit contribution or incentive.

I am going to dig it out later and check. As I've mentioned many times in various similar threads, Renault/Dacia finance paperwork states that if you withdraw, you are liable for any deposit contribution or incentive.

Edit: It says

If your Finance Agreement was subject to a deposit contribution you may need to repay this.

May being the ambiguous word I feel.

Edited by KTF on Friday 23 July 08:43

And from the agreement itself it says under 'changing my mind':

"If my credit agreement includes a Finance Deposit Contribution, I will need to increase my own deposit accordingly to cover this. If I want to withdraw from the credit agreement I will have to let RCIFS know (by telephone or in writing) and will have to repay the amount of credit with interest within 30 days together with any deposit allowance or other allowance paid by RCIFS. I will NOT be entitled to return the vehicle."

When I called them to cancel they only asked for the original finance amount + interest, not the original finance amount + interest + the £250 contribution.

Edited by KTF on Friday 23 July 09:58

KTF said:

To cancel after the 4 days it took to get the details it was the loan plus £4ish interest, to settle it was the loan plus £40.

I would hope the fact they charged you £4 gets you off.I've no idea how the car industry continues to get away with charging different prices for cash or credit. It's 'forcing' people to take credit.

I called the finance company and they said that any deposit contribution is nothing to do with them and is dealer provided. I would have to take it up with the dealer and argue it with them.

The dealer is saying that as I cancelled the finance, the contribution was no longer valid so I owed them the difference.

There is nothing in the delaer t&c that I can see that make any mention at all to what happens if you cancel the finance or deposit contributions.

The dealer is saying that as I cancelled the finance, the contribution was no longer valid so I owed them the difference.

There is nothing in the delaer t&c that I can see that make any mention at all to what happens if you cancel the finance or deposit contributions.

KTF said:

I called the finance company and they said that any deposit contribution is nothing to do with them and is dealer provided. I would have to take it up with the dealer and argue it with them.

The dealer is saying that as I cancelled the finance, the contribution was no longer valid so I owed them the difference.

There is nothing in the delaer t&c that I can see that make any mention at all to what happens if you cancel the finance or deposit contributions.

I suggest you speak to Trading Standards or Citizens Advice Bureau.The dealer is saying that as I cancelled the finance, the contribution was no longer valid so I owed them the difference.

There is nothing in the delaer t&c that I can see that make any mention at all to what happens if you cancel the finance or deposit contributions.

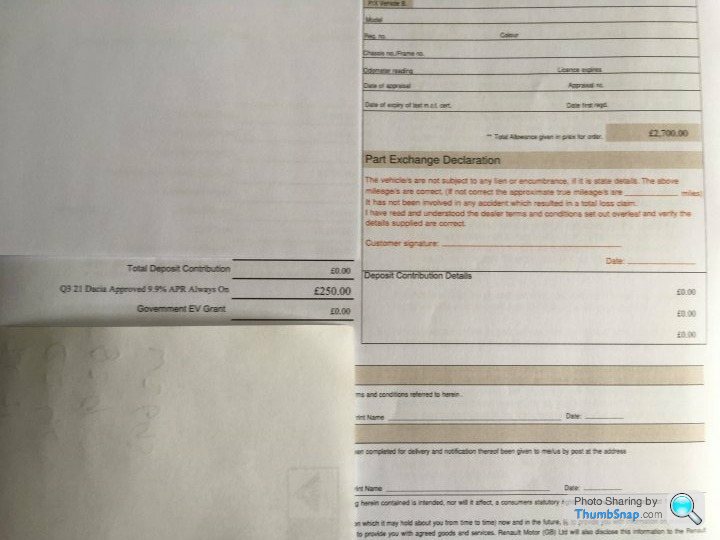

What paperwork supported the 'request for payment'?

How was this £250 described on your vehicle invoice...........or was it lumped in with PX or something?

Here is the section from the invoice.

There was nothing to support the request for payment other than several phone calls asking for me to call them back.

My car was at the dealer for warranty work so I spoke to the salesperson then and that is when they mentioned the £250 must be paid.

There was nothing to support the request for payment other than several phone calls asking for me to call them back.

My car was at the dealer for warranty work so I spoke to the salesperson then and that is when they mentioned the £250 must be paid.

Edited by KTF on Friday 23 July 11:07

Graeme123 said:

If you paid on credit card I would be blocking the payment and then going to another dealer if you needed any work done.

I did pay on credit card. Legally I wanted to try to find out where I stand as this seems a bit of a grey area.For example, if I had never gone in to the place again, what would they have done? The fact that they had the car and the keys at the point they brought it up did also not help.

I called my card company and told them the whole situation. They are going to raise it as a disputed transaction and have asked for a copy of the t&c (which make no mention of deposit incentives or what happened if you cancel the finance and have taken out an incentive). It frozen until then.

Like you said above, I very much doubt they would have chased it had I not walked in and spoke to them.

Like you said above, I very much doubt they would have chased it had I not walked in and spoke to them.

Dear car salesman. I have a question for you.... When you get a car from a part ex. What do you think when you later find out that part-ex’d car is an absolute dog that the seller was getting rid off only because it had so many faults? If you re-sell these cars with a warranty, it must be a nightmare for you? And possibly a financial loss?

How do you deal with these lemons?

How do you deal with these lemons?

Mr Miata said:

Dear car salesman. I have a question for you.... When you get a car from a part ex. What do you think when you later find out that part-ex’d car is an absolute dog that the seller was getting rid off only because it had so many faults? If you re-sell these cars with a warranty, it must be a nightmare for you? And possibly a financial loss?

How do you deal with these lemons?

Very good question, lets assume the light is on for a cam chain position sensor pointing to a stretched chain but the owner cleared it with an ODB2 blue tooth dongle and their phone before they part exchanged it, knowing it would come back.How do you deal with these lemons?

Wasn't me, but I know someone who did this with WBAC.............

Gassing Station | General Gassing | Top of Page | What's New | My Stuff