How the hell do people afford cars these days?

Discussion

To me, the correlation between how expensive a car is in terms of total cost of ownership and how nice it is seems weak at best, non-existent at worst. I can understand people spending a lot on something special, but spending £400 a month to run a two litre diesel rep mobile baffles me.

Each to their own though. The more people buy boring new cars, the cheaper they'll be for me to buy second-hand a few years down the line.

Each to their own though. The more people buy boring new cars, the cheaper they'll be for me to buy second-hand a few years down the line.

I often think the same.

Currently running a 2004 Accord 2.4 ex manual. Works fine. Will keep it indefinitely at this point as my financial situation isn't great.

I often look at "cheap" cars. Like Kia Rio 1.0 TGDI Etc

Still £230 pm + for those basic cars!!

So those people I know driving new BMW 118i, c220d etc, must be paying close to £400 (if not more) per month

Currently running a 2004 Accord 2.4 ex manual. Works fine. Will keep it indefinitely at this point as my financial situation isn't great.

I often look at "cheap" cars. Like Kia Rio 1.0 TGDI Etc

Still £230 pm + for those basic cars!!

So those people I know driving new BMW 118i, c220d etc, must be paying close to £400 (if not more) per month

Brand new cars are horrendously expensive. I mean I look at many of them and can't believe the RRPs on them but that said for most new car buyers they don't see the RRP, they see the monthly cost.

Seems leases and PCP means monthly costs are fairly reasonable and it seems people are prepared to pay a fairly significant sum per month to own a car. I suppose one thing to consider is that they'll all be under warranty so no repair costs, some factor in servicing etc. So it's literally that amount per month.

Between me and my partner we have six cars, she owns her car (2011 Merc ML) outright, I have a small personal loan for my daily car (2008 Merc S Class) and I own the others having saved/paid them off. That said between the loan and paying to store two of my cars I pay out roughly £400, not including fuel. tax and insurance. I do earn well I will admit and my other half works and pays for her own vehicle.

I think people have come to assume that cars cost X amount a month and that's how they run them. Although I'd be surprised if the average earner is paying £250+ but I'm not surprised if couples pay a monthly PCP of £500 or so if both earn. Can't say I fancy it much myself.

Seems leases and PCP means monthly costs are fairly reasonable and it seems people are prepared to pay a fairly significant sum per month to own a car. I suppose one thing to consider is that they'll all be under warranty so no repair costs, some factor in servicing etc. So it's literally that amount per month.

Between me and my partner we have six cars, she owns her car (2011 Merc ML) outright, I have a small personal loan for my daily car (2008 Merc S Class) and I own the others having saved/paid them off. That said between the loan and paying to store two of my cars I pay out roughly £400, not including fuel. tax and insurance. I do earn well I will admit and my other half works and pays for her own vehicle.

I think people have come to assume that cars cost X amount a month and that's how they run them. Although I'd be surprised if the average earner is paying £250+ but I'm not surprised if couples pay a monthly PCP of £500 or so if both earn. Can't say I fancy it much myself.

Alex_225 said:

Brand new cars are horrendously expensive. I mean I look at many of them and can't believe the RRPs on them but that said for most new car buyers they don't see the RRP, they see the monthly cost.

Seems leases and PCP means monthly costs are fairly reasonable and it seems people are prepared to pay a fairly significant sum per month to own a car. I suppose one thing to consider is that they'll all be under warranty so no repair costs, some factor in servicing etc. So it's literally that amount per month.

Between me and my partner we have six cars, she owns her car (2011 Merc ML) outright, I have a small personal loan for my daily car (2008 Merc S Class) and I own the others having saved/paid them off. That said between the loan and paying to store two of my cars I pay out roughly £400, not including fuel. tax and insurance. I do earn well I will admit and my other half works and pays for her own vehicle.

I think people have come to assume that cars cost X amount a month and that's how they run them. Although I'd be surprised if the average earner is paying £250+ but I'm not surprised if couples pay a monthly PCP of £500 or so if both earn. Can't say I fancy it much myself.

Jesus, a loan to run a 2008 S Class.Seems leases and PCP means monthly costs are fairly reasonable and it seems people are prepared to pay a fairly significant sum per month to own a car. I suppose one thing to consider is that they'll all be under warranty so no repair costs, some factor in servicing etc. So it's literally that amount per month.

Between me and my partner we have six cars, she owns her car (2011 Merc ML) outright, I have a small personal loan for my daily car (2008 Merc S Class) and I own the others having saved/paid them off. That said between the loan and paying to store two of my cars I pay out roughly £400, not including fuel. tax and insurance. I do earn well I will admit and my other half works and pays for her own vehicle.

I think people have come to assume that cars cost X amount a month and that's how they run them. Although I'd be surprised if the average earner is paying £250+ but I'm not surprised if couples pay a monthly PCP of £500 or so if both earn. Can't say I fancy it much myself.

Brave

Saudade said:

I think if you're on a combined income of £100k and can't afford a car you want something is very wrong or doesn't add up.

We're on about 60k and while we don't go on holiday abroad, we have 2 dogs (both cost a lot of money, their 4 beds are close to 2k, nevermind food, vet bills and the rest - one has a lifelong medical problem and the other is 14), we pay for the best internet, have good phones, don't have a water meter and don't worry about elec/gas, we could easily spend 600pm on a car and not really worry about it, I won't do that because it isn't a smart financial decision.

I think that is maybe what OP and everyone else is saying - they can afford the car, but it doesn't make sense to actually pay for one, especially in the current market.

Where you live plays a huge part. I could afford pretty much anything where I from, but where I live now means moving house is really quite difficult to stomach, financially.We're on about 60k and while we don't go on holiday abroad, we have 2 dogs (both cost a lot of money, their 4 beds are close to 2k, nevermind food, vet bills and the rest - one has a lifelong medical problem and the other is 14), we pay for the best internet, have good phones, don't have a water meter and don't worry about elec/gas, we could easily spend 600pm on a car and not really worry about it, I won't do that because it isn't a smart financial decision.

I think that is maybe what OP and everyone else is saying - they can afford the car, but it doesn't make sense to actually pay for one, especially in the current market.

When it comes to borrowing against a new car I think you've got to be barking mad, unless someone else like work is paying for it, considering not only are you paying interest but the car is depreciating in value. Also especially since many cars from mid 90s to say 2006 will last many years with basic mainteance and are fundametally better cars to drive than the modern computer controlled bloated dross we have today. I would however take a loan to buy an appreciating classic car if I had to.... £25k loan to buy something really interesting vs £25k to buy a brand new shopping tolley hmmmm tough decision.

It just depends on so many variables - mortgage amount, kids, other financial commitments etc.

My wife and I earn between us circa 115-120k - myself as main bread winner.

However, i've been lucky with sharesaves, redundancy payment etc and it means I have bought my last 3 cars outright. Technically my current car is waaaay above my paygrade but feck it - I can afford it and can run it (albeit if it was a daily at 17-18mpg it would cripple me).

Mortgage is low and we're quite comfortable, though not at all rich and we're still careful with our money.

I all just depends on priorities - there are more 40k plus cars on driveways around where I am than I suspect there are people who could afford them not on a monthly plan but end of the day people budget and plan as suits them.

My wife and I earn between us circa 115-120k - myself as main bread winner.

However, i've been lucky with sharesaves, redundancy payment etc and it means I have bought my last 3 cars outright. Technically my current car is waaaay above my paygrade but feck it - I can afford it and can run it (albeit if it was a daily at 17-18mpg it would cripple me).

Mortgage is low and we're quite comfortable, though not at all rich and we're still careful with our money.

I all just depends on priorities - there are more 40k plus cars on driveways around where I am than I suspect there are people who could afford them not on a monthly plan but end of the day people budget and plan as suits them.

Cant Find a Charger when I need one said:

Jesus, a loan to run a 2008 S Class.

Brave

I've got money aside to run it, I just didn't want to pay outright for it. I'm not a complete mentalist!Brave

Although to be fair the last 12 months cost me £330 plus fuel/tax/insurance. The first year it needed about £4k, mostly covered by warranty anyway and then £1200 on the MOT/Service.

deckster said:

A cursory google shows leases from around £300/month, whereas with practically zero effort I'm going to be paying £150/month for mine (admittedly with a bit of help from the generosity of HMG's EV grant, which you can't get any more).

There are also company EV schemes that allow you to pay out of your gross salary for an EV lease so you'd save about 40% on the cost. I'd jump at the chance to do this as pre-Covid I was paying £250 pm on fuel which would be more like £350 now so getting an EV and charging it for free at work would be a no brainer.cerb4.5lee said:

With the way that things are going...I'm starting to wonder how people can afford to live...never mind buying/running cars! Everything is so chuffing expensive currently, and it will only get worse too.

Indeed - it all seems pretty depressing really. I giant poo sandwich with poo sauce.dave_s13 said:

Nobody can say the current market isn't fooked though, the most sensible thing at the moment would be to sell up and get a bicycle.

Not sure that is the answer either given lack of stock and crazy prices for bike parts due to the impact of covid on the supply chain. Looks like walking might be the only option soon...

Some of these prices are just insane. I expect I’d be shocked if I looked into the finances of the people buying stuff like this:

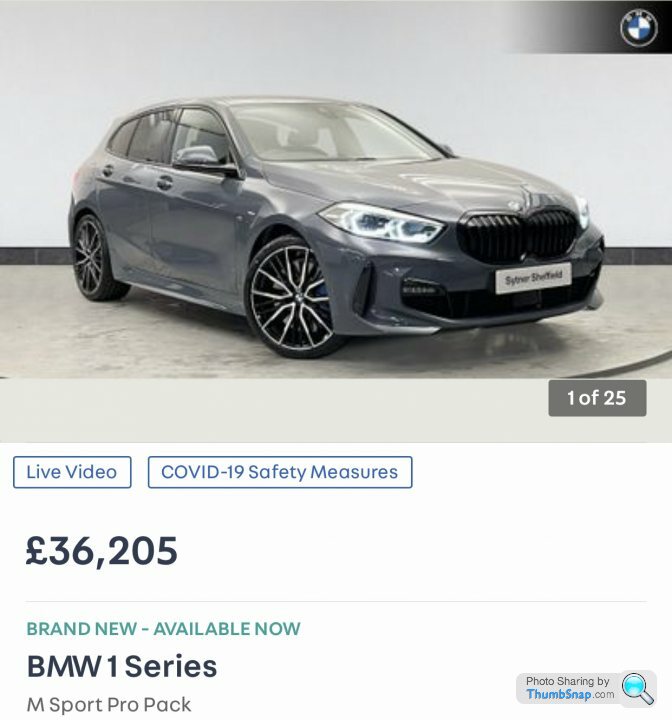

- A 118d with a whopping 150hp…don’t worry though, it’s not just an M-Sport, it’s an M-Sport “Pro”. Because you clearly need to be a “Pro” to handle this FWD diesel hatch.

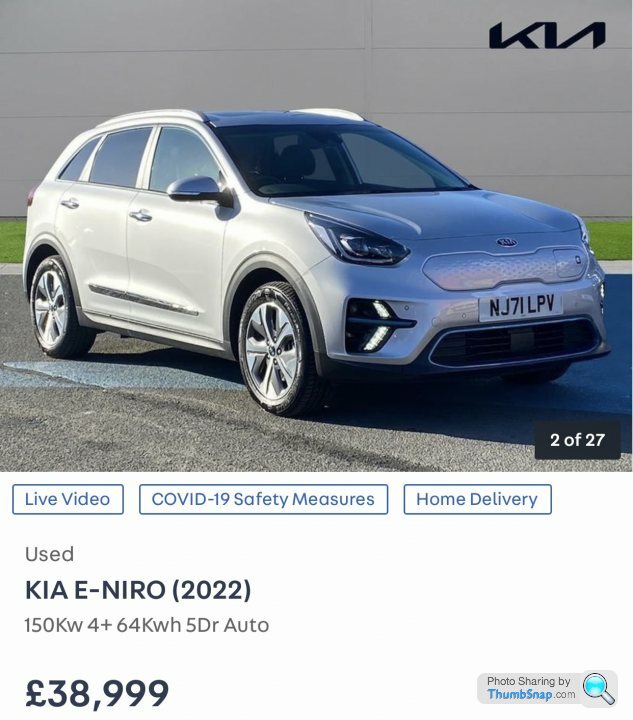

I thought Kias were supposed to be cheap? £672 per month! One of my neighbours bought one and it apparently takes 16 hours to charge via a domestic socket because they don’t have an EV charger (splitting an electrical loop would require digging-up the road and neighbour’s freshly-laid drives).

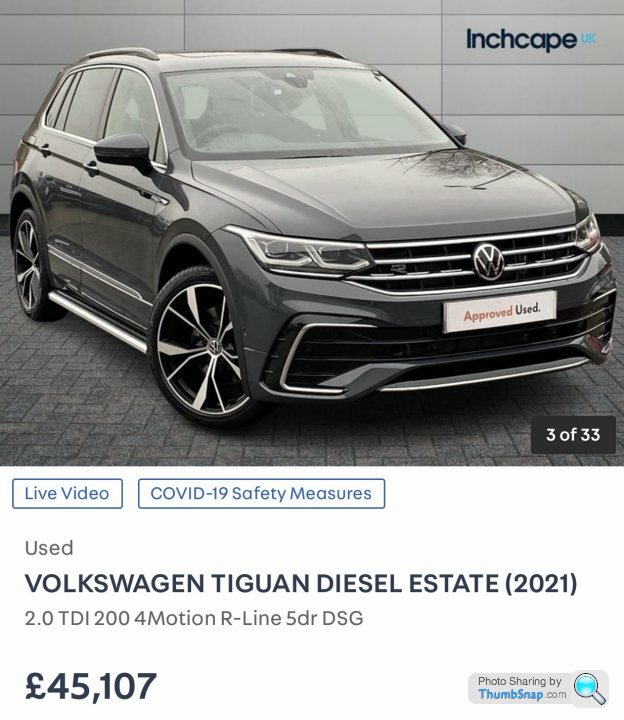

And £45k for a generic Golf-platform crossover with repmobile 2.0 TDI engine. Absolutely mental!

- A 118d with a whopping 150hp…don’t worry though, it’s not just an M-Sport, it’s an M-Sport “Pro”. Because you clearly need to be a “Pro” to handle this FWD diesel hatch.

I thought Kias were supposed to be cheap? £672 per month! One of my neighbours bought one and it apparently takes 16 hours to charge via a domestic socket because they don’t have an EV charger (splitting an electrical loop would require digging-up the road and neighbour’s freshly-laid drives).

And £45k for a generic Golf-platform crossover with repmobile 2.0 TDI engine. Absolutely mental!

I've leased my single family car since I first took the plunge away from old sheds back in 2014.

I'm worse off financially than if I'd kept my £2k year 2000 MkIV Golf which owed me just insurance, RFL and servicing/MOT. But it's not crippling for a single income family with a lower income than the OP's.

On the upside, I've enjoyed trying different new metal (M135i, A4, Octavia vRS, A4 Avant...) with set budget each month. The added bonus has been reliability worries haven't been a consideration which is good when ferrying my two young kids on holiday or visiting friends further afield.

My current steed is a modest Kia Proceed GT at £2.2k initial and £241 per month for 36 months. It's actually quite a fun little thing, and I'm pleased I've stuck to the leasing mantra of 'chasing the deal, not the car'. For context, this is the highest price I've paid for any of my leases to-date so I've not gone anywhere near the ridiculous £400-900 figures that some cars are demanding currently.

Prices have gone pretty bonkers in the last 18 months or so, so when this lease is up then I'll most likely get something with second hand with 6 cylinders as I can't see any interesting being good value on lease for the foreseeable. I want to get back into a BMW since I still look back whistfully at my old M135i - what a great car that was.

I'm worse off financially than if I'd kept my £2k year 2000 MkIV Golf which owed me just insurance, RFL and servicing/MOT. But it's not crippling for a single income family with a lower income than the OP's.

On the upside, I've enjoyed trying different new metal (M135i, A4, Octavia vRS, A4 Avant...) with set budget each month. The added bonus has been reliability worries haven't been a consideration which is good when ferrying my two young kids on holiday or visiting friends further afield.

My current steed is a modest Kia Proceed GT at £2.2k initial and £241 per month for 36 months. It's actually quite a fun little thing, and I'm pleased I've stuck to the leasing mantra of 'chasing the deal, not the car'. For context, this is the highest price I've paid for any of my leases to-date so I've not gone anywhere near the ridiculous £400-900 figures that some cars are demanding currently.

Prices have gone pretty bonkers in the last 18 months or so, so when this lease is up then I'll most likely get something with second hand with 6 cylinders as I can't see any interesting being good value on lease for the foreseeable. I want to get back into a BMW since I still look back whistfully at my old M135i - what a great car that was.

Edited by JuanGandini on Tuesday 8th March 15:56

Saudade said:

I think if you're on a combined income of £100k and can't afford a car you want something is very wrong or doesn't add up.

We're on about 60k and while we don't go on holiday abroad, we have 2 dogs (both cost a lot of money, their 4 beds are close to 2k, nevermind food, vet bills and the rest - one has a lifelong medical problem and the other is 14), we pay for the best internet, have good phones, don't have a water meter and don't worry about elec/gas, we could easily spend 600pm on a car and not really worry about it, I won't do that because it isn't a smart financial decision.

I think that is maybe what OP and everyone else is saying - they can afford the car, but it doesn't make sense to actually pay for one, especially in the current market.

Yes exactly, It's not as if im looking at my bank account and wondering where my money is going, its justifying the expenditure on something that in my opinion isnt worth the money, eg a Honda E for £400 pm with x amount down at the start with limited mileage as an example. We're on about 60k and while we don't go on holiday abroad, we have 2 dogs (both cost a lot of money, their 4 beds are close to 2k, nevermind food, vet bills and the rest - one has a lifelong medical problem and the other is 14), we pay for the best internet, have good phones, don't have a water meter and don't worry about elec/gas, we could easily spend 600pm on a car and not really worry about it, I won't do that because it isn't a smart financial decision.

I think that is maybe what OP and everyone else is saying - they can afford the car, but it doesn't make sense to actually pay for one, especially in the current market.

I can afford that, i just don't think it represents value for money.

dundarach said:

An interesting comparison I've often wondered about is:

Value of car, vs Value of house.

Both our cars work out at roughly 2.35%

The next street some houses are at around 20% I'd guess.

That's one very obvious illustration of how people spend their money differently. (naturally mortgages and leasing of cars are all different etc.)

Interesting. I have just calculated our house value, our liquid assets, plus a pension pot (already retired, so this is a private pension awaiting). It comes to 2.6% car to assets.Value of car, vs Value of house.

Both our cars work out at roughly 2.35%

The next street some houses are at around 20% I'd guess.

That's one very obvious illustration of how people spend their money differently. (naturally mortgages and leasing of cars are all different etc.)

Apart from my very first brand new car bought on a finance loan, I have bought all cars new, for cash, and kept for 10 plus years. The previous car for 19 years. I save up the money in-between.

My current car F30 335d is probably my last ICE, after that I will probably lease an EV when they mature a bit more, if I am still around and driving!

I've slowly become convinced that most people 'buying' these things are actors employed by the government to create the illusion of prosperity.

You see these property shows where a droopy and lumpen couple are told the house they really like is £250,000 more than the other one and they give an indifferent shrug.

I'm not buying it.

You see these property shows where a droopy and lumpen couple are told the house they really like is £250,000 more than the other one and they give an indifferent shrug.

I'm not buying it.

Pica-Pica said:

dundarach said:

An interesting comparison I've often wondered about is:

Value of car, vs Value of house.

Both our cars work out at roughly 2.35%

The next street some houses are at around 20% I'd guess.

That's one very obvious illustration of how people spend their money differently. (naturally mortgages and leasing of cars are all different etc.)

Interesting. I have just calculated our house value, our liquid assets, plus a pension pot (already retired, so this is a private pension awaiting). It comes to 2.6% car to assets.Value of car, vs Value of house.

Both our cars work out at roughly 2.35%

The next street some houses are at around 20% I'd guess.

That's one very obvious illustration of how people spend their money differently. (naturally mortgages and leasing of cars are all different etc.)

Apart from my very first brand new car bought on a finance loan, I have bought all cars new, for cash, and kept for 10 plus years. The previous car for 19 years. I save up the money in-between.

My current car F30 335d is probably my last ICE, after that I will probably lease an EV when they mature a bit more, if I am still around and driving!

https://www.pistonheads.com/gassing/topic.asp?h=0&...

https://www.pistonheads.com/gassing/topic.asp?h=0&...

https://www.pistonheads.com/gassing/topic.asp?h=0&...

Some notable legends on those though - thelostboy in particular

Gassing Station | Car Buying | Top of Page | What's New | My Stuff