Taycan 4S Cross Turismo

Discussion

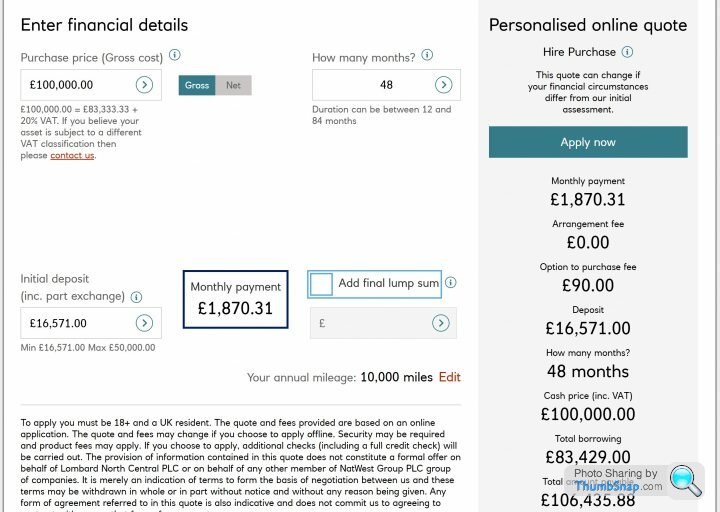

Prompted by the Interstellar I did some on line hunting.

Most of the online quotes are fill your details in and we'll get back to you (i've filled a couple in), however Lombard aren't, you actually get some numbers.

The following looks very appealing, 4 year's HP full ownership at 48 months.

I found it here for those interested.

https://www.lombard.co.uk/assets/business-car-fina...

Balloon options are available, but when I added those the total payable increased a noticeable amount.

Most of the online quotes are fill your details in and we'll get back to you (i've filled a couple in), however Lombard aren't, you actually get some numbers.

The following looks very appealing, 4 year's HP full ownership at 48 months.

I found it here for those interested.

https://www.lombard.co.uk/assets/business-car-fina...

Balloon options are available, but when I added those the total payable increased a noticeable amount.

Edited by 21ATS on Saturday 29th May 21:47

It usually shows the apr on the right. Mine is 3.8 but not sure on 100k. Is it about 6.9%?

You seem to get a better rate online than talking to their account manager too. I went that route and they couldn’t match online.

You seem to get a better rate online than talking to their account manager too. I went that route and they couldn’t match online.

- ***

Edited by interstellar on Sunday 30th May 00:56

All comes down to what its worth after 4 years and 40k miles.

PCH costs over the term on a 4S with £12k of options comes in at around £1375 a month or £66k over the term, so the HP car would need to be worth £50k+ for it to be financially worthwhile, and to balance out the significant additional outlay over those 4 years I'd be wanting £55-60k back personally.

Not sure how realistic that is on a car listing at £88k before options, especially in the mad world of BEV's?

PCH costs over the term on a 4S with £12k of options comes in at around £1375 a month or £66k over the term, so the HP car would need to be worth £50k+ for it to be financially worthwhile, and to balance out the significant additional outlay over those 4 years I'd be wanting £55-60k back personally.

Not sure how realistic that is on a car listing at £88k before options, especially in the mad world of BEV's?

SWoll said:

All comes down to what its worth after 4 years and 40k miles.

PCH costs over the term on a 4S with £12k of options comes in at around £1375 a month or £66k over the term, so the HP car would need to be worth £50k+ for it to be financially worthwhile, and to balance out the significant additional outlay over those 4 years I'd be wanting £55-60k back personally.

Not sure how realistic that is on a car listing at £88k before options, especially in the mad world of BEV's?

The intention is 5-6 year ownership window as realistically I'm doing 5-6K miles a year.PCH costs over the term on a 4S with £12k of options comes in at around £1375 a month or £66k over the term, so the HP car would need to be worth £50k+ for it to be financially worthwhile, and to balance out the significant additional outlay over those 4 years I'd be wanting £55-60k back personally.

Not sure how realistic that is on a car listing at £88k before options, especially in the mad world of BEV's?

Factor in your tax rebates and check your figures.

You're working 48 x £1,375 and arriving at 66K. Is there no deposit? Does this include vat or at least 50% of vat after offset?

You need to look at this globally, which Is why I'm still crunching numbers.

Edited by 21ATS on Sunday 30th May 10:09

21ATS said:

SWoll said:

All comes down to what its worth after 4 years and 40k miles.

PCH costs over the term on a 4S with £12k of options comes in at around £1375 a month or £66k over the term, so the HP car would need to be worth £50k+ for it to be financially worthwhile, and to balance out the significant additional outlay over those 4 years I'd be wanting £55-60k back personally.

Not sure how realistic that is on a car listing at £88k before options, especially in the mad world of BEV's?

The intention is 5-6 year ownership window as realistically I'm doing 5-6K miles a year.PCH costs over the term on a 4S with £12k of options comes in at around £1375 a month or £66k over the term, so the HP car would need to be worth £50k+ for it to be financially worthwhile, and to balance out the significant additional outlay over those 4 years I'd be wanting £55-60k back personally.

Not sure how realistic that is on a car listing at £88k before options, especially in the mad world of BEV's?

Factor in your tax rebates and check your figures.

You're working 48 x £1,375 and arriving at 66K. Is there no deposit? Does this include vat or at least 50% of vat after offset?

You need to look at this globally, which Is why I'm still crunching numbers

Edited by 21ATS on Sunday 30th May 10:09

Those are straight PCH (with VAT) numbers from Hitachi Capital for a 1 + 47 10k mile per year deal on a car with £12k of options (£265 extra per month).

https://leasing.com/independent-brokers/hitachi-ca...

For 5k miles per year the total cost drops by approx £4k over the term.

The big question will always be residual value and your appetite for risk in the fast evolving BEV marketplace. With the release of he ETron GT, EQS, updated Model S and general weak residuals on premium EV's (look at the numbers on the iPace, EQC and ETron SUV) who knows what a first gen Taycan will be worth in 4-5 years?

Edited by SWoll on Sunday 30th May 11:29

You make a good point.

Lots of talk on here of ensuring flexibility, I.e the ability to buy the car at end of the term. As it could be considerably more expensive to start again in 36/48months when any tax benefits have been reduced.

However, part of me feels that in 3-5yrs the EV market would have changed drastically. Thus as you say will a gen 1 Taycan with mileage, in need of a warranty renewal and half way through its battery warranty be worth anything?

I personally get bored of cars after 2/3yrs, so I’m not really fussed about the option to buy. Thus will probably go down the lease route and keep it simple and know exactly where I stand at all times.

Lots of talk on here of ensuring flexibility, I.e the ability to buy the car at end of the term. As it could be considerably more expensive to start again in 36/48months when any tax benefits have been reduced.

However, part of me feels that in 3-5yrs the EV market would have changed drastically. Thus as you say will a gen 1 Taycan with mileage, in need of a warranty renewal and half way through its battery warranty be worth anything?

I personally get bored of cars after 2/3yrs, so I’m not really fussed about the option to buy. Thus will probably go down the lease route and keep it simple and know exactly where I stand at all times.

SWoll said:

I'm comparing personal HP with PCH as per the previous post.

Those are straight PCH (with VAT) numbers from Hitachi Capital for a 1 + 47 10k mile per year deal on a car with £12k of options (£265 extra per month).

https://leasing.com/independent-brokers/hitachi-ca...

For 5k miles per year the total cost drops by approx £4k over the term.

The big question will always be residual value and your appetite for risk in the fast evolving BEV marketplace. With the release of he ETron GT, EQS, updated Model S and general weak residuals on premium EV's (look at the numbers on the iPace, EQC and ETron SUV) who knows what a first gen Taycan will be worth in 4-5 years?

This is why it's good to talk through these things and get a different point of view. The residual sure is a complete unknown.Those are straight PCH (with VAT) numbers from Hitachi Capital for a 1 + 47 10k mile per year deal on a car with £12k of options (£265 extra per month).

https://leasing.com/independent-brokers/hitachi-ca...

For 5k miles per year the total cost drops by approx £4k over the term.

The big question will always be residual value and your appetite for risk in the fast evolving BEV marketplace. With the release of he ETron GT, EQS, updated Model S and general weak residuals on premium EV's (look at the numbers on the iPace, EQC and ETron SUV) who knows what a first gen Taycan will be worth in 4-5 years?

Edited by SWoll on Sunday 30th May 11:29

I've run through your numbers above and get the following assuming I'm doing this right.

£66,000 48 month total cost incl VAT.

Minus 50% VAT reclaimed (£5,500) = £60,500

Offset against CT at an average of 20% over the term (£12,100)

Leaves you with a 4 year cost of £48,400 then hand it back.

vs the example I run above as follows:-

£16,751 Deposit + 48 £1866.28 = £106,422.44

Assuming you're able to write down 50% initial capital cost and I assume this is on invoice price of £100,000. (so half of 19% of £100,000 = £9,500)

£106,422.44 - £9,500 = £96,922.44 and you own the car outright at year 4.

A difference of £48,522.44. <-------So that car needs to be worth this amount at year 4 to cost the same as Contract hire.

So it really only makes sense to buy if you're going to run the car for 5 or 6 years. At which point you're taking a step into the unknown on residuals and tech.

- Note - I am open to correction on any of the above numbers if an accountant is reading this!

Edited by 21ATS on Sunday 30th May 14:36

labstaR said:

We are only talking tax relief on these EV’s.

I still think the main priority is whether or not you actually want the car. Isn’t the range about 200m?

Suits me perfectly, My average journey is under a 20 mile round trip and for the 4 times a year I need to do a 300 mile round trip on the same day I have another car.I still think the main priority is whether or not you actually want the car. Isn’t the range about 200m?

Grr_Boris said:

Grr_Boris said:

Looking at ordering a CT 4S for end 2021/early 2022 delivery. Given a choice between Rear wheel steering and Torque vectoring plus, which would you choose, and why?! (Or neither?)

Any thoughts from those who have already driven / specc’d their cars?Thanks

Porsche Torque Vectoring Plus (PTV Plus): more agile self-steering

Porsche Torque Vectoring Plus (PTV Plus) uses an electronically controlled differential lock on the rear axle for variable distribution of the drive torque between the rear wheels. On the one hand, additional yaw torque can be generated on the rear axle by braking the inner wheel on the bend. This ensures that the vehicle's steering response is even more agile. On the other hand, it improves traction by specifically locking the differential when accelerating out of corners.

Rear axle steering: maximum steering precision and easier manoeuvring

Rear-axle steering is available as an option (standard in the Taycan Turbo S). This further increases comfort, driving safety and driving dynamics. The vehicle steers without delay and builds up lateral acceleration at the rear axle much sooner. The result is even more impressive steering precision.

At low speeds of up to about 50 km/h, the rear wheels steer in the opposite direction to the front wheels. The steering angle depends on the driving speed and is a maximum of 2.8 degrees. This virtual shortening of the wheelbase results in a more dynamic steering response when cornering. At the same time, manoeuvring is easier as the turning circle has been reduced by around 60 centimetres to 11.2 metres. In addition, with rear-axle steering, the Taycan automatically features Power Steering Plus with greater support for steering assistance at low speeds.

At speeds exceeding approximately 50 km/h, the rear wheels steer in the same direction as the front axle, again depending on the speed. The wheelbase is therefore virtually lengthened, thereby increasing stability, for example when changing lanes on the motorway.

https://newsroom.porsche.com/en/products/taycan/ch...

Edited by BorkBorkBork on Tuesday 1st June 03:30

A little update on what I'm learning about the tax situation on EV's.

I've now spoken with two accountants both of whom are explaining that the capital allowance write down for a pure EV is 100% in year one if you buy (Finance lease) as opposed to contract hire. The idea behind this is BIK takes care of the element of private use in the case of cars supplied through Ltd companies. Which of course is currently where the huge saving is for director/owners.

Making a percentage deduction (for private use) of the Capital allowance would be done in the case of Sole traders and Partnerships where no BIK taxation exists.

This swings it for us if it is indeed the case we can write down £19,000 per car in year one against CT (so we can effectively use our year one CT payment as the deposit on both cars - £38,000), if we intend to keep the car post 4 years due to relatively low mileage. With the residuals being unknown now there is an element of risk but we would have the option to sell at 4 years if it look liked the most appropriate choice.

Check with your own accountant, sometimes there seem to be different interpretations of how these reliefs work.

I've now spoken with two accountants both of whom are explaining that the capital allowance write down for a pure EV is 100% in year one if you buy (Finance lease) as opposed to contract hire. The idea behind this is BIK takes care of the element of private use in the case of cars supplied through Ltd companies. Which of course is currently where the huge saving is for director/owners.

Making a percentage deduction (for private use) of the Capital allowance would be done in the case of Sole traders and Partnerships where no BIK taxation exists.

This swings it for us if it is indeed the case we can write down £19,000 per car in year one against CT (so we can effectively use our year one CT payment as the deposit on both cars - £38,000), if we intend to keep the car post 4 years due to relatively low mileage. With the residuals being unknown now there is an element of risk but we would have the option to sell at 4 years if it look liked the most appropriate choice.

Check with your own accountant, sometimes there seem to be different interpretations of how these reliefs work.

In a rather different situation here.

FT employee, start a new role shortly which is going to take me squarely into the punitive tax band between £100-125k.

Octopus energy have recently launched their "Electric Dreams" salary sacrifice offering, and based on quotes if I sacrifice the £25k I should be able to get into a CT Turbo with plenty of options for a cost to me of £800 a month (what the additional £25k would be worth taken as salary).

I know it will affect pension contributions and fine with that, so overall looks like a no brainer assuming I can get it sorted and I'm not missing something obvious?

https://www.thisismoney.co.uk/money/cars/article-9...

https://www.octopusev.com/salary-sacrifice

FT employee, start a new role shortly which is going to take me squarely into the punitive tax band between £100-125k.

Octopus energy have recently launched their "Electric Dreams" salary sacrifice offering, and based on quotes if I sacrifice the £25k I should be able to get into a CT Turbo with plenty of options for a cost to me of £800 a month (what the additional £25k would be worth taken as salary).

I know it will affect pension contributions and fine with that, so overall looks like a no brainer assuming I can get it sorted and I'm not missing something obvious?

https://www.thisismoney.co.uk/money/cars/article-9...

https://www.octopusev.com/salary-sacrifice

21ATS said:

A little update on what I'm learning about the tax situation on EV's.

I've now spoken with two accountants both of whom are explaining that the capital allowance write down for a pure EV is 100% in year one if you buy (Finance lease) as opposed to contract hire. The idea behind this is BIK takes care of the element of private use in the case of cars supplied through Ltd companies. Which of course is currently where the huge saving is for director/owners.

Making a percentage deduction (for private use) of the Capital allowance would be done in the case of Sole traders and Partnerships where no BIK taxation exists.

This swings it for us if it is indeed the case we can write down £19,000 per car in year one against CT (so we can effectively use our year one CT payment as the deposit on both cars - £38,000), if we intend to keep the car post 4 years due to relatively low mileage. With the residuals being unknown now there is an element of risk but we would have the option to sell at 4 years if it look liked the most appropriate choice.

Check with your own accountant, sometimes there seem to be different interpretations of how these reliefs work.

Spoken to ours today. They are certain it’s full allowance if it’s an employee or director of a limited company. Personal use only comes into it for partners or sole traders.I've now spoken with two accountants both of whom are explaining that the capital allowance write down for a pure EV is 100% in year one if you buy (Finance lease) as opposed to contract hire. The idea behind this is BIK takes care of the element of private use in the case of cars supplied through Ltd companies. Which of course is currently where the huge saving is for director/owners.

Making a percentage deduction (for private use) of the Capital allowance would be done in the case of Sole traders and Partnerships where no BIK taxation exists.

This swings it for us if it is indeed the case we can write down £19,000 per car in year one against CT (so we can effectively use our year one CT payment as the deposit on both cars - £38,000), if we intend to keep the car post 4 years due to relatively low mileage. With the residuals being unknown now there is an element of risk but we would have the option to sell at 4 years if it look liked the most appropriate choice.

Check with your own accountant, sometimes there seem to be different interpretations of how these reliefs work.

Accountant pointed me to last paragraph on this page: https://www.gov.uk/capital-allowances/business-car...

BorkBorkBork said:

Spoken to ours today. They are certain it’s full allowance if it’s an employee or director of a limited company. Personal use only comes into it for partners or sole traders.

Accountant pointed me to last paragraph on this page: https://www.gov.uk/capital-allowances/business-car...

You have summed it up correctly. Private use adjustment doesn’t apply to companiesAccountant pointed me to last paragraph on this page: https://www.gov.uk/capital-allowances/business-car...

BorkBorkBork said:

Spoken to ours today. They are certain it’s full allowance if it’s an employee or director of a limited company. Personal use only comes into it for partners or sole traders.

Accountant pointed me to last paragraph on this page: https://www.gov.uk/capital-allowances/business-car...

Seems pretty clear from this. - So that's a buy for us rather than contract hire.Accountant pointed me to last paragraph on this page: https://www.gov.uk/capital-allowances/business-car...

Using cars outside your business

If you’re a sole trader or partner and you also use your car outside your business, calculate how much you can claim based on the amount of business use.

If your business provides a car for an employee or director you can claim capital allowances on the full cost. You may need to report it as a benefit if they use it personally.

Edited by 21ATS on Tuesday 1st June 22:29

Gassing Station | Porsche EVs | Top of Page | What's New | My Stuff