Taycan 4S Cross Turismo

Discussion

Lots of people talking about contract hire rates. Whilst I'm still waiting for a definitive answer from my account my personal "fag packet" calculations are telling me we should be buying these not renting them for three years.

Remember also that on a contract hire deal you'll only be able to reclaim 50% of the vat if there is any personal use whatsoever.

At £1,160+vat per month on a 6+35 deal through Porsche and assuming you're reclaiming half the vat you're paying £52K over three years, or half the value of the car.

Of course you can offset the non vat part against Corporation tax that's £47,560 x 19% = £9,036.

So the hire costs around £41,000 over three years on a £100K list price - ish. Assuming I'm calculating this correctly (always open to be corrected by someone better informed).

If you have to have a new car every three years or can't stomach the idea of running one of these out of warranty then that may be the way forward.

Buying it - I'm waiting for a quote on a Business Finance lease purchase through a broker for both our cars. I'm yet to fully understand how much we can write down in year one on asset value. The guy I'm doing the finance through (mentioned earlier in this thread) was taking delivery of his Taycan Turbo today. His idea is buying it and keeping it long term writing down is value over an extended period. I have to say this made more sense to me and suits my driving requirements.

I do so few miles, I don't even commute ( my business is in the grounds of my property) both my current vehicles which I bought new are 4 and 5.5 years old respectively, with just under 20,000 miles on each of them. So I tend to keep a car for 5 to 6 years minimum if I buy it new. It smooths out the depreciation curve and I get better value from my cars. I'm also fortunate that I don't have a compulsion to have the latest and greatest thing.

I feel with the reduction in moving parts on these EV's and a 20,000 mile/two year service interval then hiring one for three years makes no sense for me. Now if you're doing 15K to 20K miles a year this dynamic changes dramatically.

Has anyone else crunched these numbers yet and have a better grasp of which is the better way to go for your own circumstances?

Remember also that on a contract hire deal you'll only be able to reclaim 50% of the vat if there is any personal use whatsoever.

At £1,160+vat per month on a 6+35 deal through Porsche and assuming you're reclaiming half the vat you're paying £52K over three years, or half the value of the car.

Of course you can offset the non vat part against Corporation tax that's £47,560 x 19% = £9,036.

So the hire costs around £41,000 over three years on a £100K list price - ish. Assuming I'm calculating this correctly (always open to be corrected by someone better informed).

If you have to have a new car every three years or can't stomach the idea of running one of these out of warranty then that may be the way forward.

Buying it - I'm waiting for a quote on a Business Finance lease purchase through a broker for both our cars. I'm yet to fully understand how much we can write down in year one on asset value. The guy I'm doing the finance through (mentioned earlier in this thread) was taking delivery of his Taycan Turbo today. His idea is buying it and keeping it long term writing down is value over an extended period. I have to say this made more sense to me and suits my driving requirements.

I do so few miles, I don't even commute ( my business is in the grounds of my property) both my current vehicles which I bought new are 4 and 5.5 years old respectively, with just under 20,000 miles on each of them. So I tend to keep a car for 5 to 6 years minimum if I buy it new. It smooths out the depreciation curve and I get better value from my cars. I'm also fortunate that I don't have a compulsion to have the latest and greatest thing.

I feel with the reduction in moving parts on these EV's and a 20,000 mile/two year service interval then hiring one for three years makes no sense for me. Now if you're doing 15K to 20K miles a year this dynamic changes dramatically.

Has anyone else crunched these numbers yet and have a better grasp of which is the better way to go for your own circumstances?

Also - what do you "get" for the interior leather upgrade? I actually like the Black/Chalk beige interior which is one of the no cost options, I think it goes nicely with the Cherry paint. It is available as an extra with the nearly £3K in uplift.

I understand you get the dash trimmed and the door cappings but is there anything else, is it a "better" quality leather or something?

I'm actually looking forward to seeing one of these in the flesh. Tonbridge are expecting showroom models to start arriving in July so we should get a chance to have a better look.

I understand you get the dash trimmed and the door cappings but is there anything else, is it a "better" quality leather or something?

I'm actually looking forward to seeing one of these in the flesh. Tonbridge are expecting showroom models to start arriving in July so we should get a chance to have a better look.

BorkBorkBork said:

We are buying. Deduct the full cost from profits with the first year allowance.

This is also my preferred choice, however how much are you deducting for private use from the year one allowance? It's that part I'm struggling with.You realise you can't write down 100% of the cost unless it's a pool vehicle and is never parked at your house right?

My understanding of this is also that when the vehicle is sold you have to refund the relevant amount of CT against the sale price at the time. Hence my choice to keep long term.

Edited by 21ATS on Friday 28th May 19:54

JJMatrixx said:

Surely when you come to sell you have a CGT balancing charge so net net, this really isn't as good as you think it is.

Lease will give you a 1-2% BIK, 50% VAT claim and payments deductible for Corporation Tax.

When you do the maths and are exposed to the depreciation on them, add in the cost of finance if you have that, and there's zero chance of buying this car being cheaper than leasing it.

It's this I'm still trying to figure out.Lease will give you a 1-2% BIK, 50% VAT claim and payments deductible for Corporation Tax.

When you do the maths and are exposed to the depreciation on them, add in the cost of finance if you have that, and there's zero chance of buying this car being cheaper than leasing it.

The trouble is we don't know what the depreciation curve of this car is, there's not enough data. Plus I intend to keep the car for some years. Maybe up to 7. Buying then stacks up as far as I can work out. But I'm a low mile user.

I'm yet to receive firm figures from either Porsche or my broker for the exact specs we've ordered, once I do I'll do some number crunching.

I think being able to keep our options open makes sense. I have zero doubt that once HMRC realise that this is actually a genuine benefit like it used it be, the door will be firmly closed. To that end being able to claim in full in year one has it's upsides.

Lets not forget though that the real benefit here is being able to buy within the realms of your business and not having to make a purchase using money removed from your company on which you've paid 40% tax before you even buy a car privately.

My Audi daily went for a service and MOT on Thursday, it's 4 year anniversary. It's covered just under 20,000 miles in that time, but only 3,000 in the last 12 months due to the lockdowns. I usually do around 6k-7k miles a year in each of my two cars. This year I did less than 5k between them.

So it seems paying for an 8K or 10K mile per year contract hire a bit daft in my case.

I don't think there's a one size fit's all solution here. For a user needing north of 15K+ miles per year I think contract hire might actually stack up.

I think being able to keep our options open makes sense. I have zero doubt that once HMRC realise that this is actually a genuine benefit like it used it be, the door will be firmly closed. To that end being able to claim in full in year one has it's upsides.

Lets not forget though that the real benefit here is being able to buy within the realms of your business and not having to make a purchase using money removed from your company on which you've paid 40% tax before you even buy a car privately.

My Audi daily went for a service and MOT on Thursday, it's 4 year anniversary. It's covered just under 20,000 miles in that time, but only 3,000 in the last 12 months due to the lockdowns. I usually do around 6k-7k miles a year in each of my two cars. This year I did less than 5k between them.

So it seems paying for an 8K or 10K mile per year contract hire a bit daft in my case.

I don't think there's a one size fit's all solution here. For a user needing north of 15K+ miles per year I think contract hire might actually stack up.

You can't use PCP as a business anyway. It's personal finance and can only be done in a oersonal status.

A limited company has to use business finance lease with a balloon. Or HP. The difference being with BFL is the balloon isn't guaranteed and there's no option to hand back. You're committed to the full contract value.

A limited company has to use business finance lease with a balloon. Or HP. The difference being with BFL is the balloon isn't guaranteed and there's no option to hand back. You're committed to the full contract value.

Prompted by the Interstellar I did some on line hunting.

Most of the online quotes are fill your details in and we'll get back to you (i've filled a couple in), however Lombard aren't, you actually get some numbers.

The following looks very appealing, 4 year's HP full ownership at 48 months.

I found it here for those interested.

https://www.lombard.co.uk/assets/business-car-fina...

Balloon options are available, but when I added those the total payable increased a noticeable amount.

Most of the online quotes are fill your details in and we'll get back to you (i've filled a couple in), however Lombard aren't, you actually get some numbers.

The following looks very appealing, 4 year's HP full ownership at 48 months.

I found it here for those interested.

https://www.lombard.co.uk/assets/business-car-fina...

Balloon options are available, but when I added those the total payable increased a noticeable amount.

Edited by 21ATS on Saturday 29th May 21:47

SWoll said:

All comes down to what its worth after 4 years and 40k miles.

PCH costs over the term on a 4S with £12k of options comes in at around £1375 a month or £66k over the term, so the HP car would need to be worth £50k+ for it to be financially worthwhile, and to balance out the significant additional outlay over those 4 years I'd be wanting £55-60k back personally.

Not sure how realistic that is on a car listing at £88k before options, especially in the mad world of BEV's?

The intention is 5-6 year ownership window as realistically I'm doing 5-6K miles a year.PCH costs over the term on a 4S with £12k of options comes in at around £1375 a month or £66k over the term, so the HP car would need to be worth £50k+ for it to be financially worthwhile, and to balance out the significant additional outlay over those 4 years I'd be wanting £55-60k back personally.

Not sure how realistic that is on a car listing at £88k before options, especially in the mad world of BEV's?

Factor in your tax rebates and check your figures.

You're working 48 x £1,375 and arriving at 66K. Is there no deposit? Does this include vat or at least 50% of vat after offset?

You need to look at this globally, which Is why I'm still crunching numbers.

Edited by 21ATS on Sunday 30th May 10:09

SWoll said:

I'm comparing personal HP with PCH as per the previous post.

Those are straight PCH (with VAT) numbers from Hitachi Capital for a 1 + 47 10k mile per year deal on a car with £12k of options (£265 extra per month).

https://leasing.com/independent-brokers/hitachi-ca...

For 5k miles per year the total cost drops by approx £4k over the term.

The big question will always be residual value and your appetite for risk in the fast evolving BEV marketplace. With the release of he ETron GT, EQS, updated Model S and general weak residuals on premium EV's (look at the numbers on the iPace, EQC and ETron SUV) who knows what a first gen Taycan will be worth in 4-5 years?

This is why it's good to talk through these things and get a different point of view. The residual sure is a complete unknown.Those are straight PCH (with VAT) numbers from Hitachi Capital for a 1 + 47 10k mile per year deal on a car with £12k of options (£265 extra per month).

https://leasing.com/independent-brokers/hitachi-ca...

For 5k miles per year the total cost drops by approx £4k over the term.

The big question will always be residual value and your appetite for risk in the fast evolving BEV marketplace. With the release of he ETron GT, EQS, updated Model S and general weak residuals on premium EV's (look at the numbers on the iPace, EQC and ETron SUV) who knows what a first gen Taycan will be worth in 4-5 years?

Edited by SWoll on Sunday 30th May 11:29

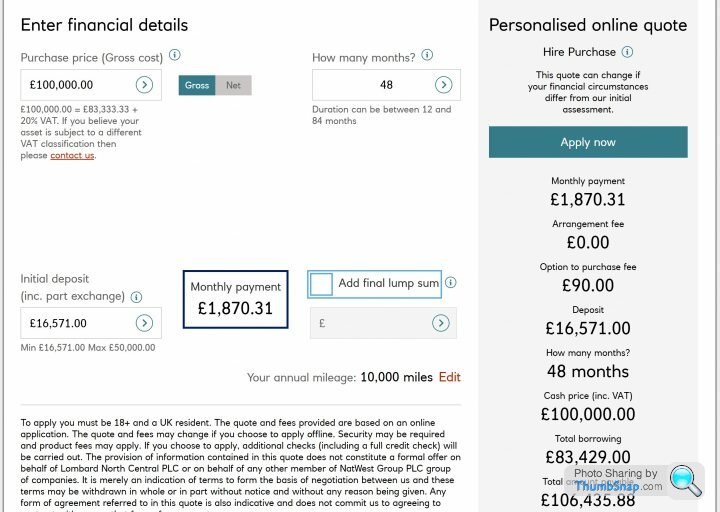

I've run through your numbers above and get the following assuming I'm doing this right.

£66,000 48 month total cost incl VAT.

Minus 50% VAT reclaimed (£5,500) = £60,500

Offset against CT at an average of 20% over the term (£12,100)

Leaves you with a 4 year cost of £48,400 then hand it back.

vs the example I run above as follows:-

£16,751 Deposit + 48 £1866.28 = £106,422.44

Assuming you're able to write down 50% initial capital cost and I assume this is on invoice price of £100,000. (so half of 19% of £100,000 = £9,500)

£106,422.44 - £9,500 = £96,922.44 and you own the car outright at year 4.

A difference of £48,522.44. <-------So that car needs to be worth this amount at year 4 to cost the same as Contract hire.

So it really only makes sense to buy if you're going to run the car for 5 or 6 years. At which point you're taking a step into the unknown on residuals and tech.

- Note - I am open to correction on any of the above numbers if an accountant is reading this!

Edited by 21ATS on Sunday 30th May 14:36

labstaR said:

We are only talking tax relief on these EV’s.

I still think the main priority is whether or not you actually want the car. Isn’t the range about 200m?

Suits me perfectly, My average journey is under a 20 mile round trip and for the 4 times a year I need to do a 300 mile round trip on the same day I have another car.I still think the main priority is whether or not you actually want the car. Isn’t the range about 200m?

A little update on what I'm learning about the tax situation on EV's.

I've now spoken with two accountants both of whom are explaining that the capital allowance write down for a pure EV is 100% in year one if you buy (Finance lease) as opposed to contract hire. The idea behind this is BIK takes care of the element of private use in the case of cars supplied through Ltd companies. Which of course is currently where the huge saving is for director/owners.

Making a percentage deduction (for private use) of the Capital allowance would be done in the case of Sole traders and Partnerships where no BIK taxation exists.

This swings it for us if it is indeed the case we can write down £19,000 per car in year one against CT (so we can effectively use our year one CT payment as the deposit on both cars - £38,000), if we intend to keep the car post 4 years due to relatively low mileage. With the residuals being unknown now there is an element of risk but we would have the option to sell at 4 years if it look liked the most appropriate choice.

Check with your own accountant, sometimes there seem to be different interpretations of how these reliefs work.

I've now spoken with two accountants both of whom are explaining that the capital allowance write down for a pure EV is 100% in year one if you buy (Finance lease) as opposed to contract hire. The idea behind this is BIK takes care of the element of private use in the case of cars supplied through Ltd companies. Which of course is currently where the huge saving is for director/owners.

Making a percentage deduction (for private use) of the Capital allowance would be done in the case of Sole traders and Partnerships where no BIK taxation exists.

This swings it for us if it is indeed the case we can write down £19,000 per car in year one against CT (so we can effectively use our year one CT payment as the deposit on both cars - £38,000), if we intend to keep the car post 4 years due to relatively low mileage. With the residuals being unknown now there is an element of risk but we would have the option to sell at 4 years if it look liked the most appropriate choice.

Check with your own accountant, sometimes there seem to be different interpretations of how these reliefs work.

BorkBorkBork said:

Spoken to ours today. They are certain it’s full allowance if it’s an employee or director of a limited company. Personal use only comes into it for partners or sole traders.

Accountant pointed me to last paragraph on this page: https://www.gov.uk/capital-allowances/business-car...

Seems pretty clear from this. - So that's a buy for us rather than contract hire.Accountant pointed me to last paragraph on this page: https://www.gov.uk/capital-allowances/business-car...

Using cars outside your business

If you’re a sole trader or partner and you also use your car outside your business, calculate how much you can claim based on the amount of business use.

If your business provides a car for an employee or director you can claim capital allowances on the full cost. You may need to report it as a benefit if they use it personally.

Edited by 21ATS on Tuesday 1st June 22:29

SWoll said:

Makes for a very expensive 3 year lease cost. Are we really supposed to believe that a car with £15k of options is going to be worth no more than a standard car at 3 years/30k miles. Surely even 33% retained value would be more like the truth?

We've weighed up the options and certainly for us buying the cars makes sense and we're aiming for a 5 year term of ownership, possibly longer. To that end we didn't really want a balloon payment and straight HP makes more sense. We'll deposit the amount equal to the CT relief in year one on the grounds we would have been paying that out anyhow. I'm comfortable taking a punt that these cars will have a reasonable residual. It may work out that at year 4 there's so much equity if they hold value well that we could roll them into new ones. Subject to the state of tax at the time.

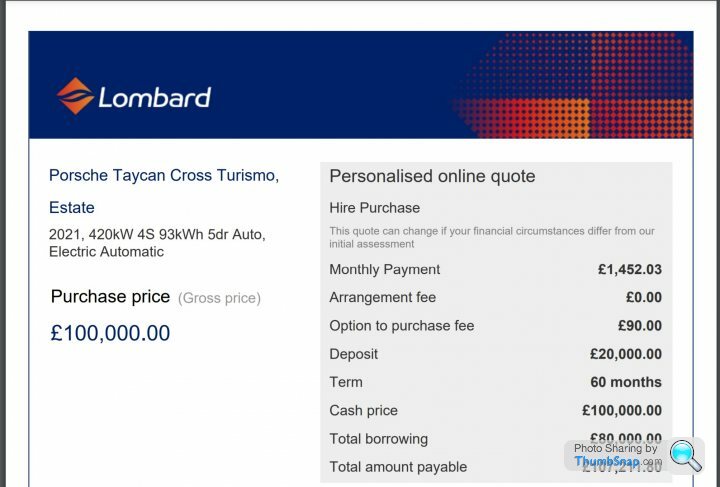

I got this quote off the Lombard website today. I think this compares favourably to lease deals.

ds666 said:

I must say purchasing does look attractive based on the Lombard finance .

My big worry about buying now is that battery tech is getting better with every new launch ( e.g. i4 BMW ) , so range getting better and choice is also increasing by the week .

In 5 years the Porsche , great as it is now , may be "old hat " .

The way I see it is that it provides us more options with the only negatives being if the residual value tanks or there's a massive rethink in taxation. Worst case scenario is then we own the cars.My big worry about buying now is that battery tech is getting better with every new launch ( e.g. i4 BMW ) , so range getting better and choice is also increasing by the week .

In 5 years the Porsche , great as it is now , may be "old hat " .

I phoned Lombard this morning to confrim the apr - it's 3.4%

I think I'm going to struggle to beat that.

JJMatrixx said:

I went into my OPC today...a few things clarified:

1. They said the 150kw DC charger is fairly essential as Porsches are the only cars to run on 800V as it’s better for heat reduction. So if you don’t spec this and turn up to a normal 50kw charger, it will be 400V and the car won’t charge.

2. The charge pack you get as standard is a 3 pin and a 5 pin. It’s not waterproof so they suggest that’s plugged in, in the garage, then get the 7m cable so you can run it to the car outside. Of course, if you have a wall box then it’s just a usual Type 2 (I think) cable.

3. Without Sport +, there’s a sport button on the steering wheel. He thought Sport+ would do very little on an EV.

4. Their PCP figures were nearly £5k more over the term than my lease deal.

1. That sounds like an absolute must, I'll have a chat with my dealer and add it if it is that important.1. They said the 150kw DC charger is fairly essential as Porsches are the only cars to run on 800V as it’s better for heat reduction. So if you don’t spec this and turn up to a normal 50kw charger, it will be 400V and the car won’t charge.

2. The charge pack you get as standard is a 3 pin and a 5 pin. It’s not waterproof so they suggest that’s plugged in, in the garage, then get the 7m cable so you can run it to the car outside. Of course, if you have a wall box then it’s just a usual Type 2 (I think) cable.

3. Without Sport +, there’s a sport button on the steering wheel. He thought Sport+ would do very little on an EV.

4. Their PCP figures were nearly £5k more over the term than my lease deal.

2. I feel it's pretty fundamental to get a wall box installed at home if you have one of these cars (if that's practical of course). I have a feeling the extension cable slows down the charge rate - you might want to check that.

3. My understand was Sport+ was where the "overboost" was accessed for launch starts. In so much as the car isn't using all the available power in any of the other modes but "full Banana Mode" was accessed in Sport +?

4. Get quotes from places other than Porsche (VWFS). The deal I got through Lombard was untouchable.

On a seperate point I have discovered I may have three phase leccy entering my house and was mildly excited that there's a chance I could fit a 22kw charger at home, only to notice when looking at the 150kw DC charger specs above there is another option below for 22KW AC for on board three phase charging, at a further £1200.

I know Porsche gouge with options, I get that from the outset but if the 150kw charge thingy is so absolutely imporant and future proofing the car that really should be in the base spec considering the 800v battery architecture is designed for it. Much of the other stuff is personal taste, but fundmentally being able to charge the car, that's really not an option.

BorkBorkBork said:

I’ve specc’d the DC charger option, but as stated above, only as a cheap arse covering exercise. Most 150kw UK charging points work off 960v I believe. On the continent it might be more useful by all accounts.

More here: https://www.drivingelectric.com/comment/1683/optio...

Actually that's a very good article and reflects my position exactly. Up until 3 weeks ago I had zero interest in Electric cars, particualrly Tesla's, one You Tube video on the Taycan Cross Turismo and a lesson in company car tax rates and we had two on order.More here: https://www.drivingelectric.com/comment/1683/optio...

Edited by BorkBorkBork on Saturday 5th June 14:33

I'm scratching my head about having to pay for a cable to charge my car. It's Porsche, it is what it is and I guess and it's unlikely to change.

And yes, paying for folding mirrors grated a little with me also on my £100,000 car spec.

Gassing Station | Porsche EVs | Top of Page | What's New | My Stuff