AML - Stock Market Listing

Discussion

Ghini said:

https://www.autocar.co.uk/car-news/new-cars/aston-...

Finally some information on what direction AM is taking for their hybrids; The obvious direction with Mercedes tech, so no Lucid or Geely tech for the Hybrids.

Finally some information on what direction AM is taking for their hybrids; The obvious direction with Mercedes tech, so no Lucid or Geely tech for the Hybrids.

That article date is 26 July 2023.

Lucid cars are battery only. I don't know whether Geely build any PHEVs.

PHEV batteries take up a considerable amount of space, obviously less than an EV.

One Mercedes model, which is available in both IC and PHEV forms, loses one third of its boot space, for the provision of PHEV batteries under the boot floor.

Sports and GT cars do not have much spare space to start with, so it will be interesting to see how PHEV technology is engineered into existing models.

Thank you for your detailed reply, LT

LooneyTunes said:

... For proper sized facilities someone looking at it with a view to providing a facility would typically get much greater level of insight/access than simply looking at the published accounts. Depending on the type of facility being considered you might actually want to get under the skin of the business model to quite a significant degree. For example, factors such as the reality behind statements around order book (inc. geography/currency), ownership structure, investor support and existing obligations would be areas to concentrate on plus perhaps some more specific details if the type of facility necessitated it.

Prospect of recovery in the event of default should feature too, so there's a fair amount of work often to be done when looking at collateralisation. One of the big challenges in the automotive industry, especially in the UK, is that the history isn't great and there's not really enough collateral for all who might want it. That has sometimes resulted in firms looking for alternative ways to raise money leveraging the assets they have. That can add further complications to traditional debt issuance. ...

That is an interesting aspect.

Over the years, this topic must have revealed a few helpful tips.

Expect you remember pre IPO, when to boost excitement, a record number of new model announcements took place and a great deal of other hype became obvious to the posters here, even including one isolated year of declared pre-tax profit (coincidence?). That was subsequently almost totally reversed, when the sale of intellectual property and tooling, became a bad debt.

Repeated statements of growth, profitability and intending to use the capital raised to increase profitability (which they measure by EBITDA !). Have tansformed not just the Company, but even the industry. Sunshine just over the hirizon. The best one of course was, "Let me be crystal-clear, black-and-white: we do not need money." I think it was £575 million that was raised just months later (and then spent). Capital raising requires preparation time, so people must have known what is planned.

I think the loan notes are secured against property, therefore reducing the lenders risk.

I was puzzled, that the first time for AML, the various loan note debts had identical maturity dates. If there happened to be a coinciding economic crisis, or loss of confidence, the risk would be game over.

Aston Martin's battery electric vehicle partner is Lucid. It is therefore interesting to follow the (stuttering) progress of Lucid.

Their results for 2023 have been announced.

'On a full-year basis, the Company produced 8,428 vehicles, meeting the higher end of the 2023 annual production guidance of 8,000 to 8,500 vehicles, and delivered 6,001 vehicles in 2023.

Lucid today also announced its 2024 annual production guidance of approximately 9,000 vehicles, and will continue to prudently manage and adjust production to meet sales and delivery needs.'

I am assuming produced means built, whereas delivered means sold.

Therefore, they seem pleased that building 8,428 cars met their target,

but selling 6,001 cars, no comment about that.

So what about the remaining 2,427 cars. Have they just been dumped in the factory car park ?

Revenue

2022 $608.2 million

2023 $595.3 million

Pre-tax Loss

2022 $1,304.1 million

2023 $2,827.4 million

Staggering.

CEO's explanation.

"Lucid is investing for the long term in technology, manufacturing and partnerships to further solidify our place in the market as the premier luxury EV brand in the world," said Peter Rawlinson, Lucid's CEO and CTO. "In 2023, we made our first strategic technology arrangement, gained market share, completed the Air lineup, and unveiled Gravity. As we start 2024, I'm very excited about the year ahead and beyond. We are entering the next transformational phase of the Lucid vehicle lineup and are laser-focused on growth."

"I'd like to echo Peter's excitement as we start the year," said Gagan Dhingra, Lucid's Interim Chief Financial Officer and Principal Accounting Officer. "We outpaced our total addressable market and made headway with our cost optimization programs – a key strategic priority for the Company. I'm excited about the future as Gravity start of production is scheduled for late 2024 and the start of production for our high-volume Midsize platform is scheduled for late 2026."

(I very nearly mention losing all that money, but I think I got away with it.) -

One might ask, how long can this firm keep going like this, but no need, because there is an exteremly wealthy majority owner.

What do you make of it ?

SSO said:

Jon39 said:

Aston Martin's battery electric vehicle partner is Lucid. It is therefore interesting to follow the (stuttering) progress of Lucid.

Their results for 2023 have been announced.

'On a full-year basis, the Company produced 8,428 vehicles, meeting the higher end of the 2023 annual production guidance of 8,000 to 8,500 vehicles, and delivered 6,001 vehicles in 2023.

Lucid today also announced its 2024 annual production guidance of approximately 9,000 vehicles, and will continue to prudently manage and adjust production to meet sales and delivery needs.'

If my understanding from their statement is correct, they are unable to sell all the cars they are making.

Therefore on that basis, they could meet any production target guidance.

It they had say set guidance at 20,000, it would have just meant dumping 13,999 cars in the factory car park, rather than the 2,499 that are already there.

I might be misunderstanding their meaning of 'produced' and 'delivered', but surely target guidance should be on cars sold (wholesale), not just any number that they choose to build.

Anyway, overall it all looks pretty hopeless. Huge and increasing losses and with a nation population in the region of 300 million, who only wanted 6,001 of their cars. Warren Buffett would probably be coughing into his See's candy, if asked whether Lucid might be a good investment.

However, there does seem to be quite a close race, between Lucid and AML for total wholesale numbers.

An occasional look (don't waste your time) at the AML share chat forums, suggests that when a new model is annoucemed, it will be followed by Company profitability and a much higher share price.

Well, what has actually happened ?

2003 & 2005 .......... DB9 and Vantage introduced.

................................. The order book really was full at that time and record sales were achieved.

................................. Modest pre-tax profits were reported, but partly illusionary, because Ford were paying development costs.

2016 & 2018 ........... DB11 and Vantage introduced.

................................. Financial losses continued.

2023 & 2024 ........... DB12 and Vantage introduced.

................................. The chat forum consensus, is that it will be different this time.

................................. I would suggest, that they don't even know what has happened before.

................................. Several posters think the share price will soon increase, simply because it has fallen so far.

................................. Uncommon sense seems to be widespread. They are thinking about the share price and not the business.

Edited by Jon39 on Tuesday 27th February 08:48

If you would like to feel part of the results announcement tomorrow morning, you just need to register.

Title: Aston Martin Lagonda 2023 Full Year Results

Date: Wednesday, February 28, 2024

Time: 8:00 AM (GMT+00:00) United Kingdom Time

Duration: 60 minutes

https://www.astonmartinlagonda.com/investors/resul...

Click on, 'REGISTER TO WATCH HERE'.

It can be quite informative and entertaining.

'Politician's Answers' during the Q & A, have been noted before.

I watched the presentation this morning. Internet went slow motion, so missed some parts.

A few points that I did notice;

- Was the cash flow positive in Q4 as promised. - Think they were silent about that milestone being achieved.

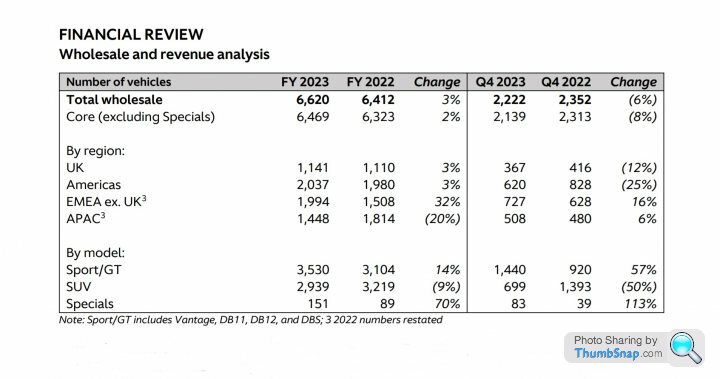

- Several mentions of very strong DBX 707 sales. - Check the overall SUV sales below (down 9% in 2023).

Think they said that soon, only the 707 version will be available.

- The CFO suggested that refinancing might not involve equity. The trend at present (higher interest rates) is to use equity, to reduce debt interest payments. We shall wait and see on that one. After hearing the question, I expected him to ignore, or be vague about that. Any anticipation of equity dilution can depress a share price.

There was much talk about a big sales increase in Sports/GT.

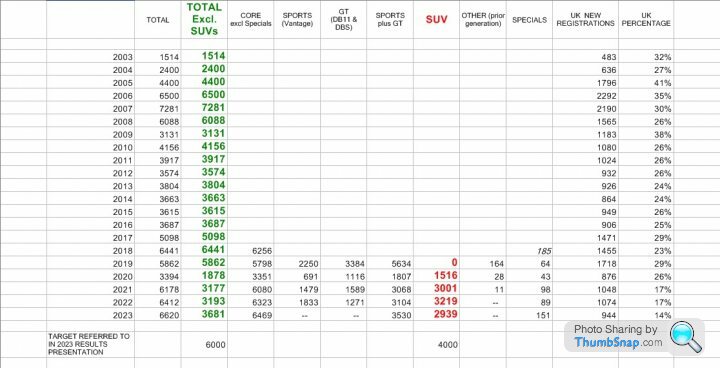

This is a category that has withered over the years. From the peak of 7281, it is now 3681. Thank goodness for the DBX.

As we have discussed, The new models are good, so if enough customers are willing to pay the higher margins, the target mentioned is now 6000.

60% new customers was frequently mentioned. Turn that around and of course any loss of existing customers, increases the percentage of new customers.

Some factual information below.

Sports and GT figures are no longer reported separately, therefore we cannot see Vantage sales.

(Tap/click to enlarge, then when open, repeat)

Edited by Jon39 on Wednesday 28th February 19:34

LooneyTunes said:

That's not a surprise. Many are struggling to raise equity in the current market without taking a serious caning on valuations.

Thank you LT.

Of course raising capital through equity solves the burden of interest payments, and Aston Martin have repeatedly done it in recent years, so to an outsider, they always made it appear easy and Mr. Stroll does spin a good line about sunshine over the horizon. At least they now have new models which have rightly been really well received, but even so, becoming profitable at EBITDA level is one thing, whereas Pre-tax is another huge leap.

I think there is $1,143,720,000 outstanding (part repayment in Oct 2022) for the Senior Secured Notes 10.5% Nov 2025.

When that was issued, the BoE base rate was 0.1% and the FX 1.32.

Economic conditions have of course changed considerably, so with that debt then agreed at 10.5%, how high do you think it could be, if it were to be refinanced now?

There must be a point, where companies become overwhelmed by their debt interest payments..

One example of refinancing this month;

$1,700,000,000 aggregate principal amount of guaranteed debt securities consisting of

(1) $850,000,000 5.834% Notes due 2031 (7 years) and

(2) $850,000,000 6.000% Notes due 2034 (10 years).

So there is a company paying rates now, which are far below the AML November 2020 rate.

As far as I know, the negotiations might have been routine, but that company has plenty of cashflow and reported 2023 revenue of

£27 billion, so in a completely different position compared to AML.

Edited by Jon39 on Wednesday 28th February 19:39

Kart16 said:

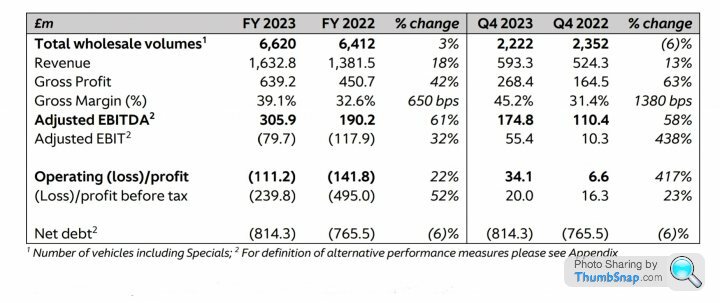

Please, can a member here who knows accounting clarify the passage from EDITDA to EBIT and then to profit loss before tax?

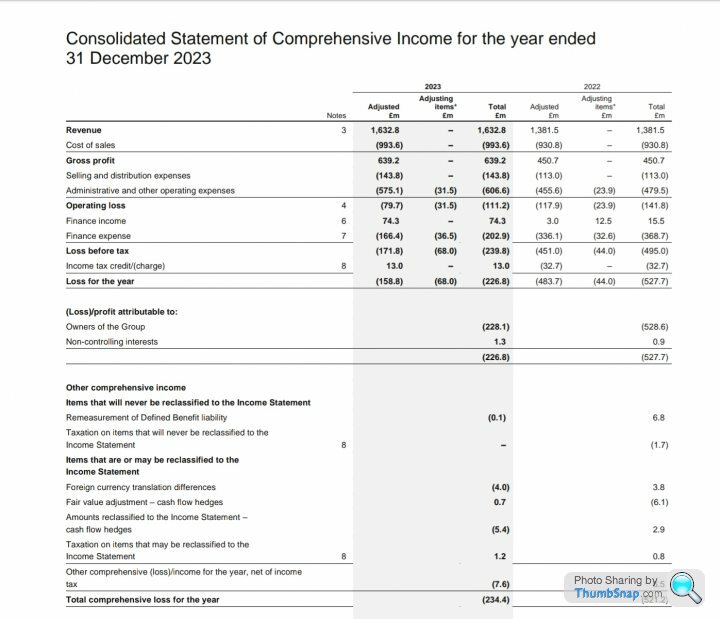

AFAIK (studied accounting a long time ago), AML had a total amortization plus depreciation of -385.6M (-305.9M-79.7M), correct? Then how do you arrive in -111.2M and -239.8M respectively? Thanks!!

AFAIK (studied accounting a long time ago), AML had a total amortization plus depreciation of -385.6M (-305.9M-79.7M), correct? Then how do you arrive in -111.2M and -239.8M respectively? Thanks!!

In the words of the late Mr. Charlie Munger, EBITDA and EBIT are (I don't like to say), but he despises the misuse of EBITDA.

Absolutely meaningless and frequently used by firms, trying to pretend they are profitable.

Here is the answer to your question, explained by (probably) the most successful investors in the world.

(Tap/click to enlarge and when open, repeat.)

Edited by Jon39 on Wednesday 28th February 20:53

Thank you SSO for your article.

When AML obtained their stock market listing, Andy Palmer had dreams of entry into the FTSE 100.

Probably in conjunction with that (grandios) expectation, they began quarterly reporting.

Now, from their point of view, half year reporting would seem much more suitable.

It would stop us analysing in such detail.

EXTRACT

'Positive FCF expected in H2’23

which was later revised to Positive FCF in Q4 2023. What AML delivered in Q4 2023 was -£63 mil. of Free Cash Flow. As misses go, this one is quite impressive, especially considering that the revised outlook to have positive FCF in Q4 2023 was issued in November. Just to make matters worse, FCF was actually worse in 2023 at a -£360 mil. than it was in 2022 (-£299 mil.). Positive Free Cash Flow is basically table stakes to be considered a heathy business and despite the latest promises that AML will now get there in the 2nd half of 2024, that still seems a long way off.'

This has been the general pattern throughout AMs history. First enjoy the cars, second worry about the financials. Spending more than earning would normally be disastrous for any business, but AM has always had an increasingly wonderful image and money has always been forthcoming in the hour of need.

Since the arrival of Mr Stroll, the continuous fund raising has been remarkable. Certainly a positive difference from the old days, where failure was followed by a fresh benefactor.

Like you, I had expected the next fund raising to be equity based rather than debt, but LooneyTunes, who I think might be involved in corporate debt markets, has pointed out that the equity route is extremely difficult at present. A shame because equity could considerably reduce the ongoing cost of debt.

The AML shareholders have been compliant up to now, presumably because Mr Stroll has "transformed" the Company and always forecasts growth, together with future profitability.

Edited by Jon39 on Monday 4th March 09:28

SSO said:

Looking back on the results again, perhaps the most shocking item is missing the lowered guidance that AML issued in Nov. Certainly in my past professional life, if you lowered guidance, you made sure the new number was one you would not only hit, but beat. How they messed that up is a real head scratcher.

Yes, that was strange.

There was only about one month remaining, so the directors must have had an accurate estimate of the December sales, especially as for one of those weeks, I presume production might have been stopped anyway.

I expect you consider the next debt refinancing, to be a very important transaction.

Do you have any guesses, as to what alternatives there might be ?

Hope it will not result in more USD loan notes, with even higher interest rates.

Do you know anything about the 2021 Long Term Incentive Plan?

I am wondering if it is an all-employee option scheme?

At least that would be fairer to employees, than the first one.

78,050 new ordinary shares are being issued, to be held by the Employee Benefit Trust, pending exercises.

Debt refinancing announced today.

Offer £1,140 million (equivalent) loan notes, maturity 2029.

And revolving credit facility agreement £170 million.

https://www.londonstockexchange.com/news-article/A...

Does (equivalent) mean the currency will be USD ?

Geely (minority Aston Martin) shareholder is a remarkable business.

Their first car was launched in 1999 and in 2023 had sales totalling 2.79 million cars.

Recently the have been fund raising, by floating several of their subsidiaries on the US stock market.

That has not been such a happy outcome though.

Full article here

https://archive.li/QuFyr

Thankyou4calling said:

So AM sold 6500 cars last year and 3000 were the DBX.

Obviously some bought the DBX but would've bought a sports car so allowing for some crossover I guess they would've sold maybe 4000 cars total without an SUV.

That's very concerning id say.

Obviously some bought the DBX but would've bought a sports car so allowing for some crossover I guess they would've sold maybe 4000 cars total without an SUV.

That's very concerning id say.

The table below (posted on the previous page), shows what you are referring to Simon. The green column.

If there had not been an Aston Martin SUV model, who knows what would have happened, because total sports car sales since the pandemic, have remained in the 3,000s.

It is perhaps unreasonable to compare with the AM sports car sales in 2006, 2007 and 2008.

Do you think buyers perhaps now have less desire for a 2 seater sports car?

We now see the fashion for SUVs dominating our roads. My son is of an age where keeping up with fashion might be expected, but he uses traditional estate cars. He considers some SUVs to just be jacked up estate cars, often with less accomodation space than might be expected. The huge wheel arches are one aspect that can reduce interior luggage space.

I don't know, but do you think the overall sports car market, is simply smaller than it was 15 years ago?

Aston Martin sometimes compare themselves with Ferrari, but we have to admit that Ferrari as a business, is unique ("buy 3 basic Ferraris first, then we might even think about considering you for a special. Even a hint about discount though and you're out").

AstonZagato said:

Well... I've just sold a Vanquish S and I am sort of thinking that I might buy a DBX and flip the Rangie to combine the two cars into one DBX.

I am sure that you will know a revised DBX is expected.AML indicated (in the recent results presentation) that the 707 will take over from the lower powered model.

Presumably the latest interiors will be incorporated.

Minglar said:

Great news.

Bearing in mind the prevailing base rates at the time of the last issue, very good that the interest rates remain almost unchanged.

There are some issues around 5%, but for the very big firms.

Minglar said:

Yes Jon, I would agree. The RNS was published after the U.K. market closed. There is also a split between US Dollars and Sterling which should help to reduce future FX implications. Combine this with no additional cash raise via equity then it should really be good news, at least in the short term. It will be interesting to see how the market reacts tomorrow morning. Fingers crossed. BRM.

The morning buyers were clearly confident, following news of the successful offer.

As the refinancing purely dealt with existing debt, presumably it is now important for the Company to resolve the consistent

negative cash flow.

Annual interest payments will total £116.8m (at FX 1.275).

The early repayment of existing Loan Notes debt was scheduled to be completed yesterday.

10.5% Loan Notes $1,226,235,041

15% Loan Notes $138,490,152

Total $1,364,725,193

The new debt now is;

Dollar Notes $960 million 10% Secured Notes 2029

Sterling Notes £400 million 10.375% Senior Secured Notes 2029

Total (at the present exchange rate) $1,468 million (or £1,156,million).

If my figures are correct and ignoring the fees involved to arrange the new Loan Notes, there will be about £80 million left over cash available to AML, as a result of the debt refinancing.

Total Loan Notes following the partial repayment on 11 Oct 2022 (using FX 1·27) totalled £1,051 million.

Early redemption amount paid on 21 Mar 2024 was $1,364,725,193·69 (£1075 million)

The 2024 new replacement Loan Notes (using FX 1·27) total £1,156 million.

Edited by Jon39 on Sunday 24th March 20:40

SSO said:

So debt has increase again....and they save about $5 mil. a year in interest. Other than extending the maturity date, not sure this has really changed much.

My arithmetic with the refinancing showed some extra money might (don't know cost of fees) have gone into the business 'till', but projecting forward from here, based on the last reported rate of cash outflow, how long will the present available cash last ?

Think the expected "fulsome fund raising", was stated as 2024 H1 or H2.

Gassing Station | Aston Martin | Top of Page | What's New | My Stuff