AML - Stock Market Listing

Discussion

RL17 said:

ball definitely rolling if you look at control of that company

good too see AML still being used

good too see AML still being used

Yes, I looked at the shareholder details.

Do you think that indicates Investindustrial might sell their entire holding, which would perhaps be the convention for that type of investor after this time period?

Some say announcement on Wednesday, when the 2018 Interim results are due.

https://news.sky.com/story/amp/aston-martin-roars-...

Edited by Jon39 on Tuesday 28th August 19:15

London Stock Exchange have been informed by AML of their intention to obtain a listing

Andy Palmer has just been interviewed on the Radio 4 Today programme.

He emphasised his point about AML being a car company, but also a luxury goods company and therefore is better placed to deal with economic changes.

He is certainly doing an excellent job, but do you think some of these comments are exaggerated?

In 2008 the Company was immediately badly hit by that economic downturn.

We do not yet know the IPO valuation, but is AML really worth more than these two consistantly profitable and dividend paying FTSE 100 companies, Marks and Spencer and Severn Trent?

Edited by Jon39 on Wednesday 29th August 09:26

murphyaj said:

IPO valuations are usually based not on current scale and profits, but on future potential. In it's current form, no Aston Martin is not worth more than those two companies. However M&S is a mature company with limited room for growth, in fact quite the opposite as the high street is in terminal decline and a utility company like Severn Trent effectively operates at a fixed scale. Aston Martin has huge potential to grow sales all around the globe, especially with the DBX. Whether it will fulfil that potential and become a money-making machine like Ferrari, or whether history will repeat itself and it will fall into terminal losses, that's where the risk comes in that is always with case with any IPO.

An excellent summary AJ, and my thoughts exactly.

You may have seen my topic, where UK quarterly sales of the DB9 and DB11 are compared.

The DB9 numbers are way ahead of the DB11.

The new Vantage quarterly comparison will be a tough one also, because of the original model's two year waiting list, but we will not know until next year, because production only began a couple of months ago.

In my opinion, the early (IPO) investors are effectively taking a bet on the DBX. Hopefully, if that sells as many as the Bentayga, the share price should be fine. Andy Palmer has been open about this, in his occasional comments about the DBX project becoming the financial support for sports cars.

It will be interesting to see how things go as a PLC.

It seems that there might be arrangements for AM customers to participate in the IPO. Hope that means owners, and not just dealer favourites.

We might all be able to meet at the AGM.

Edited by Jon39 on Wednesday 29th August 11:37

IanV12VSRs said:

I am not sure about your focus on U.K. sales Jon. To my thinking it only has relevance if the country mix and sales achieved in those countries remains the same if you are to take any trends from it. If they are not the same then what can you take from them?

For example, in the early days of the DB9 how many were sold in China, if any, compared with how much bigger the Chinese market is to the company now. Another way of thinking about it is how does the proportion of sales split between the U.K. and the ROW compare between the two periods. Do you have access to those figures?

For example, in the early days of the DB9 how many were sold in China, if any, compared with how much bigger the Chinese market is to the company now. Another way of thinking about it is how does the proportion of sales split between the U.K. and the ROW compare between the two periods. Do you have access to those figures?

Yes you are quite right Ian.

There is public access available for us to quarterly UK model sales, and the Company release annual information about total sales.

Other figure are quoted on a random basis, but my UK focus is because there is nothing else to go on. The UK market does though remain the biggest region for AML.

The ROW proportion you refer to, can therefore be calculated. I am away from the figures at present, but I don't think it has moved very much from around 70% export.

Various figures are also provided in the Annual Report, which can be seen on the the Companies House website (search Aston Martin Holdings UK Limited). For China, a big percentage sales increase was announced, but the numbers might perhaps be less than people think. 324 cars in 2017 (176 cars in 2016). The sales numbers mentioned for China by Mercedes-Benz and Volkswagen are staggering, but perhaps selling sports cars there is a different business.

JulianPH said:

HL call Aston "the world’s fastest-growing automotive brand". Surely this is a great big pile of crock from a regulated firm looking to earn from trading AM shares... Or are the number of units sold (historically) so low that the increase in recent years (on a percentage basis) really is that great?

Yes, of course statistics can be used in imaginative ways.

In fact that HL reference might have originated from an Aston Martin press release.

Peak sales for Aston Martin was during the Ford ownership era. (From memory) about 7,200 just before the economic crash, then a steady decline until the 2017 increase (5,098) up from 3,687 in 2016.

As you know, IPOs need careful timing. As a financial man, this article will be of interest to you.

https://www.bloomberg.com/view/articles/2018-05-24...

Man maths comes to mind. Development spending becomes an asset on the balance sheet, and reported profits increase. Fair enough, but the proportion involved does seem very stretched in comparison to other car manufacturers. I wonder how far the new investors will look into all this?

RobDown said:

The Registration document is available on the Corporate section of the Aston Martin website. Prospectus scheduled for Dec 20th

I would be interested to look through The Registration Document Rob, and have tried to find it, but without success.

If it is in the investors section of the corporate website, that requires a login.

Is there something simple which I have misunderstood?

RobDown said:

I’ve just noticed in that quote that I’ve accidentally put Dec 20th when it should have been Sep 20th

I don’t think you need a log-in Jon. Try this link

https://amlcorp.blob.core.windows.net/default-stor...

I don’t think you need a log-in Jon. Try this link

https://amlcorp.blob.core.windows.net/default-stor...

Excellent.

Thank you Rob.

Some light reading for my coffee break this morning.

Cold said:

Where do the big money, small production run cars fit within the growth forecasts for the company? Negligible volume but big revenue generators or just a handy pocketful of cash that distract from the task of getting the volume sellers out the door?

I think it might be the second of your alternatives.

I read one of Andy Palmers 'interviews', where he indicated that even at about £2m each, the Valkyrie run of cars might not produce a profit. The development costs are obviously very high. I think he then went on to talk about the 'halo' aspect, because AML want to have a mid-engine car in the range and the Valkyrie will demonstrate a high standard of expertise in this new area for AM.

The current model introductions mean huge development costs (a large portion of which was put on the 2017 balance sheet as investment and not an expense on the P&L ie. profit in 2017), so cash clearly is needed. Think how much the total Valkyrie deposits must be. Helpful as an interest free loan.

Edited by Jon39 on Thursday 30th August 08:59

raceboy said:

Could almost be tempted to have a very small dabble if they included owners of any old Astons in that, and if the 'dividend' included a few Aston perks, a bit off at the Dealers, fizz and nibble car launch invites, that sort of thing I'd be very tempted, I'm that easily bought.

Dividend. You will be lucky.

As a shareholder, you are entitled to attend the Annual General Meeting though.

You might have to be satisfied with a 'free' coffee, or if a company feels generous towards its owners, possibly a good lunch.

That us usually about it. A few companies do shareholder perks, but it us a bit of a gimmick.

Dividends are only when a company has excess cash, and spending on the next new model will I expect always be AMs priority.

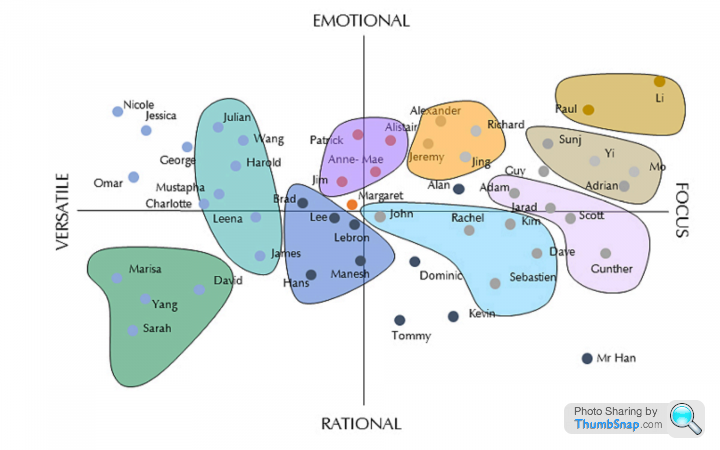

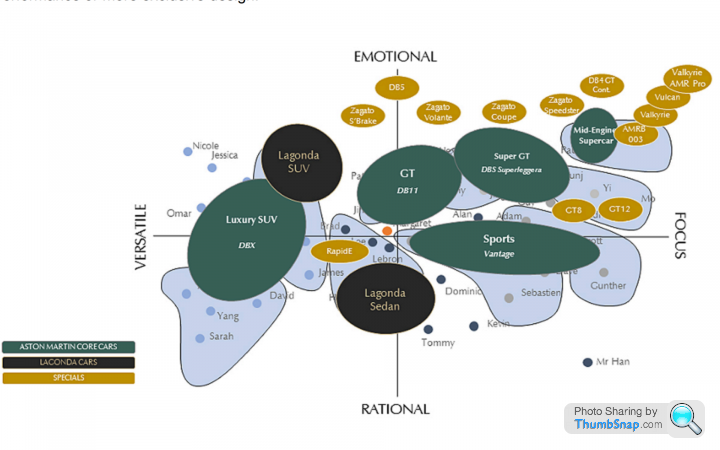

Snippets from the AML document.

I had thought that I bought my Vantage, because to me it looked beautiful.

It seems now though that I was wrong. It was to do with my emotions and tendencies.

This must be all about Charlotte (DBX) and Marcus (Vantage).

Try choosing the model to fit your own personality.

Nicole is very versatile, but probably keeps bursting into tears.

Perhaps Sarah would be better for me.

FUTURE MODEL PLANS

(tap / click to enlarge)

Edited by Jon39 on Thursday 30th August 14:00

avinalarf said:

I agree with you but ,on the preface that you can't time the market, it is what it is.

There are the environmental legislations plus we are entering into a period of time where the Worlwide economic prospects are probably due for a fall.

They were just not geared up for a float 3 years ago which I agree would have been better than now.

There are the environmental legislations plus we are entering into a period of time where the Worlwide economic prospects are probably due for a fall.

They were just not geared up for a float 3 years ago which I agree would have been better than now.

If there is a big stock market fall, between now and the flotation date, you are correct Steven.

Otherwise I think they have timed this to perfection.

Remember the shareholder(s) selling, would like to achieve the highest possible price.

Three years ago, losses were the norm, so the talked about £5bn market value now, would have been impossible then.

- The first of the seven new models DB11 has been in production for a while.

- The Vantage has been launched, but if the long-term strength of demand should disappoint, that is conveniently an unknown.

- DBSS launch received strong acclaim.

- Excitement is building about Valkyrie. Potential investors will love the prospect of selling £2m cars.

- Several new models including the SUV in prospect.

- Very strong revenue increase last year.

- Investors both large and small can get very excited with IPOs, and a combination of James Bond, talk of submarines and aeroplanes (licence, but forget that), multi-million pound cars which sell instantly, what could be more exciting?

- Reported the first profit full year for some time.

This last point is debatable, but probably not widely known, unless you like delving into accounts.

It might explain why the float is in London and not New York, which was considered, according to the Company.

'Aston Martin spent 224 million pounds on R&D last year (one-quarter of sales) but only 11 million pounds of that was expensed in the profit and loss statement. The rest — some 95 per cent (far above other car manufacturers) — was capitalized on its balance sheet. If Aston Martin was based in the U.S., where GAAP accounting rules usually prohibit companies from capitalizing R&D costs, it would have reported another full-year loss.'

Edited by Jon39 on Thursday 30th August 17:25

RobDown said:

ah apologies, I took the SEC reference to mean you were in the US

The disappointment from my perspective is that are no "perks" or discounts for retail shareholders. Would have been nice to maybe have got a discount off servicing or maybe off accessories bought from the AM Shop.

The disappointment from my perspective is that are no "perks" or discounts for retail shareholders. Would have been nice to maybe have got a discount off servicing or maybe off accessories bought from the AM Shop.

Oooh, we must not mention US. With the USA GAAP accounting standards, Aston Martin are still making a loss.

You are normally spot on with accuracy Rob, so I was surprised that you were hoping for 'a discount off servicing'.

The servicing dealers are not connected with the IPO.

My apologies if you have your own special personal arrangements with Gaydon or Works, for your servicing.

When you bought your Aston Martin, did they tell you the price of the car after you had agreed to buy?

'Applying for shares

Once the Retail Offer is open, the minimum application amount for Customers is £10,000 of shares and the maximum amount is £50,000 of shares in the Retail Offer. Although the prospectus will contain the expected minimum and maximum prices, the price of the shares in the Retail Offer will not be determined until after the Retail Offer closes.

You will, therefore, not know the price of the shares when you apply. This means that, when you apply for shares, you will be asked as part of your application to state the amount of money you wish to invest rather than the number of shares you wish to apply for.'

I have been investing for 30 years (never in the car manufacturing sector though), but without knowing a company value, it is not possible to 'do the numbers'.

As soon as I saw £5 billion being mentioned, my intuition said, I'm out. On top of the achieved valuation, don't forget to factor in the amount of debt outstanding.

Edited by Jon39 on Monday 10th September 17:47

RobDown said:

Now you surprise me Jon

With your 30 years of investing I would expect you to be able to multiply the number of shares of AML with the range to be published in the prospectus to be able to work out the valuation on the company.

There’s no smoke and mirrors here Jon, much as you try to allude to it; this is the way IPOs have been done for longer than your 30 years of investing

With your 30 years of investing I would expect you to be able to multiply the number of shares of AML with the range to be published in the prospectus to be able to work out the valuation on the company.

There’s no smoke and mirrors here Jon, much as you try to allude to it; this is the way IPOs have been done for longer than your 30 years of investing

In this instance Rob, it of course depends how wide the stated range might be, as to how much the initial value could vary.

There are not very many IPOs now, which are open to individual investors, compared to the 1980s / 1990s.

Then they tended always to have set prices before submitting the application(s), with the lack of demand risk being underwritten.

Occasionally an auction system was used, where investors applied at their chosen price per share. Above the strike price (set partly according to demand) you were allocated shares (often scaled back), but applications below the strike price were rejected. Therefore you could decide your own maximum price.

I would like to buy a tiny part of the AML business, but only after the IPO froth and excitement is over. I would not treat it as an investment holding though. Would be great if the purchase could be in certificated form (very old fashioned I know), but a framed broker statement would not look very good on the car house wall.

Edited by Jon39 on Monday 10th September 20:19

The shares will have a price between 1750p and 2250p.

This will give the Company a stock market value of between £4 billion and £5.1 billion.

Trading to begin on or about the 8th October.

25% of the shares are being sold.

Prospectus later today.

Edited by Jon39 on Thursday 20th September 08:03

Upperworks said:

Don’t see what the big deal is. Worst case is you lose £50k on AM.

Plenty of us on here have lost a lot more than that on Astons already

Plenty of us on here have lost a lot more than that on Astons already

A great post Ross.

The shares being sold in the IPO, are not newly issued shares.

In this instance, I hope they will be referred to as Pre-owned, and not just second hand ordinary shares.

You should be able to access the IPO Prospectus from this webpage.

https://www.astonmartinlagonda.com/investors/ipo

Edited by Jon39 on Thursday 20th September 18:09

RL17 said:

Potential CEO payout and 4 year tie in ...

If the share price is high in 2022, then I would say, well deserved AP.

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

Can anyone please help me with the historic P/E ratio calculation?

2017 net profit: £74.1m

Average number of shares: 3,285,891 (Aston Martin Holdings (UK) Limited)

Eps: 2,256p

In the new company (Aston Martin Lagonda Global Holdings PLC) at admission there will be 229,521,199 shares in issue.

Therefore the 2017 EPS = 0.32p.

The historic P/E ratio (using the mid IPO price) would be 2000p divided by 0.32p = 6,250.

I know that the IPO valuation will be forward looking, but the historic figure can be a helpful starting point, for an investor to start getting a feel for a business.

6250 is ridiculously high, so where have I gone wrong?

Thanks.

Edited by Jon39 on Friday 21st September 19:01

Gassing Station | Aston Martin | Top of Page | What's New | My Stuff