AML - Stock Market Listing

Discussion

Westlondondriver said:

I think the eps is £0.32 not 0.32p looking at your numbers. So P/E ratio is nearer 60 which is still high.

Thank you Westlondondriver.

At least when my maths is out, I realise something is not right, so not all brain cells lost yet.

AML have not made a profit forecast in the prospectus. I thought they would, with only a few months remaining in their 2018 financial year. Therefore the prospective P/E remains unknown.

Are you a preferred customer of Aston Martin?

Has anyone heard of the Henniker Club

My guess would be, it is for customers who do not currently own an Aston Martin (therefore not eligible to buy shares in the IPO), but who have paid deposits for multi-million pound Astons. That excludes me then. To use the well known quote, I would not want to be in a club, that accepts me as a member.

Extract from the prospectus;

5.1.1 Details of the Customer Offer

Only Eligible Customers are entitled to apply for Shares in the Customer Offer. Eligible Customers are persons who are: (a) owners of an Aston Martin car and were detailed on Aston Martin Lagonda’s CRM system as at 24 August 2018; and/or (b) members of the Aston Martin Owners Club ("AMOC") and whom confirmed to AMOC that they wished to receive further information on the Offer by 12 p.m. (midday) (U.K.time) on Monday 17 September 2018; and (c) resident in the U.K.

Preferred Customers are those Eligible Customers who are also, as at 24 August 2018, members of Aston Martin Lagonda's Henniker Club.

Pursuant to the Customer Offer, each Eligible Customer is entitled to apply to purchase Shares up to a maximum of £50,000 at the Offer Price, save in the case of Preferred Customers, who are entitled to apply to purchase Shares up to a maximum of £99,999 at the Offer Price.

Edited by Jon39 on Monday 24th September 14:41

JB65 said:

V12Manual said:

GBP 22 million over four years? Sounds like a bargain frankly given what Dr Palmer is doing.

:-) if only we were rewarded for the promises we madeHopefully it is not as easy as that. I have not studied the terms, but these days, the schemes are normally subject to a strict delivery criteria.

What could possibly go wrong during the next four years? The prospectus contains a lengthy list of risks.

JB65 said:

£35m at IPO with £7m immediate pay with IPO price being the only variable it seems.

https://www.thetimes.co.uk/edition/business/welcom...

https://www.thetimes.co.uk/edition/business/welcom...

If the IPO goes to plan (remember what happened with BP In 1987), then the present investors who are selling their shares, will see a total of £1,275,000,000.

They might be the only Aston Martin investors in 105 years, to have ever made a profit on the money they put in to this business. I think you will agree, AP and his team have made that achievement possible for the investors. The balance of the share award, locked in I think for 4 years, requires the ship to keep going strongly, otherwise the share price falls, together with the value of his award.

Seems a fair deal to me. Reward for the achievement so far ( a tiny percentage) and for the second part, a carrot to keep the profits growing.

I think the 4 year second part, will certainly not be easy.

RobDown said:

Brief update - price range for shares has been narrowed to £18.50-£20 this morning (from £17.50-22.50). Books are covered at those levels. Gives a valuation of 4.2-4.5 bn

I was hoping for FTSE 100 eligibility, then the trackers would have to buy.

Just missed at this stage then.

Minglar said:

Should all eligible participants have received an email or postal communication by now?

It looks like the window to apply on line for initial shares has now closed, which ties in with Robs comments on levels of interest/coverage.

Best Regards

Minglar

It looks like the window to apply on line for initial shares has now closed, which ties in with Robs comments on levels of interest/coverage.

Best Regards

Minglar

Yes, my own email arrived several weeks ago.

If you have not had one Richard, perhaps you are not on the database at Gaydon.

Unless there is a price jump during the first few days of trading, then it will not make any difference to you, because you can buy in the market. If you like the thought of having a share certificate rather than just a broker statement, you need to make sure your selected stock broker allows certificated purchases.

I think initial trading is planned for Wednesday, but dealing for private individuals begins next week.

It would be interesting to see how many car owners have applied for shares in the IPO, but we will probably never know.

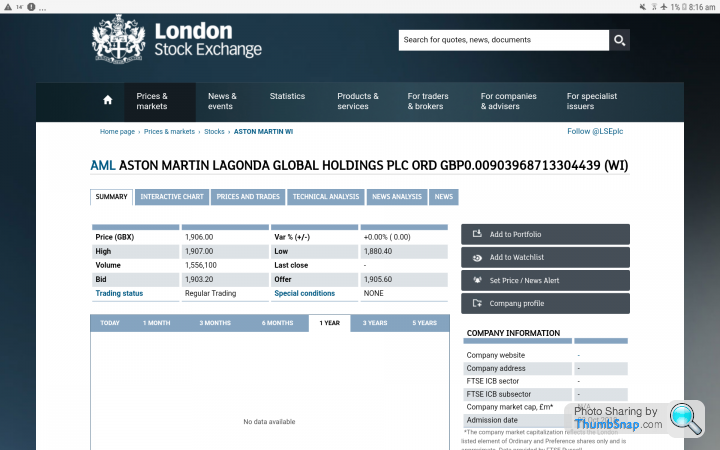

ASTON MARTIN LAGONDA GLOBAL HOLDINGS PLC - SHARE TRADING HAS BEGUN

The IPO offer price was set at 1900p.

The share price increased slightly when trading commenced, but half an hour later trading was about 1830p.

Now you know why I did not want to apply in the IPO.

Edited by Jon39 on Wednesday 3rd October 08:40

Buster73 said:

Somebody sold £21m worth at 8.00 am this morning.

I think that trade would be in connection with the internal auction system.

I have never understood how it all works, but you can see very big trades recorded for most quoted companies, at both opening and closing each day.

jonby said:

Price now 1776

As a financial man Jonby, did you foresee this?

Being one of the stockmarket biggest one day fallers (7.5% at present), is not what they would have hoped for.

There was so much hype leading up the IPO to boost the float price, and the 2017 profit was only achieved by balance sheet accounting, which is very important to fundamental investors.

OK for the sellers. However, considering the seller aspect, what puzzles me, is that I don‘t think the Italian owner did sell completely.

We are only talking about a one day movement, but an IPO first day is often remembered.

Selecting a price which results in a first day increase, is a good way to start.

Agree with your points hornbaek.

The three present core models should be the regular main sellers. We do know that UK sales of the DB11 are trailing the DB9, and from what has been stated here, there does not appear to be a lengthy queue of existing Vantage owners, anxious to buy the new Vantage.

One interesting point with the ‘specials', is how the prices have gradually inflated.

It would appear that AML have recently discovered strengthening demand, far exceeding the limited number they choose, and with each successive model have increased the price. Don't blame them, but do you think £7 million is taking Mickey and perhaps nearing the bursting of a bubble?

The increasing demand and prices.

V12V Zagato - was that about £300,000 and did not sell the planned number?

One-77 - £1.0m, the final few were slow sellers.

Vulcan - £1.8m, the final few took a while to sell.

Valkyrie - £2.4m, could have sold over double the number.

Two Zagatos - £7.2m (that is the cost of 3 road legal Valkyries).

Edited by Jon39 on Wednesday 3rd October 21:55

jonby said:

The funny thing is, the more expensive the model, the easier it seems to sell out ......

But was the market then the norm, or is now the norm ? I'm not leaning one way or the other - I have no clue. I certainly hope it works.

But was the market then the norm, or is now the norm ? I'm not leaning one way or the other - I have no clue. I certainly hope it works.

Revenue and profit.

Only the insiders would know. AP has said the Valkyrie with high development costs may not be profitable, but will be a halo car for [the marketing of] subsequent mid-engined models.

Edited by Jon39 on Thursday 4th October 12:14

George29 said:

Jon39 said:

Revenue and profit.

Only the insiders would know. AP has said the Valkyrie with high development costs may not be profitable, but will be a halo car for [the marketing of] subsequent mid-engined models.

Could argue Valkyrie is underpriced. I’d certainly suggest it is compared to rivals. That rebodied Bugatti is around twice the price for example.

Good to hear from you again George.

When the pair of Zagatos were announced (£7.2m incl tax), it certainly made the Valkyrie look underpriced, or the Zagatos overpriced.

Would you buy an Aston Martin again, if the Company had become a Ferrari, or Fiat subsidiary ?

http://www.providencejournal.com/entertainmentlife...

.....................................................................

Words can sometimes come back to bite.

'The British carmaker, said investors in the IPO should be prepared to pay 19 pounds a share or risk losing out on the deal, according to terms obtained by Bloomberg.'

( The closing price on Friday was 17 pounds. - Oops! )

Edited by Jon39 on Saturday 6th October 22:36

Thank you hornbaek, for your earlier detailed explanation, about the present IPO process.

I applied in scores of new issues during the 1980s, and did not know about the underwriting change to the system.

In those days there were a few auction type issues, where you could make multiple applications at different prices, but most were fixed price offers, where the issue price was known before any applications were posted.

It appears to me that the underwriting risk has now been eliminated, but replaced by the 'stabilisation' system, so who carries the risk involved there? In the initial days of this AML IPO, the stabilisation would have involved purchases, so who takes that short-term book loss?

With my equity investing, I always consider the basic fundamentals, so decided for AML the P/E ratio was far too high for me, and therefore did not make an application for shares. Therefore, what has occurred to the market valuation, is what I thought would happen.

The often mentioned comparison to Ferrari by AP, has now encouraged me to look at their 3 year results. Quite a surprise to see remarkable growth in both Rev. and Pre-tax. If AML can match those percentages in 2018/19/20, all will be well. Hopefully by not continuing with regular assistance from their R & D accounting.

Edited by Jon39 on Tuesday 9th October 08:09

Shares are now changing hands at 1,500p, therefore the IPO initial investors are now looking at 21% (book) losses.

Here are a few figures which you may like to consider.

What do you think a fair valuation (share price) might be ?

Profit attributable to the Company owners

2017 first half year = £15.6m.

2017 full year = £74.2m.

2018 first half year = £8.7m.

Price ÷ Earnings Ratio (historic, based on full year 2017)

Issue Price 1900p = 55.4.

At 1500p = 43.7.

Company Market Value

At 1900p = £4.3 billion

At 1500p = £3.4 billion

There has not been a Company forecast for the 2018 profits, but I think all that we know, is that the first half is lower than in 2017, and that there has been mention of about £50 million costs for the IPO.

Graze01 said:

Jon

What explains the huge rise in profit second half of 2017 and the halving of profit first half 2017 vs first half 2018?

Was second half 2018 when they treated investment in new plant Etc as profit?

Graeme

What explains the huge rise in profit second half of 2017 and the halving of profit first half 2017 vs first half 2018?

Was second half 2018 when they treated investment in new plant Etc as profit?

Graeme

There are two documents Graeme, which if read more thoroughly than I have done, probably provide the answers to your two questions.

1) Full year 2017 Report and Accounts (on the Companies House website - Aston Martin Holdings (UK) Ltd)

2) The IPO Registration document, including the first half 2018 results (on the Aston Martin website IPO page).

There are future 3 year car production estimates in that document, which will be interesting to remember.

My ( possibly cynical) guess for your first question, is that as much business as possible was being transacted in the second half 2017, in preparation for the IPO. Were there quite a few special models being delivered and announced (deposit payments - would they be included in revenue?), during the second half of 2017?

For your second question, could it have perhaps mainly been due to reduced Vantage activity in the first half of 2018, before the model changeover?

soofsayer said:

... Retail investors have been hit, but I would have thought institutional investors would have got a healthy discount on the IPO price before trading began and are still sitting on net gains.

I thought that everyone applying in an IPO paid the same price ie. in this case, £19 for 25% of the Company.

Are you saying individuals paid £19, but unaware to them, institutions had discounts of about 20%?

Surely not. That is not fair without being disclosed. Is it amongst the small print of the Prospectus?

RobDown said:

BTW - I’d flag up that Ferrari shares are down 17% over the last week. And TATA a lot more. Not a good time to be in the car space

Have you looked at Ferrari's last 3 year revenue and profit growth, Rob?

I was surprised.

I think they are now even saying their self imposed production limit, is fully sold for a year or so ahead.

That of course provides scope for an uplift to margins, if they wanted to.

An enviable position to be in, but whether their current PE level can be sustained, I don't know.

Gassing Station | Aston Martin | Top of Page | What's New | My Stuff