AML - Stock Market Listing

Discussion

I watched the presentation this morning. Internet went slow motion, so missed some parts.

A few points that I did notice;

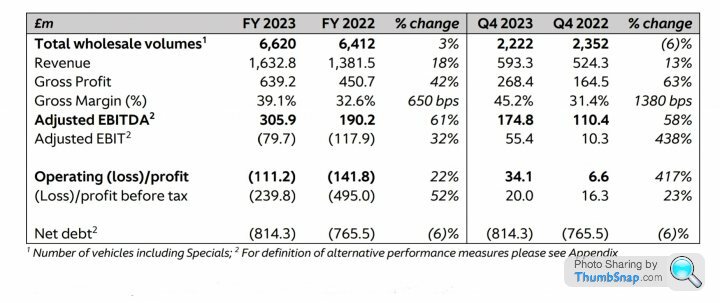

- Was the cash flow positive in Q4 as promised. - Think they were silent about that milestone being achieved.

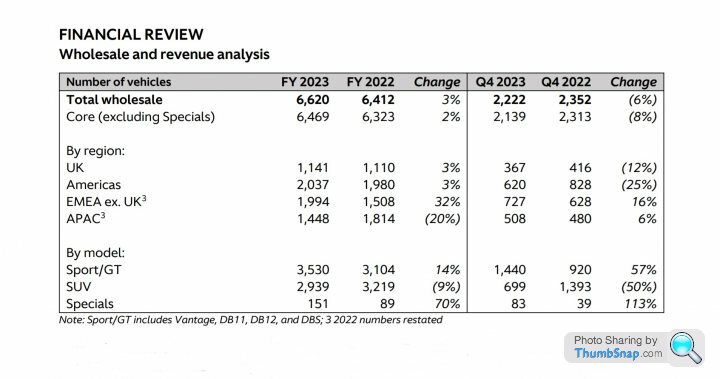

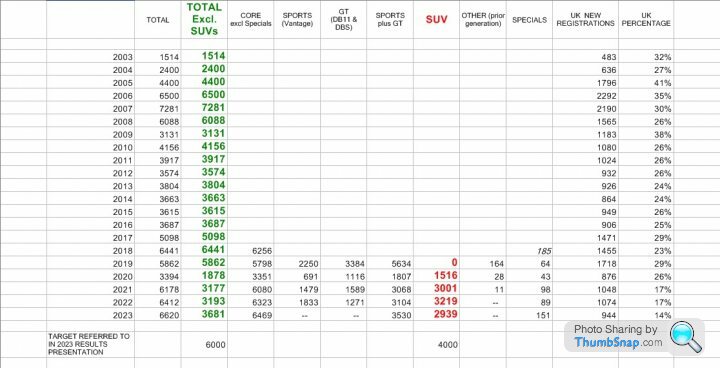

- Several mentions of very strong DBX 707 sales. - Check the overall SUV sales below (down 9% in 2023).

Think they said that soon, only the 707 version will be available.

- The CFO suggested that refinancing might not involve equity. The trend at present (higher interest rates) is to use equity, to reduce debt interest payments. We shall wait and see on that one. After hearing the question, I expected him to ignore, or be vague about that. Any anticipation of equity dilution can depress a share price.

There was much talk about a big sales increase in Sports/GT.

This is a category that has withered over the years. From the peak of 7281, it is now 3681. Thank goodness for the DBX.

As we have discussed, The new models are good, so if enough customers are willing to pay the higher margins, the target mentioned is now 6000.

60% new customers was frequently mentioned. Turn that around and of course any loss of existing customers, increases the percentage of new customers.

Some factual information below.

Sports and GT figures are no longer reported separately, therefore we cannot see Vantage sales.

(Tap/click to enlarge, then when open, repeat)

Edited by Jon39 on Wednesday 28th February 19:34

Jon39 said:

- The CFO suggested that refinancing might not involve equity. The trend at present (higher interest rates) is to use equity, to reduce debt interest payments. We shall wait and see on that one. After hearing the question, I expected him to ignore, or be vague about that. Any anticipation of equity dilution can depress a share price.

LooneyTunes said:

That's not a surprise. Many are struggling to raise equity in the current market without taking a serious caning on valuations.

Thank you LT.

Of course raising capital through equity solves the burden of interest payments, and Aston Martin have repeatedly done it in recent years, so to an outsider, they always made it appear easy and Mr. Stroll does spin a good line about sunshine over the horizon. At least they now have new models which have rightly been really well received, but even so, becoming profitable at EBITDA level is one thing, whereas Pre-tax is another huge leap.

I think there is $1,143,720,000 outstanding (part repayment in Oct 2022) for the Senior Secured Notes 10.5% Nov 2025.

When that was issued, the BoE base rate was 0.1% and the FX 1.32.

Economic conditions have of course changed considerably, so with that debt then agreed at 10.5%, how high do you think it could be, if it were to be refinanced now?

There must be a point, where companies become overwhelmed by their debt interest payments..

One example of refinancing this month;

$1,700,000,000 aggregate principal amount of guaranteed debt securities consisting of

(1) $850,000,000 5.834% Notes due 2031 (7 years) and

(2) $850,000,000 6.000% Notes due 2034 (10 years).

So there is a company paying rates now, which are far below the AML November 2020 rate.

As far as I know, the negotiations might have been routine, but that company has plenty of cashflow and reported 2023 revenue of

£27 billion, so in a completely different position compared to AML.

Edited by Jon39 on Wednesday 28th February 19:39

Jon39 said:

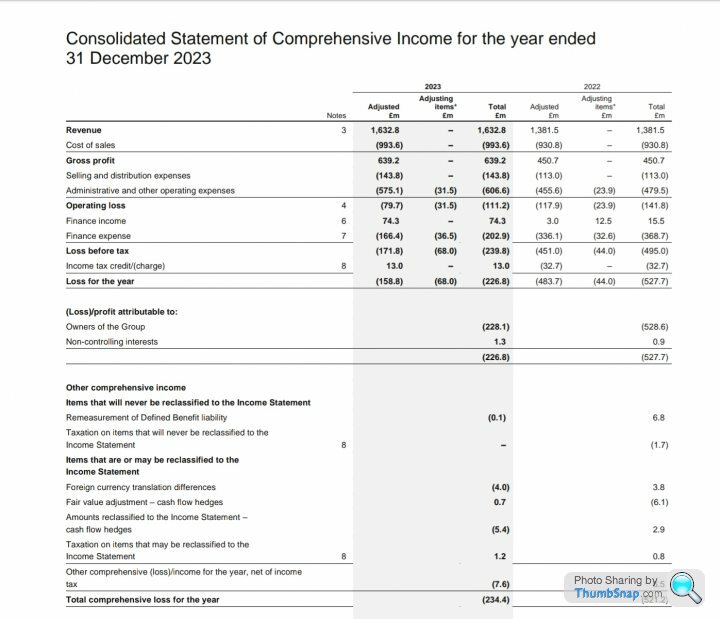

Please, can a member here who knows accounting clarify the passage from EDITDA to EBIT and then to profit before tax? AFAIK (studied accounting a long time ago), AML had a total amortization plus depreciation of -385.6M (-305.9M-79.7M), correct? Then how do you arrive in -111.2M and -239.8M respectively? Thanks!!

Kart16 said:

Please, can a member here who knows accounting clarify the passage from EDITDA to EBIT and then to profit loss before tax?

AFAIK (studied accounting a long time ago), AML had a total amortization plus depreciation of -385.6M (-305.9M-79.7M), correct? Then how do you arrive in -111.2M and -239.8M respectively? Thanks!!

AFAIK (studied accounting a long time ago), AML had a total amortization plus depreciation of -385.6M (-305.9M-79.7M), correct? Then how do you arrive in -111.2M and -239.8M respectively? Thanks!!

In the words of the late Mr. Charlie Munger, EBITDA and EBIT are (I don't like to say), but he despises the misuse of EBITDA.

Absolutely meaningless and frequently used by firms, trying to pretend they are profitable.

Here is the answer to your question, explained by (probably) the most successful investors in the world.

(Tap/click to enlarge and when open, repeat.)

Edited by Jon39 on Wednesday 28th February 20:53

Jon39 said:

Economic conditions have of course changed considerably, so with that debt then agreed at 10.5%, how high do you think it could be, if it were to be refinanced now?

Really wouldn’t like to speculate on that. There are so many variables, but bear in mind that the headline rate is rarely the only cost. I do enjoy SSO and the AML saga

https://karenable.com/astonmartins-fy-2023/

As expected, it looks like AML is well on its way to running out of cash again while its “Administrative & Operating Expenses” are growing at a significantly higher rate than AML’s revenue. It will be very interesting to see how the 2024 refinancing will be handled and if equity will turn out to be a big part of it. AML whiffed big time on its original 2023 goal of being Free Cash Flow positive in the 2nd half, and in fact 2023 was worse in this area than both 2021 & 2022. DBX volumes look like they have hit a wall, and that wall is only about half the way to where AML thought they would be not too long ago. The Q4 wholesales were well short of the target and the DB12 start up has been a bit of a mess. The DB12 orderbook still looks light, certainly lighter than expected given all the PR around it. The 2024 Guidance looks a lot like the 2023 Guidance and that didn’t go so well. The big bet last year was the DB12 and that start up went about as smoothly as the DBX 707 did. This year it’s the new Vantage, it will be interesting to see if AML has learned from its past

https://karenable.com/astonmartins-fy-2023/

As expected, it looks like AML is well on its way to running out of cash again while its “Administrative & Operating Expenses” are growing at a significantly higher rate than AML’s revenue. It will be very interesting to see how the 2024 refinancing will be handled and if equity will turn out to be a big part of it. AML whiffed big time on its original 2023 goal of being Free Cash Flow positive in the 2nd half, and in fact 2023 was worse in this area than both 2021 & 2022. DBX volumes look like they have hit a wall, and that wall is only about half the way to where AML thought they would be not too long ago. The Q4 wholesales were well short of the target and the DB12 start up has been a bit of a mess. The DB12 orderbook still looks light, certainly lighter than expected given all the PR around it. The 2024 Guidance looks a lot like the 2023 Guidance and that didn’t go so well. The big bet last year was the DB12 and that start up went about as smoothly as the DBX 707 did. This year it’s the new Vantage, it will be interesting to see if AML has learned from its past

Interesting, write up but I disagree with the comments about raising equity rather than debt.

Yes, the current interest rate environment might generally make equity seem appealing, but AML’s current shareholders would get bent over raising equity. There isn’t much around, and anyone able to write big equity cheques to a firm in AML’s general position (burning cash, underperforming) will make eye-watering demands (not just financial, but likely also relating to Board composition/Chair), especially given the limited exit options.

Don’t forget either than debt impacts the company balance sheet. Equity valuations impact the balance sheets of the holders of that equity.

Yes, the current interest rate environment might generally make equity seem appealing, but AML’s current shareholders would get bent over raising equity. There isn’t much around, and anyone able to write big equity cheques to a firm in AML’s general position (burning cash, underperforming) will make eye-watering demands (not just financial, but likely also relating to Board composition/Chair), especially given the limited exit options.

Don’t forget either than debt impacts the company balance sheet. Equity valuations impact the balance sheets of the holders of that equity.

Thank you SSO for your article.

When AML obtained their stock market listing, Andy Palmer had dreams of entry into the FTSE 100.

Probably in conjunction with that (grandios) expectation, they began quarterly reporting.

Now, from their point of view, half year reporting would seem much more suitable.

It would stop us analysing in such detail.

EXTRACT

'Positive FCF expected in H2’23

which was later revised to Positive FCF in Q4 2023. What AML delivered in Q4 2023 was -£63 mil. of Free Cash Flow. As misses go, this one is quite impressive, especially considering that the revised outlook to have positive FCF in Q4 2023 was issued in November. Just to make matters worse, FCF was actually worse in 2023 at a -£360 mil. than it was in 2022 (-£299 mil.). Positive Free Cash Flow is basically table stakes to be considered a heathy business and despite the latest promises that AML will now get there in the 2nd half of 2024, that still seems a long way off.'

This has been the general pattern throughout AMs history. First enjoy the cars, second worry about the financials. Spending more than earning would normally be disastrous for any business, but AM has always had an increasingly wonderful image and money has always been forthcoming in the hour of need.

Since the arrival of Mr Stroll, the continuous fund raising has been remarkable. Certainly a positive difference from the old days, where failure was followed by a fresh benefactor.

Like you, I had expected the next fund raising to be equity based rather than debt, but LooneyTunes, who I think might be involved in corporate debt markets, has pointed out that the equity route is extremely difficult at present. A shame because equity could considerably reduce the ongoing cost of debt.

The AML shareholders have been compliant up to now, presumably because Mr Stroll has "transformed" the Company and always forecasts growth, together with future profitability.

Edited by Jon39 on Monday 4th March 09:28

12TS said:

I do enjoy SSO and the AML saga

https://karenable.com/astonmartins-fy-2023/

As expected, it looks like AML is well on its way to running out of cash again while its “Administrative & Operating Expenses” are growing at a significantly higher rate than AML’s revenue. It will be very interesting to see how the 2024 refinancing will be handled and if equity will turn out to be a big part of it. AML whiffed big time on its original 2023 goal of being Free Cash Flow positive in the 2nd half, and in fact 2023 was worse in this area than both 2021 & 2022. DBX volumes look like they have hit a wall, and that wall is only about half the way to where AML thought they would be not too long ago. The Q4 wholesales were well short of the target and the DB12 start up has been a bit of a mess. The DB12 orderbook still looks light, certainly lighter than expected given all the PR around it. The 2024 Guidance looks a lot like the 2023 Guidance and that didn’t go so well. The big bet last year was the DB12 and that start up went about as smoothly as the DBX 707 did. This year it’s the new Vantage, it will be interesting to see if AML has learned from its past

Much appreciated. https://karenable.com/astonmartins-fy-2023/

As expected, it looks like AML is well on its way to running out of cash again while its “Administrative & Operating Expenses” are growing at a significantly higher rate than AML’s revenue. It will be very interesting to see how the 2024 refinancing will be handled and if equity will turn out to be a big part of it. AML whiffed big time on its original 2023 goal of being Free Cash Flow positive in the 2nd half, and in fact 2023 was worse in this area than both 2021 & 2022. DBX volumes look like they have hit a wall, and that wall is only about half the way to where AML thought they would be not too long ago. The Q4 wholesales were well short of the target and the DB12 start up has been a bit of a mess. The DB12 orderbook still looks light, certainly lighter than expected given all the PR around it. The 2024 Guidance looks a lot like the 2023 Guidance and that didn’t go so well. The big bet last year was the DB12 and that start up went about as smoothly as the DBX 707 did. This year it’s the new Vantage, it will be interesting to see if AML has learned from its past

Looking back on the results again, perhaps the most shocking item is missing the lowered guidance that AML issued in Nov. Certainly in my past professional life, if you lowered guidance, you made sure the new number was one you would not only hit, but beat. How they messed that up is a real head scratcher.

SSO said:

Looking back on the results again, perhaps the most shocking item is missing the lowered guidance that AML issued in Nov. Certainly in my past professional life, if you lowered guidance, you made sure the new number was one you would not only hit, but beat. How they messed that up is a real head scratcher.

Yes, that was strange.

There was only about one month remaining, so the directors must have had an accurate estimate of the December sales, especially as for one of those weeks, I presume production might have been stopped anyway.

I expect you consider the next debt refinancing, to be a very important transaction.

Do you have any guesses, as to what alternatives there might be ?

Hope it will not result in more USD loan notes, with even higher interest rates.

Do you know anything about the 2021 Long Term Incentive Plan?

I am wondering if it is an all-employee option scheme?

At least that would be fairer to employees, than the first one.

78,050 new ordinary shares are being issued, to be held by the Employee Benefit Trust, pending exercises.

Jon39 said:

SSO said:

Looking back on the results again, perhaps the most shocking item is missing the lowered guidance that AML issued in Nov. Certainly in my past professional life, if you lowered guidance, you made sure the new number was one you would not only hit, but beat. How they messed that up is a real head scratcher.

Yes, that was strange.

There was only about one month remaining, so the directors must have had an accurate estimate of the December sales, especially as for one of those weeks, I presume production might have been stopped anyway.

I expect you consider the next debt refinancing, to be a very important transaction.

Do you have any guesses, as to what alternatives there might be ?

Hope it will not result in more USD loan notes, with even higher interest rates.

Do you know anything about the 2021 Long Term Incentive Plan?

I am wondering if it is an all-employee option scheme?

At least that would be fairer to employees, than the first one.

78,050 new ordinary shares are being issued, to be held by the Employee Benefit Trust, pending exercises.

On the next debt/equity raise, no idea but I think its going to be very tough.

Details on the LTI should be in last year Annual Report.

Jon39 said:

Like you, I had expected the next fund raising to be equity based rather than debt, but LooneyTunes, who I think might be involved in corporate debt markets, has pointed out that the equity route is extremely difficult at present. A shame because equity could considerably reduce the ongoing cost of debt.

The AML shareholders have been compliant up to now, presumably because Mr Stroll has "transformed" the Company and always forecasts growth, together with future profitability.

Don’t mistake shareholder compliance for belief. Many shareholders will be seriously under water at the moment, as they were when Stroll came in, with some having mentally written off their investments. Stroll’s consortium brought hope. Does that hope still exist or translate into confidence? Perhaps, but I doubt some of the Trump-esque traits and statements help…

A large part of problem from an equity investment perspective is that they’ve made such a hash of the DBX volumes that you could argue that they almost seem to have shown that there isn’t much of a market for an Aston SUV after all (a re-run of the Rapide story?). The trouble is, if the promised volume cash cow doesn’t deliver, an independent future seem much less likely. A challenging place to be if wanting to raise equity.

I still maintain that, although they don’t seem to realise it, increased focus owner engagement and marketing would help them. I compare what my Ferrari driving friends see/experience with Ferrari vs my own experiences with Aston and they’re poles apart…

LooneyTunes said:

Jon39 said:

Like you, I had expected the next fund raising to be equity based rather than debt, but LooneyTunes, who I think might be involved in corporate debt markets, has pointed out that the equity route is extremely difficult at present. A shame because equity could considerably reduce the ongoing cost of debt.

The AML shareholders have been compliant up to now, presumably because Mr Stroll has "transformed" the Company and always forecasts growth, together with future profitability.

Don’t mistake shareholder compliance for belief. Many shareholders will be seriously under water at the moment, as they were when Stroll came in, with some having mentally written off their investments. Stroll’s consortium brought hope. Does that hope still exist or translate into confidence? Perhaps, but I doubt some of the Trump-esque traits and statements help…

A large part of problem from an equity investment perspective is that they’ve made such a hash of the DBX volumes that you could argue that they almost seem to have shown that there isn’t much of a market for an Aston SUV after all (a re-run of the Rapide story?). The trouble is, if the promised volume cash cow doesn’t deliver, an independent future seem much less likely. A challenging place to be if wanting to raise equity.

I still maintain that, although they don’t seem to realise it, increased focus owner engagement and marketing would help them. I compare what my Ferrari driving friends see/experience with Ferrari vs my own experiences with Aston and they’re poles apart…

Minglar said:

As I said in another thread recently, buying new does not make a huge amount of sense to me even if you can afford it. I do worry a little that there is too much overlap between DB12 and new new Vantage and they will eat away at each others sales volumes.

They do look tidy, and yes there's some crossover, but I don't think that's necessarily a bad thing as you'd have few people looking at buying one of each. A bigger issue may turn out to be the ever higher entry point to the brand. DBX could have helped them with that, but sales seemingly hitting a wall is no surprise. Their marketing has been terrible, especially taking into account that product's importance to AML's revival.I know AML has seemingly decided to focus efforts on new customers, but I cannot help but ask myself which would have been more successful: pushing press cars to youtubers (most of whom seem to be ignored or disliked by many who could actually buy the cars) or making sure that each dealership had a couple of DBXs to use as service loan cars for clients in the country and/or known to drive other 4x4s and then following up with them?

AML know where I live, their collection drivers take one of my cars, then swap in for another, and doubtless see what else is parked around the place. How much proactive marketing for DBX? Nothing. Not even a brochure to leave out for Mrs LT to flick through and decide she fancied one. Insanity.

I don't get how a firm pushing

Compare and contrast to another brand I've never bought from who turned up at my office not once, not twice, but three times with out an appointment to see if I could spare a few minutes to have a look and maybe go for a drive. I was busy each time but they took members of my staff out in the hope that they'd say good things to me (they did). If I was in the market for what they were offering, I would have probably given them a call.

Debt refinancing announced today.

Offer £1,140 million (equivalent) loan notes, maturity 2029.

And revolving credit facility agreement £170 million.

https://www.londonstockexchange.com/news-article/A...

Does (equivalent) mean the currency will be USD ?

Geely (minority Aston Martin) shareholder is a remarkable business.

Their first car was launched in 1999 and in 2023 had sales totalling 2.79 million cars.

Recently the have been fund raising, by floating several of their subsidiaries on the US stock market.

That has not been such a happy outcome though.

Full article here

https://archive.li/QuFyr

Jon39 said:

Debt refinancing announced today.

Offer £1,140 million (equivalent) loan notes, maturity 2029.

And revolving credit facility agreement £170 million.

https://www.londonstockexchange.com/news-article/A...

Does (equivalent) mean the currency will be USD ?

Interesting about Lotus. Hadn’t realised that was a SPAC.

Gassing Station | Aston Martin | Top of Page | What's New | My Stuff