Gone very quiet

Discussion

105.4 said:

akirk said:

How does that compare to pre-lockdown?

I assume that we should expect now to be an amalgam of pre / during lockdown?

I dont know for sure the exact numbers during lockdown, as I was doing something else for a living then. All I do know is that every single day was like the Christmas peak.I assume that we should expect now to be an amalgam of pre / during lockdown?

Even if I did know the figures, I don’t think it would go down very well for me to post them on a public forum.

Sorry.

As above, I think it is a totally predictable pattern - lockdown = shops not easy to access / concerns about meeting others / bored / spare cash from not commuting / incomes protected / more time in house to look at what is needed => vastly increased spend on mail order

I wouldn't expect it to return to exactly the same as pre-lockdown, but a drop in mail order is of little surprise...

I think that there are a lot of very misleading stats around, and even more misleading interpretations - we seem as a society to only consider +ve increases as being of any value - forgetting that for any organisation / economy / pattern of shopping to have a peak implies a drop - you can't have continual growth on growth nothing works like that and any expectation of such simply drives patterns to a more abrupt fall-off or correction

if we stopped obsessing about every figure having to show growth against previous figures - i.e. stopped micro-analysing figures day on day / week on week / month on month / even year on year, then we would a) have less anxiety and b) we would have a more reasonable understanding of reality... It helps no-one for a business to say - April 18th 2023 was 23% down on April 18th 2022 - it is totally meaningless, yet that it is the kind of micro-analysis that we now do - instead of looking at the longer term and saying that generally 2023 is good v. 2022 or that overall the business is healthy with income above expenditure / good cash flow / low defaulting on invoices / etc.

instead of reading 2023 as being lower than 2022 = calamity and crisis in the business, perhaps we need to read that same scenario as 2022 being a peak and actually the growth curve is a bit slower / more bumpy than 2022's growth suggests... looking at whether the economy / business / market is healthy over a longer period...

sadly culture / politics doesn't encourage this - instead we are encouraged to think that every business is a unicorn in the making expecting exponential growth and failing if it doesn't perform to some abstract and unrealistic model - it is why we get such a bumpy economy - if commentators and investors started to prioritise businesses with lower but longer and more stable growth or performance, we would have a much more stable economy... but in a world where everyone is an influencer / eCommerce whizz kid / has a technology company being launched, we seem to expect businesses to succeed within a year or two, and write them off if any period shows a drop against a previous period - totally unrealistic

Aventador 700 said:

As things go further into these tougher times, this thread is getting more and more sporadic, i guess thats only to be expected as people like delivering good news and not the woes.

can we take it that the quieter this thread, the worse things are getting?

I’m happy to post about the bad times as well as the good. can we take it that the quieter this thread, the worse things are getting?

The year so far:

January sales; Pretty much the same as last year.

February; Very quiet, which personally, was a good thing as I was absolutely exhausted after October-January.

March; It was steady.

April. Busy. 22% up on last year, predominantly from my middle class to millionaires row areas. The benefits area remained constant / slight increase on last year, whilst my working class area had taken a slight dip.

So far in May; Yesterday was my busiest day of the year so far by 135 packages and also my busiest week, but due to the bank holiday, this was over five days instead of the usual six or seven days. The middle class and millionaires row areas are flying, the working class area is picking up nicely and is now busy, whilst my benefits class area remains constant. Next week is forecast to be just as busy as this week has been.

One thing of note is that I’m seeing a lot more smaller packages coming through. The bigger / heavier the parcels the more I get paid for them. I’m going to have to work out this evening how this has affected my average pay per day and see if this trend has reduced my average by a few pence or not.

But to counterbalance that, the cost of diesel has dropped by nearly 10p per litre since February.

I’m already having a lot of customers in my working class, middle class and millionaires row areas telling me that they’re ordering clothes for their holidays, so folk are still spending money on foreign travel. It will be interesting to see how things are during June once all of these Bank Holidays are out of the way.

I deliver parcels to a guy who is a salesman at a local German car dealership, (I won’t say which brand). He’s at the end of my round when I’ve usually got a few minutes in the bag, so we’ll sometimes have a quick chat and compare notes about how busy / quiet we are.

He was telling me that last weekend his dealership did 55 handovers for new cars, (I can’t remember if he said that was on a Saturday or a Sunday), although he did say that he’s seeing a trend in people stating to increase the term that they’re taking finance over.

I’m not in London, or Leeds or Manchester. I’m a smallish, Northern, provincial area. I’m still confused about where folk are getting the money from tbh.

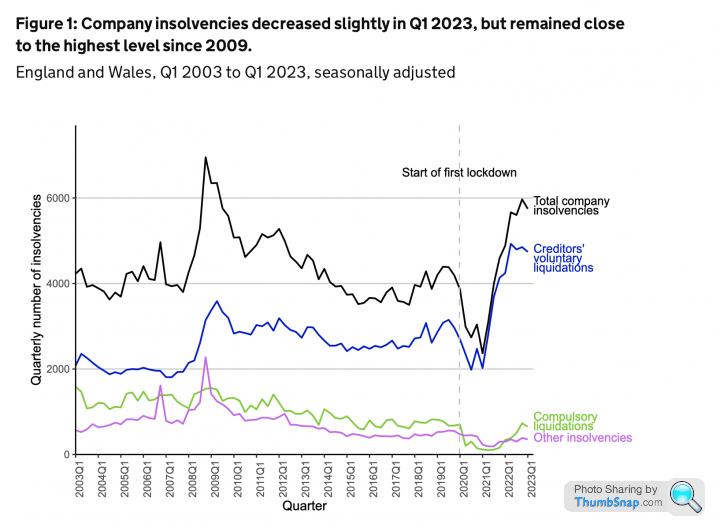

A small bit of good news is that the UK company insolvencies look to have peaked.

https://www.gov.uk/government/statistics/company-i...

https://www.gov.uk/government/statistics/company-i...

Aventador 700 said:

As things go further into these tougher times, this thread is getting more and more sporadic, i guess thats only to be expected as people like delivering good news and not the woes.

can we take it that the quieter this thread, the worse things are getting?

no don't think so - I think it is important to separate what is discussed / assumed online and what is reality - there is probably a tendency for the online discussions to be an atypical group of people so i am not sure that they are indicative of what the actual economy is doing... We have hundreds of clients, so I see a good cross section of small business across the UK and increasingly around the world - not seeing a huge number of issues, I wouldn't say that money is always rolling in with abundance but companies generally seem to be optimistic and most are very busy...can we take it that the quieter this thread, the worse things are getting?

Wilmslowboy said:

A small bit of good news is that the UK company insolvencies look to have peaked.

https://www.gov.uk/government/statistics/company-i...

When you look at that graph it’s criminal what the politicians did with their over reaction to covid. I know they all got rich from it but that graph shows a lot of misery and poverty was caused while they enjoyed lording it over everyone and filling their own pockets. https://www.gov.uk/government/statistics/company-i...

Douglas Quaid said:

When you look at that graph it’s criminal what the politicians did with their over reaction to covid. I know they all got rich from it but that graph shows a lot of misery and poverty was caused while they enjoyed lording it over everyone and filling their own pockets.

I think people would benefit from learning how to count in Italian how many Shell petrol station there are.

Douglas Quaid said:

Wilmslowboy said:

A small bit of good news is that the UK company insolvencies look to have peaked.

https://www.gov.uk/government/statistics/company-i...

When you look at that graph it’s criminal what the politicians did with their over reaction to covid. I know they all got rich from it but that graph shows a lot of misery and poverty was caused while they enjoyed lording it over everyone and filling their own pockets. https://www.gov.uk/government/statistics/company-i...

In my world (well, the fashion part of it), there’s still a ton of pain.

Internet Fusion just went down last week - £110m pa business. Plenty of others showing a lot of signs of distress. Yet another Retention of Title form to complete This year we’ve lost customers in Sweden, Germany, UK, Netherlands and USA. Last year we lost 1 in total.

This year we’ve lost customers in Sweden, Germany, UK, Netherlands and USA. Last year we lost 1 in total.

Thankfully I’ve a very robust and effective credit control function, so if we get the stock back we’ll only be down maybe a couple of £k. But others not so much. Someone I know with a large, previously *very* profitable fashion agency is likely closing the whole thing this year - the bottom’s just completely fallen out of it in a double whammy of downturn + shifts in buying.

There’s a lot more pain and bloodshed yet to come in this sector

Internet Fusion just went down last week - £110m pa business. Plenty of others showing a lot of signs of distress. Yet another Retention of Title form to complete

This year we’ve lost customers in Sweden, Germany, UK, Netherlands and USA. Last year we lost 1 in total.Thankfully I’ve a very robust and effective credit control function, so if we get the stock back we’ll only be down maybe a couple of £k. But others not so much. Someone I know with a large, previously *very* profitable fashion agency is likely closing the whole thing this year - the bottom’s just completely fallen out of it in a double whammy of downturn + shifts in buying.

There’s a lot more pain and bloodshed yet to come in this sector

skwdenyer said:

In my world (well, the fashion part of it), there’s still a ton of pain.

There’s a lot more pain and bloodshed yet to come in this sector

Forgive me if you’ve already mentioned it in this thread, and by all means tell me to sod off and mind my own business, but what is it exactly that you do in the fashion world?There’s a lot more pain and bloodshed yet to come in this sector

Design? Manufacturer? By from other manufacturers and sell on to bigger businesses?

I’m seeing strong numbers at my end of the chain, but then I’ve got no idea how slim the margins are, only what volume is being shifted locally.

I have noticed a drop off with M&S, ASOS, Pretty Little Thing and BooHoo, with SHEIN and stuff from Vinted getting ever more popular. Next is up and down, which I’m assuming ties into whatever sales they may or may not be having. Gratans / Freemans is always popular amongst ladies of a certain age.

105.4 said:

skwdenyer said:

In my world (well, the fashion part of it), there’s still a ton of pain.

There’s a lot more pain and bloodshed yet to come in this sector

Forgive me if you’ve already mentioned it in this thread, and by all means tell me to sod off and mind my own business, but what is it exactly that you do in the fashion world?There’s a lot more pain and bloodshed yet to come in this sector

Design? Manufacturer? By from other manufacturers and sell on to bigger businesses?

I’m seeing strong numbers at my end of the chain, but then I’ve got no idea how slim the margins are, only what volume is being shifted locally.

I have noticed a drop off with M&S, ASOS, Pretty Little Thing and BooHoo, with SHEIN and stuff from Vinted getting ever more popular. Next is up and down, which I’m assuming ties into whatever sales they may or may not be having. Gratans / Freemans is always popular amongst ladies of a certain age.

You’re right about margins. Take Internet Fusion - they grew to £110m turnover, but margins were slim-to-none.

Much of fashion has essentially been struggling since the GFC in ‘08. Most of us buy in USD & sell in GBP (and EUR and some USD). GBP was 2 USD back then… Meanwhile wage inflation in places like India has been running at 7.5% pa for 15 years, and commodity prices (especially cotton) have been pretty, err, volatile recently.

During Covid, logistics prices went through the roof. They’ve come down, but not reverted entirely.

And so on. This is why clothes often don’t seem as durable these days (they’re not - they’ve been value-engineered to try to keep increases down); it is why so much moved to China - which has had its own problems of late.

UK online retail is also a major problem area for clothing - people expect free delivery, free returns, and constant discounts / proportions. The rise of “performance marketing” (which basically means paying operations like voucher and cashback sites for clicks) has generated another hand in the till, as it were. Customers expect up to 20% off their first order, and a further promo, and free delivery & free returns (some brands have returns rates in the 50% range - 30% is typical).

Those clicks can easily cost you 10% of the gross sale (before returns) = 15% of net sales (because you still pay to acquire the customer who returned their order). Add, say, 20% off first order, and your acquisition cost has just gone up a lot.

Here are some numbers. Not mine per se, but not unrepresentative of the sector.

Consider a garment selling online at, say, £80. With 20% off your first order, that’s £64 - £53 without VAT. That piece probably cost £15 landed in the UK. Free delivery cost, say, £5, and the free return (at 30% rate) cost £1.75 (average). Pick & pack outbound & return perhaps another £3. You might see 15% loss / unsellable returns, too, so that’s another, say, £0.75 off the bottom line. Consumables, card processing, etc - add another £1.25 per item. And the acquisition cost could easily be £8.

So now you’ve taken £53 and paid out £35. So you’ve made £18 gross (34%). From that you’d have to pay warehousing, design, garment tech, QC, testing, certification, marketing, shoot fees, insurance, PR, admin, accountancy, offices, IT etc. And there will be dead stock each season that needs clearing. And of course the financing cost of acquiring boat loads of stock. So the gross margin over the whole piece is probably closer to 20%. If you’re employing, say, 10 people at an average of £40k per head, and putting them in an office with usual accoutrements, you need to shift probably £3m of net sales to break even - before returns that’s closer to £4.5m of top line sales. Plus VAT

There are an awful lot of brands out there on life support, chasing volume in hopes of being able to ride it out. But actual profit isn’t so easy. Not unless you can offshore an awful lot of the underlying activity to much lower-wage countries.

Internet Fusion (who I mentioned earlier - ran Surfdome, Country Casuals, etc) bought at wholesale. So they were probably paying £27 for an £80 (RRP) garment. Their underlying costs weren’t all that different to the above (no designers, but a lot more marketing spend). It isn’t hard to see how they were still making no money on >£100m of sales.

What you’re seeing is what I’d expect you to say

SHEIN, Next are basically platforms now where others take a lot of the risk (and make no money) - great if you can get it. Same for Vinted - where there a lot of sellers operating either as solo operators without really costing their time.The industry is in a funny place right now. The key is going to be figuring out how to add value for lower in-cost (ie higher in-margin). With the FX rate where it is, that’s now not easy. Throw in a cost of living crisis and you have a perfect storm for a lot of brands to vanish / go bust & be bought up / etc over the next year or so.

skwdenyer said:

105.4 said:

skwdenyer said:

In my world (well, the fashion part of it), there’s still a ton of pain.

There’s a lot more pain and bloodshed yet to come in this sector

Forgive me if you’ve already mentioned it in this thread, and by all means tell me to sod off and mind my own business, but what is it exactly that you do in the fashion world?There’s a lot more pain and bloodshed yet to come in this sector

Design? Manufacturer? By from other manufacturers and sell on to bigger businesses?

I’m seeing strong numbers at my end of the chain, but then I’ve got no idea how slim the margins are, only what volume is being shifted locally.

I have noticed a drop off with M&S, ASOS, Pretty Little Thing and BooHoo, with SHEIN and stuff from Vinted getting ever more popular. Next is up and down, which I’m assuming ties into whatever sales they may or may not be having. Gratans / Freemans is always popular amongst ladies of a certain age.

You’re right about margins. Take Internet Fusion - they grew to £110m turnover, but margins were slim-to-none.

Much of fashion has essentially been struggling since the GFC in ‘08. Most of us buy in USD & sell in GBP (and EUR and some USD). GBP was 2 USD back then… Meanwhile wage inflation in places like India has been running at 7.5% pa for 15 years, and commodity prices (especially cotton) have been pretty, err, volatile recently.

During Covid, logistics prices went through the roof. They’ve come down, but not reverted entirely.

And so on. This is why clothes often don’t seem as durable these days (they’re not - they’ve been value-engineered to try to keep increases down); it is why so much moved to China - which has had its own problems of late.

UK online retail is also a major problem area for clothing - people expect free delivery, free returns, and constant discounts / proportions. The rise of “performance marketing” (which basically means paying operations like voucher and cashback sites for clicks) has generated another hand in the till, as it were. Customers expect up to 20% off their first order, and a further promo, and free delivery & free returns (some brands have returns rates in the 50% range - 30% is typical).

Those clicks can easily cost you 10% of the gross sale (before returns) = 15% of net sales (because you still pay to acquire the customer who returned their order). Add, say, 20% off first order, and your acquisition cost has just gone up a lot.

Here are some numbers. Not mine per se, but not unrepresentative of the sector.

Consider a garment selling online at, say, £80. With 20% off your first order, that’s £64 - £53 without VAT. That piece probably cost £15 landed in the UK. Free delivery cost, say, £5, and the free return (at 30% rate) cost £1.75 (average). Pick & pack outbound & return perhaps another £3. You might see 15% loss / unsellable returns, too, so that’s another, say, £0.75 off the bottom line. Consumables, card processing, etc - add another £1.25 per item. And the acquisition cost could easily be £8.

So now you’ve taken £53 and paid out £35. So you’ve made £18 gross (34%). From that you’d have to pay warehousing, design, garment tech, QC, testing, certification, marketing, shoot fees, insurance, PR, admin, accountancy, offices, IT etc. And there will be dead stock each season that needs clearing. And of course the financing cost of acquiring boat loads of stock. So the gross margin over the whole piece is probably closer to 20%. If you’re employing, say, 10 people at an average of £40k per head, and putting them in an office with usual accoutrements, you need to shift probably £3m of net sales to break even - before returns that’s closer to £4.5m of top line sales. Plus VAT

There are an awful lot of brands out there on life support, chasing volume in hopes of being able to ride it out. But actual profit isn’t so easy. Not unless you can offshore an awful lot of the underlying activity to much lower-wage countries.

Internet Fusion (who I mentioned earlier - ran Surfdome, Country Casuals, etc) bought at wholesale. So they were probably paying £27 for an £80 (RRP) garment. Their underlying costs weren’t all that different to the above (no designers, but a lot more marketing spend). It isn’t hard to see how they were still making no money on >£100m of sales.

What you’re seeing is what I’d expect you to say

SHEIN, Next are basically platforms now where others take a lot of the risk (and make no money) - great if you can get it. Same for Vinted - where there a lot of sellers operating either as solo operators without really costing their time.The industry is in a funny place right now. The key is going to be figuring out how to add value for lower in-cost (ie higher in-margin). With the FX rate where it is, that’s now not easy. Throw in a cost of living crisis and you have a perfect storm for a lot of brands to vanish / go bust & be bought up / etc over the next year or so.

Thanks

C722 said:

Construction (Groundworks) here, very busy at present, lots of enquires and work being secured. Just as busy as the previous 2 years.

Only snag has been the very weather that’s stopped or slowed a few jobs. March was exceptionally bad and April was average but not dry enough to improve the situation much.I think there’s a general reticence to spend as people readjust to the return to normal interest rates.

105.4 said:

Aventador 700 said:

As things go further into these tougher times, this thread is getting more and more sporadic, i guess thats only to be expected as people like delivering good news and not the woes.

can we take it that the quieter this thread, the worse things are getting?

I’m happy to post about the bad times as well as the good. can we take it that the quieter this thread, the worse things are getting?

The year so far:

January sales; Pretty much the same as last year.

February; Very quiet, which personally, was a good thing as I was absolutely exhausted after October-January.

March; It was steady.

April. Busy. 22% up on last year, predominantly from my middle class to millionaires row areas. The benefits area remained constant / slight increase on last year, whilst my working class area had taken a slight dip.

So far in May; Yesterday was my busiest day of the year so far by 135 packages and also my busiest week, but due to the bank holiday, this was over five days instead of the usual six or seven days. The middle class and millionaires row areas are flying, the working class area is picking up nicely and is now busy, whilst my benefits class area remains constant. Next week is forecast to be just as busy as this week has been.

One thing of note is that I’m seeing a lot more smaller packages coming through. The bigger / heavier the parcels the more I get paid for them. I’m going to have to work out this evening how this has affected my average pay per day and see if this trend has reduced my average by a few pence or not.

But to counterbalance that, the cost of diesel has dropped by nearly 10p per litre since February.

I’m already having a lot of customers in my working class, middle class and millionaires row areas telling me that they’re ordering clothes for their holidays, so folk are still spending money on foreign travel. It will be interesting to see how things are during June once all of these Bank Holidays are out of the way.

I deliver parcels to a guy who is a salesman at a local German car dealership, (I won’t say which brand). He’s at the end of my round when I’ve usually got a few minutes in the bag, so we’ll sometimes have a quick chat and compare notes about how busy / quiet we are.

He was telling me that last weekend his dealership did 55 handovers for new cars, (I can’t remember if he said that was on a Saturday or a Sunday), although he did say that he’s seeing a trend in people stating to increase the term that they’re taking finance over.

I’m not in London, or Leeds or Manchester. I’m a smallish, Northern, provincial area. I’m still confused about where folk are getting the money from tbh.

Abroad, france tourism in the less elite south destinations are 50% down, northern france is 100%, fuel & restaurant costs to blame as far as hospitality owners can see.

5* cote d’azur as busy as ever, yet the cheaper accommodation is struggling, another sign of the wealth gap widening or at least the middle earners feeling things sooner.

Yet to hit peak prices/season though, so we’ll see..

Car market throughout france, germany, italy seems pretty stagnant in the classic / investment sector.

American car market in the 500k + is crazy busy and the very wealthy are still spending massively on 10m + houses in spain, 25% rise in the last 12mths

I hope people finding it tough hang on in there and dont give up, there's always been tough times throughout history, stick at it, mop up later is all i can say.

Aventador 700 said:

I hope people finding it tough hang on in there and dont give up, there's always been tough times throughout history, stick at it, mop up later is all i can say.

Recessions tend to be relatively short. I do think at certain levels, the uk is effectively in a real terms recession if you look at GDP factoring in inflation. I also think it will recover, although I think the present government and the opposition are as disconnected from real business as is possible. Clueless.Gassing Station | Business | Top of Page | What's New | My Stuff