Previous work pension - what to do? - haven't a clue!

Discussion

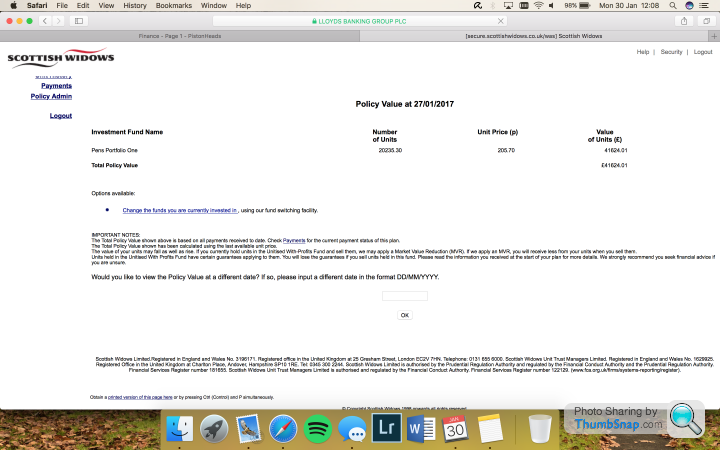

I have a pension with Scottish Widows in the fund 'Pension Portfolio One'.

I last looked at the value on 2/06/2016 = £33,570

I'm 33, i'm not paying into it. Should I transfer it? Pay a small fee into it? Leave it? I dont really like the idea of Pension and would rather invest in something else (property at the moment!).

Open to suggestions.

Thanks in advance for the info!

I last looked at the value on 2/06/2016 = £33,570

I'm 33, i'm not paying into it. Should I transfer it? Pay a small fee into it? Leave it? I dont really like the idea of Pension and would rather invest in something else (property at the moment!).

Open to suggestions.

Thanks in advance for the info!

I'd check the fees and charges first - if it is a low cost wrapper it probably makes sense to leave it there. If, not, perhaps transfer it to a SIPP and stick it in a different fund from there.

I don't understand your comment about not liking the idea of a pension? - What's not to like - Pensions are one of the best savings vehicles available. You get full tax relief on the way in and the opportunity for it to grow for the next ~20 years. You can manage it yourself and be a stock picker or let a managed fund take care of it. In all likelihood, you can take it out tax free (ish) and it is inheritable.....Tough to beat with any other investment scheme. As part of a balanced approach to saving, It is unlikely you will regret paying into a pension scheme.

In terms of where you are, 33k at 33 is not a lot to have in a pension imho, I would be looking to add to it in one way or another - especially if you can make use of employers contributions as well.

Have a look at some of the online calculators and assess how much you think you should have at age 40 and you'll probably start worrying that you are way behind or are going to end up old and poor.

I'd also check the value now - the last 9 months have probably been quite kind to the pot value - I know mine has rocketed in that time but I still feel as though it is behind where I want it to be.

Bob

I don't understand your comment about not liking the idea of a pension? - What's not to like - Pensions are one of the best savings vehicles available. You get full tax relief on the way in and the opportunity for it to grow for the next ~20 years. You can manage it yourself and be a stock picker or let a managed fund take care of it. In all likelihood, you can take it out tax free (ish) and it is inheritable.....Tough to beat with any other investment scheme. As part of a balanced approach to saving, It is unlikely you will regret paying into a pension scheme.

In terms of where you are, 33k at 33 is not a lot to have in a pension imho, I would be looking to add to it in one way or another - especially if you can make use of employers contributions as well.

Have a look at some of the online calculators and assess how much you think you should have at age 40 and you'll probably start worrying that you are way behind or are going to end up old and poor.

I'd also check the value now - the last 9 months have probably been quite kind to the pot value - I know mine has rocketed in that time but I still feel as though it is behind where I want it to be.

Bob

jinkster said:

I have a pension with Scottish Widows in the fund 'Pension Portfolio One'.

I last looked at the value on 2/06/2016 = £33,570

I'm 33, i'm not paying into it. Should I transfer it? Pay a small fee into it? Leave it? I dont really like the idea of Pension and would rather invest in something else (property at the moment!).

1. That doesn't really make sense, a pension is a (tax efficient) investment wrapper not an asset class. I last looked at the value on 2/06/2016 = £33,570

I'm 33, i'm not paying into it. Should I transfer it? Pay a small fee into it? Leave it? I dont really like the idea of Pension and would rather invest in something else (property at the moment!).

2. You can hold property within a pension

3. You can't just take money out of your pension to do what you want with!

jinkster said:

Open to suggestions.

Thanks in advance for the info!

Shouldn't you check how the portfolio is performing at the moment before deciding whether to add new money to it or transfer it?Thanks in advance for the info!

jinkster said:

Scottish Widows platform only operates during office hours

Seriously???!!! If so it is the only one that does that I have ever heard of.As has already been said, a personal pension is simply a tax wrapper (or allowance) and about the best there is. Nothing not to like and everything to like.

Don't confuse it with the investment held within it. Life insurance companies used to restrict you to holding their own investment funds when they ran the tax wrapper for you.

Nowdays you have far more choice, including SIPPs (Self Invested Personal Pensions) which are exactly the same thing but where you pick pretty much any investment you like within your pension.

This can include thousands of managed funds, shares in pretty much any companies you like, bonds, cash, commercial property (not residential though), land, gold bullion, etc. You can even borrow up to half the value of your SIPP to invest in property and land.

Pensions are great, they only have a bad reputation because of bad fund performance from some life insurance companies that used to have a monopoly on selling them with only their funds available to invest in.

http://www.scottishwidows.co.uk/global/log_in_or_r...

Our eServices are available Mon–Fri 8am–8pm and Sat 8am–5pm. Some of our products may be available outside these hours.

Crazy isn't it! I'll check out the SIPP and look at transferring.

Thanks for the help

Our eServices are available Mon–Fri 8am–8pm and Sat 8am–5pm. Some of our products may be available outside these hours.

Crazy isn't it! I'll check out the SIPP and look at transferring.

Thanks for the help

jinkster said:

Annual fee is 0.550%

Should I switch it somewhere else?

https://www.trustnet.com/Factsheets/Factsheet.aspx...

I would just check the annual fee again (for the pension wrapper AND the fund itself) and if it is a total of 0.55% I can see no reason for moving it quite frankly.

JulianPH said:

jinkster said:

Annual fee is 0.550%

Should I switch it somewhere else?

https://www.trustnet.com/Factsheets/Factsheet.aspx...

I would just check the annual fee again (for the pension wrapper AND the fund itself) and if it is a total of 0.55% I can see no reason for moving it quite frankly.

Gassing Station | Finance | Top of Page | What's New | My Stuff