£5k, short term investment?

Discussion

I have £5k to invest for a period of 2 to 3 years depending on how other things go.

I currently have this in a savings account with nets me around 1% interest (more than my ISA).

I am sure that there is a better place for this, but not sure where that is. Any recommendations? Thanks.

I currently have this in a savings account with nets me around 1% interest (more than my ISA).

I am sure that there is a better place for this, but not sure where that is. Any recommendations? Thanks.

Over that period look at banks offering the best interest rates.

For example, nationwide flex direct offers 5% on £2.5k for a year. You can then also use a linked saver at 5%, but you can only put in an amount per month, not in one go, so the headline interest rate isn't on the full amount.

Other banks do similar things so take a look, Tesco 3% on £3k for example.

You'll probably have to move things around each year as most rates are for 12 months only.

For example, nationwide flex direct offers 5% on £2.5k for a year. You can then also use a linked saver at 5%, but you can only put in an amount per month, not in one go, so the headline interest rate isn't on the full amount.

Other banks do similar things so take a look, Tesco 3% on £3k for example.

You'll probably have to move things around each year as most rates are for 12 months only.

Viper said:

picking a few decent funds for ISA is the key, mine are currently 20% and 15% so far this year

Even a 3 year term, on a small investment has got to be worth a try with the lowly being rates offered elsewhere

Only if you can afford to accept a 10-20% loss on your investment!Even a 3 year term, on a small investment has got to be worth a try with the lowly being rates offered elsewhere

Edited by Viper on Thursday 10th August 21:38

Why not hedge your bets and split your funds over multiple investments?

Funding Circle offer 50 quid cash back with an invitation and I agree that the 5% Nationwide deal is fantastic (I have it myself, but there's a caveat - you have to pay in 1k per month, although it's no problem to move it out again to another account after a few days!)

2.5K in each gives you a guaranteed return of 5% over a year on half your investment, an instant 2% return on the other (50 pound cashback for 2.5K investment) with a potential return of 10%. In my experience (only of a year) just a fraction of FC loans default, and I'm in profit so far at over 8% on 9K but maybe I'm just lucky! :/

but maybe I'm just lucky! :/

The Funding Circle ISA (IFISA) will also be available soon, but not just yet. Not that 5K will attract tax, but if you get bitten by the p2p bug then it's worth knowing

Funding Circle offer 50 quid cash back with an invitation and I agree that the 5% Nationwide deal is fantastic (I have it myself, but there's a caveat - you have to pay in 1k per month, although it's no problem to move it out again to another account after a few days!)

2.5K in each gives you a guaranteed return of 5% over a year on half your investment, an instant 2% return on the other (50 pound cashback for 2.5K investment) with a potential return of 10%. In my experience (only of a year) just a fraction of FC loans default, and I'm in profit so far at over 8% on 9K

but maybe I'm just lucky! :/The Funding Circle ISA (IFISA) will also be available soon, but not just yet. Not that 5K will attract tax, but if you get bitten by the p2p bug then it's worth knowing

Edited by jzbc on Saturday 12th August 09:41

Edited by jzbc on Sunday 13th August 11:51

Over 3 full years you'll be very very unlikely to not beat inflation and savings rates in a conservatively managed global equity fund concentrating on high value companies, something like Fundsmith. Or a global tracker, just stay invested and don't lose your bottle if it takes a dip.

FredClogs said:

Over 3 full years you'll be very very unlikely to not beat inflation and savings rates in a conservatively managed global equity fund concentrating on high value companies, something like Fundsmith. Or a global tracker, just stay invested and don't lose your bottle if it takes a dip.

2017 is the 30th year of me being an equity enthusiast, however, I would not suggest equities to the OP.

OP states 'for a period of 2 to 3 years'.

It breaks one of the golden rules, to invest in equities with any intention of withdrawing funds after a specific short-term period.

If your withdrawal time coincides with a market fall and you have to sell at a loss, you will regret ever getting involved (as many novice investors discover unfortunately).

Edited by Jon39 on Saturday 12th August 19:04

jzbc said:

Why not hedge your bets and split your funds over multiple investments?

Funding Circle offer 50 quid cash back with an invitation and I agree that the 5% Nationwide deal is fantastic (I have it myself, but there's a caveat - you have to pay in 1k per month, although it's no problem to move it out again to another account after a few days!)

2.5K in each gives you a guaranteed return of 5% over a year on half your investment, an instant 2% return on the other (50 pound cashback for 2.5K investment) with a potential return of 10%. In my experience (only of a year) just a fraction of FC loans default, and I'm in profit so far at over 8% on 9K but maybe I'm just lucky! :/

The Funding Circle ISA (IFISA) will also be available soon, but not just yet. Not that 5K will attract tax, but if you get bitten by the p2p bug then it's worth knowing

I should note that p2p isn't as risky as it sounds Funding Circle offer 50 quid cash back with an invitation and I agree that the 5% Nationwide deal is fantastic (I have it myself, but there's a caveat - you have to pay in 1k per month, although it's no problem to move it out again to another account after a few days!)

2.5K in each gives you a guaranteed return of 5% over a year on half your investment, an instant 2% return on the other (50 pound cashback for 2.5K investment) with a potential return of 10%. In my experience (only of a year) just a fraction of FC loans default, and I'm in profit so far at over 8% on 9K

but maybe I'm just lucky! :/The Funding Circle ISA (IFISA) will also be available soon, but not just yet. Not that 5K will attract tax, but if you get bitten by the p2p bug then it's worth knowing

according to FC:

according to FC:Funding Circle said:

- Lend to 100+ businesses

- Lend no more than 1% of your total to each one

Every investor who has followed these two steps has earned a positive return. 92% have earned 5% or more. Correct as of 1st April 2017.

If default is a serious concern then an investor can always stick with A+ (safest) loans to lessen their exposure..- Lend no more than 1% of your total to each one

Every investor who has followed these two steps has earned a positive return. 92% have earned 5% or more. Correct as of 1st April 2017.

tharriso said:

Funding Circle

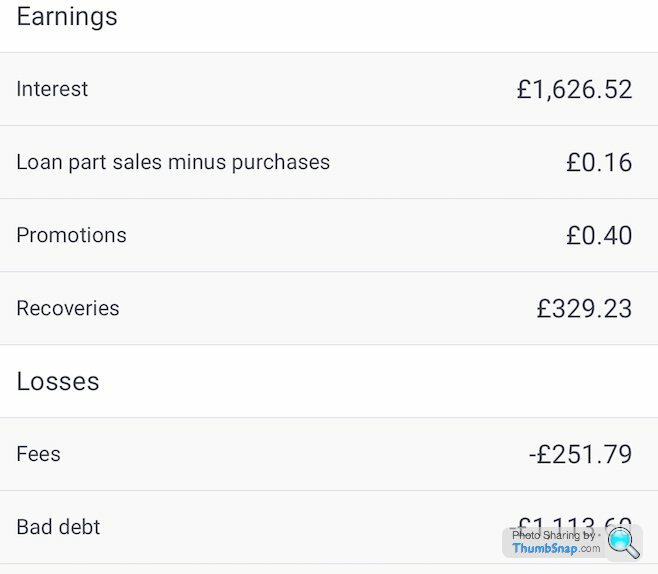

I invested some proceeds of a house sale into P2P lending 18 months ago (FC, Zopa, lending works)/.Funding Circle was BY FAR the worst. Put in £15,000. Most gains lost to BAD DEBT and fees. and these were A+ loans (see below).

Fortunately I got my capital out within a couple of days.

The best performer was Zopa. No bad debt. Minimal fees. And very easy to transfer in and out.

Edited by audidoody on Tuesday 15th August 11:28

audidoody said:

I invested some proceeds of a house sale into P2P lending 18 months ago (FC, Zopa, lending works)/.

Funding Circle was BY FAR the worst. Put in £15,000. Most gains lost to BAD DEBT and fees. and these were A+ loans (see below).

Fortunately I got my capital out within a couple of days.

The best performer was Zopa. No bad debt. Minimal fees. And very easy to transfer in and out.

I assume that Funding Circle have their own (internal) loan rating approach which is inconsistent with the official ECAI rating agencies, so that an A+ loan on Funding circle is in no way compatible with an A+ compote bond rated A+ by S&P?!Funding Circle was BY FAR the worst. Put in £15,000. Most gains lost to BAD DEBT and fees. and these were A+ loans (see below).

Fortunately I got my capital out within a couple of days.

The best performer was Zopa. No bad debt. Minimal fees. And very easy to transfer in and out.

Edited by audidoody on Tuesday 15th August 11:28

I imagine that this is done deliberately to confuse less informed investors?

edited to add this last comment certainly wasn't directed at you, audidoody!

Edited by sidicks on Tuesday 15th August 16:08

Gassing Station | Finance | Top of Page | What's New | My Stuff