Low Valuation - Insurance write off

Discussion

Hi everyone!

My wife drives a 2008 Porsche Cayenne GTS, has 111k, full service history, every single possible option and some rare ones at that. Spectacular condition.

She caught the front left corner on a fence which damaged the headlight, wing and bumper. A bodyshop has quoted £5000 to repair, I could personally have everything done, using second hand parts for about around £2.5k-£3k which I’d rather not, I’d prefer to go through her insurance and have them repair it rather than short change us/categorise the car.

However, they have said it’s a write off and offered £7.6k.

NO!

I sent a ton of evidence, 5 examples of cars on the market, a valuation from Porsche club GB (£13k), and photos of the car. Now this car, is EXTREMELY clean, show condition, it is immaculate as I’m very particular, I clean the inner arches out, underside and regularly detail the car. I used to win shows with some of my other cars so I’m not exaggerating on its condition being very clean. It’s also had a ton spent recently on new Michelin tyres, full set of wishbones, arms, steering joints and so on, it drives perfect.

Anyway, after submitting the evidence, I got a re-evaluation today of £8.5k.

Now I am under the impression that the valuation should enable us to buy a like for like car…

I think £8.5k is below the belt, the worst example on the market with 150k is up for this figure! The next example is £9990! The top being a 56k mile car for £15k and in the middle, a 100k mile car for £12k. All of which have less options and not as desirable, IMO.

Heres is their email with this new valuation in reply to all of the evidence which I sent in.

“We review Market guides such as Glass’s Guide, Parkers and CAPS which are considered to be a reliable source for valuing used vehicles. This is because their figures take into account the make and model of a vehicle and its age, mileage and condition. Crucially, their values are based on actual sale transactions as opposed to asking prices which reflect the sellers’ highest expectations and are inevitably subject to negotiation.

We also look into online adverts to see the current market advertised prices, this helps us determine if the guides are in line with real world values.

Upon review I am in a position to offer a value of £8500.00 to settle your claim.

The value offered would be less any contractual agreements you have under your insurance policy.

If you feel that you can accept the value offered, then please let me know and I will submit the file back to our claims team to consider raising payment.”

A lot of questions come to mind, how do “Crucially, their values are based on actual sale transactions as opposed to asking prices” ok, do they know every sale transaction from the likes of eBay and other marketplaces? I doubt it..

Then a contradiction of “asking prices” yet they then go on to look at online adverts… well you clearly haven’t as you’d see that from the few on the market, mine is not comparable to an £8.5k example.

Clearly an email template they send or a joke.

What do I do, am I right to be angry? I want them to either raise the value to what it should be and fix the car or payout a value over £11k. Then I will buy it back and repair. Appreciate any advice here.

Thanks

My wife drives a 2008 Porsche Cayenne GTS, has 111k, full service history, every single possible option and some rare ones at that. Spectacular condition.

She caught the front left corner on a fence which damaged the headlight, wing and bumper. A bodyshop has quoted £5000 to repair, I could personally have everything done, using second hand parts for about around £2.5k-£3k which I’d rather not, I’d prefer to go through her insurance and have them repair it rather than short change us/categorise the car.

However, they have said it’s a write off and offered £7.6k.

NO!

I sent a ton of evidence, 5 examples of cars on the market, a valuation from Porsche club GB (£13k), and photos of the car. Now this car, is EXTREMELY clean, show condition, it is immaculate as I’m very particular, I clean the inner arches out, underside and regularly detail the car. I used to win shows with some of my other cars so I’m not exaggerating on its condition being very clean. It’s also had a ton spent recently on new Michelin tyres, full set of wishbones, arms, steering joints and so on, it drives perfect.

Anyway, after submitting the evidence, I got a re-evaluation today of £8.5k.

Now I am under the impression that the valuation should enable us to buy a like for like car…

I think £8.5k is below the belt, the worst example on the market with 150k is up for this figure! The next example is £9990! The top being a 56k mile car for £15k and in the middle, a 100k mile car for £12k. All of which have less options and not as desirable, IMO.

Heres is their email with this new valuation in reply to all of the evidence which I sent in.

“We review Market guides such as Glass’s Guide, Parkers and CAPS which are considered to be a reliable source for valuing used vehicles. This is because their figures take into account the make and model of a vehicle and its age, mileage and condition. Crucially, their values are based on actual sale transactions as opposed to asking prices which reflect the sellers’ highest expectations and are inevitably subject to negotiation.

We also look into online adverts to see the current market advertised prices, this helps us determine if the guides are in line with real world values.

Upon review I am in a position to offer a value of £8500.00 to settle your claim.

The value offered would be less any contractual agreements you have under your insurance policy.

If you feel that you can accept the value offered, then please let me know and I will submit the file back to our claims team to consider raising payment.”

A lot of questions come to mind, how do “Crucially, their values are based on actual sale transactions as opposed to asking prices” ok, do they know every sale transaction from the likes of eBay and other marketplaces? I doubt it..

Then a contradiction of “asking prices” yet they then go on to look at online adverts… well you clearly haven’t as you’d see that from the few on the market, mine is not comparable to an £8.5k example.

Clearly an email template they send or a joke.

What do I do, am I right to be angry? I want them to either raise the value to what it should be and fix the car or payout a value over £11k. Then I will buy it back and repair. Appreciate any advice here.

Thanks

How is it a write off if it costs £5,000 to repair yet the insurance company is offering you £8,500

Also if its worth what you say then you let them write it off and keep the salvage and repair it for the reduced amount using second hand parts then you are well in profit and you still have the car.

?

Also if its worth what you say then you let them write it off and keep the salvage and repair it for the reduced amount using second hand parts then you are well in profit and you still have the car.

?

OP, I can understand your frustration, but try to avoid getting angry with whoever you are dealing with. You have a few options:

1. Stand your ground and refuse to accept their offer. I had similar some years back, and it was clear the insurer were basing their values on trade prices, as if I wished to part exchange the car, rather than buy a replacement. I went several rounds, like you providing evidence. It was raised to a more senior claims negotiator, still with slow progress. I suggested that I would be happy for them to provide a replacement vehicle if they were confident they could find one for the price they suggested. Eventually, they came back with a figure I was content with. (Which probably equated to a hard bargained private sale figure)

2. As suggested above, try to argue for the company to repair. Get a few quotes and show the insurer their loss would be lower to repair than write-off - assuming you don't expect hire cars etc provided. Both win here - the insurer saves, and you get your immaculate car back without an insurance marker.

3. Ask what the insurer would charge you to buy back at scrap value. Maybe £8500 payout with £1500 or so to buy back for you to repair wouldn't be so bad?

4. Don't claim at all, bite the bullet and get it fixed at your expense (you'd loose less than just accepting £8500 if your figures are right)

Annoying, I know, but there are several ways you could approach it. Good luck.

1. Stand your ground and refuse to accept their offer. I had similar some years back, and it was clear the insurer were basing their values on trade prices, as if I wished to part exchange the car, rather than buy a replacement. I went several rounds, like you providing evidence. It was raised to a more senior claims negotiator, still with slow progress. I suggested that I would be happy for them to provide a replacement vehicle if they were confident they could find one for the price they suggested. Eventually, they came back with a figure I was content with. (Which probably equated to a hard bargained private sale figure)

2. As suggested above, try to argue for the company to repair. Get a few quotes and show the insurer their loss would be lower to repair than write-off - assuming you don't expect hire cars etc provided. Both win here - the insurer saves, and you get your immaculate car back without an insurance marker.

3. Ask what the insurer would charge you to buy back at scrap value. Maybe £8500 payout with £1500 or so to buy back for you to repair wouldn't be so bad?

4. Don't claim at all, bite the bullet and get it fixed at your expense (you'd loose less than just accepting £8500 if your figures are right)

Annoying, I know, but there are several ways you could approach it. Good luck.

I had similar for my claim.

It's not like for like. The settlement I was offered wouldn't have paid for a similar age/spec/mileage replacement.

I did some digging, and the comparison they use is the industry standard, the Financal Ombudsman states it's the market value.

https://www.financial-ombudsman.org.uk/consumers/c...

Before I agreed the settlement, the insurance offered an extra £500. Wasn't much but I put it all towards a new (to me) car, same model, newer, higher spec, similar milage, at the cost of about £1500 to me.

I think your opinions are

A) pay for the repairs yourself

B) accept the fact you're not getting "like for like".

Good luck, however you choose to proceed

It's not like for like. The settlement I was offered wouldn't have paid for a similar age/spec/mileage replacement.

I did some digging, and the comparison they use is the industry standard, the Financal Ombudsman states it's the market value.

https://www.financial-ombudsman.org.uk/consumers/c...

Before I agreed the settlement, the insurance offered an extra £500. Wasn't much but I put it all towards a new (to me) car, same model, newer, higher spec, similar milage, at the cost of about £1500 to me.

I think your opinions are

A) pay for the repairs yourself

B) accept the fact you're not getting "like for like".

Good luck, however you choose to proceed

Post copied from another post I made on a different thread of my personal experiences:

For those who don't need to read this look away as it is a long one for which I will apologise, but for the OP, take heed.

I was subject to exactly this (not yours, mine was parked at the side of the road) accident just over a year ago, you will have a fight on your hands but you need to be well prepared & willing to put up a fight.

I was up against Admiral, which is never a good start, and after telling my own ins. co. they said just to deal with the other company unless I had issues.

In the first instance they told me to get quotes for repair, which I couldn't even get a quote for over 2 weeks, so when I got a call from them & said that the car was also pushed into the next one down the road they said it is very rare that a front & rear won't be written off.

I had a look behind both bumper covers & realised that there was damage underneath so agreed to the car being a write off and then the problems started.

They said I could get a hire car replacement but that if I didn't need one the (maximum) £400 for that would be added to the settlement, we have another car, and I was off work for another 3 weeks, so decided to go this way.

They asked for pictures & replacement costs via a specific email address, so I took them found some similar cars to back up the claim of £5500 I was asking for and sent them off.

3 days later I had still heard nothing so spent the next 3 days trying every email address & phone number I could find and even raised a complaint via their website, but still nothing.

Then randomly on the next day the person I had spoken to & asked for the info phoned me & asked why I was delaying? Obviously I said I wasn't delaying & had actually done exactly what she asked for, so she said she will get back to me later that day.

By this time I was already looking for a replacement & went for a couple of test drives on a different car as what I previously had was a very rare spec (although not rare as in valuable) when I had a call back to say that they had agreed the write off and the pick up for my car was happening the next day & I needed to remove my personal plate, which I did.

On the way to seeing another car we stopped off for my wife to get some stuff from asda & while I was waiting inn the car they phoned back to agree a settlement.

She initially said (after some pre-amble) that they were willing to offer £2600, which I obviously declined in the strongest possible terms.

I then told her what to look for in autotrader & she said she had found one for £2850, and I told her to read the ad to me.

Wrong model, wrong age, wrong engine, wrong spec!

I reiterated that the closest ones in spec that I had found (not identical) were all £5500 to £5800 and that as I was the innocent third party who was legally parked on the side of the road before their clint decided to use my car instead of his brakes that I wanted to be in the same position as beforehand.

She swiftly upped the offer to a random £3800.

I then asked her where this valuation came from, to which she said "Glass's Guide" so I then asked her what the word "guide" meant and did it mean that it was a complete pricing quotation device for all exact cars or just a guide to aid valuation? Did it list my precise spec & did it give a price for my car? Which obviously it didn't.

I repeated the above about my personal valuation & insisted that I would not settle for under £5500 and was willing to enlist the Insurance Ombudsman and my own insurance company & legal assistance if needed to do so.

She then upped the offer to £4850 & added the £400 mentioned above for a hire car, then £250 for allowing just them to deal rather than accident management/my ins.co. etc £80 for transferring my personal plate which came to £5580 and I accepted.

This all took about 30 min on the phone & whilst I was VERY firm & insistant & would not be talked over no matter how many times she tried I never lost my cool & never used any obtuse language.

This is the only way to deal with them, you need to be FULLY armed & prepared to do battle, because it WILL happen.

ETA. I forgot to say that just over a week after the payout, I got an letter from Admiral saying that the complaint I raised had been found in my favour and here is a £100 cheque to compensate you, which was a nice little bonus.

For those who don't need to read this look away as it is a long one for which I will apologise, but for the OP, take heed.

I was subject to exactly this (not yours, mine was parked at the side of the road) accident just over a year ago, you will have a fight on your hands but you need to be well prepared & willing to put up a fight.

I was up against Admiral, which is never a good start, and after telling my own ins. co. they said just to deal with the other company unless I had issues.

In the first instance they told me to get quotes for repair, which I couldn't even get a quote for over 2 weeks, so when I got a call from them & said that the car was also pushed into the next one down the road they said it is very rare that a front & rear won't be written off.

I had a look behind both bumper covers & realised that there was damage underneath so agreed to the car being a write off and then the problems started.

They said I could get a hire car replacement but that if I didn't need one the (maximum) £400 for that would be added to the settlement, we have another car, and I was off work for another 3 weeks, so decided to go this way.

They asked for pictures & replacement costs via a specific email address, so I took them found some similar cars to back up the claim of £5500 I was asking for and sent them off.

3 days later I had still heard nothing so spent the next 3 days trying every email address & phone number I could find and even raised a complaint via their website, but still nothing.

Then randomly on the next day the person I had spoken to & asked for the info phoned me & asked why I was delaying? Obviously I said I wasn't delaying & had actually done exactly what she asked for, so she said she will get back to me later that day.

By this time I was already looking for a replacement & went for a couple of test drives on a different car as what I previously had was a very rare spec (although not rare as in valuable) when I had a call back to say that they had agreed the write off and the pick up for my car was happening the next day & I needed to remove my personal plate, which I did.

On the way to seeing another car we stopped off for my wife to get some stuff from asda & while I was waiting inn the car they phoned back to agree a settlement.

She initially said (after some pre-amble) that they were willing to offer £2600, which I obviously declined in the strongest possible terms.

I then told her what to look for in autotrader & she said she had found one for £2850, and I told her to read the ad to me.

Wrong model, wrong age, wrong engine, wrong spec!

I reiterated that the closest ones in spec that I had found (not identical) were all £5500 to £5800 and that as I was the innocent third party who was legally parked on the side of the road before their clint decided to use my car instead of his brakes that I wanted to be in the same position as beforehand.

She swiftly upped the offer to a random £3800.

I then asked her where this valuation came from, to which she said "Glass's Guide" so I then asked her what the word "guide" meant and did it mean that it was a complete pricing quotation device for all exact cars or just a guide to aid valuation? Did it list my precise spec & did it give a price for my car? Which obviously it didn't.

I repeated the above about my personal valuation & insisted that I would not settle for under £5500 and was willing to enlist the Insurance Ombudsman and my own insurance company & legal assistance if needed to do so.

She then upped the offer to £4850 & added the £400 mentioned above for a hire car, then £250 for allowing just them to deal rather than accident management/my ins.co. etc £80 for transferring my personal plate which came to £5580 and I accepted.

This all took about 30 min on the phone & whilst I was VERY firm & insistant & would not be talked over no matter how many times she tried I never lost my cool & never used any obtuse language.

This is the only way to deal with them, you need to be FULLY armed & prepared to do battle, because it WILL happen.

ETA. I forgot to say that just over a week after the payout, I got an letter from Admiral saying that the complaint I raised had been found in my favour and here is a £100 cheque to compensate you, which was a nice little bonus.

If you wanted your car insured for a particular amount, you should have bought a policy with an agreed value for the vehicle. Yes it will cost more, but it avoids this sort of issue.

No help to the OP right now I guess, but maybe for when you take out future insurance for a car you deem to be much better than average.

No help to the OP right now I guess, but maybe for when you take out future insurance for a car you deem to be much better than average.

I suppose you need a WBAC valuation as the trade price - as it should be above that.

Also a full list of comparable vehicles for sale on Autotrader and EBay motors.

Your spec and options aren’t really worth more money, but you should be able to get yourself into something comparable after a fight.

I only had one write off, with Direct Line, their opening offer was higher than I had prepared for and when I hesitated thinking about it they upped it a bit and I was right in the middle of the range of advertised similar cars.

Also a full list of comparable vehicles for sale on Autotrader and EBay motors.

Your spec and options aren’t really worth more money, but you should be able to get yourself into something comparable after a fight.

I only had one write off, with Direct Line, their opening offer was higher than I had prepared for and when I hesitated thinking about it they upped it a bit and I was right in the middle of the range of advertised similar cars.

last year my 3 series was written off and the first offer from the insurance was about half the cost it would be to replace the vehicle like for like.

i complained they raised the offer but ti was still below the 'market' value. they said that was the final offer.

they paid the money to my bank account

I raised a complaint with the ombudsman who took over a month to review and sided with me and the insurance eventually sent me an the extra to arrive at market value

The insurance company kept quoting prices from a book they said is what they used but the policy booklet stated market value to replace the vehicle with a similar spec which is what the ombudsman pulled them on.

i complained they raised the offer but ti was still below the 'market' value. they said that was the final offer.

they paid the money to my bank account

I raised a complaint with the ombudsman who took over a month to review and sided with me and the insurance eventually sent me an the extra to arrive at market value

The insurance company kept quoting prices from a book they said is what they used but the policy booklet stated market value to replace the vehicle with a similar spec which is what the ombudsman pulled them on.

Thanks to each and every one of you, very helpful replies indeed.

To be honest, for this car, as my wifes run around, I never thought to give an agreed value like I do with some of my others, I never anticipated or realised, how scamming insurance companies can be. In 20 years, I have only had 1 experience of insurance and that was from a neighbour hitting a car of mine, I just had to take 1 phone call and my car was collected while a courtesy car was dropped off and the damage was reversed, great!

This however, has been hassle from the beginning, this is with Hastings Direct and I can only take it as a lesson for the future, we're always learning..

They provided a list of bodyshops for me to choose from, all with 1 or 2 star ratings, I was told I could choose my own but they would charge £250 for the pleasure. Anyway, I was offered a bigger list and found a bodyshop with 5 star google ratings and photos of good work, so went with that. 2 weeks went by and not a peep, nothing, I called to complain that my wife has been left with a car that has a broken headlight (I had actually made best of this so that the car could be used) and that we need a courtesy car that will get 2 prams in and the variety of kids stuff.. 5 days and many phone calls went by and a Fiat 500 turns up... okkkkkkkk! Never heard from any bodyshops, I had to chase and chase and chase.

After they called to give the news of the £7k valuation and that they will write it off, the Fiat 500 was promptly collected the next day! I thought that was harsh and the lady on the phone was practically laughing. Couldn't believe it.

Anyway, I am where I am now, I don't think I am dreaming with my valuation, there are very few Cayenne 957 GTS's on the market and mine is certainly the best of the bunch. So I will construct a reply to ensure they have actually read my evidence pack and request that they find me a similar car I can buy for £8.5k.

Noted on the ombudsman and will check out my policy details now.

Thanks again all!

To be honest, for this car, as my wifes run around, I never thought to give an agreed value like I do with some of my others, I never anticipated or realised, how scamming insurance companies can be. In 20 years, I have only had 1 experience of insurance and that was from a neighbour hitting a car of mine, I just had to take 1 phone call and my car was collected while a courtesy car was dropped off and the damage was reversed, great!

This however, has been hassle from the beginning, this is with Hastings Direct and I can only take it as a lesson for the future, we're always learning..

They provided a list of bodyshops for me to choose from, all with 1 or 2 star ratings, I was told I could choose my own but they would charge £250 for the pleasure. Anyway, I was offered a bigger list and found a bodyshop with 5 star google ratings and photos of good work, so went with that. 2 weeks went by and not a peep, nothing, I called to complain that my wife has been left with a car that has a broken headlight (I had actually made best of this so that the car could be used) and that we need a courtesy car that will get 2 prams in and the variety of kids stuff.. 5 days and many phone calls went by and a Fiat 500 turns up... okkkkkkkk! Never heard from any bodyshops, I had to chase and chase and chase.

After they called to give the news of the £7k valuation and that they will write it off, the Fiat 500 was promptly collected the next day! I thought that was harsh and the lady on the phone was practically laughing. Couldn't believe it.

Anyway, I am where I am now, I don't think I am dreaming with my valuation, there are very few Cayenne 957 GTS's on the market and mine is certainly the best of the bunch. So I will construct a reply to ensure they have actually read my evidence pack and request that they find me a similar car I can buy for £8.5k.

Noted on the ombudsman and will check out my policy details now.

Thanks again all!

Checked policy. valuation should be "up to market value at time of incident"

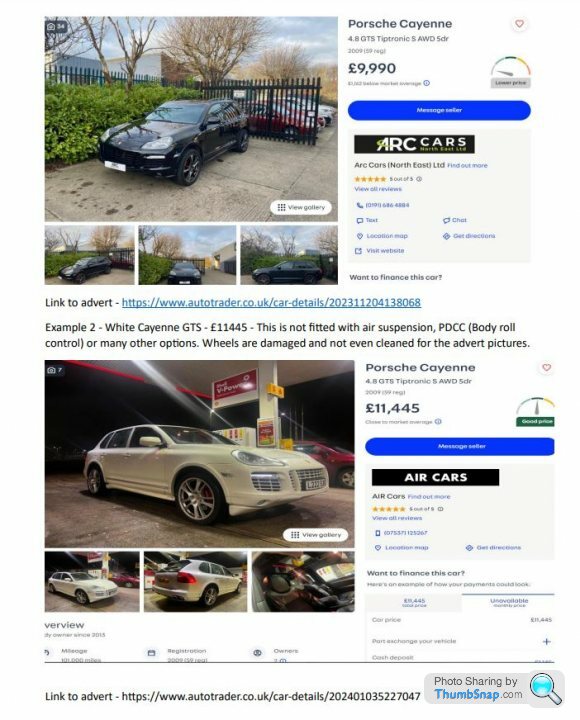

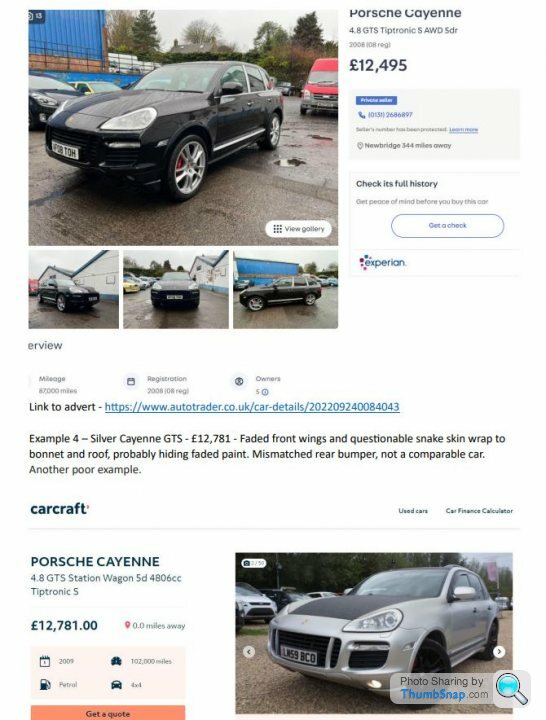

Below are the examples of cars and info, which I sent to them as part of the evidence I gathered.

Just for reference, these are the only GTS models available.

I don't expect to get £13k but I don't think £11k is unreasonable, which should warrant a repair!

Although I am becoming open to an offer of £10k, having them write the vehicle off and then allow me to purchase it back, but this depends on what the re-purchase cost would be. Do they take the vehicle and assses or simply offer a buy back figure over the phone to save the logistics? I don't anticipate selling this vehicle, we will run it until the engine or gearbox gives up the ghost so a cat rating on the vehicle won't be so bad.

My mind is all over the place (busy time for my businesses) so forgive any inconsistent thoughts I type here.

Below are the examples of cars and info, which I sent to them as part of the evidence I gathered.

Just for reference, these are the only GTS models available.

I don't expect to get £13k but I don't think £11k is unreasonable, which should warrant a repair!

Although I am becoming open to an offer of £10k, having them write the vehicle off and then allow me to purchase it back, but this depends on what the re-purchase cost would be. Do they take the vehicle and assses or simply offer a buy back figure over the phone to save the logistics? I don't anticipate selling this vehicle, we will run it until the engine or gearbox gives up the ghost so a cat rating on the vehicle won't be so bad.

My mind is all over the place (busy time for my businesses) so forgive any inconsistent thoughts I type here.

kestral said:

How is it a write off if it costs £5,000 to repair yet the insurance company is offering you £8,500

Also if its worth what you say then you let them write it off and keep the salvage and repair it for the reduced amount using second hand parts then you are well in profit and you still have the car.

?

The reason is that you can't directly compare the payout vs the cost of the repair. You have to then add in the additional costs whilst the car is in the garage awaiting repair - You'll be in a courtesy car that the insurance is stumping up for. When combining the rental costs with the fact that insurance repairs require new OEM parts only, you could be in a courtesy car for a long time and that quickly tickets that £5k in to >£8.5k in costs.Also if its worth what you say then you let them write it off and keep the salvage and repair it for the reduced amount using second hand parts then you are well in profit and you still have the car.

?

During peak COVID some of the times in courtesy cars were stretching way over 6months as parts backlogs were (and some still are) absolutely nuts.

Trax said:

Can you find the retail value that CAP, Cazoo Glass' etc give for your car? That's what the Ombudsman will say they have to pay, which gives the market value.

This is the thing - insurers appear to pay out at Glasses/CAP, but regular punters don’t buy their cars at CAP, they either buy them private or from a dealer with their markup. there are 2 options for keeping the vehicle - one is writing it off and buying it back, the other is "cash in leiu of repair" - this is basically where they give you a wodge of cash and call it a day. The advantage of the latter is that it means the car does not receive a CAT marker.

Give them a call and see if they'll offer you the £5.5k as cash-in-lieu then get the car repaired at a proper place (or save yourself a couple grand and DIY it).

Give them a call and see if they'll offer you the £5.5k as cash-in-lieu then get the car repaired at a proper place (or save yourself a couple grand and DIY it).

5lab said:

there are 2 options for keeping the vehicle - one is writing it off and buying it back, the other is "cash in leiu of repair" - this is basically where they give you a wodge of cash and call it a day. The advantage of the latter is that it means the car does not receive a CAT marker.

Give them a call and see if they'll offer you the £5.5k as cash-in-lieu then get the car repaired at a proper place (or save yourself a couple grand and DIY it).

I said keep the salvage and repair, but iI did not know it was Hastings involved.Give them a call and see if they'll offer you the £5.5k as cash-in-lieu then get the car repaired at a proper place (or save yourself a couple grand and DIY it).

If I remember Hastings is one of the insurance companies that do not let the salvage to be retained by the policy holder.

OP is consulting his policy.

I am guessing as when my last car was written off they take a line 'cars for sale don't sell for that price' so they try and claim some discount on advertised price.

Therefore I was told that they take around 15% off, so 9-11k seems to be around where your at, so take 15% off 11k and get 9.35k.

I would say values don't seem to have dropped on these older SUVs yet, so if you can get 10k your doing well.

With the mileage they based on some youtubers can become money pits do you have some bills you can send in?

Therefore I was told that they take around 15% off, so 9-11k seems to be around where your at, so take 15% off 11k and get 9.35k.

I would say values don't seem to have dropped on these older SUVs yet, so if you can get 10k your doing well.

With the mileage they based on some youtubers can become money pits do you have some bills you can send in?

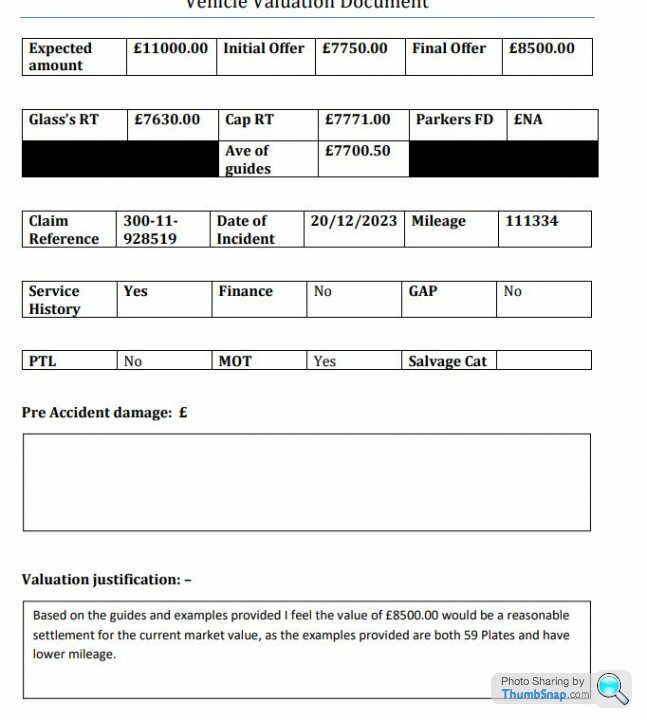

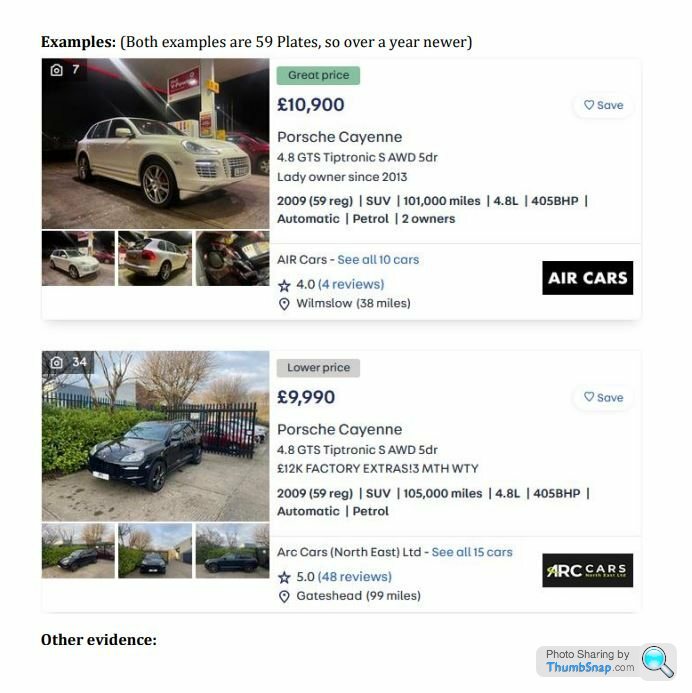

I just noticed an attachment on the email sent.

Please see below

The have based it on those being a 59 plate, regardless of their condition, the black one is a dog and autotrader even states is it £1.3k under the average value.

The white one has also been reduced in price since my screenshot, aren't they meant to take the value at time of accident, which was before christmas, so not fair to use a reduced price now?

So by his logic, "Both examples are over a year newer" - So in a years time you expect them to have depreciated another 20-30%? lol! Where is the logic

Sorry but there is no chance anyone would have my car on the market for £8.5k or even accept that little for it, no way!

I still have not replied but trying to compile something..

Before I saw the above, I had written this;

I hope this email finds you well. I appreciate your efforts in assessing the valuation for my 2008 Porsche Cayenne GTS following the recent accident. However, after careful consideration and market research, I believe that the offered value of £8,500 does not accurately reflect the true market value of my vehicle at time of accident.

I have attached evidence of recent online listings for similar models, which I do not appear in the same condition or as well optioned, which consistently show a market value well above the offered amount. My car has been meticulously maintained, has a full service history, and is in immaculate condition, factors that contribute significantly to its overall value. I cannot purchase a similar vehicle for the amount you are offering.

I kindly request a thorough review of the valuation, taking into account the provided evidence again. I believe a fair and equitable settlement should be in line with the current market value for my vehicle.

If necessary, I am prepared to escalate this matter to the Financial Ombudsman Service for a third-party review. I trust that we can reach a mutually agreeable resolution before considering such steps.

I look forward to your prompt attention to this matter and a revised valuation that accurately reflects the fair market value of my vehicle.

Thank you for your understanding and cooperation.

Sincerely,

Please see below

The have based it on those being a 59 plate, regardless of their condition, the black one is a dog and autotrader even states is it £1.3k under the average value.

The white one has also been reduced in price since my screenshot, aren't they meant to take the value at time of accident, which was before christmas, so not fair to use a reduced price now?

So by his logic, "Both examples are over a year newer" - So in a years time you expect them to have depreciated another 20-30%? lol! Where is the logic

Sorry but there is no chance anyone would have my car on the market for £8.5k or even accept that little for it, no way!

I still have not replied but trying to compile something..

Before I saw the above, I had written this;

I hope this email finds you well. I appreciate your efforts in assessing the valuation for my 2008 Porsche Cayenne GTS following the recent accident. However, after careful consideration and market research, I believe that the offered value of £8,500 does not accurately reflect the true market value of my vehicle at time of accident.

I have attached evidence of recent online listings for similar models, which I do not appear in the same condition or as well optioned, which consistently show a market value well above the offered amount. My car has been meticulously maintained, has a full service history, and is in immaculate condition, factors that contribute significantly to its overall value. I cannot purchase a similar vehicle for the amount you are offering.

I kindly request a thorough review of the valuation, taking into account the provided evidence again. I believe a fair and equitable settlement should be in line with the current market value for my vehicle.

If necessary, I am prepared to escalate this matter to the Financial Ombudsman Service for a third-party review. I trust that we can reach a mutually agreeable resolution before considering such steps.

I look forward to your prompt attention to this matter and a revised valuation that accurately reflects the fair market value of my vehicle.

Thank you for your understanding and cooperation.

Sincerely,

Edited by MarkGolf on Friday 19th January 11:34

Edited by MarkGolf on Friday 19th January 11:38

Gassing Station | Speed, Plod & the Law | Top of Page | What's New | My Stuff