Home Insurance contents question - Outbuilding defintion

Discussion

Not sure if this is the right section to ask but here goes.

Unfortunately we had a severe garage fire at our home last week which has caused extensive damage.

We have a separate policy for Buildings Cover and another one for Contents.

The company who are dealing with the buildings have been superb and had people on site within a day.

Sadly the company dealing with the contents claim have been next to useless.

Their loss adjuster only attended our home yesterday, almost a full week after the fired damage occurred.

He spent less than 15 minutes looking at the damage in the garage and took no pictures or notes as far as we could tell.

Then as he was getting ready to leave he said, “ oh by the way, your garage is classed as an outbuilding, and the maximum claim for an outbuilding is £5000, so don’t bother listing the items damaged by the fire, I can just write you a cheque right now for the £5K”

We responded with, what the heck? We don’t believe that.

We asked him to go away and confirm the policy details and the level of cover, which he did by telephoning back 6 hours later, to confirm what he has already said, they class a garage as an outbuilding and therefore the maximum claim will be £5K.

We responded with a rejection of the offer in writing and asked for the matter to be escalated, we have done this in writing and via the telephone it have had zero response.

So back to our original question regarding the legal definition of an outbuilding.

Our house is a large detached property, with two single garages integrated into the main part of the building.

The garage access is through the kitchen utility via a door from the utility to the garage.

We believe that this therefore does not class our garage as an outbuilding as it is an integral part of the house.

Does anyone have any experience of claims of this type and policy definitions at all?

Thanks in advance guys.

Unfortunately we had a severe garage fire at our home last week which has caused extensive damage.

We have a separate policy for Buildings Cover and another one for Contents.

The company who are dealing with the buildings have been superb and had people on site within a day.

Sadly the company dealing with the contents claim have been next to useless.

Their loss adjuster only attended our home yesterday, almost a full week after the fired damage occurred.

He spent less than 15 minutes looking at the damage in the garage and took no pictures or notes as far as we could tell.

Then as he was getting ready to leave he said, “ oh by the way, your garage is classed as an outbuilding, and the maximum claim for an outbuilding is £5000, so don’t bother listing the items damaged by the fire, I can just write you a cheque right now for the £5K”

We responded with, what the heck? We don’t believe that.

We asked him to go away and confirm the policy details and the level of cover, which he did by telephoning back 6 hours later, to confirm what he has already said, they class a garage as an outbuilding and therefore the maximum claim will be £5K.

We responded with a rejection of the offer in writing and asked for the matter to be escalated, we have done this in writing and via the telephone it have had zero response.

So back to our original question regarding the legal definition of an outbuilding.

Our house is a large detached property, with two single garages integrated into the main part of the building.

The garage access is through the kitchen utility via a door from the utility to the garage.

We believe that this therefore does not class our garage as an outbuilding as it is an integral part of the house.

Does anyone have any experience of claims of this type and policy definitions at all?

Thanks in advance guys.

Equus said:

I can't comment on the interpretation for insurance purposes, but both Planning and Building Regulations think in terms of a 'building' being a single unit, regardless of subdivision for different uses.

Therefore if a structure is physically attached to the main part of the dwellinghouse, it forms part of the same 'building' (and, indeed, a terrace of houses or block of flats can comprise multiple dwellings within a single building). An outbuilding, by definition, would normally be an entirely separate structure (even if physically separated only by a matter of millimetres).

Thanks bud, that was exactly what we thought.Therefore if a structure is physically attached to the main part of the dwellinghouse, it forms part of the same 'building' (and, indeed, a terrace of houses or block of flats can comprise multiple dwellings within a single building). An outbuilding, by definition, would normally be an entirely separate structure (even if physically separated only by a matter of millimetres).

We were thinking that the legal definition on an outbuilding is a building that is separate or detached from the main residence.

It looks like the issue is going to be around definitions and what the policy wording relates too.

Dog Star said:

Perhaps relevant to your claim, OP.

We had our detached, brick garage burgled in 2014. We had unlimited contents cover.

Insurance - who were about to pay out on the huge amount of stuff that was stolen - clocked this and my claim was knocked back to £2k, the max that could be paid for outbuilding contents.

I was told, at the time, that if my garage had been integral (as yours is) that the claim would have been settled in full. Integral = attached to main house. That was with LV=.

Hi Chap, thanks for much for this, it’s very interesting that some companies seem to class it as a different legal entity.We had our detached, brick garage burgled in 2014. We had unlimited contents cover.

Insurance - who were about to pay out on the huge amount of stuff that was stolen - clocked this and my claim was knocked back to £2k, the max that could be paid for outbuilding contents.

I was told, at the time, that if my garage had been integral (as yours is) that the claim would have been settled in full. Integral = attached to main house. That was with LV=.

And sorry to all yes I should have mentioned the two companies.

Our buildings cover is with Royal and Sun Alliance.

The contents cover is with Halifax.

fourstardan said:

Is there over 5k of contents gone? Feels to be quite generous for a garage tbh.

I would tend to agree that £5K is quite generous if it was just used to store just a few items such a car cleaning items etc.However as they are two large garages we have used them as additional storage areas for a manner of items.

These include my Roll Top Cabinet full of Snap on and Wera tools.

5 of my 1/8 RC race cars, two of which are Serpent 977 and Team X-Ray both with Nova Rossi race engines, which are about £1500 minimum each to replace.

Then there were other larger items such as my Hyundai Electric Start petrol generator, another item that cost over £1000.

Then there are three mountain bicycles, two Cannondales and one Specialized full suspension, and my Scott Foil Carbon road bike with Shimano DI2 Ultegra group set, which on its own will cost about £10000 to replace, the mountain bikes perhaps about £5000 to replace.

The other large item that that was not on a separate insurance policy was my Montesa Cota 4RT 2021 Trial motorcycle which was completely destroyed.

That too would cost around £7000 to replace.

Just doing a quick spreadsheet to add those items up they come to around £30000.

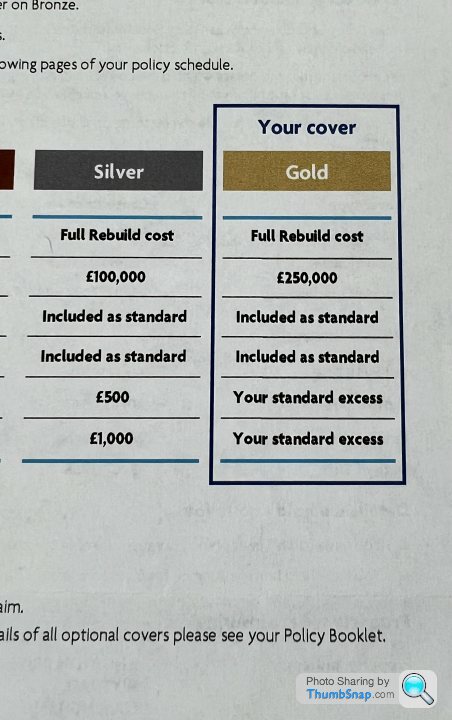

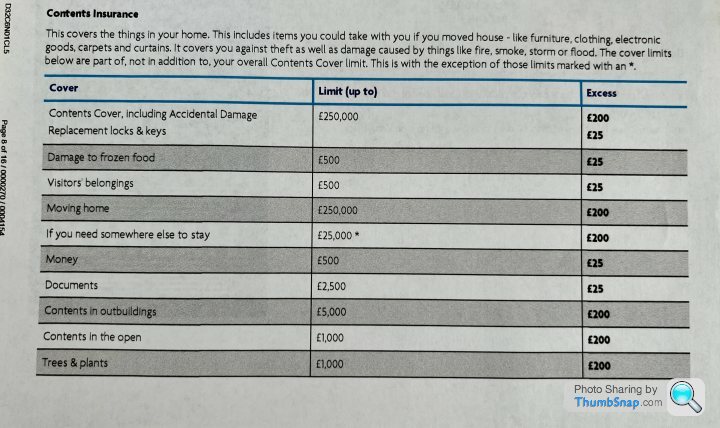

Some might say that’s a lot of moneys worth of items to have in a garage without a separate specific insurance policy to cover those specific items, but as we have Gold level cover that covers £250’000 worth of contents we felt that should be more than sufficient cover.

Here’s what’s left of my trials bike.

Condi said:

Ask them to define an outbuilding, you're not going to get a definite answer on here. It could easily be that an outbuilding is any room or building with its own entrance, in which case the garage would be an outbuilding, or that an outbuilding is any building separate to the house, in which case its probably not an outbuilding.

Fwiw a dictionary definition is "a smaller separate building such as a shed or barn that belongs to a main building, such as a house or farm." Suggesting you could argue the garage is not an outbuilding.

Thanks bud, yes we have requested that as part of our formal complaint, still not had a reply on that one though. Fwiw a dictionary definition is "a smaller separate building such as a shed or barn that belongs to a main building, such as a house or farm." Suggesting you could argue the garage is not an outbuilding.

Deesee said:

Note the bold, as its a policy definition, as below..

However..

You would have needed the bike & model cars with seperate individual listings/specified items, this is normally 2/3k (I cant find it on the PDF posted above), or separate cover.

Other items they should pay if they are outside of the what we don't cover section.

Also you might want to check if 250k contents cover is actually enough, its probably not, and if 'underinsured' they could ratchet down a claim.

Nb, edit, they also have a separate pedal bike section/cover. check your policy schedule for pedal cover.

Good luck.

Edited by Deesee on Thursday 31st August 09:18

We have done exactly the same, but can’t help feeling that those to paragraphs effectively contradict themselves?

We know now about having to list items of value above £2000 as separate items to be covered, have to be honest never spotted that before and as a result we never added any items.

And of course the range of high value items I own that are in the garage would have probably have doubled or perhaps tripled the annual premium, but with hindsight it would of course been prudent to do so.

Deesee said:

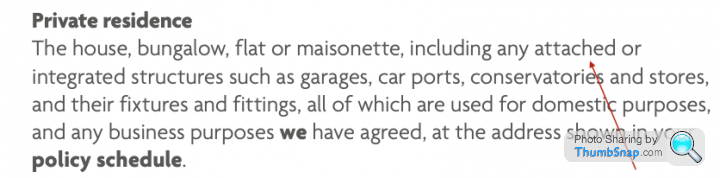

No problem, their definition takes you from outbuilding to private residence (second picture fits your description of the property), your tools will be covered, the motorised stuff won't, and you would have needed additional pedal bike cover (and this id say would have been needed to be specified as the values) this will be your schedule if you have opted for it.

Either way the tools and other goods (not including the excluded in picture 3, motor bike/pedal bikes etc) will be in excess of 5k, and they have incorrectly assessed your claim on their own definitions.

Yes the fact that they have incorrectly assessed the claim, or more importantly the loss adjuster who came to asses the damage did not adequately assess the extent of the damage.Either way the tools and other goods (not including the excluded in picture 3, motor bike/pedal bikes etc) will be in excess of 5k, and they have incorrectly assessed your claim on their own definitions.

Remember Halifax insure the contents, so items inside the house/dwelling as a whole.

The loss adjuster did not even look in the loft space, which is above the one garage, but this also extends to another loft above the utility, and the loft was also used to store a range of items some of them quite valuable.

The whole of the loft and utility area was hosed down by the fire brigade as they used heat sensing equipment to detect areas that still showed signs of heat.

In the Utility itself are electrical items such as Washing Machine, Tumble dryer and Microwave, all of which were contaminated with smoke damage and then water damage from the fire hoses.

The loss adjuster did not even look at or ask about those items, or look at any other parts of the house which has smoke damage.

We understand that most of the smoke damage will be covered by the buidings insurance, and indeed the other loss adjuster that came on behalf of RSA was very thorough, and went through the house room by toom, taking notes and pictures of every area that had visible smoke damage, and even areas that were not so visibly damaged.

As mentioned earlier it was apparent that the contents loss adjuster had predetermined that it was only the two garages that were affected, and had also pre decided that the only cover they were going to offer was the £5K just for the outbuildings.

This will be the main area we will contest to ensure that we are able to claim for exactly what was damaged in the fire as part of the contents cover for the shoot of the house.

Deesee said:

I with you 100% on this, they have used an incorrect way of assigning and assessing your claim.. thats totally not fair, has put you in a worse position as well as creating additional stress, its certainly not treating customers fairly.

You'll need to itemise these goods/valuables, pictures, and perhaps receipts/bank transactions/ebay statements etc.

Thankfully it sound like everyone is safe, and well, stuff can be replaced.

Is it worth appointing a loss assessor? Even retrospectively to deal with the 'grey areas' that may appear between the buildings and contents, and help with the complaint with the contents?

Yes the main point is as you say that the everyone is safe, it might have been a very much worse outcome if my daughter had not been still awake at 2AM in the morning and heard what she thought was somone trying to break into the garage, which we now know was actually all the aerosols I had in the garage for bike maintenance etc going pop.You'll need to itemise these goods/valuables, pictures, and perhaps receipts/bank transactions/ebay statements etc.

Thankfully it sound like everyone is safe, and well, stuff can be replaced.

Is it worth appointing a loss assessor? Even retrospectively to deal with the 'grey areas' that may appear between the buildings and contents, and help with the complaint with the contents?

We actually had a Loss Assessor attend just a few days ago, it was his advice that we reject the offer and contest what the loss adjuster was saying regarding the garage being classed as an outbuilding.

He also told us it was not worth his company taking on the case, as the total claim was likely to be less than £100K which seems to be the minimum amount they use as a starting point to justify them taking on such a claim.

I think he mentioned that they charge 30% of any claim as their fee, so it would need to be £100m claim to get a £30K fee.

alscar said:

Apologies if I have missed it but are u saying there is maximum any one item limit that has been exceeded on at least the trail bike ?

If so that will limit their payout.

As alluded to by others if your garage only was £30k are you happy that the rest of the actual house possessions is £ 220k or less ?

If so then no issue but if not then the LA may suggest you are under insured and apply average to whatever the loss quantum for the garage is.

Hopefully you will still end up with more than the £5k the LA suggested though.

Best of luck.

That’s a good point, but I don’t think that the total of our normal contents/possessions would ever be more than £250’000.If so that will limit their payout.

As alluded to by others if your garage only was £30k are you happy that the rest of the actual house possessions is £ 220k or less ?

If so then no issue but if not then the LA may suggest you are under insured and apply average to whatever the loss quantum for the garage is.

Hopefully you will still end up with more than the £5k the LA suggested though.

Best of luck.

The higher value items we own, such as my watch collection, and my wife’s jewellery all have separate insurance policy’s for them, as indeed does my professional camera equipment.

Our other high value items such as Apple IMacs, Apple MacBook Pros and IPads are also covered on a separate tech policy too.

The main item damaged in the garage that is a higher value is my Montesa Trials bike, Which as a pure off road bike that is not road registered cannot be covered by a traditional motor vehicle policy.

There are some specialist companies who will provide theft cover for them only, as they do not have an ignition key or any form of locks, but it does seem focused on not getting them stolen from the back of your car or trailer as an example.

Deesee said:

The issue there is you have an upper limit on the common insurance policy, and are the high value items are included/excluded on a separate policy.

Your iPads/Macs etc will be covered you don’t need a separate policy for these, unless they are over the floor limit?

You can’t double insure items, Halifax will argue that, if you think it’s 250k + the nice stuff…

I don’t want to cause problems/issues as happy to help but I think you’ve pressed the easy buttons on the meerkat..(or other)..

Tbh I’m still struggling at 250k contents..

Thanks for the feedback.Your iPads/Macs etc will be covered you don’t need a separate policy for these, unless they are over the floor limit?

You can’t double insure items, Halifax will argue that, if you think it’s 250k + the nice stuff…

I don’t want to cause problems/issues as happy to help but I think you’ve pressed the easy buttons on the meerkat..(or other)..

Tbh I’m still struggling at 250k contents..

What is it that you are struggling with re the £250k contents? That it’s too low?

I can’t recall what we used as a decision making criteria on the insurance company to choose, but it certainly wasn’t using any compare the market type companies.

We have had this policy with the Halifax from the first time we took out the mortgage on this home which was almost 20 years ago now.

We have never looked to change the insurance provider and just renewed it each year, admittedly not really studying what was covered and not covered that closely.

The combined insurance premium is about £1000 per year for both the contents and the buildings cover, and both of them seem to provide a good level of cover which in my eyes more than covers any costs of replacement or repairs should the worse happen.

Are you suggesting that we need to review both the providers and the total insured limits/maximum amount?

alscar said:

With the separate policies as you say hopefully the potential for under insurance is minimised.

We have a quad bike which is included under our Homeowners policy but only for fire and theft.

Again not Road registered.

We did have to specifically mention and get endorsed onto the policy.

Yep with hindsight I should have declared the Montesa Trials bike to make sure it was on the policy as an item of over £2000 in value, one of those things I forgot to do and i am now going to have to pay the cost.We have a quad bike which is included under our Homeowners policy but only for fire and theft.

Again not Road registered.

We did have to specifically mention and get endorsed onto the policy.

An update on the situation with the contents claim.

We have no had an email stating that as we have rejected the original offer of £5K, they have raised our complaint to the claims handling investigation department.

The real problem here is that they have stated that it is now going to take 8 weeks to investigate the disputed claim.

Jesus, 8 bloody weeks! We will be Lucy to see a resolution of this matter before November.

Are all insurance companies this bad?

We have no had an email stating that as we have rejected the original offer of £5K, they have raised our complaint to the claims handling investigation department.

The real problem here is that they have stated that it is now going to take 8 weeks to investigate the disputed claim.

Jesus, 8 bloody weeks! We will be Lucy to see a resolution of this matter before November.

Are all insurance companies this bad?

A bit of an update on our situation.

We are still at a stalemate with the contents insurance claim.

We have been chasing them almost daily, but get the same answer, which is it can take up to 8 weeks to resolve a claim dispute when an offer has been made.

This brought up another talking point, at no time have we had any formal offer or written communication which could be classed as an offer or payment, settlement or otherwise from the contents insurance company ( Halifax ).

We also have not received any official report relating to the contents insurance loss adjusters visit and his findings.

By contrast the buildings insurance (RSA - Nationwide) have been exemplary.

They produced a full report, documented actions, assigned multiple companies to do the work, the electricians , the garage door repair company, and the cleaning company to remove the smoke damage and soot from the whole house.

For each of these services they have asked for a quote, got one, made an offer and issued the payment.

We shall of course be reviewing the providers at renewal time, and bringing the contents and buildings cover all under one main provider.

We are still at a stalemate with the contents insurance claim.

We have been chasing them almost daily, but get the same answer, which is it can take up to 8 weeks to resolve a claim dispute when an offer has been made.

This brought up another talking point, at no time have we had any formal offer or written communication which could be classed as an offer or payment, settlement or otherwise from the contents insurance company ( Halifax ).

We also have not received any official report relating to the contents insurance loss adjusters visit and his findings.

By contrast the buildings insurance (RSA - Nationwide) have been exemplary.

They produced a full report, documented actions, assigned multiple companies to do the work, the electricians , the garage door repair company, and the cleaning company to remove the smoke damage and soot from the whole house.

For each of these services they have asked for a quote, got one, made an offer and issued the payment.

We shall of course be reviewing the providers at renewal time, and bringing the contents and buildings cover all under one main provider.

Another update, and predictably they have said they don’t see our compliant as justified.

They are still standing by the fact that the policy states that it only covers items in an outbuilding up to £5000.

However they ignored our request for clarification of their policy defintion for an outbuilding and how they decided that a garage is also an outbuilding.

We also asked for clarification regarding the fact our garage is integral to the main building of the house, and that as it is accessed only from the house that we believe it is a part of the house, and therefore not an outbuilding, again that clarification was ignored.

We did notice that in all the policy documents it only refers to £5000 being the maximum for an outbuilding, but in their response to our complaint letter the wording “ Garages and Outbuildings “ is used in reply to the complaint and not just the word “ outbuildings “.

So they have changed the wording and definitions to suit themselves and limit their liability and therefore the maximum settlement figure.

The only options we now have are to either accept the £5000 figure or take it to the insurance ombudsman with an official complaint.

Also as an update we have now completed to the best of our ability the spreadsheet list of the items destroyed in the fire, which totals almost £37’600, not including my Montesa Trials bike.

So a £32’000 kick in the balls basically.

I’m out of options now, short of taking out a hitman contract on the claims assessor so that I get some satisfaction out of this whole car crash situation !

They are still standing by the fact that the policy states that it only covers items in an outbuilding up to £5000.

However they ignored our request for clarification of their policy defintion for an outbuilding and how they decided that a garage is also an outbuilding.

We also asked for clarification regarding the fact our garage is integral to the main building of the house, and that as it is accessed only from the house that we believe it is a part of the house, and therefore not an outbuilding, again that clarification was ignored.

We did notice that in all the policy documents it only refers to £5000 being the maximum for an outbuilding, but in their response to our complaint letter the wording “ Garages and Outbuildings “ is used in reply to the complaint and not just the word “ outbuildings “.

So they have changed the wording and definitions to suit themselves and limit their liability and therefore the maximum settlement figure.

The only options we now have are to either accept the £5000 figure or take it to the insurance ombudsman with an official complaint.

Also as an update we have now completed to the best of our ability the spreadsheet list of the items destroyed in the fire, which totals almost £37’600, not including my Montesa Trials bike.

So a £32’000 kick in the balls basically.

I’m out of options now, short of taking out a hitman contract on the claims assessor so that I get some satisfaction out of this whole car crash situation !

KTMsm said:

I would either send an very specific letter with numbered points

1) What is your definition of an outbuilding

Etc

Or just go straight to the ombudsman

That is exactly what we did, and as I said they have chosen to ignore those specific requests for clarification of the definition on an outbuilding.1) What is your definition of an outbuilding

Etc

Or just go straight to the ombudsman

They have just repeated that the claim can only be for a maximum of £5000 as it is an outbuilding.

So an update on this, can’t believe we are in the middle of November and no resolution relating to the contents.

We sent a second recorded letter to the contents insurance company, but just got the exact same boilerplate letter back from them with a sorry, it’s £5K take it or leave it.

We told them formally that we would raise a complaint with the Ombudsman, just an automated email reply to that, with a “ we acknowledge your complaint “

We have had no other communication with the contents insurance company since.

We did start the formal process of filing a complaint with the ombudsman, at first it said you must file a complaint online only.

We had no response to that, except for an initial email response stating that if we did not have a response from them in six weeks we should consider the matter closed as they have decided it’s not a valid complaint.

We decided to write a formal letter with the reasons for the full complaint and that we wanted the matter to be fully investigated.

That was 8 weeks ago.

Last Friday we received an email, which looked suspiciously like an automated fob off email, with a single question, “ do you want us to still investigate your claim? Yes or no was the only option, so off course said yes.

I’m sure it will now be another 8 weeks before we hear anything from them.

We sent a second recorded letter to the contents insurance company, but just got the exact same boilerplate letter back from them with a sorry, it’s £5K take it or leave it.

We told them formally that we would raise a complaint with the Ombudsman, just an automated email reply to that, with a “ we acknowledge your complaint “

We have had no other communication with the contents insurance company since.

We did start the formal process of filing a complaint with the ombudsman, at first it said you must file a complaint online only.

We had no response to that, except for an initial email response stating that if we did not have a response from them in six weeks we should consider the matter closed as they have decided it’s not a valid complaint.

We decided to write a formal letter with the reasons for the full complaint and that we wanted the matter to be fully investigated.

That was 8 weeks ago.

Last Friday we received an email, which looked suspiciously like an automated fob off email, with a single question, “ do you want us to still investigate your claim? Yes or no was the only option, so off course said yes.

I’m sure it will now be another 8 weeks before we hear anything from them.

grumbas said:

I've only skim read the thread. But as has been alluded to several times, the schedule and policy wording Halifax issued to you at point of purchase are what matters here. I can see other posters have found generic Halifax documents that seem to support your position, but it's critical you read yours in detail.

At this point I would absolutely take this to the Ombudsman. They are incredibly fair and their findings are binding on the insurer.

But you need to explain what you expect the outcome to be and why you believe it is covered under the policy documents you've got, as that is how the Ombudsman will assess the complaint. Or, if you think the insurer is relying on a point buried in the small print, you can try to argue that it's an unfair exclusion (eg if they define integral garages as outbuildings). The better you present your argument, the easier it is for the Ombudsman to assess your claim.

You can also complain about the time taken and poor communication, it's not unusual for the Ombudsman to award compensation payments. Absolutely explain how the buildings insurer has responded to the incident by way of comparison.

Don't bother with a solicitor, or trying to make a claim against the insurer through the legal system. You can get the outcome you need for free through the Ombudsman.

Edited to add, when they responded to your complaint, did they say it was their 'final response'? If so that's your green light for the Ombudsman to automatically accept the case. If they didn't ask them to issue a final response, otherwise the Ombudsman will offer them the chance to review the complaint again without getting involved.

Thanks for taking the time to read and comment bud.At this point I would absolutely take this to the Ombudsman. They are incredibly fair and their findings are binding on the insurer.

But you need to explain what you expect the outcome to be and why you believe it is covered under the policy documents you've got, as that is how the Ombudsman will assess the complaint. Or, if you think the insurer is relying on a point buried in the small print, you can try to argue that it's an unfair exclusion (eg if they define integral garages as outbuildings). The better you present your argument, the easier it is for the Ombudsman to assess your claim.

You can also complain about the time taken and poor communication, it's not unusual for the Ombudsman to award compensation payments. Absolutely explain how the buildings insurer has responded to the incident by way of comparison.

Don't bother with a solicitor, or trying to make a claim against the insurer through the legal system. You can get the outcome you need for free through the Ombudsman.

Edited to add, when they responded to your complaint, did they say it was their 'final response'? If so that's your green light for the Ombudsman to automatically accept the case. If they didn't ask them to issue a final response, otherwise the Ombudsman will offer them the chance to review the complaint again without getting involved.

Edited by grumbas on Monday 13th November 12:27

All of your points are great and well founded, most of them we have already documented, delivered via email and asked for actions and outcomes upon.

We are waiting now to see what the next action is from the ombudsman to see what they advise re a more acceptable Claim that actually covers what we lost in the fire.

K87 said:

I am not sure if you have said whether the insurers are correct or not, is there a mention of a £5000 sublimit for the contents of garages. I know that I found a policy wording on the Internet that made their position untenable but that is not to say that your particular wording was the same. If they are correct and it says, for example, that 'cover on the contents of garages is limited to £5000' and the definition of garages in the wording doesn't differentiate between integral or an outbuilding, if they are correct in their £5000 position then any complaint to an Ombudsman would be down to insurers Conduct and suchlike.

I need to re read the actual terms in our own policy document as you mention, but I am fairly sure that there is not a definition of a garage per sey, just the definition of an outbuilding and that is what the contents insurer is referring to as that is stated as having a maximum claim of £5000 for contents in an outbuilding.We have made multiple requests to Halifax Insurance for a definition of A - A Garage, B - An Outbuilding, C - An Integral Garage.

Each time we have had this request ignored by Halifax Insurance.

Can’t remember if I posted it, but we have been contacted now by the Ombudsman who have agreed to look at our case.

Gassing Station | Homes, Gardens and DIY | Top of Page | What's New | My Stuff