Negotiating with a Ferrari Main dealer

Discussion

So, I am focussing on a 2015 Cali T from Meridien Modena and will probably drive 250 miles to go and see it next week. Its a Grigio Titania with Nero leather and duo tone paint, so Nero roof.

Dealer has come up with a deal that is not far from where i want to be, its a 30 month contract so the two year warranty and service pack cover (2 services left) works out near perfectly.

My question is, how hard can i push the dealer on the finance. I have spoken to a few main dealers, and they all seem to say ' we will speak to ferrari finance to get a better rate/higher residual balloon" etc, is this BS or do they actually have to refer to Ferrari FS for this to 'tweak' the deal?

I have seen finance rates ranging from 6.6% APR to 8.8% APR, even 6.6% seems a bit high, but how low will they go - has anyone any experience of this?

The residual balloon seems high, but do they genuinely pitch these to ensure that they keep the customer at the end with some equity for the next one?

Is there anything else that can be bartered into the deal? Official merchandise, driving experiences?

Any help appreciated - this would be my first Ferrari.

Dealer has come up with a deal that is not far from where i want to be, its a 30 month contract so the two year warranty and service pack cover (2 services left) works out near perfectly.

My question is, how hard can i push the dealer on the finance. I have spoken to a few main dealers, and they all seem to say ' we will speak to ferrari finance to get a better rate/higher residual balloon" etc, is this BS or do they actually have to refer to Ferrari FS for this to 'tweak' the deal?

I have seen finance rates ranging from 6.6% APR to 8.8% APR, even 6.6% seems a bit high, but how low will they go - has anyone any experience of this?

The residual balloon seems high, but do they genuinely pitch these to ensure that they keep the customer at the end with some equity for the next one?

Is there anything else that can be bartered into the deal? Official merchandise, driving experiences?

Any help appreciated - this would be my first Ferrari.

Regy53 said:

Stickyone said:

So, I am focussing on a 2015 Cali T from Meridien Modena and will probably drive 250 miles to go and see it next week. Its a Grigio Titania with Nero leather and duo tone paint, so Nero roof.

Dealer has come up with a deal that is not far from where i want to be, its a 30 month contract so the two year warranty and service pack cover (2 services left) works out near perfectly.

My question is, how hard can i push the dealer on the finance. I have spoken to a few main dealers, and they all seem to say ' we will speak to ferrari finance to get a better rate/higher residual balloon" etc, is this BS or do they actually have to refer to Ferrari FS for this to 'tweak' the deal?

I have seen finance rates ranging from 6.6% APR to 8.8% APR, even 6.6% seems a bit high, but how low will they go - has anyone any experience of this?

The residual balloon seems high, but do they genuinely pitch these to ensure that they keep the customer at the end with some equity for the next one?

Is there anything else that can be bartered into the deal? Official merchandise, driving experiences?

Any help appreciated - this would be my first Ferrari.

Cant help you as going through the same experience at the moment, 6,8% is the number they are stuck at.... I was at the dealership today could of looked for you Dealer has come up with a deal that is not far from where i want to be, its a 30 month contract so the two year warranty and service pack cover (2 services left) works out near perfectly.

My question is, how hard can i push the dealer on the finance. I have spoken to a few main dealers, and they all seem to say ' we will speak to ferrari finance to get a better rate/higher residual balloon" etc, is this BS or do they actually have to refer to Ferrari FS for this to 'tweak' the deal?

I have seen finance rates ranging from 6.6% APR to 8.8% APR, even 6.6% seems a bit high, but how low will they go - has anyone any experience of this?

The residual balloon seems high, but do they genuinely pitch these to ensure that they keep the customer at the end with some equity for the next one?

Is there anything else that can be bartered into the deal? Official merchandise, driving experiences?

Any help appreciated - this would be my first Ferrari.

I saw your car as i was looking at that specific colour in a 458 elsewhereOh, and the lowest i got from Meridien was 6.8%

chrisbell08 said:

So I got a test drive, fell in love with it!

The guys at brum are great and I put a deposit down on this

https://birmingham.ferraridealers.com/en_gb/search...

Fantastic news, good for you, it looks awesome!The guys at brum are great and I put a deposit down on this

https://birmingham.ferraridealers.com/en_gb/search...

Spill the beans, what did you get the car for, and did you go with Ferrari finance?

chrisbell08 said:

Ahh so here's the one sticking point, it was 6:20pm and my son (he's 5) was getting fed up and hungry. I wasn't happy with the deal they gave but it was close so I agreed to put a deposit down pending the finance getting agreed.

I wanted to have the chance to shop around to ensure I'm getting the best deal on the finance (not just the numbers but also lowest risk) and didn't think just saying yes on the day was the smartest thing todo.

The best they would do is:

Sale Price: £115,000

Deposit: £20,000

Baloon: £66,000

Monthly: £1149

APR: 8.2% (Started at 9.7)!

Term: 48 months Lease Purchase

They've said there's some movement on the sale price and apr but they need to contact Ferrari about the apr. I said I wouldn't go higher than 6.9 as that seems the industry standard.

My budget is £1000/month £20k deposit so I will see over the next few days how they get to that (Without kicking the balloon up we agreed that was the max).

I told the guys that I would be planning to keep the car 2-3 years but they said the 4 year deals are pretty standard and there shouldn't be any concern about negative equity after 2 years, does that sound right or just salesmen BS?

The other car I was considering was an Aston Martin DB11 and they gave me this deal (which seemed a great deal tbf)

Sale Price: £93,000

Deposit: £13,000

Baloon: £69,000

Monthly: £1000

APR: 6.9%

Term: 24 months PCP

Here's my thoughts, as I am deep in the throes of negotiating with a Ferrari dealerI wanted to have the chance to shop around to ensure I'm getting the best deal on the finance (not just the numbers but also lowest risk) and didn't think just saying yes on the day was the smartest thing todo.

The best they would do is:

Sale Price: £115,000

Deposit: £20,000

Baloon: £66,000

Monthly: £1149

APR: 8.2% (Started at 9.7)!

Term: 48 months Lease Purchase

They've said there's some movement on the sale price and apr but they need to contact Ferrari about the apr. I said I wouldn't go higher than 6.9 as that seems the industry standard.

My budget is £1000/month £20k deposit so I will see over the next few days how they get to that (Without kicking the balloon up we agreed that was the max).

I told the guys that I would be planning to keep the car 2-3 years but they said the 4 year deals are pretty standard and there shouldn't be any concern about negative equity after 2 years, does that sound right or just salesmen BS?

The other car I was considering was an Aston Martin DB11 and they gave me this deal (which seemed a great deal tbf)

Sale Price: £93,000

Deposit: £13,000

Baloon: £69,000

Monthly: £1000

APR: 6.9%

Term: 24 months PCP

Their car is VERY expensive for a 16 plate Cali T (it might be because its Rosso/Crema), The two I am looking at - one Main Dealer 16 plate 9500 miles with Special Handling pack and lots of options (£107000). The second independent trader; 16 plate 5700 miles (20 months Ferrari warranty) - £99,995.

I assume you have no part ex. So I would want at least £5000 off the price of the car (and probably more - show them evidence from the others cars on sale) and ask for a rate of 6.8% which I have had from every Ferrari dealer I have dealt with. This will bring the monthly payment to under £1000.

The basic CAP value of a 16 plate Cali T as a Trade in with 8000 miles is £88,000. This is without options, so this would increase (maybe even to £95K for a car with lots of options, decent colours). That's a HUGE dealer margin on your car.

If it were me, I would be wary of the high Balloon, and you can ask for a lower one - which will increase the monthly payment, but it will give you more protection, if you want some equity at the end. I have a PCP quote on both of the above cars (via Oracle) and the 4 year GFV is around £43000 for a 16 plate Cali T with mid 20k's mileage)

Visit to the Ferrari Main dealer confirmed for Thursday.

I have their initial finance quote, I know what I want it to change to , IF they want me to fund via Ferrari FS. They will be making c2% of the amount borrowed as a commission from FFS so I expect there to be movement. If not, I have a back up plan with two quotes from brokers, who I am more than happy to deal with.

I have a quote with 6.8% APR finance and a stupidly high balloon of 74% of the selling price (30 month contract). What I want is to lower the balloon by £12k to give me a fighting chance of getting my full deposit back in equity and for the finance rate to drop to 5.9%. It will be an additional £200/month on the finance, but decent peace of mind.

I want them to be calling me in two years to persuade me to sell the Cali T to get into a 458/488 for not a lot more money

I have their initial finance quote, I know what I want it to change to , IF they want me to fund via Ferrari FS. They will be making c2% of the amount borrowed as a commission from FFS so I expect there to be movement. If not, I have a back up plan with two quotes from brokers, who I am more than happy to deal with.

I have a quote with 6.8% APR finance and a stupidly high balloon of 74% of the selling price (30 month contract). What I want is to lower the balloon by £12k to give me a fighting chance of getting my full deposit back in equity and for the finance rate to drop to 5.9%. It will be an additional £200/month on the finance, but decent peace of mind.

I want them to be calling me in two years to persuade me to sell the Cali T to get into a 458/488 for not a lot more money

chrisbell08 said:

Stickyone said:

Visit to the Ferrari Main dealer confirmed for Thursday.

I have their initial finance quote, I know what I want it to change to , IF they want me to fund via Ferrari FS. They will be making c2% of the amount borrowed as a commission from FFS so I expect there to be movement. If not, I have a back up plan with two quotes from brokers, who I am more than happy to deal with.

I have a quote with 6.8% APR finance and a stupidly high balloon of 74% of the selling price (30 month contract). What I want is to lower the balloon by £12k to give me a fighting chance of getting my full deposit back in equity and for the finance rate to drop to 5.9%. It will be an additional £200/month on the finance, but decent peace of mind.

I want them to be calling me in two years to persuade me to sell the Cali T to get into a 458/488 for not a lot more money

Which dealer?I have their initial finance quote, I know what I want it to change to , IF they want me to fund via Ferrari FS. They will be making c2% of the amount borrowed as a commission from FFS so I expect there to be movement. If not, I have a back up plan with two quotes from brokers, who I am more than happy to deal with.

I have a quote with 6.8% APR finance and a stupidly high balloon of 74% of the selling price (30 month contract). What I want is to lower the balloon by £12k to give me a fighting chance of getting my full deposit back in equity and for the finance rate to drop to 5.9%. It will be an additional £200/month on the finance, but decent peace of mind.

I want them to be calling me in two years to persuade me to sell the Cali T to get into a 458/488 for not a lot more money

Off to the Ferrari dealer today to view and drive the Cali T. Deal is sorted and agreed, just waiting to hear that finance is approved and I will be good to go.

To say, I am excited is an understatement, going to a Ferrari main dealer, is like going to the ultimate toy shop. I want to find the time to be able to look at the other cars in the showroom, I know I will be mentally planning the future upgrade to a Portofino/488/458

I went for a 3 year LP deal with Ferrari FS, with the 'standard' (not inflated) balloon payment at the end, which is around £12k less than the inflated balloon I was initially offered to keep the payments down. It means paying more per month, but I have no doubt it's the right thing to do if I want to maintain Ferrari ownership into the future. Ideally, I would like to be in a position to upgrade before the service pack and two year warranty expire, hopefully with a chunk of equity for the next one.

I'll post some pictures later if people are interested.

To say, I am excited is an understatement, going to a Ferrari main dealer, is like going to the ultimate toy shop. I want to find the time to be able to look at the other cars in the showroom, I know I will be mentally planning the future upgrade to a Portofino/488/458

I went for a 3 year LP deal with Ferrari FS, with the 'standard' (not inflated) balloon payment at the end, which is around £12k less than the inflated balloon I was initially offered to keep the payments down. It means paying more per month, but I have no doubt it's the right thing to do if I want to maintain Ferrari ownership into the future. Ideally, I would like to be in a position to upgrade before the service pack and two year warranty expire, hopefully with a chunk of equity for the next one.

I'll post some pictures later if people are interested.

Why on finance? (I think this is a recurring PH question!)

I believe that the vast majority of people buy cars on finance, presumably because they don't have the cash (likely) or if they did, why would they drop £100k cash on a car unless they are super (cash) rich. If they don't have the cash, most can afford a deposit and a monthly amount.

I don't have £100k in ready cash, but I still want, and can afford a Ferrari, the variety of financial products out there make the car available to me. To be honest, even if I did have £100k in bank (from a pension lump sum say) I still wouldn't drop it all on a car.

I believe that the vast majority of people buy cars on finance, presumably because they don't have the cash (likely) or if they did, why would they drop £100k cash on a car unless they are super (cash) rich. If they don't have the cash, most can afford a deposit and a monthly amount.

I don't have £100k in ready cash, but I still want, and can afford a Ferrari, the variety of financial products out there make the car available to me. To be honest, even if I did have £100k in bank (from a pension lump sum say) I still wouldn't drop it all on a car.

Ferruccio said:

Depreciation + finance + insurance + maintenance, makes supercars an expensive passion usually.

If you can knock one of these out, it makes it a bit less costly.

Very True....If you can knock one of these out, it makes it a bit less costly.

Depreciation - almost inevitable, try and buy sensibly and when the depreciation is fattening out

Finance - again - shop around, try and keep finance rate down (hence amount of interest you pay)

Maintenance - buy one with a service pack and new tyres!

Insurance - its costing me £10/month more than my previous 718 S.

Ferruccio said:

anonymous said:

[redacted]

In my view, yes. Financing a depreciating asset is something that I have never understood.

The argument made by those who do have the cash, is that they can “do so much more with the cash”. Maybe.

PS. I don't want this thread to descend into a discussion about finance - thanks

chrisbell08 said:

Can somebody explain why the numbers quoted by Ferrari don't actually add up on the calculators,

So I did what we all do and got carried away and moved my deposit over from a Cali T to a Portofino. I felt I was viewing the Cali T as a stepping stone to a Portofino so in the long term, I'd be better just paying a bigger deposit now and keeping the car longer instead of keeping the Cali for 24 months then having to cough up another deposit for a Portofino.

So here's the initial quote they gave me for the Portofino:

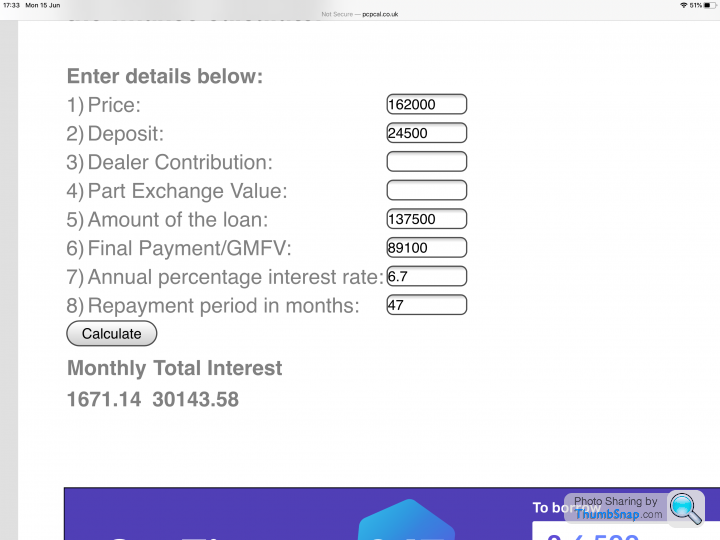

Price: £162,000

Deposit: £24,500

Balloon: £89,100 (55%)

APR 8.2% (Funny I said the APR needs to be in the 6's and he said ( I think I can do that lol)

Monthly £1662

If you put these numbers into a PCP calculator it comes out as 1,794.98, what am I missing? As the other guy mentions above the numbers they gave me the first time didn't add up either

Turns out the car they were selling me didn't have apple car play (I stupidly assumed this was standard before watching a YT video on them) so this deal is now dead in the water so need to keep on the lookout for another one.

Id love a Portofino next, my Cali T is delivered on Saturday. I also love a bit of ‘mission creep’ ha ha! So I did what we all do and got carried away and moved my deposit over from a Cali T to a Portofino. I felt I was viewing the Cali T as a stepping stone to a Portofino so in the long term, I'd be better just paying a bigger deposit now and keeping the car longer instead of keeping the Cali for 24 months then having to cough up another deposit for a Portofino.

So here's the initial quote they gave me for the Portofino:

Price: £162,000

Deposit: £24,500

Balloon: £89,100 (55%)

APR 8.2% (Funny I said the APR needs to be in the 6's and he said ( I think I can do that lol)

Monthly £1662

If you put these numbers into a PCP calculator it comes out as 1,794.98, what am I missing? As the other guy mentions above the numbers they gave me the first time didn't add up either

Turns out the car they were selling me didn't have apple car play (I stupidly assumed this was standard before watching a YT video on them) so this deal is now dead in the water so need to keep on the lookout for another one.

If it’s the Rosso car in Birmingham, it’s a stunner. Are you saying that it’s off, as it doesn’t have Car Play?

I was in Leeds on Saturday, they have a brand now Rosso/Crema Portfino in the showroom, it’s a cancelled order, £200k list and it’s for sale at £185k, might be worth a call.

Re finance, I get too roughly £1662 using 6.8% APR and assumes a 4 year term.

chrisbell08 said:

How much wiggle room do you think they will have on the price when its new? My biz partner brought a Lamborgini Evo yesterday and he got £35k off list

The conversation I had with the salesman was that they don’t discount brand new at all.I personally think it would be a brave move to buy new when the initial deprecation is quite steep. There is a 2019 Rosso Portofino on the Ferrari website for £159k which has Apple Car Play And 3000 miles.

chrisbell08 said:

Stickyone said:

The conversation I had with the salesman was that they don’t discount brand new at all.

I personally think it would be a brave move to buy new when the initial deprecation is quite steep. There is a 2019 Rosso Portofino on the Ferrari website for £159k which has Apple Car Play And 3000 miles.

I think it depends on how long you want to keep the car, if you have gap insurance and are going to keep the car for 3 years then you'll be fine. If your keeping a car 12-18 months new isn't a good idea lolI personally think it would be a brave move to buy new when the initial deprecation is quite steep. There is a 2019 Rosso Portofino on the Ferrari website for £159k which has Apple Car Play And 3000 miles.

Gassing Station | Ferrari V8 | Top of Page | What's New | My Stuff