AML - Stock Market Listing

Discussion

We have discussed some aspects of this subject already, but an event has now occurred, which illustrates the concerns which I have previously referred to.

Motor manufacturing is a cyclical business. That was dramatically illustrated in 2008, when Aston Martin annual production numbers plummeted. There were redundancies at Gaydon to reduce existing costs, but as a private company they were abke to remain 'under the radar' and get on with the job. As the economic climate gradually improved, so did the company.

Once a company becomes a quoted company, some different circumstances arise. When difficult trading times occur, then sometimes predators become interested.

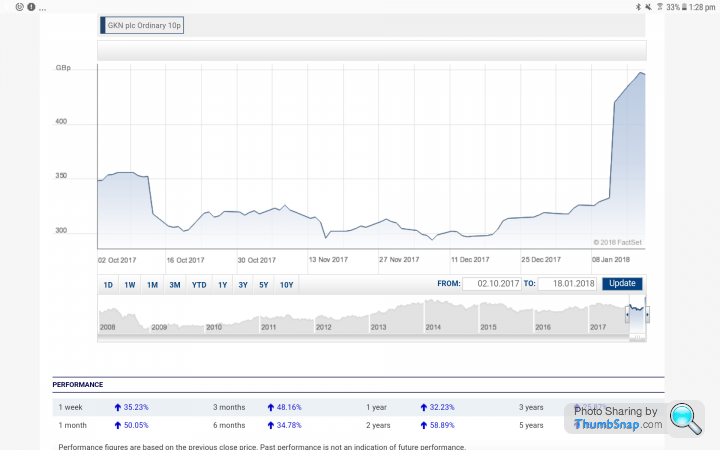

This has just happened to GKN (vested interest). The share price chart below tells the story. A few months ago GKN announced a profits warning (the share price drop). This week, an unsolicited takeover bid has been announced (the share price rise).

Anyone can attempt a takeover when a company is publicly quoted, but it could not happen to Aston Martin now.

Many of you will know all about this post flotation risk, but I thought it might be worth mentioning again.

If the present majority shareholders decide to float the Company though, then that is what will happen.

I fear this is quite awkward.

Usually a private equity shareholder wants to sell after a few years, and obviously at the best price.

Often an IPO can achieve a good price.

They are in business to take risks and make money. Nothing wrong with that.

After they have left the scene though, it is just another deal completed for them.

Aston Martin PLC would then be in the 'jungle', with a risk of being bought by anybody, particularly during difficult trading periods, because then the maket value would be lower.

Zod said:

I depends on how much they float. Few IPOs these days are of more than 28-29%. You can't launch a bid with that level of free float unless you get enough of the pre-IPO shareholders on side.

Thank you Zoe, an important point.

Is there a pattern, whereby when private equity firms sell, it is usually their entire stakes ?

I think in this case, the holding is stated as 37.5%, so still below the crucial level.

The other shareholders, I think have been much longer-term (since the Ford sale), not that we can read anything into that.

RL17 said:

So Ferrari ...MV of $22.5bn (PE ratio of 35)

Seen reports of Aston at £5bn, or just under $7bn.

Seen reports of Aston at £5bn, or just under $7bn.

The Ferrari PE is historic presumably?

Would you consider Ferrari to be completely unique? A car manufacturer, supplier of branded 'objects' and operator of profitable theme parks. I hear that they don't even have to sell cars anymore. Customers apply and apparently are then vetted, to see if they are eligible to buy one.

For AM, the talk we have heard, about luxury goods ratings for a car manufacturer puzzles me.

Perhaps depends on whether one is a seller, or buyer of the stock.

2016 Pre Tax Loss was said to be -£162.8 million.

A 2017 Pre tax positive figure I think is forecast, but for an IPO MV of £5bn, how high would that make the PE ?

Edited by Jon39 on Friday 19th January 22:38

Excellent news. Back in the black.

Thought the talk of ' Profits grow by quarter of a billion pounds ' was just a little too much hype, when the pre-tax was £87m.

"Job done", AP is reported to have said. I hope those were not his words.

I have mentioned before, but there is an interesting pattern now developing, in comparison to the period when the DB9 and Vantage were introduced.

The Company was profitable from 2000 to 2010 (except 2004). Peak production at Gaydon was 7281 cars in 2007. Peak pre-tax profit of that period was £57m in 2006, the year before the Ford sale.

I will look at the 2017 accounts, when they appear at Companies House.

New Articles of Association were adopted in May 2017, and I noticed the signature of Dr. Bez. Presumably he has retained his shareholding.

ajr550 said:

That knighthood for Andy Palmer that nobody wanted to support must be getting closer !

My guess is that Dr. Palmer would want to show that he and his team, were responsible for sustaining profitability, before any business honours are considered.

A decade or so ago, two new models were introduced, there were sales and production records, and the Company was profitable.

No gong for Dr. Bez.

The tricky part is always when the 'honeymoon' period for each mainstream new model ends, and then sales begin to decline. For the DB9 that occurred in year 3 after launch, and for the Vantage it was year 4, although unfortunately a recession probably had an influence on the timing of that.

RobDown said:

Totally agree

The promising thing here though is that there’s a steady stream of new model launches planned (one a year) so hopefully AML can avoid that famine/feast routine

critical one though is the DBX (PH is going to hate it/hope it’s not launched in lime). Get that one right and it will be Saint Palmer not just Sir...

The promising thing here though is that there’s a steady stream of new model launches planned (one a year) so hopefully AML can avoid that famine/feast routine

critical one though is the DBX (PH is going to hate it/hope it’s not launched in lime). Get that one right and it will be Saint Palmer not just Sir...

Yes Rob, if the DBX sells as planned (was 7,000 pa mentioned), then that will be the masterstroke.

I have been thinking about the annual introduction of new models, as a way to keep the early sales momentum flowing.

It might not as straight forward as it seems. Presumably as before with the DB9 and Vantage, it is the DB11 and Vantage that will be the two best seller mainstream models, so those sales will be the important ones. It sounds as though most of the other models will be far more expensive, therefore one would expect lower sales numbers. There should of course be the potential, for a greater amount of profit on each car. The Taraf is at a high price point, but to be a profitable overall project, possibly not enough sold.

Edited by Jon39 on Wednesday 28th February 16:46

The Chinese motor manufacturer Geely has acquired almost 10 per cent of Daimler for about $9bn, becoming its largest shareholder in the latest sign of the global ambitions of the group.

This indirectly gives them a stake in Aston Martin of nearly 0.5%.

Geely already own Volvo, the London Taxi Cab maker, and a 51% stake in Lotus.

Li Shufu founded Geely in 1986 as a refrigerator maker, with money borrowed from his family. He transformed the company into a success, selling inexpensive products to Chinese consumers.

He only began car manufacturing in 2002.

Together with electric and autonomous, are we seeing the begining of major changes, in the long-standing established order of motor manufacturers.

No announcement yet, but here is some fresh market talk.

https://news.sky.com/story/aston-martin-lines-up-b...

RobDown said:

I struggle to believe they will go for a sole listing in New York, the natural home for this one should be London.

And a dual listing seems unnecessary (cost wise) at this point.

Might be fun to put a bit of money into it

And a dual listing seems unnecessary (cost wise) at this point.

Might be fun to put a bit of money into it

Kleinman - his catchphrase is always, "Yes, that's right Ian".

Agree, 'Hand made in England, listed in USA', does not have the same ring to it.

A bit of money being the operative word. Just 18 cars sold during February in UK, but supposedly worth £5 billion.

It is the sort of shareholding where I like to frame the share certificate, but they will probably refuse to issue certificates.

See you at the AGM, Rob.

HBradley said:

As was mentioned in the article, It’s also Brexit-proof.

You have lost me with that, Humphrey.

The Company is domiciled in the UK.

Extract from article;

' While the UK car market has been beset by Brexit-related jitters, a decision to list in New York would be unrelated to the UK's departure from the European Union, the source added. '

RobDown said:

We value stocks based on future prospects and fundamentals, and those aren’t materially driven by the listing location.

Agree with that, so;

Present fundamentals do not equal £5,000,000,000. The 2017 (and probably 2018) P/E number would be too big for the column.

The last sale was I think at £368 million, and record production of over 7,000 was achieved soon after that.

The big IPO sell must therefore be purely on future prospects, ie. DBX.

They really will be able to use that frequently used motor manufacturers saying, in the case of the DBX,

'this is the most important car in the history of the company'.

Thinking about the 2018 financial year, UK DB11 sales are slowing (don't know worldwide), and the new Vantage production will only be for half of the year.

Perhaps therefore, if profits growth is modest in 2018, an early flotation would be better.

Having said that though, do profits forecasts still normally appear in an IPO prospectus?

Edited by Jon39 on Tuesday 6th March 10:48

Zod said:

Profit forecasts rarely appear in IPO prospectuses because of liability concerns. Forecasts get to the market through the "independent" connected analysts' research.

Thank you Zod.

I spotted your use of quotation marks.

If there is to be a float, then perhaps an early one will work best for the sellers.

I meant to refer to the marked decrease in net assets. Have not seen the 2017 accounts yet.

Presumably that reflects all of the new model development.

Perhaps an IPO will be an exit for the private equity investor, but also an opportunity for equity fund raising for the Company.

The present amount of debt in relation to profits worries me. Any comments about that?

HBradley said:

Jon, unless I've mis-interpreted the quote, the fact that the offering is in NY would insulate it from Brexit?

Or am I wrong?

Or am I wrong?

When a UK company has a share listing in USA, it is just where the market place is, for shareholders to buy and sell their shares.

If the company is situated and domiciled in the UK, then all the normal UK rules, laws and conditions continue to apply. Next door might be a London quoted business, but HMRC still want their take from both firms

Whether in or out of the EU, various trade tariffs apply. Some of the present EU tariffs, on finished goods entering the EU, would presumably cease upon exit.

Where the Referendum vote did help AML for a while, was the currency rate. When the exchange rate (£ to $) went immediately down from about 1.45 to about 1.25 following the vote, the profit on each car sold overseas increased (assuming unaltered prices). Recently the exchange rate has been back up near 1.40 again, so that unexpected benefit did not last long. A relief to the UK importers though.

Minglar said:

Thank you for posting that Richard.

It is the first article I have read, which looks much deeper into the financial background.

I have talked here several times about the amount of AML pre flotation hype going on, possibly risking repeating myself. Numerous new models being spoken about (some of which are not due for many years), using words to exaggerate profitability (quarter-billion pound improvement in pre-tax profit), and issuing many more press releases than usual.

It has been noticed before, that creating a frenzy before an IPO does work, by getting a higher price for the seller, but even though investors might get sucked in initially, share prices eventually settle to a level reflecting future expected profitability (a recent example was AO World plc. Even the name hinted at global domination).

As I have previously mentioned, what is going on now is almost a mirror image of the Dr. Bez era at the time the DB9 and Vantage were launched. Even without knowing the accounting aspects described in the article, we all know there are two pairs of new core models, good initial sales and on both occasions the Company becomes profitable. It is becoming apparent to us though, that the DB9 sales, do appear to have been better than the DB11, which is a worry.

Dr. Palmer has been open when describing the SUV needing to financially support the sports cars, so I think if there is a Company flotation, then the new share buyers are effectively taking a single bet on one model range, the SUV.

An interesting point in the article, about the total amount of money being held as interest free deposits for the Valkyrie. Recently Andy Palmer was 'quoted' as saying AML may not make a profit on the Valkyrie project. I couldn't understand why that was said

jonby said:

I don't quite get what you don't quite get ? . . .

. . .Now is the perfect time to float.

. . .Now is the perfect time to float.

First point Jonby.

Yes there is the halo effect, and researching new tech. for future use, but why would a commercial business embark on any big project, without an expectation of profit?

It has been suggested that the car might be priced at £3m.

I think it was also suggested that about 350 serious buyers were refused a car.

With such enormous unsatisfied demand, perhaps the car could have been £4m, or enough to produce a financial return.

What we do not know, and this possibility was suggested by a contributor on here, is are Red Bull really the real owners of the Valkyrie project?

Second point. Yes, you are right. Even before knowing new Vantage sales figures, the timing is looking good for the sellers.

I do have fears for AML being a plc later on (difficult economic cycles etc), but the sellers (private equity) don't normally want to remain owners of any business for too long, but whilst they are still owners, they of course are in the position to make decisions about selling.

( I had better not say anymore about this for a while - might get into trouble with other contributors! )

Flotation getting closer ?

Appear to be hoping for a market valuation, similar to Severn Trent and Marks and Spencer, both of which have adjusted pre-tax profits of over £500 million.

Is that perhaps ambitious, when considering the huge 2017 development spend accounting arrangements?

https://news.sky.com/story/aston-martin-drives-pla...

Edited by Jon39 on Friday 22 June 21:58

-

- North America is the second biggest market (1,277 cars in 2017) for Aston Martin, and clearly very important.

UK being the biggest (1,538 cars in 2017).

Whether the talk of tariffs on cars imported from the EU to the USA is a real possibility, or a negotiating tactic, we do not know, but it might have an influence upon any IPO decision.

Gassing Station | Aston Martin | Top of Page | What's New | My Stuff