Just how far can Covid 19 drive down the markets?

Discussion

Derek Chevalier said:

JulianPH said:

JulianPH said:

You didn't answer my question on your "fixed" charges...?

You still haven't...https://ritholtz.com/2019/04/3-30-the-new-2-20/

https://www.institutionalinvestor.com/article/b1f1...

Edited by Derek Chevalier on Monday 13th April 21:53

janesmith1950 said:

6 months academy then out and about for another 6-12 months with SJP from scratch, or 12 week course with Quilter.

My wife looked at the SJP academy (she hasn't worked since 2011 and never been in financial services). Was accepted into the academy and needed to pass the R01 before it commenced. She went to an SJP open evening mid January and had passed the R01 before end of Feb.

She would have been client facing by September.

Yup but I doubt she would have been researching, designing and managing bespoke portfolios for each individual client but instead merely holding the basic regulation required to permit her to sell the house view and products. My wife looked at the SJP academy (she hasn't worked since 2011 and never been in financial services). Was accepted into the academy and needed to pass the R01 before it commenced. She went to an SJP open evening mid January and had passed the R01 before end of Feb.

She would have been client facing by September.

SJP was really born out of the end of/evolution of the private client stock broker in the mid 90s. As more data and resources became available to retail consumers the days of an individual stock broker running a book of clients and making all the portfolio decisions themselves came to a rapid end. It was already migrating the investment decisions away from the individual stock broker whose performance tended to be unbelievably shocking and self enriching to a central research team who designed house portfolios that brokers had to follow. This was a huge cost saving as it meant the start of the demise of the commission junkie as unless they had a very strong hold on their clients you could replace them with a basic house employee as all they would be doing is mainting the house portfolios. SJP was born as a strange hybrid. Some of its franchise arms were the last hiding place of the commission junkie business but also a big player in the ‘house’ portfolio market.

I recall in the early 2000s lots of the old commission hacks ending up with franchised offices at SJP and also the US Raymond James setting up their franchise operation (a company that gets no scrutiny on PH but if SJP does then so should this little gem). But SJP also offered much better deals to graduates than the transitioning private client brokers who were slower to move away from the nepotism, alcoholism and overt incompetence.

SJP today is a double edged sword. There are some bits which are more akin to double glazing sales and other bits reminiscent of the 90s but on the whole they are an enormous improvement over what they replaced.

Pretty much anyone can become regulated under SJP just like anyone could become a reggie rep through a private client broker and start being allowed to operate some front office aspects so in SJP’s case you are probably, once qualified to the basic regulatory requirement, able to talk to clients and talk to potential clients I doubt that you are permitted to discuss anything other than the house or franchise products and your development will be monitored etc.

The private client industry moved into the modern wealth management industry as well as the IFA industry.

The clue is in the name as it is a long read but taken at face value it's helped me understand some of what I was watching unfold.

The long read, How coronavirus almost brought down the global financial system

The long read, How coronavirus almost brought down the global financial system

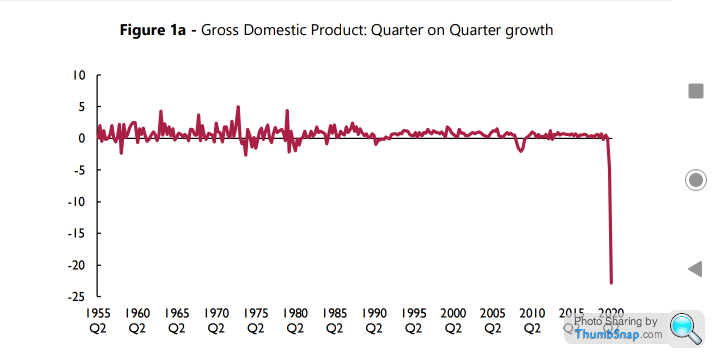

Scary chart of the month from here

https://www.niesr.ac.uk/publications/april-2020-gd...

The last data point is a forecast, but even if it's remotely accurate shows how unprecedented all this is.

https://www.niesr.ac.uk/publications/april-2020-gd...

The last data point is a forecast, but even if it's remotely accurate shows how unprecedented all this is.

Derek Chevalier said:

rockin said:

People who are better at guesstimating than others tend to be the ones who earn the best returns - which links with the concept of "the more I practice the luckier I get".

I think you would struggle to find a serious player in the financial markets who would agree. The market just isn't that generous because you have people that are smarter, with more information and can act more quickly upon it that can exploit any inefficiencies before you even realise they exist.If you have the good fortune to speak to one of the very successful quant hedge funds (and bearing in mind these people have almost unlimited resources), they will tell you the edges are tiny.

How on earth can someone's "guesstimate" be better than the thousands of other people trying to do the same thing with the same information?

This is £3.95 on Kindle - its worth a read.

https://www.amazon.co.uk/Incredible-Shrinking-Alph...

I grew up, in professional terms, in the general environment that you espouse which is that you build a long term plan that doesn’t seek alpha but seeks to follow predicted general market returns and maximise tax efficiency. It’s very boring but it’s going to work and much of what you pay for ongoing as a client is oversight that the plan structure remains relevant as does the tax efficiency etc. but also much is to have a mothering arm to ensure the client sticks to the plan.

But in many regards there is a new ‘alpha’ born from the absolutely enormous migration of serious retail investors away from individual equities to massive funds. Funds that have specific investment remits that cannot deviate in the face of evolving market conditions.

I pretty much invest in major index trackers. It’s boring and unadventurous and my pension is really boring, structured for someone much older and giving away a lot of potential returns for someone my age. But I earn my living from the markets and a big shock to the markets could easily translate to an enormous shock to my income and prospects going forward so my investments are extremely risk averse, just looking for 4-5% average annual returns.

However, I use products such as spreadbets to generate an alpha. Not trading as I don’t believe you can make money trading in the typical sense. When the market went into sell off I hedged a portion of my portfolio just short selling the FTSE and S&P. Going forward I am very comfortable with the view that oil will trend back up towards $75 so expecting to be able to build exposure to oil through a later point in the year and add a small return over the market. Likewise I’m starting to add small index positions aiming to generate a small additional return as the market recovers. And prior to the C19 event there have always been boring defensive blue chip stocks that get trapped in 5-10% pricing cycles where you could seek to grab a .5-1% return over a week using spreadbets to avoid Stamp Duty so making that activity viable.

I think the new alpha comes from people holding say a Vanguard fund, understanding that it operates to a fixed set of rules and that the market doesn’t, that the market will have phases when certain sectors are outperforming and others underperforming but the modern fund portfolio cannot take advantage. I think the risk is that investors then start trading funds, just looking at which ones are going up this month more than the one they are holding and swapping in to it. Personally I see this as trading and really bad trading as it is essentially paying huge fees away for an event that has already happens. It’s like buying tickets at face value for an event that has just finished. Conversely, I feel that investors should do more what you advocate which is to build an unadventurous portfolio and strategy that will have enough ongoing contributions to meet the end objectives on a pretty modest expected return and then seek to find alpha around that structure if they do wish. Buy your Vanguard funds, set up regular monthly contributions that are large enough to meet your long term objective but then don’t go trading these funds like platforms such as HL naturally encourage through the delivery of live data and a trading platform but instead look to periodically make short term investments around your long term portfolio.

The weightings of oil, pharma, utilities can’t change in a typical fund but there are times when you know that being a little over or underweight in a sector is the right thing. It’s madness to change your fund to achieve that but perfectly logical to use a spread bet to take a small element of additional exposure or to reduce exposure for a short period of time. That’s what I think modern alpha is. It’s the application of modern financial retail tools to apply a thin layer of flexibility and agility over the modern retail fund trend.

ILikeCake said:

Scary chart of the month from here

https://www.niesr.ac.uk/publications/april-2020-gd...

The last data point is a forecast, but even if it's remotely accurate shows how unprecedented all this is.

My understanding of the markets is that a bounce back recovery is priced in, so an opposite swing in growth will near balance out the fall.https://www.niesr.ac.uk/publications/april-2020-gd...

The last data point is a forecast, but even if it's remotely accurate shows how unprecedented all this is.

I don’t think that’s how its going to work out. Although there is economic activity ‘waiting’ to happen (so is not lost) there is a huge amount of discretionary spending that has been lost and will not be recovered.

soofsayer said:

My understanding of the markets is that a bounce back recovery is priced in, so an opposite swing in growth will near balance out the fall.

I don’t think that’s how its going to work out. Although there is economic activity ‘waiting’ to happen (so is not lost) there is a huge amount of discretionary spending that has been lost and will not be recovered.

There was a study by Oxford Uni that thought the recovery would be sharp and quick. Let's hope so.I don’t think that’s how its going to work out. Although there is economic activity ‘waiting’ to happen (so is not lost) there is a huge amount of discretionary spending that has been lost and will not be recovered.

The way I see it is that this is a once in a 100+ year event (fingers crossed!) and no one has the foggiest what will happen. There are so many theories and forecasts out there that one is going to be correct just by chance alone.

I don't think there is even a consensus about how much such a drastic short-term fall in GDP really matters. Individuals/businesses have largely been protected so far by the gov's measures of shielding imminent drops in personal welfare by switching it to long-term issues about the sustainability of gov debt.

We live in interesting times...

DonkeyApple said:

I think the new alpha comes from people holding say a Vanguard fund, understanding that it operates to a fixed set of rules and that the market doesn’t, that the market will have phases when certain sectors are outperforming and others underperforming but the modern fund portfolio cannot take advantage. I think the risk is that investors then start trading funds, just looking at which ones are going up this month more than the one they are holding and swapping in to it. Personally I see this as trading and really bad trading as it is essentially paying huge fees away for an event that has already happens. It’s like buying tickets at face value for an event that has just finished. Conversely, I feel that investors should do more what you advocate which is to build an unadventurous portfolio and strategy that will have enough ongoing contributions to meet the end objectives on a pretty modest expected return and then seek to find alpha around that structure if they do wish. Buy your Vanguard funds, set up regular monthly contributions that are large enough to meet your long term objective but then don’t go trading these funds like platforms such as HL naturally encourage through the delivery of live data and a trading platform but instead look to periodically make short term investments around your long term portfolio.

Good post DA. I admit I had to have a word with myself regarding the bit in bold. Out of interest do you use Vanguard funds, and if so which ones if you don't mind me asking.. red_slr said:

The one thing that seems to be missed by the media is that this could easily be just a blip and the main pandemic could come in the winter of 2020 or even 2021.

There seems to be a very strange pattern to me that most countries have squashed the pandemic into 6-8 weeks as we are seeing cases start to reduce now in some countries.

Globally there are about 100,000 deaths. I am sure this will rise but hopefully we are approaching the peak so perhaps we are half way there.

BUT pandemics have the power to kill millions, tens or hundreds of millions. If we have shut down the world for what could just be a blip then I don't like to think what could happen if this comes back mutated in the winter.

The big worry in my mind is that there is only one sure fire way to end a serious global financial disaster... and that involves a lot of bombs.

Yes maybe China (the apparent source alleged) could be the target of a lot of American bombsThere seems to be a very strange pattern to me that most countries have squashed the pandemic into 6-8 weeks as we are seeing cases start to reduce now in some countries.

Globally there are about 100,000 deaths. I am sure this will rise but hopefully we are approaching the peak so perhaps we are half way there.

BUT pandemics have the power to kill millions, tens or hundreds of millions. If we have shut down the world for what could just be a blip then I don't like to think what could happen if this comes back mutated in the winter.

The big worry in my mind is that there is only one sure fire way to end a serious global financial disaster... and that involves a lot of bombs.

Phooey said:

Good post DA. I admit I had to have a word with myself regarding the bit in bold. Out of interest do you use Vanguard funds, and if so which ones if you don't mind me asking..

I think this is the big new risk facing private investors, the vast quantities of live data that is delivered via a trading terminal. On the one has we have moved away from the old environment where bad private client brokers could spank a client’s portfolio for some comm to one where clients just do it themselves for the broker.

I don’t hold any Vanguard stuff. Nothing at all against them it’s just that I keep stuff really simple and just use ishares trackers. Having said that I was adamant I didn’t own any Woodford but I recurved a letter saying I did in my pension so maybe my pension holds some Vanguard.

I’m in the middle of trying to get some of their ETFs added to our spreadbet platform as I think they might be of use to some clients who fancy using a bit of leverage, using the tax advantage or hedging existing positions etc.

DonkeyApple said:

I think this is the big new risk facing private investors, the vast quantities of live data that is delivered via a trading terminal. On the one hand we have moved away from the old environment where bad private client brokers could spank a client’s portfolio for some comm to one where clients just do it themselves for the broker.

Funny.. and also very true

DonkeyApple said:

I don’t hold any Vanguard stuff. Nothing at all against them it’s just that I keep stuff really simple and just use ishares trackers. Having said that I was adamant I didn’t own any Woodford but I recurved a letter saying I did in my pension so maybe my pension holds some Vanguard.

I’m in the middle of trying to get some of their ETFs added to our spreadbet platform as I think they might be of use to some clients who fancy using a bit of leverage, using the tax advantage or hedging existing positions etc.

Cheers for reply re Vanguard. I'm always interested if the guys "in the business" use VG. I put my missus's ISA into LS80, and also added a few other bits and bobs from their shop, but have to confess to getting a little confused when it comes to the differences between ETFs and Index Funds. I have Googled it and ashamed to say it went through one ear and out...I’m in the middle of trying to get some of their ETFs added to our spreadbet platform as I think they might be of use to some clients who fancy using a bit of leverage, using the tax advantage or hedging existing positions etc.

Woodford. I had (and still have bits of) some WF. In hindsight probably my best fund of the past 6 months. Who's laughing now..

Phooey said:

but have to confess to getting a little confused when it comes to the differences between ETFs and Index Funds.

It's not really a direct comparison.An index can be tracked by a fund or an ETF.

An ETF can be traded live on the stock exchange whilst funds have set valuation points and are usually forward priced and brought/sold at a set point daily.

So if you decide at 10.44am tomorrow morning that you want to buy into a a FTSE100 index tracker you can buy an ETF there and then in pretty much realtime.

If you buy the same index via a fund you'd place the order and it would probably be submitted for dealing on Thursday and hopefully you'd get the price at Thursdays valuation point.

You can see where that falls down if you're trying to time or trade on short term price movements.

There are probably other differences but I think those are the headlines other than if you're investing outside of an ISA be cautious about the way some ETFs report income.

b hstewie said:

hstewie said:

hstewie said: It's not really a direct comparison.

An index can be tracked by a fund or an ETF.

An ETF can be traded live on the stock exchange whilst funds have set valuation points and are usually forward priced and brought/sold at a set point daily.

So if you decide at 10.44am tomorrow morning that you want to buy into a a FTSE100 index tracker you can buy an ETF there and then in pretty much realtime.

If you buy the same index via a fund you'd place the order and it would probably be submitted for dealing on Thursday and hopefully you'd get the price at Thursdays valuation point.

You can see where that falls down if you're trying to time or trade on short term price movements.

There are probably other differences but I think those are the headlines other than if you're investing outside of an ISA be cautious about the way some ETFs report income.

Interesting - thank you for explanation. Would an ETF be the preferred choice then inside an ISA/SIPP (obviously subject to costs)?An index can be tracked by a fund or an ETF.

An ETF can be traded live on the stock exchange whilst funds have set valuation points and are usually forward priced and brought/sold at a set point daily.

So if you decide at 10.44am tomorrow morning that you want to buy into a a FTSE100 index tracker you can buy an ETF there and then in pretty much realtime.

If you buy the same index via a fund you'd place the order and it would probably be submitted for dealing on Thursday and hopefully you'd get the price at Thursdays valuation point.

You can see where that falls down if you're trying to time or trade on short term price movements.

There are probably other differences but I think those are the headlines other than if you're investing outside of an ISA be cautious about the way some ETFs report income.

Phooey said:

Interesting - thank you for explanation. Would an ETF be the preferred choice then inside an ISA/SIPP (obviously subject to costs)?

I don't work in the financial industry so this is just my take on it as a (very) amateur retail investor but if the intention is to buy it and hold it I don't think it will make much practical difference whether you choose a fund or an ETF.Dealing fees and platform fees can make a difference and of course the fees on the investments themselves but I'm not sure there's much else to make one "better" than the other.

bhstewie said:

hstewie said: I don't work in the financial industry so this is just my take on it as a (very) amateur retail investor but if the intention is to buy it and hold it I don't think it will make much practical difference whether you choose a fund or an ETF.

Dealing fees and platform fees can make a difference and of course the fees on the investments themselves but I'm not sure there's much else to make one "better" than the other.

Again, thank you. ^^ makes sense.Dealing fees and platform fees can make a difference and of course the fees on the investments themselves but I'm not sure there's much else to make one "better" than the other.

I quite often Google these things but come away more confused than before

The figures for gdp and possible drop over the year of 15% is not making for pleasant reading tonight.

That’s basically unheard of in living memory and personally just my opinion but I think we are looking at long term economic disaster. I just can’t see how businesses can recover if the dip is as large as estimated and the hit the market’s might take is going to be catastrophic.

I am starting to seriously consider worst case options now. As a business owner we always look long term but if we were to see trade drop even 20% then it’s game over. We could probably survive a year or two of that but for what? If we are going to end up stuck in a 10 year depression hoping “next year will be better” then it won’t be worth putting ourselves through that.

That’s basically unheard of in living memory and personally just my opinion but I think we are looking at long term economic disaster. I just can’t see how businesses can recover if the dip is as large as estimated and the hit the market’s might take is going to be catastrophic.

I am starting to seriously consider worst case options now. As a business owner we always look long term but if we were to see trade drop even 20% then it’s game over. We could probably survive a year or two of that but for what? If we are going to end up stuck in a 10 year depression hoping “next year will be better” then it won’t be worth putting ourselves through that.

red_slr said:

The figures for gdp and possible drop over the year of 15% is not making for pleasant reading tonight.

That’s basically unheard of in living memory and personally just my opinion but I think we are looking at long term economic disaster. I just can’t see how businesses can recover if the dip is as large as estimated and the hit the market’s might take is going to be catastrophic.

I am starting to seriously consider worst case options now. As a business owner we always look long term but if we were to see trade drop even 20% then it’s game over. We could probably survive a year or two of that but for what? If we are going to end up stuck in a 10 year depression hoping “next year will be better” then it won’t be worth putting ourselves through that.

But as I've said before, it's totally different from a 'normal' demand led recession in which GDP drops are the result of the downturn. . If you run a business and trade drops because people don't have much money or don't want to spend it then how worried you should be depends on much it drops, and yes 15% or 20% is very scary.That’s basically unheard of in living memory and personally just my opinion but I think we are looking at long term economic disaster. I just can’t see how businesses can recover if the dip is as large as estimated and the hit the market’s might take is going to be catastrophic.

I am starting to seriously consider worst case options now. As a business owner we always look long term but if we were to see trade drop even 20% then it’s game over. We could probably survive a year or two of that but for what? If we are going to end up stuck in a 10 year depression hoping “next year will be better” then it won’t be worth putting ourselves through that.

But if it drops because they authorities won't let people through the door, what matters is how long until the lockdown lifts. If it's reasonably quick your customers will return. Suddenly noticing that your sales are down 100% doesn't make it any worse.

It’s not now or just after the lockdown lifts that’s the worry. We know what’s happening now but the worry is 2-3 years what happens then and how much money do I have to pump in to get to that point.

Honestly if we see a fall of 15% in gdp over long periods I expect we could lose 50%+ of trade. During 08/09 we lost about 25-30% and what was the fall in gdp then? Wasn’t it only a few %?

It took till 2015 to recover. This is a very different proposition...

Honestly if we see a fall of 15% in gdp over long periods I expect we could lose 50%+ of trade. During 08/09 we lost about 25-30% and what was the fall in gdp then? Wasn’t it only a few %?

It took till 2015 to recover. This is a very different proposition...

Gassing Station | Finance | Top of Page | What's New | My Stuff