Intelligent Money - your investment questions answered

Discussion

JulianPH said:

It was an itch worth scratching as this does indeed appear to be the case. So a company account would be tax neutral in this respect, regardless of whether the company holds the shares directly, through funds, or through our portfolios.

Thanks for confirming what I thought. As with anything the devil is in the detail. I know that it applies to dividends from UK companies.What I don't know is what else it applies to and what percentage of the income of say your Growth Portfolio would be treated as tax paid in a company.

The fund manager would be the only source of this information as only they know the breakdown of income within the fund.

DibblyDobbler said:

JulianPH said:

You can see the asset allocation of each of our portfolios here:

https://www.intelligentmoney.com/private-clients/o...

Hi Julian - I'm trying to compare your portfolios to other (seemingly at least) similar ones - eg Vhttps://www.intelligentmoney.com/private-clients/o...

d Ly and while I can see the cumulative performance and 10 year average I would like to see a graphical representation to better gauge volatility, is this possible please?

d Ly and while I can see the cumulative performance and 10 year average I would like to see a graphical representation to better gauge volatility, is this possible please?If not then no problem, it was just a thought

Thanks, Mike.

As you can see, we fell and recouped. To be fair, so did many others. This is why I wanted to give you a very bad snapshot, rather than a conveniently good one!

Thanks for reminding me to push this through the development team, it should not be difficult!!!

Cheers

Julian

Edited to add - I showed the last 6 months (the worst) rather than the last year.

Edited by JulianPH on Friday 22 February 16:58

springfan62 said:

Thanks for confirming what I thought. As with anything the devil is in the detail. I know that it applies to dividends from UK companies.

What I don't know is what else it applies to and what percentage of the income of say your Growth Portfolio would be treated as tax paid in a company.

The fund manager would be the only source of this information as only they know the breakdown of income within the fund.

As the investment manager we can also give that breakdown. This doesn't make us right or wrong for you though. What I don't know is what else it applies to and what percentage of the income of say your Growth Portfolio would be treated as tax paid in a company.

The fund manager would be the only source of this information as only they know the breakdown of income within the fund.

I hope we are right, but we will be the first to tell you if something else could be more suitable for you. This is what differentiates us from others!

Cheers

JulianPH said:

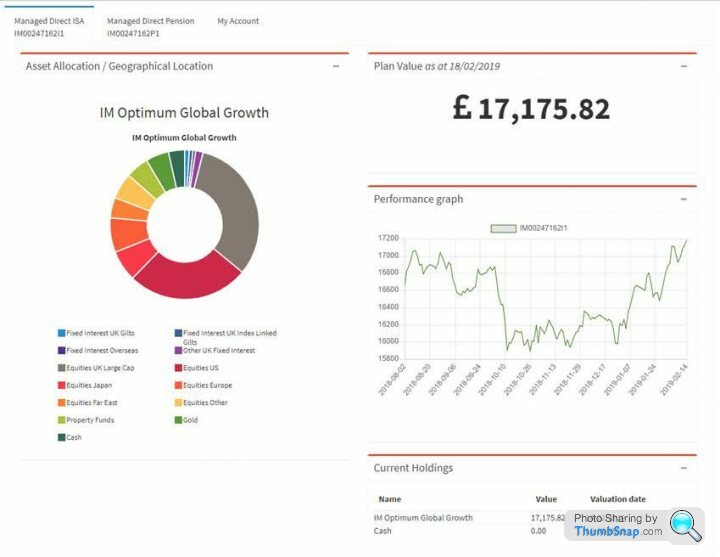

Hi Mike, I don't know why we don't already do this for past performance as you get exactly this (graphical representation) in your client view. Here is our worst year ever for a client with a small sum invested (to highlight the volatility of our Global Growth Portfolio - rather than grandstand on larger numbers over longer time frame. i.e. to understate, not overstate). Personal client data has obviously been removed:

As you can see, we fell and recouped. To be fair, so did many others. This is why I wanted to give you a very bad snapshot, rather than a conveniently good one!

Thanks for reminding me to push this through the development team, it should not be difficult!!!

Cheers

Julian

Edited to add - I showed the last 6 months (the worst) rather than the last year.

Thanks very much once again Julian As you can see, we fell and recouped. To be fair, so did many others. This is why I wanted to give you a very bad snapshot, rather than a conveniently good one!

Thanks for reminding me to push this through the development team, it should not be difficult!!!

Cheers

Julian

Edited to add - I showed the last 6 months (the worst) rather than the last year.

Edited by JulianPH on Friday 22 February 16:58

Although just a snapshot that is very interesting. Your Global Growth Portfolio seems broadly similar to the VL 80% equity fund and although it has underperformed the VL80% fund over 5 years this was an amazing bull run (which is not likely to happen again any time soon I suspect) and in a poor period your fund has done a bit better which I guess points to your aim of growth while protecting assets?

Also your more defensive funds compare well to the VL equivalents from what I can see.

I'll be keeping an eye out for when your IT boys can get this hooked up properly!

Thanks again and have a great weekend

DibblyDobbler said:

Thanks very much once again Julian

Although just a snapshot that is very interesting. Your Global Growth Portfolio seems broadly similar to the VL 80% equity fund and although it has underperformed the VL80% fund over 5 years this was an amazing bull run (which is not likely to happen again any time soon I suspect) and in a poor period your fund has done a bit better which I guess points to your aim of growth while protecting assets?

Also your more defensive funds compare well to the VL equivalents from what I can see.

I'll be keeping an eye out for when your IT boys can get this hooked up properly!

Thanks again and have a great weekend

No problem Mike Although just a snapshot that is very interesting. Your Global Growth Portfolio seems broadly similar to the VL 80% equity fund and although it has underperformed the VL80% fund over 5 years this was an amazing bull run (which is not likely to happen again any time soon I suspect) and in a poor period your fund has done a bit better which I guess points to your aim of growth while protecting assets?

Also your more defensive funds compare well to the VL equivalents from what I can see.

I'll be keeping an eye out for when your IT boys can get this hooked up properly!

Thanks again and have a great weekend

The main difference between us and Vanguard LifeStrategy is we include additional asset classes and, of course, have active asset allocation rather than follow market weightings.

It is these additional assets classes (and the asset allocation management around them) that enables us to deliver broadly similar investment returns at reduced levels of volatility. In current volatile markets it goes without saying managing volatility in the way we do is an important factor, as you have highlighted.

I also think it would be helpful if I explained why we put so much emphasis on capital preservation (though as an investment manager returns are of course hugely important!):

Nutmeg, for example, must have raised over £100m in private equity/venture capital investments. It has spent a huge amount of this on advertising and underwriting very large annual losses (c.£12m last year IIRC). The effect of this is like most other providers it is owned by corporate institutions who are speculating on its future success.

IM is completely different. I launched it (17 years ago) entirely with my own money. Whilst some industry friends went on to become shareholders and joined as directors (I am still the majority shareholder) this was due to me knowing them as like minded friends (with the exception of one we have all had family holidays together and the one that, for no particular reason, hasn't is my daughters Godfather).

So when I refer to me (for ease) I am speaking on behalf of all five of us.

I value my wealth and income (greater than many and less than others, but all earned through years of hard work) and the lion's share of it is in IM. The most important thing to me is to preserve this whilst still growing it. I apply the same principle to our clients.

The best way for me to achieve this is to use investment strategies that are designed to both protect and grow the assets and/or income of our clients, as this protects and grows my own assets and income.

This may sound selfish, but I see it as aligning my financial interests with those of our clients. If you do well, then so do I. If you don't then I lose too - and I don't like losing!

I believe this is why we have c. double the asset that Nutmeg have, despite us not having sold our soul to corporate finance and spent multi-millions on advertising. Our growth has been through word of mouth recommendations.

I only took the decision to take out our first ever direct marketing on PH two months ago because after many years of trying to help people out on the finance forum (and being active on others where I have made some great friends in the real world) I could see a synergy.

Anyway, that was a bit of a ramble, sorry for that!

Have a great weekend yourself. The rugby should be interesting...

The rugby was indeed 'interesting' - not a great weekend for either of us I suspect

Anyway, thanks again for the comprehensive reply. You make a compelling case for the IM proposition and if I do get myself psyched up to move (from HL) it will be to yourselves. I'm not going to rush into anything but what it boils down to is whether I am going to be happy choosing my own funds or whether I want somebody else to do it... recent experience would indicate the latter and it doesn't seem like something I want to be thinking about in my dotage (which appears to be fast approaching!)

Thanks again, Mike.

Anyway, thanks again for the comprehensive reply. You make a compelling case for the IM proposition and if I do get myself psyched up to move (from HL) it will be to yourselves. I'm not going to rush into anything but what it boils down to is whether I am going to be happy choosing my own funds or whether I want somebody else to do it... recent experience would indicate the latter and it doesn't seem like something I want to be thinking about in my dotage (which appears to be fast approaching!)

Thanks again, Mike.

I thought I would give an update on our International Private Client position.

Having spent over a year researching to set up an off-shore division to meet this we have (with the help of this thread) realised that this is simply not required these days.

The off-shore market seems to exist solely hide very expensive products products that facilitate - and hide - the payment of vast commissions to off-shore financial 'advisers' who are subject to very low levels of regulation when compared to the UK.

However, for British citizens resident abroad this is no longer the 'necessary' route it used to be (not that they will ever be told this by their local 'adviser'.

There are a few website changes and an international Anti Money Laundering identity verification package to bolt on, but this should only take a week or two and then access will be available.

If the country you reside in requires you to pay tax on UK held investments you will need to wait a short while longer for the completion of our Tax Certificate software. If it doesn't you can go straight ahead in a week or two.

Same PH deal - PH2607 removes the initial charge and minimum investment criteria.

Cheers

Having spent over a year researching to set up an off-shore division to meet this we have (with the help of this thread) realised that this is simply not required these days.

The off-shore market seems to exist solely hide very expensive products products that facilitate - and hide - the payment of vast commissions to off-shore financial 'advisers' who are subject to very low levels of regulation when compared to the UK.

However, for British citizens resident abroad this is no longer the 'necessary' route it used to be (not that they will ever be told this by their local 'adviser'.

HMRC said:

HMRC Guidance HS300 Non-residents and investment income

"With the exception of income from property in the UK and investment income connected to a trade in the UK through a permanent establishment, the tax charge for non-residents on investment income arising in the UK is restricted to the amount of tax, if any, deducted at source."

"With the exception of income from property in the UK and investment income connected to a trade in the UK through a permanent establishment, the tax charge for non-residents on investment income arising in the UK is restricted to the amount of tax, if any, deducted at source."

HMRC said:

Capital Gains Tax if you're abroad

"You have to pay tax on gains you make on residential property in the UK even if you’re non-resident for tax purposes. You do not pay Capital Gains Tax on other UK assets, for example shares in UK companies, unless you return to the UK within 5 years of leaving."

So we are making our existing portfolios (not new versions of them - the same ones currently used within ISAs/SIPPs/Pensions by UK residents) available in a gross roll-up account to British citizens residing outside of the UK."You have to pay tax on gains you make on residential property in the UK even if you’re non-resident for tax purposes. You do not pay Capital Gains Tax on other UK assets, for example shares in UK companies, unless you return to the UK within 5 years of leaving."

There are a few website changes and an international Anti Money Laundering identity verification package to bolt on, but this should only take a week or two and then access will be available.

If the country you reside in requires you to pay tax on UK held investments you will need to wait a short while longer for the completion of our Tax Certificate software. If it doesn't you can go straight ahead in a week or two.

Same PH deal - PH2607 removes the initial charge and minimum investment criteria.

Cheers

Mr Pointy said:

How's the tax-free GIA for UK residents coming along?

Currently in DonkeyApple's more than capable hands.We have forwarded his company transaction reports so that it can cost these in to the offering.

Obviously running our portfolios on his platform (to make them tax free) is going to incur additional costs. So the current step is to ensure any additional fees do not detract from the tax free returns (which is unlikely).

After that it is pretty straightforward to be honest. I'll keep you up to date!

Cheers

JulianPH said:

So we are making our existing portfolios (not new versions of them - the same ones currently used within ISAs/SIPPs/Pensions by UK residents) available in a gross roll-up account to British citizens residing outside of the UK.

There are a few website changes and an international Anti Money Laundering identity verification package to bolt on, but this should only take a week or two and then access will be available.

If the country you reside in requires you to pay tax on UK held investments you will need to wait a short while longer for the completion of our Tax Certificate software. If it doesn't you can go straight ahead in a week or two.

Same PH deal - PH2607 removes the initial charge and minimum investment criteria.

Cheers

?

Great to hear. I’ll be in touch. Soufflé on the cards...There are a few website changes and an international Anti Money Laundering identity verification package to bolt on, but this should only take a week or two and then access will be available.

If the country you reside in requires you to pay tax on UK held investments you will need to wait a short while longer for the completion of our Tax Certificate software. If it doesn't you can go straight ahead in a week or two.

Same PH deal - PH2607 removes the initial charge and minimum investment criteria.

Cheers

?

Testaburger said:

Great to hear. I’ll be in touch. Soufflé on the cards...

And, of course, the soufflé is the most important part!

(For anyone not getting the soufflé reference, a few years ago Testaburger and I were chatting on another thread about Fundsmith. I mentioned that I had dinner with Terry one night discussing his approach. Testaburger said the important thing was not what we discussed, but what had we eaten. We had twice baked cheese soufflé for a starter - hence the recurring comment!)

Edited for clarity!

Edited by JulianPH on Saturday 2nd March 18:01

river_rat said:

Any update on when the Junior ISA will be available?

Hello mateI actually have a meeting about that tomorrow morning. It is the same issue as the international account (a software Key Features update) as we already hold the permissions and the portfolios remain identical. It therefore makes sense to do both the international account and JISA at the same time.

I'll post again tomorrow after the meeting, but I don't see any reason why we can't go live with both of these in the next week or two, certainly in time for the tax year end.

Cheers

Intelligent Money said:

DibblyDobbler said:

Hi IM.

Can I ask a related question please?

Just say I had £800k at retirement - I'm entitled to 25% or £200k TFC I believe.

So I immediately take £100k (for the Aston + a cruise or whatever) - ie half of my entitlement (or 12.5%)

Then a year later I want to take the rest of my TFC - my fund has gone up 10% in the meantime (ie £700k to £710k) - so is the remainder of my TFC £100k or is it 12.5% of £710k ?

Cheers

PS - thinking about it it must be the former as the latter would be silly? Anyway please can you confirm

It's always easier to answer a question when you have answered yourself! It is the former because the later would be silly! Can I ask a related question please?

Just say I had £800k at retirement - I'm entitled to 25% or £200k TFC I believe.

So I immediately take £100k (for the Aston + a cruise or whatever) - ie half of my entitlement (or 12.5%)

Then a year later I want to take the rest of my TFC - my fund has gone up 10% in the meantime (ie £700k to £710k) - so is the remainder of my TFC £100k or is it 12.5% of £710k ?

Cheers

PS - thinking about it it must be the former as the latter would be silly? Anyway please can you confirm

At the point you start drawing benefits the fund value at that time is used to calculate your TFC entitlement

Regards

Nik

The amount crystallised would be a percentage, and if the value of the remaining uncrystallised benefits increased by the time the next Benefit Crystallisation Event happened, the the % entitlement would be worth more.

Are you able to offer flexible drawdown to facilitate this?

Hello crouching pigeon

You are right that this only applies if you crystallise the whole pot and I am guilty of oversimplifying my original answer on the assumption that this was the case.

You could split the pot and keep part of it uncrystallised. You could gain additional TFC if the markets move in your favour but you could also lose out on TFC if the markets fall.

Part of our Private Client Service is to go through the options available and talk you through the advantages and disadvantages of each so you can chose the route best suited to you.

Your last question is one that I can give a simple answer to yes we do offer flexi-access drawdown.

Regards

Nik

You are right that this only applies if you crystallise the whole pot and I am guilty of oversimplifying my original answer on the assumption that this was the case.

You could split the pot and keep part of it uncrystallised. You could gain additional TFC if the markets move in your favour but you could also lose out on TFC if the markets fall.

Part of our Private Client Service is to go through the options available and talk you through the advantages and disadvantages of each so you can chose the route best suited to you.

Your last question is one that I can give a simple answer to yes we do offer flexi-access drawdown.

Regards

Nik

I've just popped on here this evening, so missed the chance to respond first.

Nik was quite correct in his first answer, as when you crystallise your benefits the value of and PCLS (or Tax Free Cash, as we used to call it) is, ahem, crystallised.

However, you are equally correct in stating that crystallisation can be applied only to a part of the pension, leaving the rest to grow and deliver a bigger (or smaller) tax free element in the future. Yes, we offer this.

Since Pension Simplification, pensions have become far more complex (a lost irony).

Providing it is not a Final Salary pension we can help with this at no fee.

I hope these answers help, get in touch (here or directly) if there is anything else.

Cheers

Julian

Nik was quite correct in his first answer, as when you crystallise your benefits the value of and PCLS (or Tax Free Cash, as we used to call it) is, ahem, crystallised.

However, you are equally correct in stating that crystallisation can be applied only to a part of the pension, leaving the rest to grow and deliver a bigger (or smaller) tax free element in the future. Yes, we offer this.

Since Pension Simplification, pensions have become far more complex (a lost irony).

Providing it is not a Final Salary pension we can help with this at no fee.

I hope these answers help, get in touch (here or directly) if there is anything else.

Cheers

Julian

Just to add a question to the above, if I may.

If I take my 25% PCLS and decide that I can live on that for the next 10 years, doesn't my remaining 75% remain invested as it was before the 25% was taken anyway? That is, whether you choose to crystallise the remaining 75% or not, as long as you leave it alone then it's growing as before?

Or am I missing something fundamental here?

This all stems from the fact that I'm 56 next month, have stopped working (possibly for ever, possibly not) and have 2 pension pots with Aviva and Zurich which I'm trying to work out what to do with based on the fact that I want to keep the pots growing but also want to maximise my tax free allowance before the state pension kicks in and takes a lot of that allowance.

Maybe I need to talk to you chaps at some point once I've got my head around my own thoughts and spreadsheets

If I take my 25% PCLS and decide that I can live on that for the next 10 years, doesn't my remaining 75% remain invested as it was before the 25% was taken anyway? That is, whether you choose to crystallise the remaining 75% or not, as long as you leave it alone then it's growing as before?

Or am I missing something fundamental here?

This all stems from the fact that I'm 56 next month, have stopped working (possibly for ever, possibly not) and have 2 pension pots with Aviva and Zurich which I'm trying to work out what to do with based on the fact that I want to keep the pots growing but also want to maximise my tax free allowance before the state pension kicks in and takes a lot of that allowance.

Maybe I need to talk to you chaps at some point once I've got my head around my own thoughts and spreadsheets

garyhun said:

Just to add a question to the above, if I may.

If I take my 25% PCLS and decide that I can live on that for the next 10 years, doesn't my remaining 75% remain invested as it was before the 25% was taken anyway? That is, whether you choose to crystallise the remaining 75% or not, as long as you leave it alone then it's growing as before?

Or am I missing something fundamental here?

This all stems from the fact that I'm 56 next month, have stopped working (possibly for ever, possibly not) and have 2 pension pots with Aviva and Zurich which I'm trying to work out what to do with based on the fact that I want to keep the pots growing but also want to maximise my tax free allowance before the state pension kicks in and takes a lot of that allowance.

Maybe I need to talk to you chaps at some point once I've got my head around my own thoughts and spreadsheets

You are spot on.If I take my 25% PCLS and decide that I can live on that for the next 10 years, doesn't my remaining 75% remain invested as it was before the 25% was taken anyway? That is, whether you choose to crystallise the remaining 75% or not, as long as you leave it alone then it's growing as before?

Or am I missing something fundamental here?

This all stems from the fact that I'm 56 next month, have stopped working (possibly for ever, possibly not) and have 2 pension pots with Aviva and Zurich which I'm trying to work out what to do with based on the fact that I want to keep the pots growing but also want to maximise my tax free allowance before the state pension kicks in and takes a lot of that allowance.

Maybe I need to talk to you chaps at some point once I've got my head around my own thoughts and spreadsheets

Whether crystallised or not the 75% remaining in the pension is invested as it was before (unless you change the portfolio yourself). It doesn't stop being invested.

Feel free to talk to us to help you get your head around things! There is no charge or obligation. In fact, helping people without them becoming clients is one of our greatest source of ongoing referrals, so we welcome it!

Cheers

Thanks Julian for confirming I'm not crazy!

Once I'm ready to have a conversation with you guys, am I best calling the phone number in the OP?

Edit to add: What is/are the reason/s as to whether you crystallise or not the remaining 75%?

Pensions - the more you know, the more you don't!

Once I'm ready to have a conversation with you guys, am I best calling the phone number in the OP?

Edit to add: What is/are the reason/s as to whether you crystallise or not the remaining 75%?

Pensions - the more you know, the more you don't!

Edited by anonymous-user on Wednesday 13th March 14:29

Edited by anonymous-user on Wednesday 13th March 14:29

garyhun said:

Thanks Julian for confirming I'm not crazy!

Once I'm ready to have a conversation with you guys, am I best calling the phone number in the OP?

Edit to add: What is the reasons as to whether you crystallise or not the remaining 75%?

Pensions - the more you know, the more you don't!

I'm not saying you are not crazy, just not on this point! Once I'm ready to have a conversation with you guys, am I best calling the phone number in the OP?

Edit to add: What is the reasons as to whether you crystallise or not the remaining 75%?

Pensions - the more you know, the more you don't!

Edited by garyhun on Wednesday 13th March 14:29

Call the number in the OP or send me a PM and I'll give you the direct line for Nik or Will (they are our main Private Clients Managers working with PHers).

The main reason for crystallising the whole pot is to take the whole tax free cash element in one go (you can only take tax free cash from crystallised funds).

If you only crystallise 50%, for example, you can only take 50% of your tax free cash entitlement at that point in time.

If you have no requirement/need for the tax free cash you can crystallise much smaller amounts as and when you need them with 25% of each amount being tax free.

Either way, anything you do not withdraw remains invested.

You are absolutely right that the more you think know about pensions the more you realise you don't!

Cheers

Gassing Station | Finance | Top of Page | What's New | My Stuff