Has your insurance gone up?

Discussion

LF5335 said:

Interesting comments about actuaries. Are you sure you’re not confusing it with underwriters? Also, marine & aviation on their own are very wide products. Intrigued how you code for what is an extremely niche market with little generics that would justify the cost for the Average Joe. If you’re insuring entire portfolios then there are even fewer generics to build a coding system for.

My question on Boeing relates to the wider piece around the cover you’re offering. Only looking at the damage to the plane, misses the fundamental liability risk. Maybe that goes back to my comment on taking things literally.

I don’t intend to stump up cash to try to disrupt a market that has little to no chance of returning to profitability in the near future. The critical mass needed, the regulatory requirements around solvency alone make Personal Lines business hugely risky with little upside. If the likes of Dorect Libe who were the first real disrupters to the industry are haemorrhaging money and other newer disrupters such as Admiral are sending out thinly disguised profit concerns then I’m nowhere near good enough to sort it out. There are far easier ways to make money. However, you guys seem to believe there are better ways to do it and you’re in the enviable position to be right there and able to do it. Strange that you’re backing away.

Just how do you imagine I'm confusing actuaries with underwriters?My question on Boeing relates to the wider piece around the cover you’re offering. Only looking at the damage to the plane, misses the fundamental liability risk. Maybe that goes back to my comment on taking things literally.

I don’t intend to stump up cash to try to disrupt a market that has little to no chance of returning to profitability in the near future. The critical mass needed, the regulatory requirements around solvency alone make Personal Lines business hugely risky with little upside. If the likes of Dorect Libe who were the first real disrupters to the industry are haemorrhaging money and other newer disrupters such as Admiral are sending out thinly disguised profit concerns then I’m nowhere near good enough to sort it out. There are far easier ways to make money. However, you guys seem to believe there are better ways to do it and you’re in the enviable position to be right there and able to do it. Strange that you’re backing away.

It's clear you just want to prove you actually know something that I don't, and if I answer your question simply it's about "taking things literally". If you wanted to know what cover we provide ask that then.

You are the one that made a silly suggestion to sound smug about disrupting a market as if it would be easy, and then list all the reasons why is unlikely to succeed, and accuse me of backing away?

Killboy said:

Just how do you imagine I'm confusing actuaries with underwriters?

It's clear you just want to prove you actually know something that I don't, and if I answer your question simply it's about "taking things literally". If you wanted to know what cover we provide ask that then.

You are the one that made a silly suggestion to sound smug about disrupting a market as if it would be easy, and then list all the reasons why is unlikely to succeed, and accuse me of backing away?

Underwriters turn risk models into price, actuaries create the risk profiles. You quite clearly state (quoted below) that you create the pricing. It's clear you just want to prove you actually know something that I don't, and if I answer your question simply it's about "taking things literally". If you wanted to know what cover we provide ask that then.

You are the one that made a silly suggestion to sound smug about disrupting a market as if it would be easy, and then list all the reasons why is unlikely to succeed, and accuse me of backing away?

I don’t know anything that you don’t. You claim to be closer than all of this than I have ever claimed to be. I am a layman, you profess to be the expert, so share your expertise, instead of acting like you know something we don’t.

My challenge was around you being on the side of demanding change, when you are s]close enough to those making the current decisions to drive that change. I’m not. I own properties and used to be a co-owner of a few restaurants.

Killboy said:

There were loads of people with knowledge that used to post on these subjects. But there is a reason they don't bother. FWIW, my teams write code that calculate premiums, just for aircraft and marine assets.

I've suggested that car premium calculations could do with a bit of transparency, but Twig has said its like their KFC secret spices and should be kept secret.

Now we're talking about mpg too. Lol.

I've suggested that car premium calculations could do with a bit of transparency, but Twig has said its like their KFC secret spices and should be kept secret.

Now we're talking about mpg too. Lol.

LF5335 said:

Killboy said:

Just how do you imagine I'm confusing actuaries with underwriters?

It's clear you just want to prove you actually know something that I don't, and if I answer your question simply it's about "taking things literally". If you wanted to know what cover we provide ask that then.

You are the one that made a silly suggestion to sound smug about disrupting a market as if it would be easy, and then list all the reasons why is unlikely to succeed, and accuse me of backing away?

Underwriters turn risk models into price, actuaries create the risk profiles. You quite clearly state (quoted below) that you create the pricing. It's clear you just want to prove you actually know something that I don't, and if I answer your question simply it's about "taking things literally". If you wanted to know what cover we provide ask that then.

You are the one that made a silly suggestion to sound smug about disrupting a market as if it would be easy, and then list all the reasons why is unlikely to succeed, and accuse me of backing away?

I don’t know anything that you don’t. You claim to be closer than all of this than I have ever claimed to be. I am a layman, you profess to be the expert, so share your expertise, instead of acting like you know something we don’t.

My challenge was around you being on the side of demanding change, when you are s]close enough to those making the current decisions to drive that change. I’m not. I own properties and used to be a co-owner of a few restaurants.

Killboy said:

There were loads of people with knowledge that used to post on these subjects. But there is a reason they don't bother. FWIW, my teams write code that calculate premiums, just for aircraft and marine assets.

I've suggested that car premium calculations could do with a bit of transparency, but Twig has said its like their KFC secret spices and should be kept secret.

Now we're talking about mpg too. Lol.

I've suggested that car premium calculations could do with a bit of transparency, but Twig has said its like their KFC secret spices and should be kept secret.

Now we're talking about mpg too. Lol.

I don't understand the UKs personal insurance market. Some things just do not make sense and explanations here are clearly off the mark. For example, Twig with some authority said:

TwigtheWonderkid said:

People who request TPF&T cover end up costing the insurers more money than those who request comp. Most people want comp. In most cases, those actively looking for tpf&t are likely to be the poorest motorists. They are more likely to default on instalments thus costing the insurer more in admin.

Is that true? Well, for one insurance premiums are annualised, and if you look under the hood of what monthly instalments are its usually a credit agreement with a (usually/always?) 3rd party. Take note of the T&Cs the next time. So the insurer gets paid, the 3rd party makes some cash, and what actually happens when customers default?Then what is the relationship with the broker and the underwriter? Its pretty clear when you are on the phone that they put out the details for underwriters to price. At least in the bike world in London there were only 2 underwriters (now possibly 1) that did multi bike policies. If that's true, does the broker simply add a percentage on top? And why do the prices then occasionally vary so much? Do the brokers have deals for specific markets with underwriters?

I could go on for a lot that really doesn't make sense. So much so I actually want to know if there is a legal requirement or reason for some of it. Lets not even start on NCBs.

I've just had the joy of trying to insure 3 "high risk" bikes in central London, My car is £1400 odd - whatever - its a "nice" car on the street, I'll live with that even though its 40% more than last year. The bikes went from £1200 to £2800. Try discussing that? So I didn't renew - and suddenly come this month I got a policy for £900? Why? Did claims drop in 3 month in my area that much? Is part of the calculations - well, what else are you going to do?

The saving grace is (usually) when enough price gouging happens you end up with a regulator stepping in, and I think its high time. I'm not claiming to know anything, but these

I’m not quoting the whole thing, but one thing definitely stands out. You claim the following:

Your personal circumstances are just those, personal. Some of the personal stuff matters, some doesn’t. Why don’t you ask your motorbike broker to explain it more.

As for the rest of your stuff, I’ll take it that you know your stuff on those policies, but they’re not exactly related to each other in terms of what they’re covering. Nor does it follow that it relates in any way to this, and you’ve even written that yourself.

KillBoy said:

I don't understand the UKs personal insurance market. Some things just do not make sense and explanations here are clearly off the mark. For example, Twig with some authority said:

Surely you can see the problem with that statement. If you don’t understand it, surely you can’t state things are wide of the mark. You’ve been vocal on whatever Twig has said as being incorrect. You suggested dmy explanation of the pricing delta in TPF&T / FC was incorrect amd did so with authority. Now you say you don’t understand the market. Your personal circumstances are just those, personal. Some of the personal stuff matters, some doesn’t. Why don’t you ask your motorbike broker to explain it more.

As for the rest of your stuff, I’ll take it that you know your stuff on those policies, but they’re not exactly related to each other in terms of what they’re covering. Nor does it follow that it relates in any way to this, and you’ve even written that yourself.

LF5335 said:

I’m not quoting the whole thing, but one thing definitely stands out. You claim the following:

Your personal circumstances are just those, personal. Some of the personal stuff matters, some doesn’t. Why don’t you ask your motorbike broker to explain it more.

As for the rest of your stuff, I’ll take it that you know your stuff on those policies, but they’re not exactly related to each other in terms of what they’re covering. Nor does it follow that it relates in any way to this, and you’ve even written that yourself.

I've asked Twig if they are facts, and he said and I quote "They're possible suggestions". So I think I'll file these "suggestions" in the bin. I'll gladly listen all ears to anyone that actually knows the industry.KillBoy said:

I don't understand the UKs personal insurance market. Some things just do not make sense and explanations here are clearly off the mark. For example, Twig with some authority said:

Surely you can see the problem with that statement. If you don’t understand it, surely you can’t state things are wide of the mark. You’ve been vocal on whatever Twig has said as being incorrect. You suggested dmy explanation of the pricing delta in TPF&T / FC was incorrect amd did so with authority. Now you say you don’t understand the market. Your personal circumstances are just those, personal. Some of the personal stuff matters, some doesn’t. Why don’t you ask your motorbike broker to explain it more.

As for the rest of your stuff, I’ll take it that you know your stuff on those policies, but they’re not exactly related to each other in terms of what they’re covering. Nor does it follow that it relates in any way to this, and you’ve even written that yourself.

I've had long conversations with my broker. They can't tell me why those prices were coming back like they were either. Unfortunately they have grown a lot and sadly as is the norm with growth don't do much bespoke stuff anymore.

Killboy said:

I've asked Twig if they are facts, and he said and I quote "They're possible suggestions". So I think I'll file these "suggestions" in the bin. I'll gladly listen all ears to anyone that actually knows the industry.

OK let's clarify. For 42 years up until 2021, I worked in various rolls that, if not within the industry, were closely involved with the industry. I had at least one meeting a fortnight with insurers at a high level, I attended court cases, I helped write fleet policy wording. I argued claim settlements. I attended insurance conferences galore. I was responsible for placing the insurance for around 75,000 vehicles, cars, vans and lorries, with the odd motorcycle thrown in. And negotiating pricing. In many ways I knew more about motor insurance than many in the industry, as I was getting knowledge from maybe a dozen insurers, whereas an employee gets info from just one. When I was asked "if they were facts" and I replied "possible suggestions", I meant for the particular case we were discussing, where someone had been given a lower quote for comp than tpf&t on a particular case. Of course I have no idea why that particular insurer came up with the pricing they did on that occasion. The only thing I can state as fact is that it wasn't done out of spite. It was done for good reason by that insurer. The possible suggestions I made are all factual reasons why insurers don't want tpf&t business, or price it so highly. I don't know which or if any of them applied in this specific case.

None of that gives me a monopoly on being right, but it probably means my thoughts are not just wild stabs in the dark. Although no one is obligated to listen to them or believe them. I've asked eHonda on previous threads about his industry knowledge, as he seems to be such an expert, but i've never had a response,

Edited by TwigtheWonderkid on Friday 22 March 21:51

TwigtheWonderkid said:

OK let's clarify. For 42 years up until 2021, I worked in various rolls that, if not within the industry, were closely involved with the industry. I had at least one meeting a fortnight with insurers at a high level, I attended court cases, I helped write fleet policy wording. I argued claim settlements. I attended insurance conferences galore. I was responsible for placing the insurance for around 75,000 vehicles, cars, vans and lorries, with the odd motorcycle thrown in. And negotiating pricing. In many ways I knew more about motor insurance than many in the industry, as I was getting knowledge from maybe a dozen insurers, whereas an employee gets info from just one.

Did you do them 1 by 1? Because if you're talking fleets then you're doing what we do, and it's a bit different as I'm sure you are aware.TwigtheWonderkid said:

When I was asked "if they were facts" and I replied "possible suggestions", I meant for the particular case we were discussing, where someone had been given a lower quote for comp than tpf&t on a particular case. Of course I have no idea why that particular insurer came up with the pricing they did on that occasion. The only thing I can state as fact is that it wasn't done out of spite. It was done for good reason by that insurer. The possible suggestions I made are all factual reasons why insurers don't want tpf&t business, or price it so highly. I don't know which or if any of them applied in this specific case.

We can agree that insurers will quote high for businesses they don't want. It's not necessarily to do with risk. I think it's completely valid for 40%+ raises in prices to raise questions. There may be valid answers, but a lot of it seems to their own making.

TwigtheWonderkid said:

OK let's clarify. For 42 years up until 2021, I worked in various rolls that, if not within the industry, were closely involved with the industry. I had at least one meeting a fortnight with insurers at a high level, I attended court cases, I helped write fleet policy wording. I argued claim settlements. I attended insurance conferences galore. I was responsible for placing the insurance for around 75,000 vehicles, cars, vans and lorries, with the odd motorcycle thrown in. And negotiating pricing. In many ways I knew more about motor insurance than many in the industry, as I was getting knowledge from maybe a dozen insurers, whereas an employee gets info from just one.

When I was asked "if they were facts" and I replied "possible suggestions", I meant for the particular case we were discussing, where someone had been given a lower quote for comp than tpf&t on a particular case. Of course I have no idea why that particular insurer came up with the pricing they did on that occasion. The only thing I can state as fact is that it wasn't done out of spite. It was done for good reason by that insurer. The possible suggestions I made are all factual reasons why insurers don't want tpf&t business, or price it so highly. I don't know which or if any of them applied in this specific case.

None of that gives me a monopoly on being right, but it probably means my thoughts are not just wild stabs in the dark. Although no one is obligated to listen to them or believe them. I've asked eHonda on previous threads about his industry knowledge, as he seems to be such an expert, but i've never had a response,

You've had responses from me you just don't like them.When I was asked "if they were facts" and I replied "possible suggestions", I meant for the particular case we were discussing, where someone had been given a lower quote for comp than tpf&t on a particular case. Of course I have no idea why that particular insurer came up with the pricing they did on that occasion. The only thing I can state as fact is that it wasn't done out of spite. It was done for good reason by that insurer. The possible suggestions I made are all factual reasons why insurers don't want tpf&t business, or price it so highly. I don't know which or if any of them applied in this specific case.

None of that gives me a monopoly on being right, but it probably means my thoughts are not just wild stabs in the dark. Although no one is obligated to listen to them or believe them. I've asked eHonda on previous threads about his industry knowledge, as he seems to be such an expert, but i've never had a response,

Edited by TwigtheWonderkid on Friday 22 March 21:51

I don't discuss my personal circumstances on here.

Facts are facts it doesn't matter who they come from.

I have told you that the situation of fully comp consistently costing more is a situation fairly unique to the UK

If this was untrue it would be very easy to disprove.

But it it is true it completely undermines your claims because they are very generic points that would apply in almost every country.

I have searched and I have not found a single other country with the same situation as ours.

You won't address this, instead you attack me as the source.

If I start disclosing details of my personal circumstances no doubt you will continue to try and discredit me and it becomes even more personal which is why I choose never to discuss them.

These are not small amounts of money

There may have once been a time where some insurers were poorly accounting for some of the previously mentioned factors and genuinely pricing slightly higher based on cost of cover, but that ship has sailed.

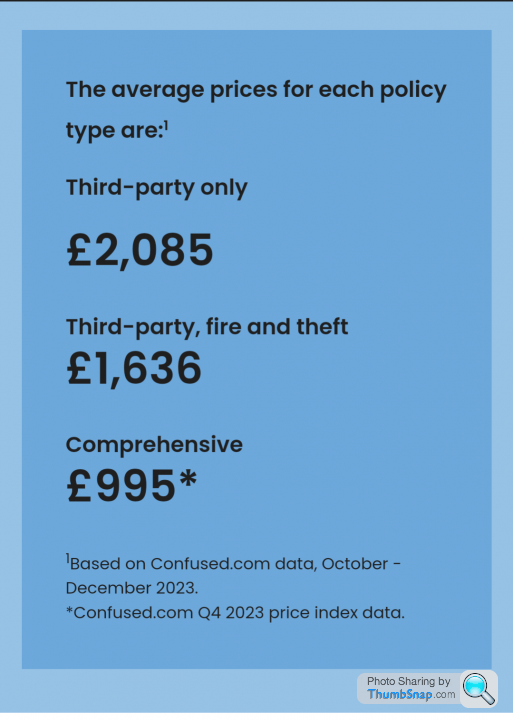

3rd party only and tpf&t are dead products and these quotes throw away quotes purely to catch out those who aren't aware fully comp be cheaper, if you cannot immediately see that from these figures then nothing is going to sway you from your heavily entrenched views.

e-honda said:

These are not small amounts of money

There may have once been a time where some insurers were poorly accounting for some of the previously mentioned factors and genuinely pricing slightly higher based on cost of cover, but that ship has sailed.

3rd party only and tpf&t are dead products and these quotes throw away quotes purely to catch out those who aren't aware fully comp be cheaper, if you cannot immediately see that from these figures then nothing is going to sway you from your heavily entrenched views.

Third party is exactly what the name suggests; only the third-party will be paid out. So I don't understand why your own car or the drivers details affect the price of this insurance. Third-party cover should be a fixed price per year, and people should therefore be incentivised to purchase fire and theft or comprehensive as an addition.

aturnick54 said:

What I fail to understand is, why is comprehensive usually the cheapest? Surely a higher level of cover should cost more?

Third party is exactly what the name suggests; only the third-party will be paid out. So I don't understand why your own car or the drivers details affect the price of this insurance.

You don't understand why a teenager with a speeding offence in a highly modified Subaru WRX is more likely to cause damage to a third party than a 50 y/o with a clean record in a Honda Jazz? If that's true, I don't think it's worth me explaining it to you.Third party is exactly what the name suggests; only the third-party will be paid out. So I don't understand why your own car or the drivers details affect the price of this insurance.

e-honda said:

You've had responses from me you just don't like them.

I don't discuss my personal circumstances on here.

I'm hardly asking for intimate details of your sex life. I don't even want to know what you do for a living. Just to tell us all what your industry experience is. I mean, you should be able to say "22 years at a senior management level" or whatever, without giving too much away. Because as it is, one might almost believe you have none at all. I don't discuss my personal circumstances on here.

Killboy said:

And forget TPF&T, how about just third party only? Cut out all the risk of car thefts, fires etc, and suddenly no one wants the business.

Disagree with the below all you like, but it is the correct answer. Ask around with your peers who do motor insurance. If the disagree, then post exactly what reasons they give. LF5335 said:

If a TPF&T customer crashes into another car and it’s their fault, what reason or incentive do they have to report the accident to their own insurers? Insurers can mitigate cost when they know about claims early, they can’t when they find out about it weeks, moths, or even years later.

If a FC customer has exactly the same fault accident they probably will contact the same insurer much earlier as they want their own car repairing. So the insurer now gets a chance to minimise the cost. They might only save a few thousand per claim, but it will be evident in their statistical experience that this is the case.

Logical? Yep

Absolute? Yep

If a FC customer has exactly the same fault accident they probably will contact the same insurer much earlier as they want their own car repairing. So the insurer now gets a chance to minimise the cost. They might only save a few thousand per claim, but it will be evident in their statistical experience that this is the case.

Logical? Yep

Absolute? Yep

e-honda said:

These are not small amounts of money

There may have once been a time where some insurers were poorly accounting for some of the previously mentioned factors and genuinely pricing slightly higher based on cost of cover, but that ship has sailed.

3rd party only and tpf&t are dead products and these quotes throw away quotes purely to catch out those who aren't aware fully comp be cheaper, if you cannot immediately see that from these figures then nothing is going to sway you from your heavily entrenched views.

LF5335 said:

If a TPF&T customer crashes into another car and it’s their fault, what reason or incentive do they have to report the accident to their own insurers? Insurers can mitigate cost when they know about claims early, they can’t when they find out about it weeks, moths, or even years later.

If a FC customer has exactly the same fault accident they probably will contact the same insurer much earlier as they want their own car repairing. So the insurer now gets a chance to minimise the cost. They might only save a few thousand per claim, but it will be evident in their statistical experience that this is the case.

Logical? Yep

Absolute? Yep

If a FC customer has exactly the same fault accident they probably will contact the same insurer much earlier as they want their own car repairing. So the insurer now gets a chance to minimise the cost. They might only save a few thousand per claim, but it will be evident in their statistical experience that this is the case.

Logical? Yep

Absolute? Yep

aturnick54 said:

What I fail to understand is, why is comprehensive usually the cheapest? Surely a higher level of cover should cost more?

Third party is exactly what the name suggests; only the third-party will be paid out. So I don't understand why your own car or the drivers details affect the price of this insurance. Third-party cover should be a fixed price per year, and people should therefore be incentivised to purchase fire and theft or comprehensive as an addition.

As I’ve posted several dozen times now on this thread:Third party is exactly what the name suggests; only the third-party will be paid out. So I don't understand why your own car or the drivers details affect the price of this insurance. Third-party cover should be a fixed price per year, and people should therefore be incentivised to purchase fire and theft or comprehensive as an addition.

LF5335 said:

If a TPF&T customer crashes into another car and it’s their fault, what reason or incentive do they have to report the accident to their own insurers? Insurers can mitigate cost when they know about claims early, they can’t when they find out about it weeks, moths, or even years later.

If a FC customer has exactly the same fault accident they probably will contact the same insurer much earlier as they want their own car repairing. So the insurer now gets a chance to minimise the cost. They might only save a few thousand per claim, but it will be evident in their statistical experience that this is the case.

Logical? Yep

Absolute? Yep

If a FC customer has exactly the same fault accident they probably will contact the same insurer much earlier as they want their own car repairing. So the insurer now gets a chance to minimise the cost. They might only save a few thousand per claim, but it will be evident in their statistical experience that this is the case.

Logical? Yep

Absolute? Yep

e-honda said:

You've had responses from me you just don't like them.

I don't discuss my personal circumstances on here.

Facts are facts it doesn't matter who they come from.

I have told you that the situation of fully comp consistently costing more is a situation fairly unique to the UK

If this was untrue it would be very easy to disprove.

But it it is true it completely undermines your claims because they are very generic points that would apply in almost every country.

I have searched and I have not found a single other country with the same situation as ours

You won't address this, instead you attack me as the source.

If I start disclosing details of my personal circumstances no doubt you will continue to try and discredit me and it becomes even more personal which is why I choose never to discuss them.

I have answered this previously. You refuse to read the answer. Here it is again:I don't discuss my personal circumstances on here.

Facts are facts it doesn't matter who they come from.

I have told you that the situation of fully comp consistently costing more is a situation fairly unique to the UK

If this was untrue it would be very easy to disprove.

But it it is true it completely undermines your claims because they are very generic points that would apply in almost every country.

I have searched and I have not found a single other country with the same situation as ours

You won't address this, instead you attack me as the source.

If I start disclosing details of my personal circumstances no doubt you will continue to try and discredit me and it becomes even more personal which is why I choose never to discuss them.

LF5335 said:

Insurance is heavily impacted by the legal framework of each country. Does each country have exactly the same legal structure, laws and general tort as the UK?

Gassing Station | General Gassing | Top of Page | What's New | My Stuff