S&P500 at record highs - time to stay in or pull out?

Discussion

ooid said:

Derek Chevalier said:

Surely it is simpler to diversify, and if you are going to hedge, you do it when protection is cheap?

https://www.aqr.com/-/media/AQR/Documents/Insights...

It's true but a bit old document, I think Cliff's ideas about Tail Risk also evolved since than. It is a also a bit single dimension, so does not include the fact on levered positions (on shorts). It is quite complex, advanced not easy as you say but highly effective.https://www.aqr.com/-/media/AQR/Documents/Insights...

This is an interesting one, though it is fairly new:

https://funds.alphaarchitect.com/caos/

"Maintains a strategic allocation to protective puts on the S&P 500."

Why would you focus on just this particular part of the market, other than to cater for recency bias?

Phooey said:

Hedge funds have been de-risking for a while. Reversion to the mean incoming, maybe.

The acute de-grossing over the last couple of weeks, particularly among equity pods at the multi-strat HFs, has been brutal. I'm thankfully out of the game now but still in touch enough to know of several folks who've been stopped out and sent packing this last week or so. Essentially the strategies have become way too crowded; everyone's had the same trades on at the same time and likely all using leverage provided by the same PBs (which is the scary bit when you really think about it). Then when the inevitable unwind comes, it's seriously ugly.IMO it demonstrates a bit of a vulnerability in the supposedly unassailable multi-strat model - or at least suggests it's at/near capacity for now - but I'm sure they'll go on, hire a load of new PMs who'll all gross up in unison and at some point we'll get to see this movie again...

I have seen posited online that Trump knows a recession is coming, potentially of epic proportions:

https://www.youtube.com/watch?v=TyJasQvlXQg

I have also seen discussion that he is looking to revalue the Fort Knox gold (if it exists ) to help fix the debt issues, and that it looks like large amounts of gold are being shipped to the US recently (either to put the gold back into Fort Knox or to add to it).

) to help fix the debt issues, and that it looks like large amounts of gold are being shipped to the US recently (either to put the gold back into Fort Knox or to add to it).

My tin foil hat wonders if he is expecting the market to play out, the everything bubble to pop, and then he will be able to shore-up / recover with gold and more sustainable market practices - ideally in advance of the BRICS gold-backed Unit currency announcements.

https://www.youtube.com/watch?v=TyJasQvlXQg

I have also seen discussion that he is looking to revalue the Fort Knox gold (if it exists

) to help fix the debt issues, and that it looks like large amounts of gold are being shipped to the US recently (either to put the gold back into Fort Knox or to add to it).My tin foil hat wonders if he is expecting the market to play out, the everything bubble to pop, and then he will be able to shore-up / recover with gold and more sustainable market practices - ideally in advance of the BRICS gold-backed Unit currency announcements.

Derek Chevalier said:

I got this far

"Maintains a strategic allocation to protective puts on the S&P 500."

Why would you focus on just this particular part of the market, other than to cater for recency bias?

I'm not a full advocate of CAOS by the way, but big respect for the founders. They are one of the leading academics turned practitioners in financial engineering. In terms of CAOS, or (any similar tail risk, though not many available publicly or ETF form), I think the point is about not knowing the unknown which are extremely rare downturns or crashes. It is not a benchmark beating long term strategy but an insurance. For me what is more interesting, when crashes happen, if you have insurance in place to protect your wealth and if enough capital is available invest in the markets as usual. For most of us, monthly, quarterly or annually accumulating when young, none of these downturns are issue(or simply noise) as we won't be withdrawing anytime soon!!"Maintains a strategic allocation to protective puts on the S&P 500."

Why would you focus on just this particular part of the market, other than to cater for recency bias?

Edited by ooid on Saturday 15th March 15:37

Phooey said:

The consumer is 70% of the economy. Aside from the uncertainty (which markets hate), the growth expectations of the S&P 500 is starting to weigh heavy on reality. Expectations among retail investors is (or was) too high. Hedge funds have been de-risking for a while. Reversion to the mean incoming, maybe.

Yep. I do wonder if the cost if leverage is also increasing given the volatility (and scarcity / reduction in value of collateral). Whilst this is probably a short term issue and a consideration for those with shorter investment horizons, I think the risk equation has moved towards the spicy end of the spectrum. The poster who mentioned devaluing gold reserves is referencing something that has been doing the rounds given it appears to marked to current market (although it's a bit of a drop on the ocean compared to the debt pile / refi needs). An interesting problem for Trump will be what the individual states dom 25% of US govt dent is held by the states, if I was California etc and feeling Trumps wrath I might start to evaluate how helpful I'd be on that front. Although that's up there on the conspiracy theory line.

ooid said:

Are you looking at Tail Risk ETFs recently?

Sorry, I miised this post.Not as yet, I use futures and put spreads when applicable, I like the liquidity and convention that I am used to? I will have a look at them, initially it could be an expensive way to buy out of the money put spreads, but I haven't gone into them enough to form an opinion?

There was a lot of short covering in Spoos and Vix last week, anything notable on tail risk ETF'?

ooid said:

I'm not a full advocate of CAOS by the way, but big respect for the founders. They are one of the leading academics turned practitioners in financial engineering. In terms of CAOS, or (any similar tail risk, though not many available publicly or ETF form), I think the point is about not knowing the unknown which are extremely rare downturns or crashes. It is not a benchmark beating long term strategy but an insurance. For me what is more interesting, when crashes happen, if you have insurance in place to protect your wealth and if enough capital is available invest in the markets as usual. For most of us, monthly, quarterly or annually accumulating when young, none of these downturns are issue(or simply noise) as we won't be withdrawing anytime soon!!

Probably also worth noting that according to their own literature, they didn't achieve their primary objective during the last three downturns.Edited by ooid on Saturday 15th March 15:37

https://funds.alphaarchitect.com/wp-content/upload...

ooid said:

I think the point is about not knowing the unknown which are extremely rare downturns or crashes.

While we may not know when crashes might happen, it's pretty safe to assume that something will happen during a multi-decade retirement. The good news is that we have over a century of historical market data to evaluate how a retirement strategy will perform when things go wrong. And when you undertake this analysis, you realise how bad things have been historically, and tend to ignore noise. (Persistent high inflation is the biggest worry, not market, IMO.)

The challenge with evaluating whether alternative approaches may or may not work is that we tend not to have sufficient historical data to make a call either way. For example, if I added this fund to an existing portfolio, how would it have impacted the sustainable withdrawal rate for someone retiring in the late 60s.

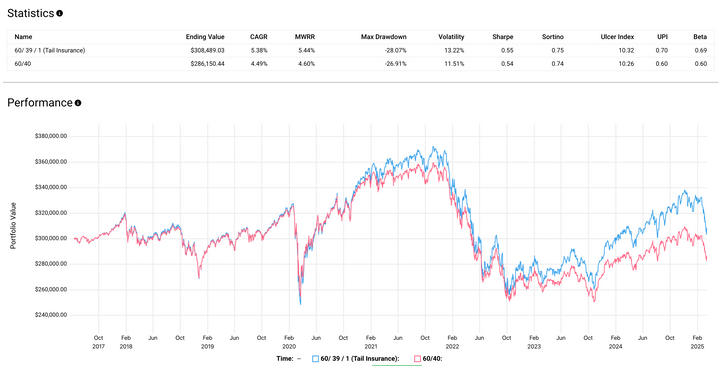

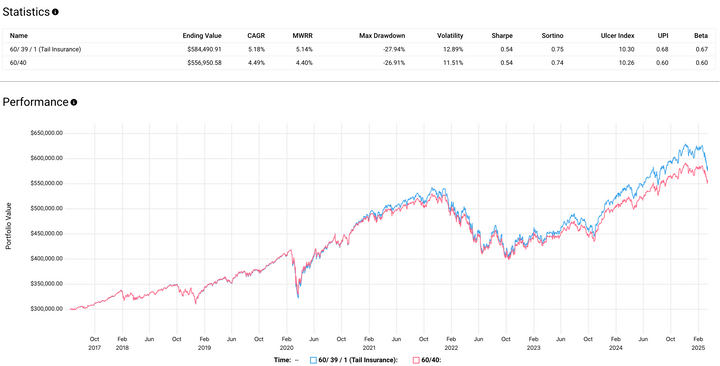

I actually created a very dummy or simplistic demonstration due to time-series limitation, so have two examples, accumulation and decumulation but same value. Starting with 300k, (annual 5% withdrawl) but using that monthly. Also the same for accumulation, not touching the capital but monthly positive cash flow.

60 / 40 and 60 / 39 / 1(Tail Hedge)

I have used one of the oldest ones (Cambria Tail Risk, not good for interest rate rise specifically), my point though, there has never been a decent ETF product to use this sort of insurance for a tiny allocation to protect overall wealth. This has been done by quite advanced dynamic hedging methods in the past, by again allocating perhaps 1% of the portfolio for actively hedging (there is a drag, but when extreme events happen pay-off is good it could simply be an insurance.)

60 / 40 and 60 / 39 / 1(Tail Hedge)

I have used one of the oldest ones (Cambria Tail Risk, not good for interest rate rise specifically), my point though, there has never been a decent ETF product to use this sort of insurance for a tiny allocation to protect overall wealth. This has been done by quite advanced dynamic hedging methods in the past, by again allocating perhaps 1% of the portfolio for actively hedging (there is a drag, but when extreme events happen pay-off is good it could simply be an insurance.)

Derek Chevalier said:

ooid said:

I think the point is about not knowing the unknown which are extremely rare downturns or crashes.

While we may not know when crashes might happen, it's pretty safe to assume that something will happen during a multi-decade retirement. The good news is that we have over a century of historical market data to evaluate how a retirement strategy will perform when things go wrong. And when you undertake this analysis, you realise how bad things have been historically, and tend to ignore noise. (Persistent high inflation is the biggest worry, not market, IMO.)

The challenge with evaluating whether alternative approaches may or may not work is that we tend not to have sufficient historical data to make a call either way. For example, if I added this fund to an existing portfolio, how would it have impacted the sustainable withdrawal rate for someone retiring in the late 60s.

https://www.morningstar.com/economy/what-weve-lear...

"And the covid crash of March 2020 was actually the least painful of these 19 crashes, due to the quick subsequent recovery"

Derek Chevalier said:

Talking of historical crashes

https://www.morningstar.com/economy/what-weve-lear...

"And the covid crash of March 2020 was actually the least painful of these 19 crashes, due to the quick subsequent recovery"

Quantative easing and subsequent expansion of Govt money supply and balance sheet like never before probably explains that?https://www.morningstar.com/economy/what-weve-lear...

"And the covid crash of March 2020 was actually the least painful of these 19 crashes, due to the quick subsequent recovery"

clubsport said:

Quantative easing and subsequent expansion of Govt money supply and balance sheet like never before probably explains that?

well if it does explain that ( and my view is that it played a huge part, along with the fact that markets dip based on sentiment/news and then often rebound) - then we're likely in for more of the same as Gov's around the world loosen their purse strings yet again. If that does come to pass/contine, then there should be a fair amount of money looking for a 'new home' and a bullish attitude towards perceived 'risk on' assets.IMO from the current position and looking at Trump's capriciousness the best thing to expect going forward from here is volatility.

If you don't have the stomach for volatility then it's time to be rebalancing towards cash and/or bonds.

Talking of bonds, in which I took a complete spanking, the MD of PIMCO was interviewed today saying that "if you go back to 2019 absolutely nobody was predicting that yields would recover from negative (real) to 2% (real)". You're darned right I wasn't! He also takes the view that stock valuations remain "full" right now even after the recent downturn.

If you don't have the stomach for volatility then it's time to be rebalancing towards cash and/or bonds.

Talking of bonds, in which I took a complete spanking, the MD of PIMCO was interviewed today saying that "if you go back to 2019 absolutely nobody was predicting that yields would recover from negative (real) to 2% (real)". You're darned right I wasn't! He also takes the view that stock valuations remain "full" right now even after the recent downturn.

okgo said:

It really isn’t scary. It’s now 6% down off peak. Or if you wish to go back, the price it was in November. 10% up YOY and only down 1.9% year to date.

Utter storm in a teacup.

It is worrying how many people think this is a big event. 20-30% in a correction isn't unheard of. Utter storm in a teacup.

StoutBench said:

okgo said:

It really isn’t scary. It’s now 6% down off peak. Or if you wish to go back, the price it was in November. 10% up YOY and only down 1.9% year to date.

Utter storm in a teacup.

It is worrying how many people think this is a big event. 20-30% in a correction isn't unheard of. Utter storm in a teacup.

The market has a 10% draw down every 14 months or so.

Its interesting that the last one was only back in August when the yen carry trade went pointy side up.

Part of me thinks this is not over yet, but it would only take some good news and we could have 2 or 3 good back to back days and we would be back at ATH.

IIRC the move from the low the big boys look for is a 1.25% day with follow through. Today currently +1.5% so tomorrow might be interesting too.

The FED slowing their QT is probably another big boost too.

We will see.

Gassing Station | Finance | Top of Page | What's New | My Stuff