Insurance no claims (legal?) conundrum

Discussion

Slow said:

Ive had 2 insurance companies never ask me for proof of no claims so you could get lucky with that.

One even gave me a second set of no claims bonuses 2 years later despite my policy being not renewed and the car sold on. Had 5 and 4 years no claims after driving for 5 years.

You may find they are in fact different brands being underwritten by the same company. So they already have your no claims details.One even gave me a second set of no claims bonuses 2 years later despite my policy being not renewed and the car sold on. Had 5 and 4 years no claims after driving for 5 years.

You might well be better sticking with coop. When you fill in any other insurance application , after you have filled in your 3 year NCB, another box will ask if you've had any claims in the last X years, which will have the biggest impact on your policy.

I'm finding being 50, NCB seems to barely make any difference.

I'm finding being 50, NCB seems to barely make any difference.

eshroom said:

Yep, I get that, proving it is a separate thing altogether. Just interested to know whether I'd be breaking their terms by saying I had 8 years NCD, if under their terms my 10 years minus 2 for the accident leaves me with 8.

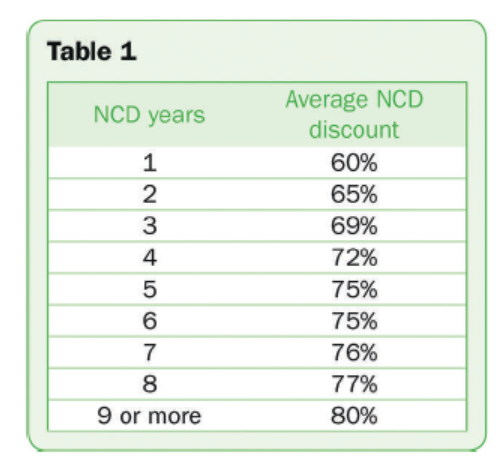

Got the renewal the other day for wife's car with LV= and they do NCB up to 9 yrs. If you've got 9+yrs then an accident drops the NCD at renewal to 4yrs. If you've got 5 to 8yrs then it drops to 3yrs.I have to say I've never thought about the percentages before - the renewal doc has a table of "average" NCD which has surprising (to me) figures:

LeoSayer said:

Is there a material difference in policy cost between 3 and 8 years NCB?

For me about 25%.RogerDodger said:

You might well be better sticking with coop.

I tried, I accepted their renewal, then they sent a letter on 27th of December asking for me to verify my license (photo and DVLA authorisation), I didn't receive this as was on holiday so they cancelled the policy on 6th January. Livid. I sent this into them yesterday but they said they would have to requote rather than offer the renewal price, and will take 3-5 working days to do so. Lucky car is off the road, and I guess I'll be using the bus for a few days.Edited by eshroom on Tuesday 14th January 11:36

eshroom said:

Yep, I get that, proving it is a separate thing altogether. Just interested to know whether I'd be breaking their terms by saying I had 8 years NCD, if under their terms my 10 years minus 2 for the accident leaves me with 8.

Doesn't work like that.I got my motorbike stolen in 2014 - 22 years documented no claims (it was actually 29 but I never got it documented more than 5 originally). It gets knocked back to 3.

I wouldn't worry about protected no claims - it only applies to your existing insurer and they will still load the premium that you are having the NCD applied to anyway.

Dog Star said:

I wouldn't worry about protected no claims - it only applies to your existing insurer and they will still load the premium that you are having the NCD applied to anyway.

No it doesn't, your NCD is protected, so if you leave company A you had the claim with and go to Company B, you can present Company B your full NCD as you have had it protected by Company A, thats the whole point, anything other than that would be anti-competitive and go against regs.Dog Star said:

I wouldn't worry about protected no claims - it only applies to your existing insurer and they will still load the premium that you are having the NCD applied to anyway.

They don't load it any extra because you have protected ncb. So protected ncb will still mean you'll be paying less following a claim. Edited by TwigtheWonderkid on Tuesday 14th January 16:33

eshroom said:

LeoSayer said:

Is there a material difference in policy cost between 3 and 8 years NCB?

For me about 25%.RogerDodger said:

You might well be better sticking with coop.

I tried, I accepted their renewal, then they sent a letter on 27th of December asking for me to verify my license (photo and DVLA authorisation), I didn't receive this as was on holiday so they cancelled the policy on 6th January. Livid. I sent this into them yesterday but they said they would have to requote rather than offer the renewal price, and will take 3-5 working days to do so. Lucky car is off the road, and I guess I'll be using the bus for a few days.Edited by eshroom on Tuesday 14th January 11:36

Rick101 said:

10 yrs NCB minus two = 3 yrs NCB.

The insurance industry... the only place where that maths makes sense!I've never really thought about it but if you have 8 years NCB and take out a policy with an insurer that only recognises five, then move provider at the end of your policy (without making any claims), will they only give you proof of 5 years NCB? Thus loosing you 3 years NCB for no reason, surely not?

Sheepshanks said:

I have to say I've never thought about the percentages before - the renewal doc has a table of "average" NCD which has surprising (to me) figures:

Has anyone ever found these discounts to reflect reality?I have a shed V70. With nine plus years no claims it was £270 to insure.

When I purchased a replacement vehicle I kept the V70 and started a new policy for it with zero no claims, it now costs £320.

gazza285 said:

Has anyone ever found these discounts to reflect reality?

I have a shed V70. With nine plus years no claims it was £270 to insure.

When I purchased a replacement vehicle I kept the V70 and started a new policy for it with zero no claims, it now costs £320.

No they're utter bI have a shed V70. With nine plus years no claims it was £270 to insure.

When I purchased a replacement vehicle I kept the V70 and started a new policy for it with zero no claims, it now costs £320.

ks, just like the entire insurance industry.

ks, just like the entire insurance industry.And you can confirm this by insuring a second car with no NCB , shop around, and you'll get the same discount as if you did have NCB.

I used to make effort to keep my 20+ years of NCB documented, but now, with 9 year caps etc I just don't sweat it. Clearly I'm low risk and get insurance quotes accordingly.

I used to make effort to keep my 20+ years of NCB documented, but now, with 9 year caps etc I just don't sweat it. Clearly I'm low risk and get insurance quotes accordingly.

Sheepshanks said:

gazza285 said:

Has anyone ever found these discounts to reflect reality?

They would mean the base premium on wife’s Tiguan was £2K, which I hope is unlikely.dibblecorse said:

More likely than you think, I used to work for one of the big providers and you'd be amazed what the base premiums are for at times so fairly standard cars, in many ways the car itself is a very small proportion of the quoting calculation.

Sure, but I meant the base premium for my wife, our address etc etc - simply with no NCD applied.Gassing Station | General Gassing | Top of Page | What's New | My Stuff