Salary sacrifice leasing

Discussion

Indeed, certainly not complaining but do want to ensure it's dealt with as efficiently as possible.

So just getting this straight in my head, if i do nothing that £27.5k is going to add £900 to my pay packet a month (which would cover the cost of our current Tesla 3) but alternatively I could sacrifice £1500 a month on a well equipped Taycan 4S + put a further £800 or so a month into my pension pot?

Seems like a no brainer, even with the EV BIK rising slightly over the next 2 years?

So just getting this straight in my head, if i do nothing that £27.5k is going to add £900 to my pay packet a month (which would cover the cost of our current Tesla 3) but alternatively I could sacrifice £1500 a month on a well equipped Taycan 4S + put a further £800 or so a month into my pension pot?

Seems like a no brainer, even with the EV BIK rising slightly over the next 2 years?

If only a Taycan was on my list.... we now have a £50k list price cap and there is a CO2 cap too, sub 120's from memory..... Our fleet have been bitten so many times by people taking say an E63, having it 18 months, resigning, and leaving them with a car with 2.5 years of lease left which nobody else wants because of the huge BiK implications!

Best I can squeeze is an M3 Long Range - just - in white, no extras! e-Niro is a more practical family hack for us, keep the 992 for weekend kicks.

I cannot answer the VAT thing, and yes its a very very nice problem to have, been there and learnt very very quickly.

My word of caution would be check out the terms of your scheme - if its a traditional company car scheme / allowance (like mine), then great, if leave, I pop the keys in the post and give them the address to come get it. Depending on the animosity I may valet it, but any issues, damage etc (unless I've been negligent) are not my problem.

In your case, what happens if you resign, or worse, things don't work out and you are made redundant - where does the liability for the vehicle then lie? Would the lease in your name and are they just paying it on your behalf?

Last thing you want to be is 1 year into a £1,500 a month Taycan lease and suddenly no income, or even moving to a new employer who does not operate in a similar manner and will not take on the lease and you are now paying a great deal of tax for the next two years!!!!

If its trad company car, and you can effectively bag a Taycan for £600 a month real world, then s t yeah, I'd do it.....

t yeah, I'd do it.....

Best I can squeeze is an M3 Long Range - just - in white, no extras! e-Niro is a more practical family hack for us, keep the 992 for weekend kicks.

I cannot answer the VAT thing, and yes its a very very nice problem to have, been there and learnt very very quickly.

My word of caution would be check out the terms of your scheme - if its a traditional company car scheme / allowance (like mine), then great, if leave, I pop the keys in the post and give them the address to come get it. Depending on the animosity I may valet it, but any issues, damage etc (unless I've been negligent) are not my problem.

In your case, what happens if you resign, or worse, things don't work out and you are made redundant - where does the liability for the vehicle then lie? Would the lease in your name and are they just paying it on your behalf?

Last thing you want to be is 1 year into a £1,500 a month Taycan lease and suddenly no income, or even moving to a new employer who does not operate in a similar manner and will not take on the lease and you are now paying a great deal of tax for the next two years!!!!

If its trad company car, and you can effectively bag a Taycan for £600 a month real world, then s

t yeah, I'd do it.....dgswk said:

If only a Taycan was on my list.... we now have a £50k list price cap and there is a CO2 cap too, sub 120's from memory..... Our fleet have been bitten so many times by people taking say an E63, having it 18 months, resigning, and leaving them with a car with 2.5 years of lease left which nobody else wants because of the huge BiK implications!

Best I can squeeze is an M3 Long Range - just - in white, no extras! e-Niro is a more practical family hack for us, keep the 992 for weekend kicks.

I cannot answer the VAT thing, and yes its a very very nice problem to have, been there and learnt very very quickly.

My word of caution would be check out the terms of your scheme - if its a traditional company car scheme / allowance (like mine), then great, if leave, I pop the keys in the post and give them the address to come get it. Depending on the animosity I may valet it, but any issues, damage etc (unless I've been negligent) are not my problem.

In your case, what happens if you resign, or worse, things don't work out and you are made redundant - where does the liability for the vehicle then lie? Would the lease in your name and are they just paying it on your behalf?

Last thing you want to be is 1 year into a £1,500 a month Taycan lease and suddenly no income, or even moving to a new employer who does not operate in a similar manner and will not take on the lease and you are now paying a great deal of tax for the next two years!!!!

If its trad company car, and you can effectively bag a Taycan for £600 a month real world, then st yeah, I'd do it.....

Agreed. Certainly needs consideration but believe these schemes are linked to the employer who signs the deal and also include early termination cover for resignation/redundancy etc.Best I can squeeze is an M3 Long Range - just - in white, no extras! e-Niro is a more practical family hack for us, keep the 992 for weekend kicks.

I cannot answer the VAT thing, and yes its a very very nice problem to have, been there and learnt very very quickly.

My word of caution would be check out the terms of your scheme - if its a traditional company car scheme / allowance (like mine), then great, if leave, I pop the keys in the post and give them the address to come get it. Depending on the animosity I may valet it, but any issues, damage etc (unless I've been negligent) are not my problem.

In your case, what happens if you resign, or worse, things don't work out and you are made redundant - where does the liability for the vehicle then lie? Would the lease in your name and are they just paying it on your behalf?

Last thing you want to be is 1 year into a £1,500 a month Taycan lease and suddenly no income, or even moving to a new employer who does not operate in a similar manner and will not take on the lease and you are now paying a great deal of tax for the next two years!!!!

If its trad company car, and you can effectively bag a Taycan for £600 a month real world, then s

t yeah, I'd do it.....Certainly what Octopus EV and Leaseplan suggest anyway in my initial research.

Essentially in your situation 40p of take home pay buys you £1 of company car lease.

My first Tesla was a company car and was an eye watering £1400 a month gross inc insurance, servicing (back in the day when it was 12 months and 12k miles), tyres etc and I was doing 30k miles a year - privately I could get the same deal for about £1100 outside the company so you can't always compare. The tax made it still worth being in the company scheme even though the BIK rates at the time were higher than today

So if your company outsources the car scheme to a 3rd party you just need to get a quote because looking up the price and thinking thats what they'll quote you isn't necessarily right, especially if they do an all inclusive expenses like tyres etc. The VAT thing becomes a bit moot until you know how the scheme runs and what the costs are as there are bigger variables, but if the company buys the car then VAT would apply, if they lease then I believe half the VAT can be recovered

Another option which my last employer offered was to allow directors to take more than one company car, I'd probably be doing that today if I still worked for them.

The point about termination costs is a good one, I can't remember the terms where I was but it was a number of months lease costs for every year outstanding if I left with the car. I was expecting EVs to change so I'd only taken it on a 30 month lease so it didn't really hurt.

And finally - I presume this has nothing to do with the NHS. I've heard but can't say I fully understand the NHS problem where salary sacrifice can have pension implications. I presume its some quirk of the NHS final salary scheme, but worth looking into if thats your position.

My first Tesla was a company car and was an eye watering £1400 a month gross inc insurance, servicing (back in the day when it was 12 months and 12k miles), tyres etc and I was doing 30k miles a year - privately I could get the same deal for about £1100 outside the company so you can't always compare. The tax made it still worth being in the company scheme even though the BIK rates at the time were higher than today

So if your company outsources the car scheme to a 3rd party you just need to get a quote because looking up the price and thinking thats what they'll quote you isn't necessarily right, especially if they do an all inclusive expenses like tyres etc. The VAT thing becomes a bit moot until you know how the scheme runs and what the costs are as there are bigger variables, but if the company buys the car then VAT would apply, if they lease then I believe half the VAT can be recovered

Another option which my last employer offered was to allow directors to take more than one company car, I'd probably be doing that today if I still worked for them.

The point about termination costs is a good one, I can't remember the terms where I was but it was a number of months lease costs for every year outstanding if I left with the car. I was expecting EVs to change so I'd only taken it on a 30 month lease so it didn't really hurt.

And finally - I presume this has nothing to do with the NHS. I've heard but can't say I fully understand the NHS problem where salary sacrifice can have pension implications. I presume its some quirk of the NHS final salary scheme, but worth looking into if thats your position.

dgswk said:

Heres Johnny said:

Another option which my last employer offered was to allow directors to take more than one company car, I'd probably be doing that today if I still worked for them.

Two EV's at 0% BiK, wow, that would be nice work if you could get it, matching his and her Taycans

Wouldn't it just. We'd probably end up with same setup we had back at the start of the year pre first lockdown only it would be considerably cheaper.

Anyway, been informed late his afternoon that due to lockdown 2.0 the decision has been made that all promotions and recruitment will be put on hold for at least a month.

My employer has just dropped a 10year max age in 2022, 5 years at 2025 (unless zero emissions), I currently get £6k per year in allowance and obviously run a 57plate shed. Main reason it’s an estate.

Appears I can pay to go up a grade or two which gets me into a Model 3 or Long Range 3 all at £0 BIK.

About to do the numbers but after tax I reckon only have circa £350 a month which when you add very thing up will be less than £350 excluding depreciation.

Looks like a no brainier to loose the £350 and get a fully financed, insured, taxed and maintained Tesla. I would have to live without the boot or potentially wait to see what other manufacturers are bringing out zero emission estates in the next two years.

We have a business mileage cap on the scheme but need to see if there is a private mileage allowance on top. This thread has been very informative.

Appears I can pay to go up a grade or two which gets me into a Model 3 or Long Range 3 all at £0 BIK.

About to do the numbers but after tax I reckon only have circa £350 a month which when you add very thing up will be less than £350 excluding depreciation.

Looks like a no brainier to loose the £350 and get a fully financed, insured, taxed and maintained Tesla. I would have to live without the boot or potentially wait to see what other manufacturers are bringing out zero emission estates in the next two years.

We have a business mileage cap on the scheme but need to see if there is a private mileage allowance on top. This thread has been very informative.

SWoll said:

Thanks for all the responses chaps. TBH I've been so busy and with the new package down to a promotion I'd not given any of this much consideration.

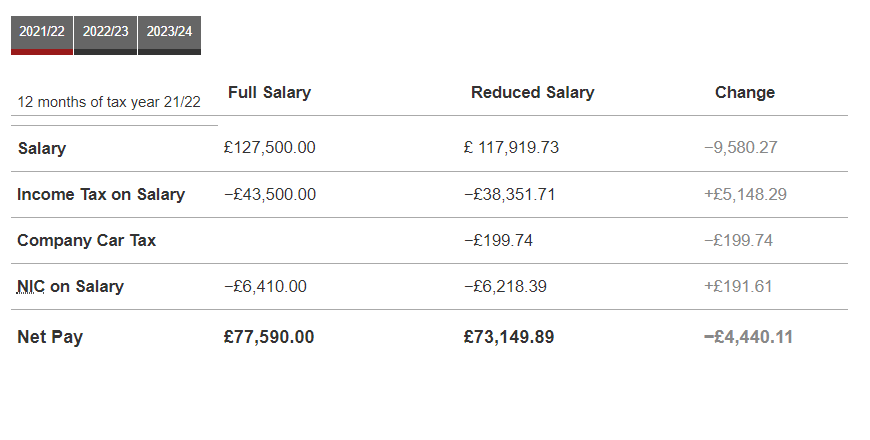

The £127.5 total includes base (£100k), bonus (£20k) and car allowance (£7.5k)

So with my pension contribution levels already high and not really able to increase by much I'm looking at the numbers and thinking that rather than take the massive tax hit I'd be better off sinking as much of that £25k as possible into an EV with things as they stand currently?

Based on the above should I be looking at the cost of Porsche Taycan's on lease and if so do I need to consider the VAT in the total sacrifice cost or would it be considered

Hmm watch out - if the £127.5k is before deducting any pension contributions and you are making high pension contributions then you aren’t at £127.5k at all. I don’t know what you mean by “high pension contributions“ - but if say you are paying say £17.5k pension contributions then you are at £110k not £127.5kThe £127.5 total includes base (£100k), bonus (£20k) and car allowance (£7.5k)

So with my pension contribution levels already high and not really able to increase by much I'm looking at the numbers and thinking that rather than take the massive tax hit I'd be better off sinking as much of that £25k as possible into an EV with things as they stand currently?

Based on the above should I be looking at the cost of Porsche Taycan's on lease and if so do I need to consider the VAT in the total sacrifice cost or would it be considered

Business contract hire means 50% of the VAT is recoverable. A car bought outright by a company cannot have any vat on the purchase price reclaimed, so contract hire brings a possible 8.3% saving (10/120) I would imagine most salary sacrifice schemes will use contract hire

Wondering if someone can answer my question please, as I can't find this on online examples. In this scenario let's say the employee's gross salary is £54000 and the annual salary sacrifice for the car is £6000 (£500*12). £4000 of the sacrifice is in the 40% tax band and £2000 of it is in the 20% band. Am I right in assuming that the "savings" on the first £4000 are greater than the £2000 portion?

Seems to me that the annual payment for the vehicle needs to be above the £50k threshold to realise the best savings? So in this example the individual ideally wants to have a £56000 gross salary for this £6000 vehicle?

I think (if the above is correct) that these schemes are often slightly missold to people with stuff like "£300 per month for a 40% tax payer", but unless your salary is far enough into the 40% band you won't get it for that net cost on every month?

Seems to me that the annual payment for the vehicle needs to be above the £50k threshold to realise the best savings? So in this example the individual ideally wants to have a £56000 gross salary for this £6000 vehicle?

I think (if the above is correct) that these schemes are often slightly missold to people with stuff like "£300 per month for a 40% tax payer", but unless your salary is far enough into the 40% band you won't get it for that net cost on every month?

Edited by F20CN16 on Friday 27th November 08:51

F20CN16 said:

Wondering if someone can answer my question please, as I can't find this on online examples. In this scenario let's say the employee's gross salary is £54000 and the annual salary sacrifice for the car is £6000 (£500*12). £4000 of the sacrifice is in the 40% tax band and £2000 of it is in the 20% band. Am I right in assuming that the "savings" on the first £4000 are greater than the £2000 portion?

Seems to me that the annual payment for the vehicle needs to be above the £50k threshold to realise the best savings? So in this example the individual ideally wants to have a £56000 gross salary for this £6000 vehicle?

I think (if the above is correct) that these schemes are often slightly missold to people with stuff like "£300 per month for a 40% tax payer", but unless your salary is far enough into the 40% band you won't get it for that net cost on every month?

Its probably worse than that, Have a salary of £56k and pay into a pension and you knock that off too but your premise is otherwise rightSeems to me that the annual payment for the vehicle needs to be above the £50k threshold to realise the best savings? So in this example the individual ideally wants to have a £56000 gross salary for this £6000 vehicle?

I think (if the above is correct) that these schemes are often slightly missold to people with stuff like "£300 per month for a 40% tax payer", but unless your salary is far enough into the 40% band you won't get it for that net cost on every month?

Edited by F20CN16 on Friday 27th November 08:51

Sales people like to make figures look attractive, hence company owners keep being told you can write the value of an EV off in the first year, which you can, but then you pay a chunk of it back when you sell.

if you look back at the early BMW i8 stories when it came out as it was one of the first interesting cars to have the option, people were saying how the tax man was paying for half of it. Only they weren't in the fullness of time.

SWoll said:

The assumption there is that the entire cost of the annual lease is covered under the 40% portion of salary yes, so as you say for a £500 a month lease best savings would be at £56k or above as that £6k would only be worth £300 or so in salary.

Heres Johnny said:

Its probably worse than that, Have a salary of £56k and pay into a pension and you knock that off too but your premise is otherwise right

Sales people like to make figures look attractive, hence company owners keep being told you can write the value of an EV off in the first year, which you can, but then you pay a chunk of it back when you sell.

if you look back at the early BMW i8 stories when it came out as it was one of the first interesting cars to have the option, people were saying how the tax man was paying for half of it. Only they weren't in the fullness of time.

Thanks for confimring guys. I left pensions out to keep it simple, but as you say it is important that all salary sacrifices keep gross above £50k to take advantage. I think the wool has been pulled over a few eyes!Sales people like to make figures look attractive, hence company owners keep being told you can write the value of an EV off in the first year, which you can, but then you pay a chunk of it back when you sell.

if you look back at the early BMW i8 stories when it came out as it was one of the first interesting cars to have the option, people were saying how the tax man was paying for half of it. Only they weren't in the fullness of time.

F20CN16 said:

SWoll said:

The assumption there is that the entire cost of the annual lease is covered under the 40% portion of salary yes, so as you say for a £500 a month lease best savings would be at £56k or above as that £6k would only be worth £300 or so in salary.

Heres Johnny said:

Its probably worse than that, Have a salary of £56k and pay into a pension and you knock that off too but your premise is otherwise right

Sales people like to make figures look attractive, hence company owners keep being told you can write the value of an EV off in the first year, which you can, but then you pay a chunk of it back when you sell.

if you look back at the early BMW i8 stories when it came out as it was one of the first interesting cars to have the option, people were saying how the tax man was paying for half of it. Only they weren't in the fullness of time.

Thanks for confirming guys. I left pensions out to keep it simple, but as you say it is important that all salary sacrifices keep gross above £50k to take advantage. I think the wool has been pulled over a few eyes!Sales people like to make figures look attractive, hence company owners keep being told you can write the value of an EV off in the first year, which you can, but then you pay a chunk of it back when you sell.

if you look back at the early BMW i8 stories when it came out as it was one of the first interesting cars to have the option, people were saying how the tax man was paying for half of it. Only they weren't in the fullness of time.

Certainly not as simple as it first appears, as I found out earlier in the thread.

SWoll said:

F20CN16 said:

SWoll said:

The assumption there is that the entire cost of the annual lease is covered under the 40% portion of salary yes, so as you say for a £500 a month lease best savings would be at £56k or above as that £6k would only be worth £300 or so in salary.

Heres Johnny said:

Its probably worse than that, Have a salary of £56k and pay into a pension and you knock that off too but your premise is otherwise right

Sales people like to make figures look attractive, hence company owners keep being told you can write the value of an EV off in the first year, which you can, but then you pay a chunk of it back when you sell.

if you look back at the early BMW i8 stories when it came out as it was one of the first interesting cars to have the option, people were saying how the tax man was paying for half of it. Only they weren't in the fullness of time.

Thanks for confirming guys. I left pensions out to keep it simple, but as you say it is important that all salary sacrifices keep gross above £50k to take advantage. I think the wool has been pulled over a few eyes!Sales people like to make figures look attractive, hence company owners keep being told you can write the value of an EV off in the first year, which you can, but then you pay a chunk of it back when you sell.

if you look back at the early BMW i8 stories when it came out as it was one of the first interesting cars to have the option, people were saying how the tax man was paying for half of it. Only they weren't in the fullness of time.

Certainly not as simple as it first appears, as I found out earlier in the thread.

It seems the companies that run company car fleets as a service know what they're doing and if you've nowhere else to go they'll be pricing accordingly, so while you may be able to see a Tesla Model 3 for say £500 a month as a company lease, whether your company will offer you it something at that rate is another matter and they may well be asking for say £600 which claws away some of the benefit. My last company car was fully serviced, tyres, insured for any driver and unlimited miles and the all up cost was something £1400 a month for what was basically a 70k car, the X5 was around a grand because they got mega discounts from BMW as they bought so many which they could pass on.

SWoll said:

Been a while since the last post on this but have been looking into it as start a new job in the next few weeks.

I've pulled the following from https://legacy.comcar.co.uk/taxtools/salarysacrifi... for a Tesla 3 Performance to replace the one we have currently through On.To that is costing £799 a month all in.

Does this look right to anyone with more knowledge in this area than I do at present? Suggests it will be costing approx £360 a month in salary reduction based on a lease cost of around £800 a month for the car so just checking I'm not missing something (aware of the affect SS will have on pension contributions).

How did you get on with this? I've just been told that we might now go salary sacrifice which changes my whole viewpoint on company cars again!!I've pulled the following from https://legacy.comcar.co.uk/taxtools/salarysacrifi... for a Tesla 3 Performance to replace the one we have currently through On.To that is costing £799 a month all in.

Does this look right to anyone with more knowledge in this area than I do at present? Suggests it will be costing approx £360 a month in salary reduction based on a lease cost of around £800 a month for the car so just checking I'm not missing something (aware of the affect SS will have on pension contributions).

jason61c said:

How did you get on with this? I've just been told that we might now go salary sacrifice which changes my whole viewpoint on company cars again!!

Blimey, a blast from the past.Didn't happen in the end, couldn't talk fleet into looking at it and have since moved on and joined the world of freelancers again.

The maths are still valid though, if your earnings hit the really punitive bands it's a no brainer.

Interesting thread.

A bog standard Taycan is coming out at £990pm for me. Frustratingly there's no option of any performance versions, but still tempting for an insured, maintained Porsche with 8k miles pa.

Picking up from a comment on the leasing thread, am I right in thinking there is no long term impact on pensions if you are on a defined contribution scheme? (i.e. average salary is calculated gross before deductions?).

A bog standard Taycan is coming out at £990pm for me. Frustratingly there's no option of any performance versions, but still tempting for an insured, maintained Porsche with 8k miles pa.

Picking up from a comment on the leasing thread, am I right in thinking there is no long term impact on pensions if you are on a defined contribution scheme? (i.e. average salary is calculated gross before deductions?).

SWoll said:

Blimey, a blast from the past.

Didn't happen in the end, couldn't talk fleet into looking at it and have since moved on and joined the world of freelancers again.

The maths are still valid though, if your earnings hit the really punitive bands it's a no brainer.

yeah, sorry about the blast!Didn't happen in the end, couldn't talk fleet into looking at it and have since moved on and joined the world of freelancers again.

The maths are still valid though, if your earnings hit the really punitive bands it's a no brainer.

trying to work it out is difficult. Earlier today I was polestar or model 3 long range(for range only!). However now, it could be something much 'nicer'

Sargeant Orange said:

Interesting thread.

A bog standard Taycan is coming out at £990pm for me. Frustratingly there's no option of any performance versions, but still tempting for an insured, maintained Porsche with 8k miles pa.

Picking up from a comment on the leasing thread, am I right in thinking there is no long term impact on pensions if you are on a defined contribution scheme? (i.e. average salary is calculated gross before deductions?).

have you found any decent websites that show what it costs you? also with the option of putting pension contribs in?A bog standard Taycan is coming out at £990pm for me. Frustratingly there's no option of any performance versions, but still tempting for an insured, maintained Porsche with 8k miles pa.

Picking up from a comment on the leasing thread, am I right in thinking there is no long term impact on pensions if you are on a defined contribution scheme? (i.e. average salary is calculated gross before deductions?).

Gassing Station | EV and Alternative Fuels | Top of Page | What's New | My Stuff