NHS lease scheme

Discussion

alfaeejit said:

Lovely car, but dont need one that big for commuting, and range wont suit, i am after 200+ real world as have a 60mile round trip + occasional and would like to run it 20-80% charging every couple of days. The Model 3 ist perfect as I like a hatchback/estate practicality (Kids + MTB), but the performance is definitely a seller 😁How long have people waited for Payroll to sign off their order? Line manager sign off was almost immediate, but have been waiting around a week for payroll. I've been assured our car is secured, but ill believe that once it's gone into the order status!

Out of interest, we have gone with NHSfleetsolutions who clearly have some every attractive electric deals, but do Tusker have the same or similar deals at all?

Out of interest, we have gone with NHSfleetsolutions who clearly have some every attractive electric deals, but do Tusker have the same or similar deals at all?

Does anyone have recent experience of early termination of their lease?

I've just made initial contact with NHS fleet solutions to ask about the cost in my final year (used to be 1 months payment) and they said you can only terminate if theirs a significant lifestyle change e.g. Marriage, divorce, death of spouse etc.

I've replied back to them to say I'm looking to cancel due to now doing much higher business miles since starting the lease and want to avoid additional mileage charges, but I've got a feeling this won't meet their requirements for termination.

HMRC guidance says to exit a salary sacrifice there has to be a lifestyle change such as the above mentioned, but doesn't say only these are adequate for early termination.

Any advice or experience?

I've just made initial contact with NHS fleet solutions to ask about the cost in my final year (used to be 1 months payment) and they said you can only terminate if theirs a significant lifestyle change e.g. Marriage, divorce, death of spouse etc.

I've replied back to them to say I'm looking to cancel due to now doing much higher business miles since starting the lease and want to avoid additional mileage charges, but I've got a feeling this won't meet their requirements for termination.

HMRC guidance says to exit a salary sacrifice there has to be a lifestyle change such as the above mentioned, but doesn't say only these are adequate for early termination.

Any advice or experience?

Mustache said:

Someone on the previous thread asked me to explain how an NHS lease reduces your pension, with full figures, so I'lll have a go.

The 2015 pension scheme, which anyone under around 57 years old is now on, is a career average based scheme. It is calculated by dividing your annual salary after each financial year by 54, and that amount goes into a 'pot'. You will have extra pots after every subsequent financial year. Each pot is revalued every year, at 1.5% above inflation, so if inflation was 2% in the last year, all the pots are revalued by 3.5%. Once you retire, all the pots are added up, and the total is paid to you annually.

As an example, someone earning 40K throughout their career of 10 years would gat the following pension (ignoring any future inflation):

Year 1: 40,000/54 = £740 compounded by 1.5% for 9 years = £846.11

Year 2: 40,000/54 = £750 compounded by 1.5% for 8 years = £833.60

Year 3: 40,000/54 = £750 compounded by 1.5% for 7 years = £821.29

Year 4: 40,000/54 = £750 compounded by 1.5% for 6 years = £809.15

Year 5: 40,000/54 = £750 compounded by 1.5% for 5 years = £797.19

Year 6: 40,000/54 = £750 compounded by 1.5% for 4 years = £785.41

Year 7: 40,000/54 = £750 compounded by 1.5% for 3 years = £773.80

Year 8: 40,000/54 = £750 compounded by 1.5% for 2 years = £762.37

Year 9: 40,000/54 = £750 compounded by 1.5% for 1 year = £751.10

Year 10: 40,000/54 = £750 compounded by 1.5% for 0 years = £740

Once you add the 10 pots up, it gives an annual retirement income of £7920.02

If someone takes out an NHS car lease of £300/month, that means their salary drops by £3600 to £36,400. So the pot that year will drop from £740 to £650, a £90 decrease, and will be decreased by the length of the lease e.g. 3 year lease = £90x3 = £180 less a year in NHS pension. If a person has 30 years left in work before retiring, that £180 would have been rebalanced every year by at lease 1.5%. That gives £240 less a year.

£240 doesn't sound that much, but that's £4800 on a 20 year retirement, and if you have multiple leases if can add up to much more than that.

It MAY be worth it for higher rate tax payers to take put an NHS lease, but I wouldn't do it as a 20% tax payer myself.

Can anyone explain why a 2 year salary sacrifice, (eg the e tron lease deal) ie 2 Reduced “pots” seems to affect the pot in every subsequent year until retirement? If say you are 35 and plan to retire at 65 (30 more annual contributions)The 2015 pension scheme, which anyone under around 57 years old is now on, is a career average based scheme. It is calculated by dividing your annual salary after each financial year by 54, and that amount goes into a 'pot'. You will have extra pots after every subsequent financial year. Each pot is revalued every year, at 1.5% above inflation, so if inflation was 2% in the last year, all the pots are revalued by 3.5%. Once you retire, all the pots are added up, and the total is paid to you annually.

As an example, someone earning 40K throughout their career of 10 years would gat the following pension (ignoring any future inflation):

Year 1: 40,000/54 = £740 compounded by 1.5% for 9 years = £846.11

Year 2: 40,000/54 = £750 compounded by 1.5% for 8 years = £833.60

Year 3: 40,000/54 = £750 compounded by 1.5% for 7 years = £821.29

Year 4: 40,000/54 = £750 compounded by 1.5% for 6 years = £809.15

Year 5: 40,000/54 = £750 compounded by 1.5% for 5 years = £797.19

Year 6: 40,000/54 = £750 compounded by 1.5% for 4 years = £785.41

Year 7: 40,000/54 = £750 compounded by 1.5% for 3 years = £773.80

Year 8: 40,000/54 = £750 compounded by 1.5% for 2 years = £762.37

Year 9: 40,000/54 = £750 compounded by 1.5% for 1 year = £751.10

Year 10: 40,000/54 = £750 compounded by 1.5% for 0 years = £740

Once you add the 10 pots up, it gives an annual retirement income of £7920.02

If someone takes out an NHS car lease of £300/month, that means their salary drops by £3600 to £36,400. So the pot that year will drop from £740 to £650, a £90 decrease, and will be decreased by the length of the lease e.g. 3 year lease = £90x3 = £180 less a year in NHS pension. If a person has 30 years left in work before retiring, that £180 would have been rebalanced every year by at lease 1.5%. That gives £240 less a year.

£240 doesn't sound that much, but that's £4800 on a 20 year retirement, and if you have multiple leases if can add up to much more than that.

It MAY be worth it for higher rate tax payers to take put an NHS lease, but I wouldn't do it as a 20% tax payer myself.

Is each years contribution not a new separate calculation, ie based on earnings that year, as wages normally go up and things like overtime etc will give a new average each year. Surely just the “pot” for the 2 years of the lease deal will be slightly less and when pension pay out time comes all of the pots will be added up and an average yearly pension payment worked out from that. I just dont understand how and why all your future years of pension contributions seem to be punished if you like for having a 2 year lease.

burt2000 said:

Can anyone explain why a 2 year salary sacrifice, (eg the e tron lease deal) ie 2 Reduced “pots” seems to affect the pot in every subsequent year until retirement? If say you are 35 and plan to retire at 65 (30 more annual contributions)

Is each years contribution not a new separate calculation, ie based on earnings that year, as wages normally go up and things like overtime etc will give a new average each year. Surely just the “pot” for the 2 years of the lease deal will be slightly less and when pension pay out time comes all of the pots will be added up and an average yearly pension payment worked out from that. I just dont understand how and why all your future years of pension contributions seem to be punished if you like for having a 2 year lease.

I'm presuming (so don't hold me to this) that the above posts are referring to the case of you having a Salary Sacrifice car for 10 / 20 years etc. The pension pot is calculated yearly, so once you drop out of the scheme and your gross pay returns to its normal amount, then the pension payment will go back to normal.Is each years contribution not a new separate calculation, ie based on earnings that year, as wages normally go up and things like overtime etc will give a new average each year. Surely just the “pot” for the 2 years of the lease deal will be slightly less and when pension pay out time comes all of the pots will be added up and an average yearly pension payment worked out from that. I just dont understand how and why all your future years of pension contributions seem to be punished if you like for having a 2 year lease.

Please, someone, correct me if I'm wrong.

Edited by The Mp on Thursday 5th March 18:33

I think the simplest way to think about this is to look at the gross deduction (sacrifice). Effectively this reduced salary is your pensionable pay for the duration of the time you are in the scheme. So for example if you are a band 7 and the effect if the sacrifice puts you into band 6 numbers, you will be contributing as a band 6 and the annual increase to your mythical pension pot will be as a band 6.

I dont' suppose this would make much difference if you are in the scheme for a couple of years, but over 20 years or so it could have a fair impact - although its difficult to fathom exactly - keeping tabs on your TRS pension estimate each year may help you map the change

I dont' suppose this would make much difference if you are in the scheme for a couple of years, but over 20 years or so it could have a fair impact - although its difficult to fathom exactly - keeping tabs on your TRS pension estimate each year may help you map the change

Greywall said:

Looks good! Must admit, I was put off initially by the pension impact but looking back, I'd take a small hit for 2/3 years, considering insurance is included too. Enjoy your Tesla!

it's not mine mate, a colleagues. He's 28 and has taken this on a 2 year lease, last of his worries is pension I guess.Looking at getting an Ipace on the NHS lease scheme. They're popping up all over the work carpark since the change in BIK rules.

A silly question, how does the tyre change work? The reason I ask is the standard 18" wheels look pretty terrible and I'd like to change them but I don't want to do that if it means I can't get the tyres replaced as part of the lease deal anymore.

If its just a polling up at Kwikfit and giving the lease company details I suspect they won't know or care what size tyres are fitted.

A silly question, how does the tyre change work? The reason I ask is the standard 18" wheels look pretty terrible and I'd like to change them but I don't want to do that if it means I can't get the tyres replaced as part of the lease deal anymore.

If its just a polling up at Kwikfit and giving the lease company details I suspect they won't know or care what size tyres are fitted.

Minstadave said:

Looking at getting an Ipace on the NHS lease scheme. They're popping up all over the work carpark since the change in BIK rules.

A silly question, how does the tyre change work? The reason I ask is the standard 18" wheels look pretty terrible and I'd like to change them but I don't want to do that if it means I can't get the tyres replaced as part of the lease deal anymore.

If its just a polling up at Kwikfit and giving the lease company details I suspect they won't know or care what size tyres are fitted.

From previous NHS leases you tip up at Kwik Fit and the fit like for like. I think they require some form of authorisation from the lease provider (i.e NHS fleet solutions, tusker, ogilvie etc). A silly question, how does the tyre change work? The reason I ask is the standard 18" wheels look pretty terrible and I'd like to change them but I don't want to do that if it means I can't get the tyres replaced as part of the lease deal anymore.

If its just a polling up at Kwikfit and giving the lease company details I suspect they won't know or care what size tyres are fitted.

Surely the Audi etron is a better car to have?

burt2000 said:

Mustache said:

Someone on the previous thread asked me to explain how an NHS lease reduces your pension, with full figures, so I'lll have a go.

The 2015 pension scheme, which anyone under around 57 years old is now on, is a career average based scheme. It is calculated by dividing your annual salary after each financial year by 54, and that amount goes into a 'pot'. You will have extra pots after every subsequent financial year. Each pot is revalued every year, at 1.5% above inflation, so if inflation was 2% in the last year, all the pots are revalued by 3.5%. Once you retire, all the pots are added up, and the total is paid to you annually.

As an example, someone earning 40K throughout their career of 10 years would gat the following pension (ignoring any future inflation):

Year 1: 40,000/54 = £740 compounded by 1.5% for 9 years = £846.11

Year 2: 40,000/54 = £750 compounded by 1.5% for 8 years = £833.60

Year 3: 40,000/54 = £750 compounded by 1.5% for 7 years = £821.29

Year 4: 40,000/54 = £750 compounded by 1.5% for 6 years = £809.15

Year 5: 40,000/54 = £750 compounded by 1.5% for 5 years = £797.19

Year 6: 40,000/54 = £750 compounded by 1.5% for 4 years = £785.41

Year 7: 40,000/54 = £750 compounded by 1.5% for 3 years = £773.80

Year 8: 40,000/54 = £750 compounded by 1.5% for 2 years = £762.37

Year 9: 40,000/54 = £750 compounded by 1.5% for 1 year = £751.10

Year 10: 40,000/54 = £750 compounded by 1.5% for 0 years = £740

Once you add the 10 pots up, it gives an annual retirement income of £7920.02

If someone takes out an NHS car lease of £300/month, that means their salary drops by £3600 to £36,400. So the pot that year will drop from £740 to £650, a £90 decrease, and will be decreased by the length of the lease e.g. 3 year lease = £90x3 = £180 less a year in NHS pension. If a person has 30 years left in work before retiring, that £180 would have been rebalanced every year by at lease 1.5%. That gives £240 less a year.

£240 doesn't sound that much, but that's £4800 on a 20 year retirement, and if you have multiple leases if can add up to much more than that.

It MAY be worth it for higher rate tax payers to take put an NHS lease, but I wouldn't do it as a 20% tax payer myself.

Can anyone explain why a 2 year salary sacrifice, (eg the e tron lease deal) ie 2 Reduced “pots” seems to affect the pot in every subsequent year until retirement? If say you are 35 and plan to retire at 65 (30 more annual contributions)The 2015 pension scheme, which anyone under around 57 years old is now on, is a career average based scheme. It is calculated by dividing your annual salary after each financial year by 54, and that amount goes into a 'pot'. You will have extra pots after every subsequent financial year. Each pot is revalued every year, at 1.5% above inflation, so if inflation was 2% in the last year, all the pots are revalued by 3.5%. Once you retire, all the pots are added up, and the total is paid to you annually.

As an example, someone earning 40K throughout their career of 10 years would gat the following pension (ignoring any future inflation):

Year 1: 40,000/54 = £740 compounded by 1.5% for 9 years = £846.11

Year 2: 40,000/54 = £750 compounded by 1.5% for 8 years = £833.60

Year 3: 40,000/54 = £750 compounded by 1.5% for 7 years = £821.29

Year 4: 40,000/54 = £750 compounded by 1.5% for 6 years = £809.15

Year 5: 40,000/54 = £750 compounded by 1.5% for 5 years = £797.19

Year 6: 40,000/54 = £750 compounded by 1.5% for 4 years = £785.41

Year 7: 40,000/54 = £750 compounded by 1.5% for 3 years = £773.80

Year 8: 40,000/54 = £750 compounded by 1.5% for 2 years = £762.37

Year 9: 40,000/54 = £750 compounded by 1.5% for 1 year = £751.10

Year 10: 40,000/54 = £750 compounded by 1.5% for 0 years = £740

Once you add the 10 pots up, it gives an annual retirement income of £7920.02

If someone takes out an NHS car lease of £300/month, that means their salary drops by £3600 to £36,400. So the pot that year will drop from £740 to £650, a £90 decrease, and will be decreased by the length of the lease e.g. 3 year lease = £90x3 = £180 less a year in NHS pension. If a person has 30 years left in work before retiring, that £180 would have been rebalanced every year by at lease 1.5%. That gives £240 less a year.

£240 doesn't sound that much, but that's £4800 on a 20 year retirement, and if you have multiple leases if can add up to much more than that.

It MAY be worth it for higher rate tax payers to take put an NHS lease, but I wouldn't do it as a 20% tax payer myself.

Is each years contribution not a new separate calculation, ie based on earnings that year, as wages normally go up and things like overtime etc will give a new average each year. Surely just the “pot” for the 2 years of the lease deal will be slightly less and when pension pay out time comes all of the pots will be added up and an average yearly pension payment worked out from that. I just dont understand how and why all your future years of pension contributions seem to be punished if you like for having a 2 year lease.

pavarotti1980 said:

Minstadave said:

Looking at getting an Ipace on the NHS lease scheme. They're popping up all over the work carpark since the change in BIK rules.

A silly question, how does the tyre change work? The reason I ask is the standard 18" wheels look pretty terrible and I'd like to change them but I don't want to do that if it means I can't get the tyres replaced as part of the lease deal anymore.

If its just a polling up at Kwikfit and giving the lease company details I suspect they won't know or care what size tyres are fitted.

From previous NHS leases you tip up at Kwik Fit and the fit like for like. I think they require some form of authorisation from the lease provider (i.e NHS fleet solutions, tusker, ogilvie etc). A silly question, how does the tyre change work? The reason I ask is the standard 18" wheels look pretty terrible and I'd like to change them but I don't want to do that if it means I can't get the tyres replaced as part of the lease deal anymore.

If its just a polling up at Kwikfit and giving the lease company details I suspect they won't know or care what size tyres are fitted.

Surely the Audi etron is a better car to have?

There wasn't much in it at the end of the but the range of the Etron meant it'd be a pain at times. The extra 40 or so miles the IPace manages made it a more realistic proposition.

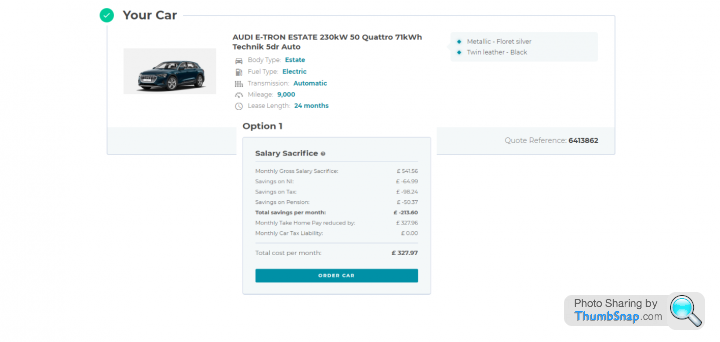

Does anyone know what sort of impact this will have on your tax code? I am trying to work out the monthly take home we will have but it’s difficult when you don’t know what your new tax code is going to be.

It will be a 9094.97 sacrifice on a 30615 salary, meaning that gross wage is now, 21520.03. Our current tax code is 1285L, does anyone know what this would change too?

It will be a 9094.97 sacrifice on a 30615 salary, meaning that gross wage is now, 21520.03. Our current tax code is 1285L, does anyone know what this would change too?

CheesecakeRunner said:

ADGAH said:

Does anyone know what sort of impact this will have on your tax code? I am trying to work out the monthly take home we will have but it’s difficult when you don’t know what your new tax code is going to be.

It will be a 9094.97 sacrifice on a 30615 salary, meaning that gross wage is now, 21520.03. Our current tax code is 1285L, does anyone know what this would change too?

What's the BIK charge for it? Simplistic way is to subtract that from the personal allowance of 12850, and assuming it's above 0, divide the result by 10 and stick the L back on.It will be a 9094.97 sacrifice on a 30615 salary, meaning that gross wage is now, 21520.03. Our current tax code is 1285L, does anyone know what this would change too?

E.g BIK of 8000. 12850 - 8000 = 4850. So 485L code.

If the result is a negative number it gets a bit more complex, when that happened to me I got a T code.

Gassing Station | Car Buying | Top of Page | What's New | My Stuff